Emerging Markets

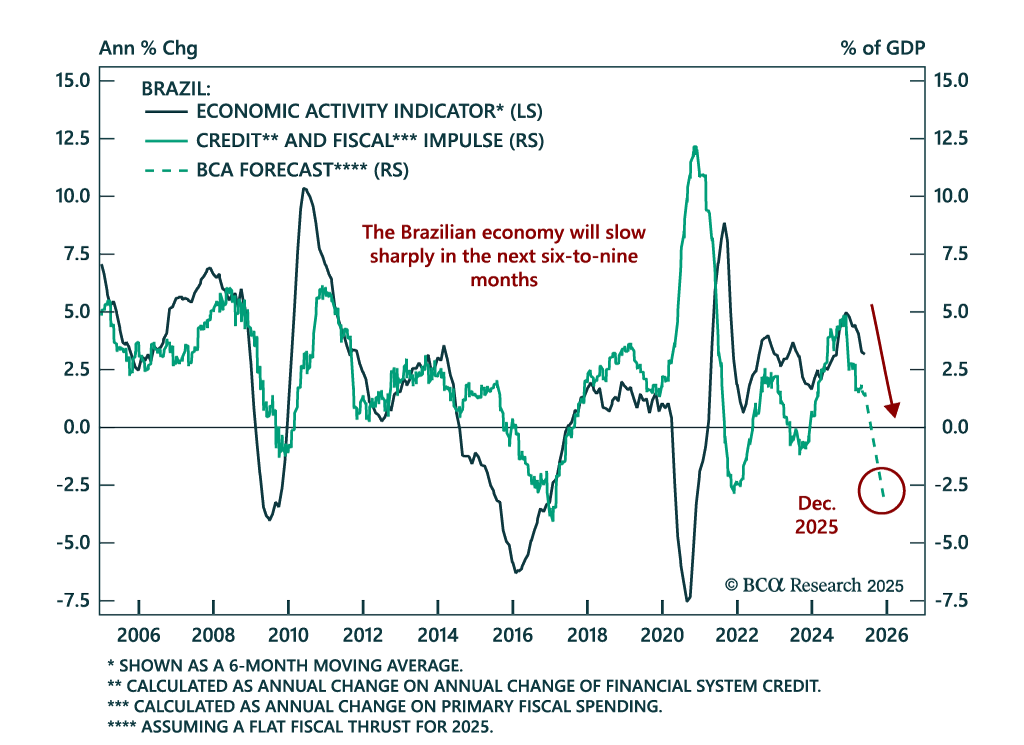

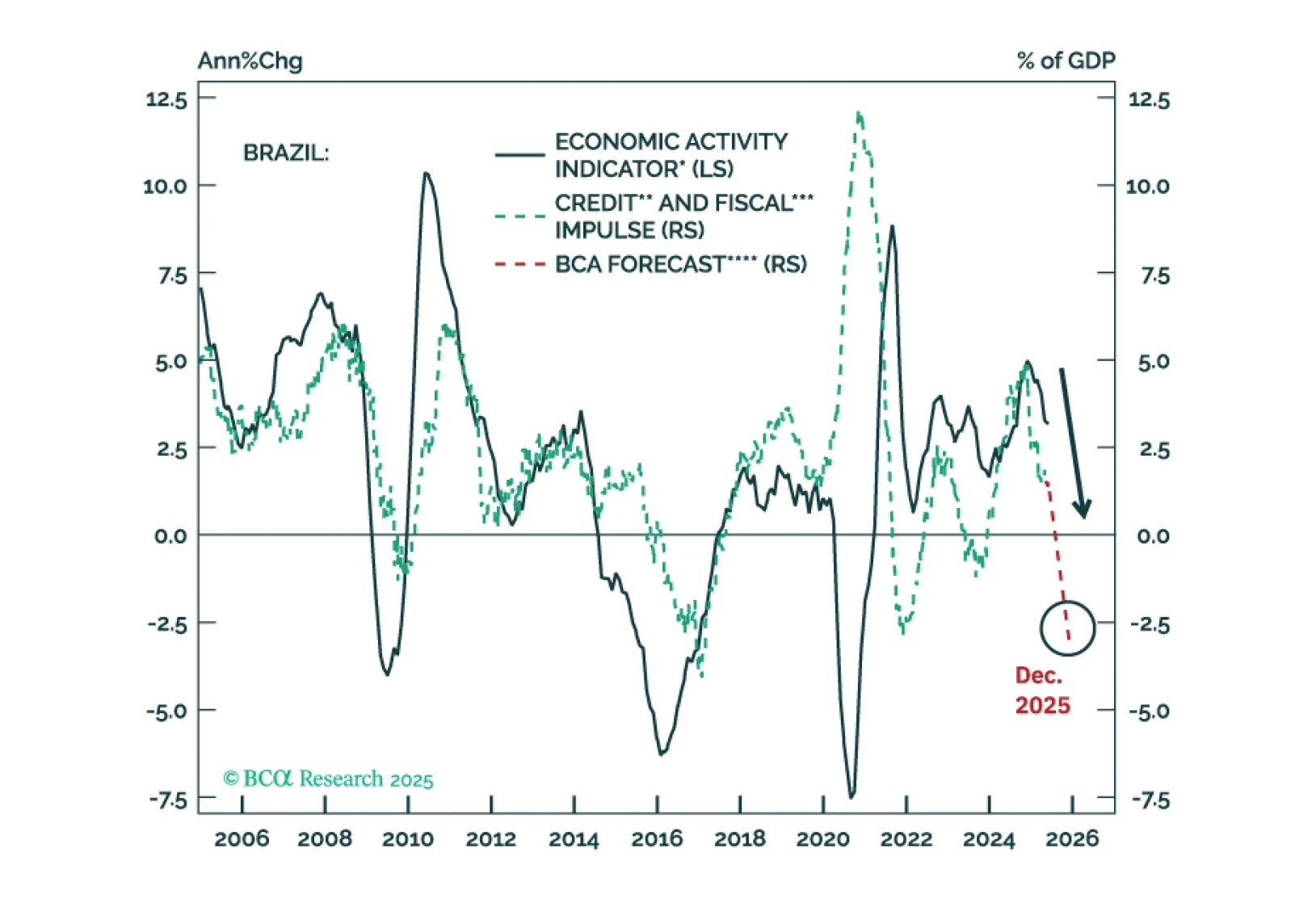

A potential right-wing government in 2027 will not stabilize the trajectory of the public debt-to-GDP ratio. Unsustainable public debt, a large current account deficit, and a sharp growth slowdown will lead Brazilian markets to underperform EM. Yet, to benefit from a quickly decelerating economy, we recommend receiving 2-year swap rates.

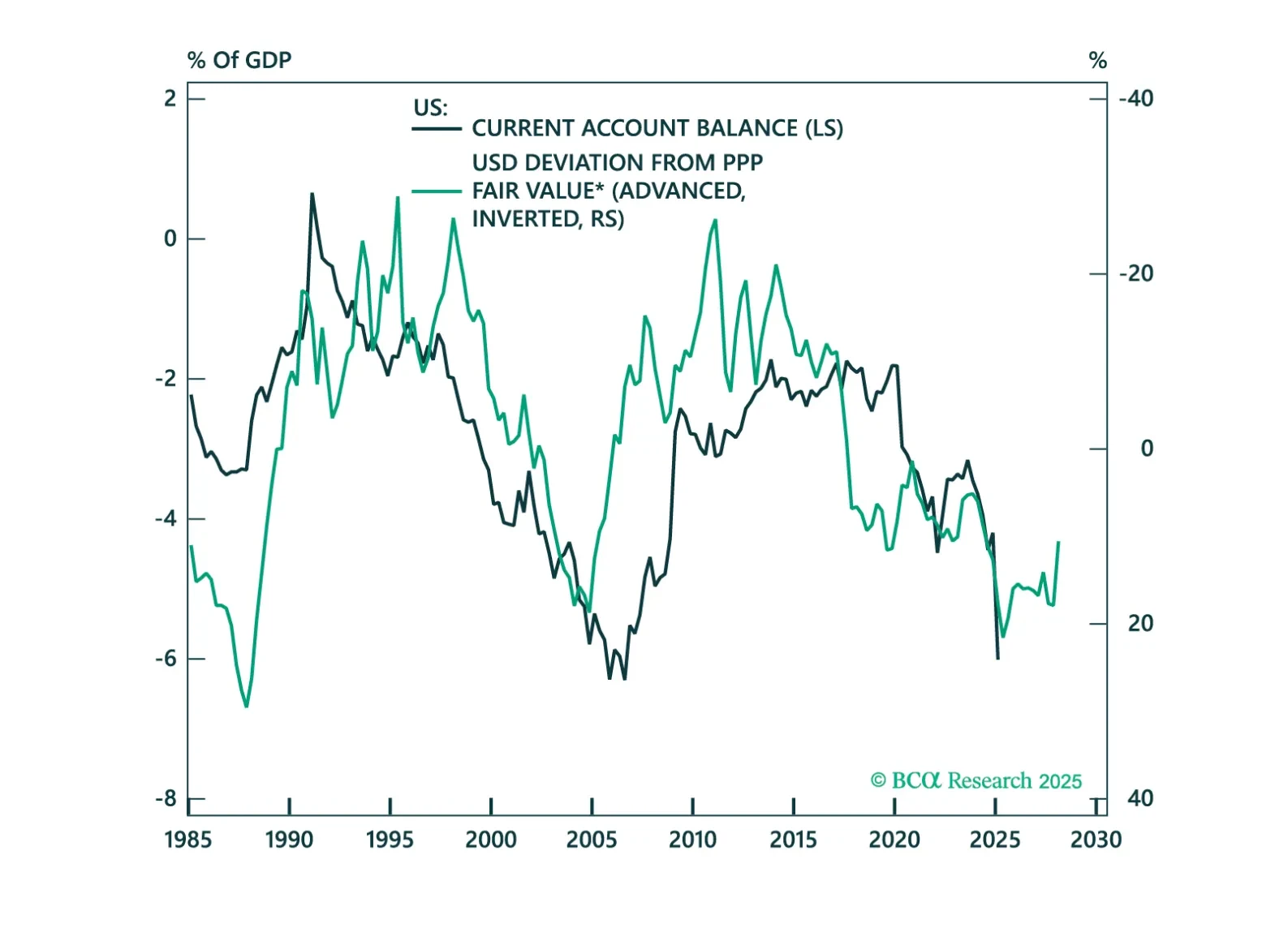

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.

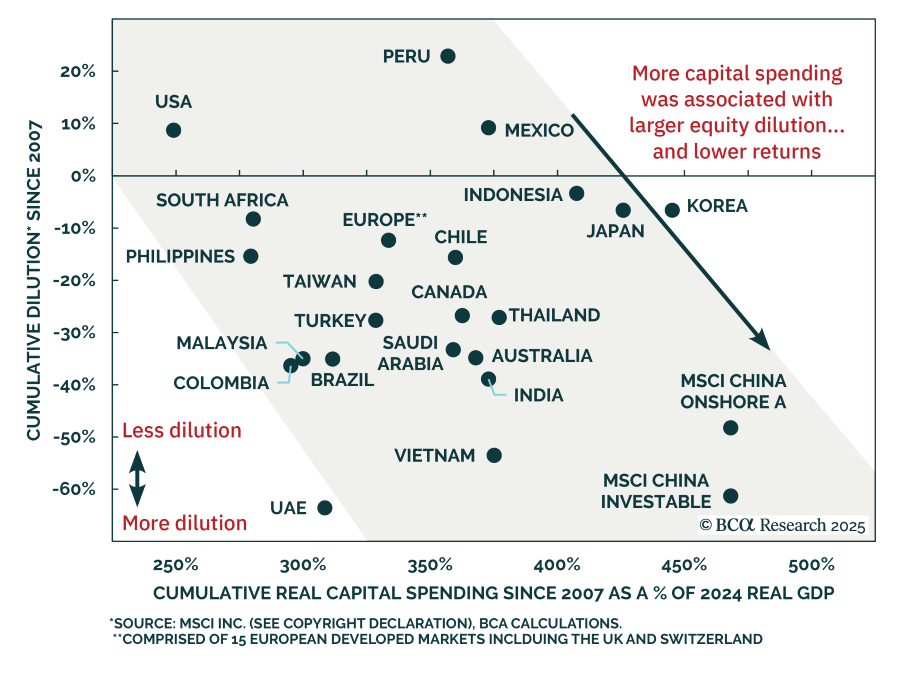

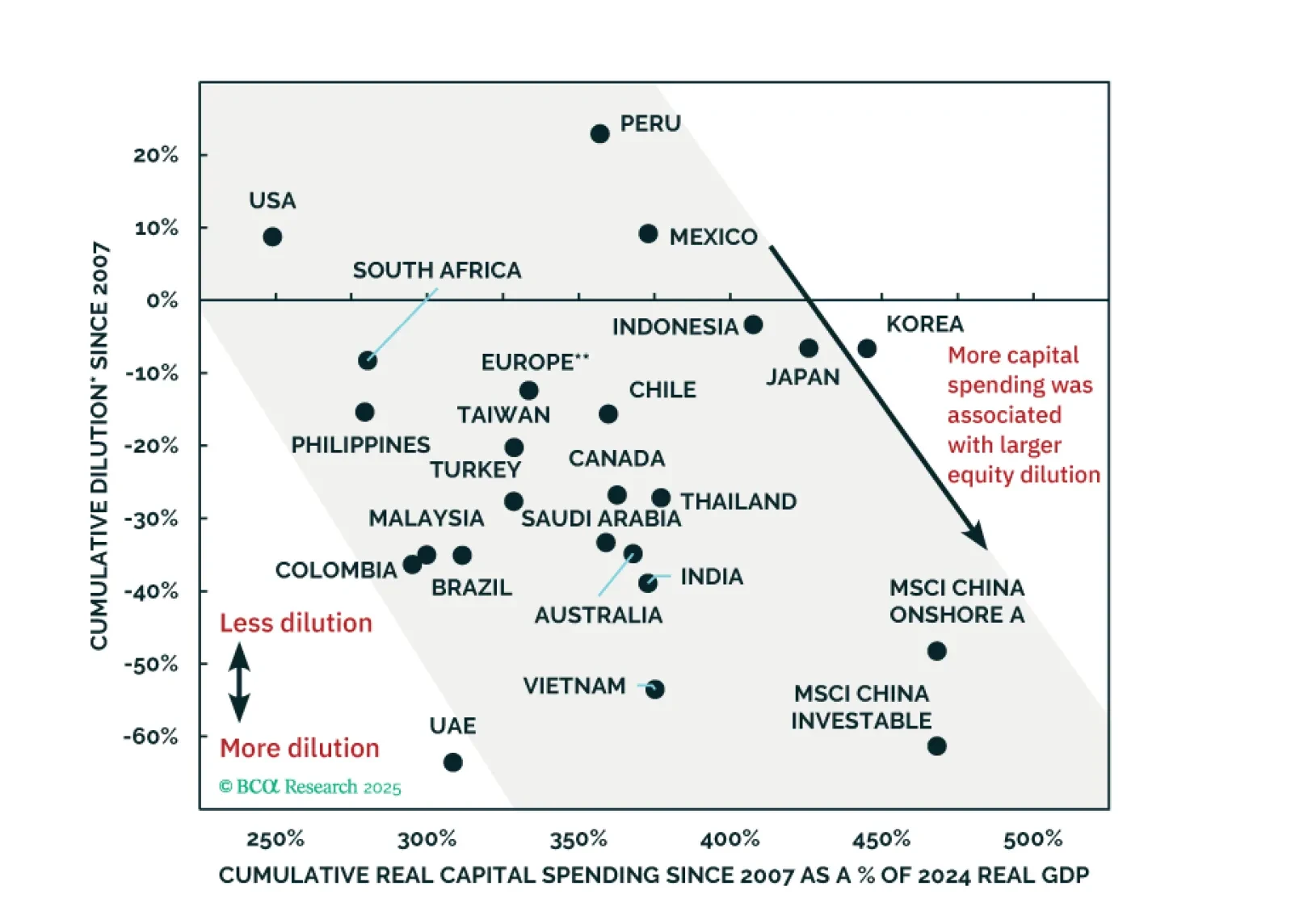

Economic growth and rapid expansions do not always translate into higher EPS and shareholder returns. One of the key reasons is dilution. We offer a typology of dilution: (1) “offensive”, (2) “defensive”, (3) corporate governance-linked, and (4) idiosyncratic cases.