Emerging Markets

China's real GDP growth decelerated to 4.7% y/y in Q2, down from 5.3% in Q1 and below the consensus forecast of 5.1%. Domestic demand weakened, with retail sales growth sliding to 2% y/y in June, down from 3.7% in the previous month. Our China Strategists…

Subdued demand for credit among Chinese private-sector businesses and households persisted through June. The stock of outstanding bank loans grew by 8.3% year-on-year, marking the slowest pace since records began in 2003. Additionally, bond issuance from…

Since early 2023, the Philippine peso has depreciated by 8% versus the US dollar despite the country’s central bank pushing up real policy rates by 500 basis points. BCA’s Emerging Markets Strategy argues that raising policy rates has not helped the currency…

South African stocks, domestic bonds, and currency have all rallied since BCA’s Emerging Markets Strategy team upgraded South African assets last month following the formation of the new national unity government. The rally's persistence, however, will depend…

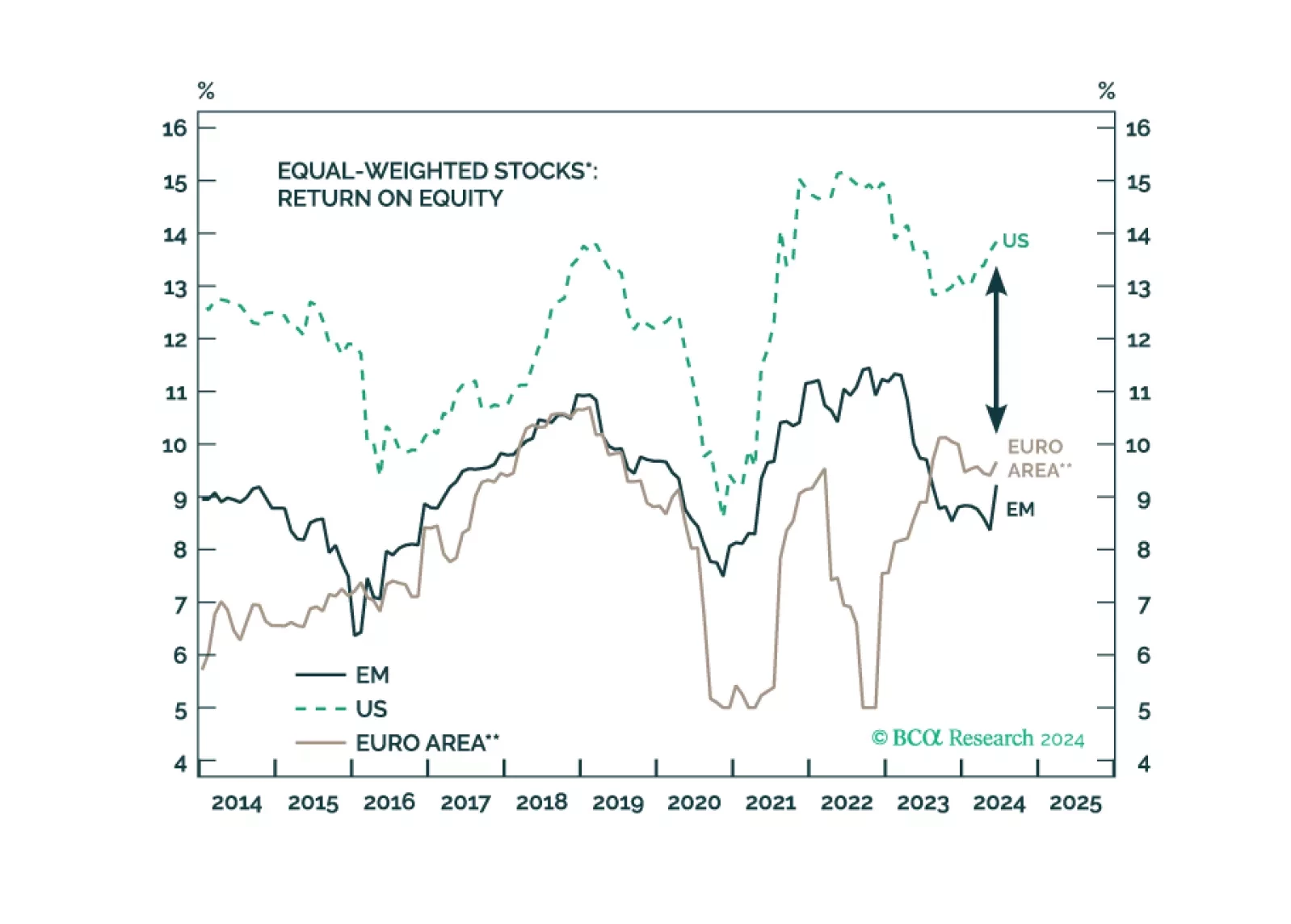

According to BCA Research’s Emerging Markets Strategy service, extremely disappointing corporate profit growth has been the main reason for EM's poor equity performance in absolute terms and massive underperformance relative to the US/DM. EM earnings per…

The failure of EM stock prices to rally over the past 13 years is rooted in their companies’ inability to grow their profits. Even though EM equities appear cheap based on their cyclically adjusted P/E ratio, there has been a regime change in EM corporate profitability. Therefore, the CAPE model should not be used to value EM stocks now.

As highlighted in Wednesday’s edition of BCA Live & Unfiltered, the Chinese economy and its financial markets face several daunting challenges. Its demographic outlook is unfavorable, with a low birthrate stifling population growth; the grim math of…

Our colleagues from the Emerging Markets Strategy team argue that investors should brace for a significant correction in Indian stocks in the coming months. They posit that the pillar of Indian corporations' sustained profit growth — surging revenues — is…

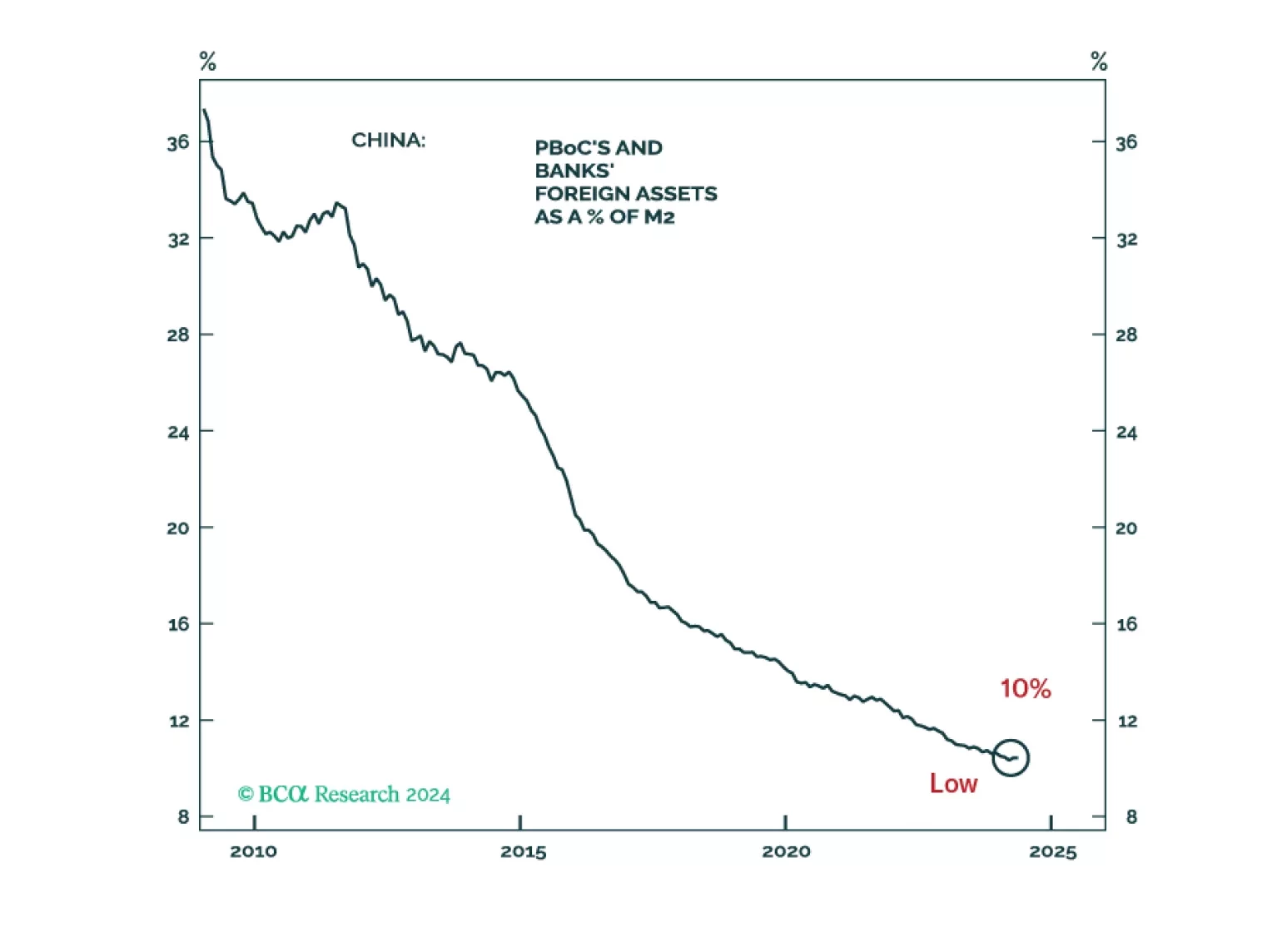

The Chinese currency has been under considerable depreciation pressure due to capital outflows. Additionally, the economy is grappling with debt deflation and a balance sheet recession, conditions that typically call for lower interest rates and a weaker…

Is the RMB cheap or expensive? Based on trade accounts, the yuan is inexpensive, but the RMB is vulnerable due to capital outflows. Yet, Beijing will not resort to a rapid devaluation for now, and the option of floating the currency is improbable. The PBoC will allow a gradual depreciation of the yuan versus the dollar, say around 5%, in the next six months.