Emerging Markets

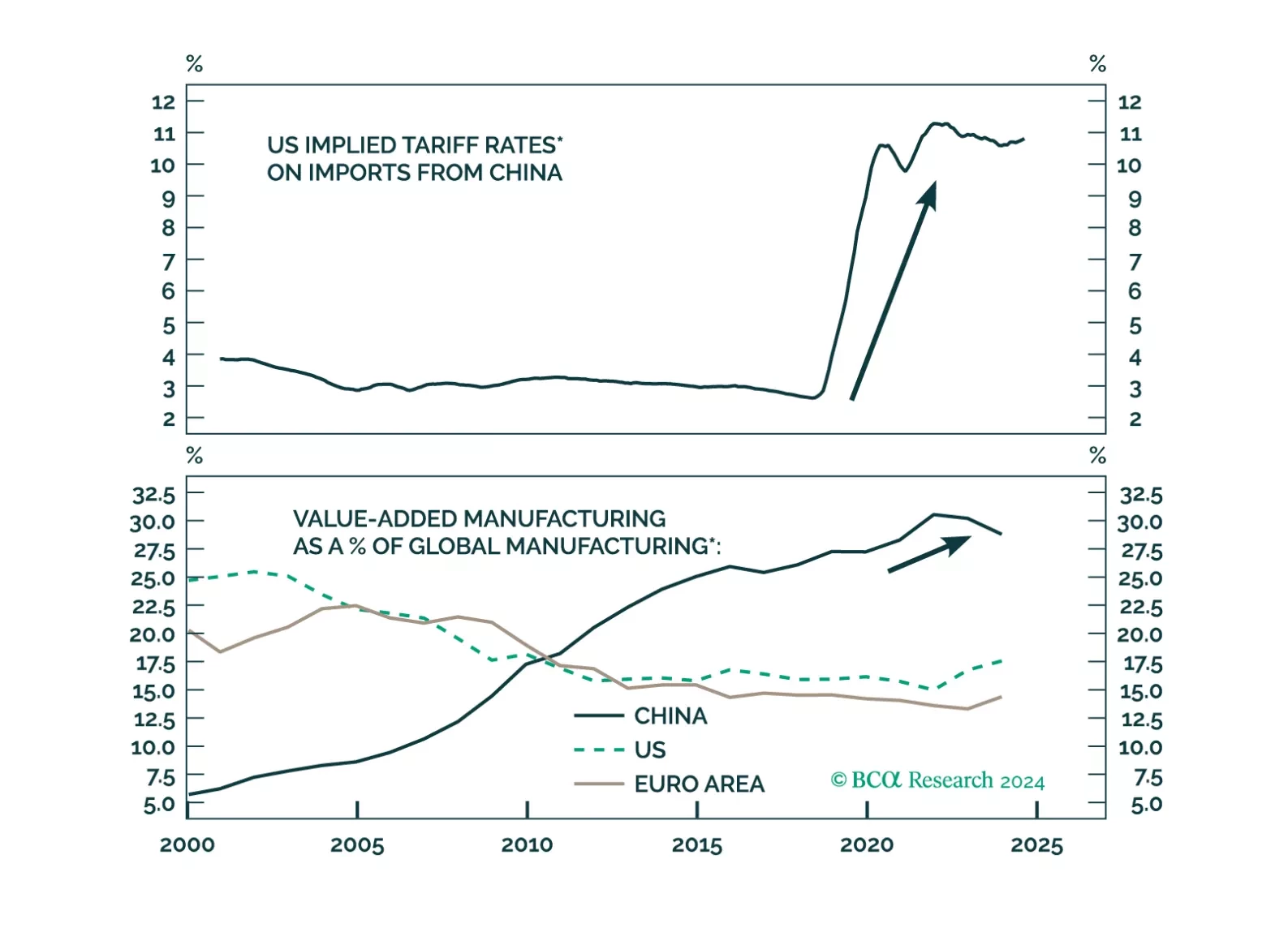

Trump's presidential re-election makes US tariff rate hikes on Chinese exports an imminent threat. Beijing has made extensive efforts to derisk the domestic economy and diversify trade away from the US. However, China is no better positioned today than it was in 2018 to withstand the impact of a renewed trade war.

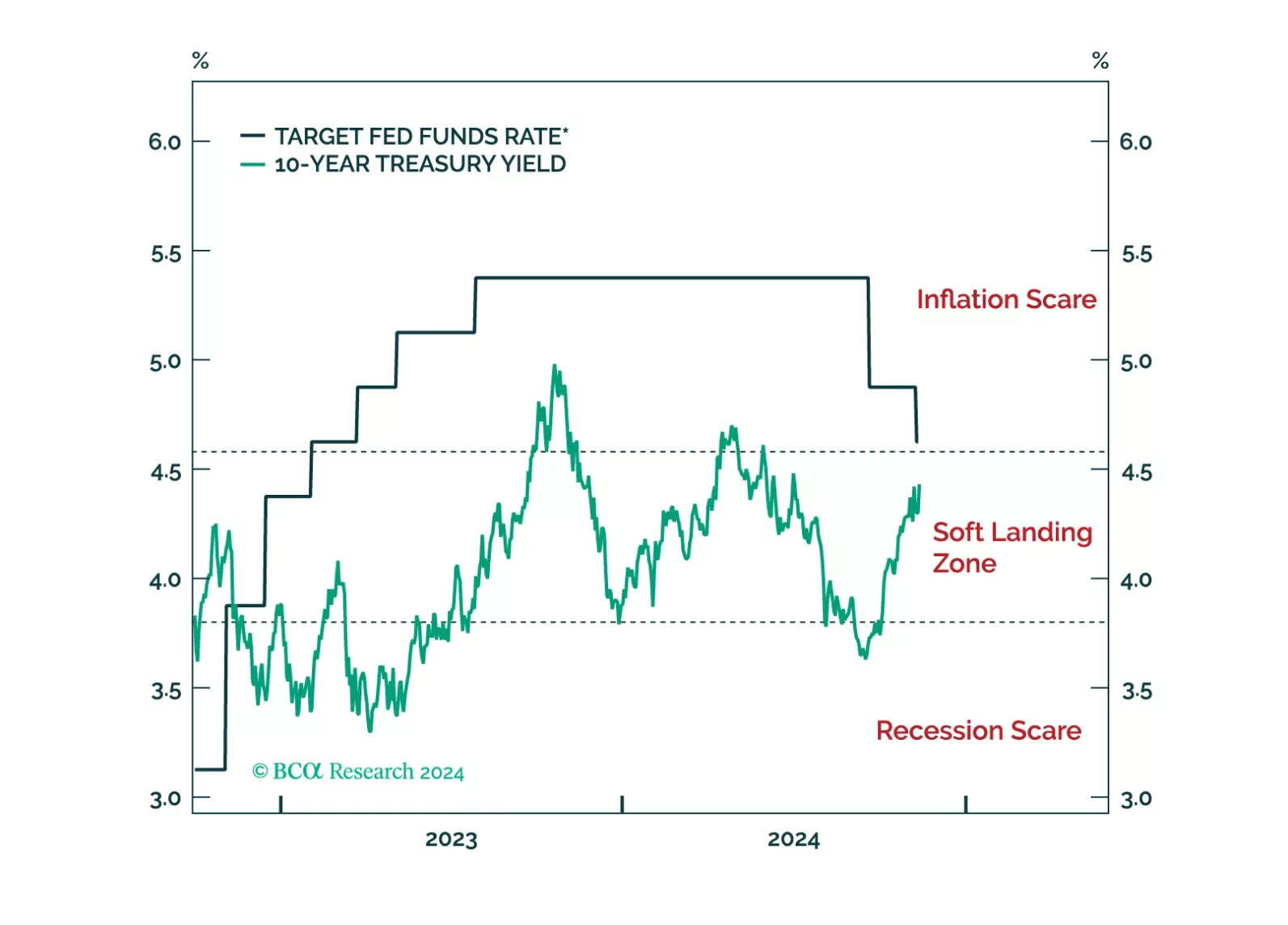

The month of November has brought us S&P 6,000! President Trump has won a “Red Sweep” (as we expected all year) and has ushered in a regime change in America. For now, we are open to chasing momentum. However, the biggest risk to the market are bond yields, which should rise as investors start to price President Trump’s policies and their impact on deficits.

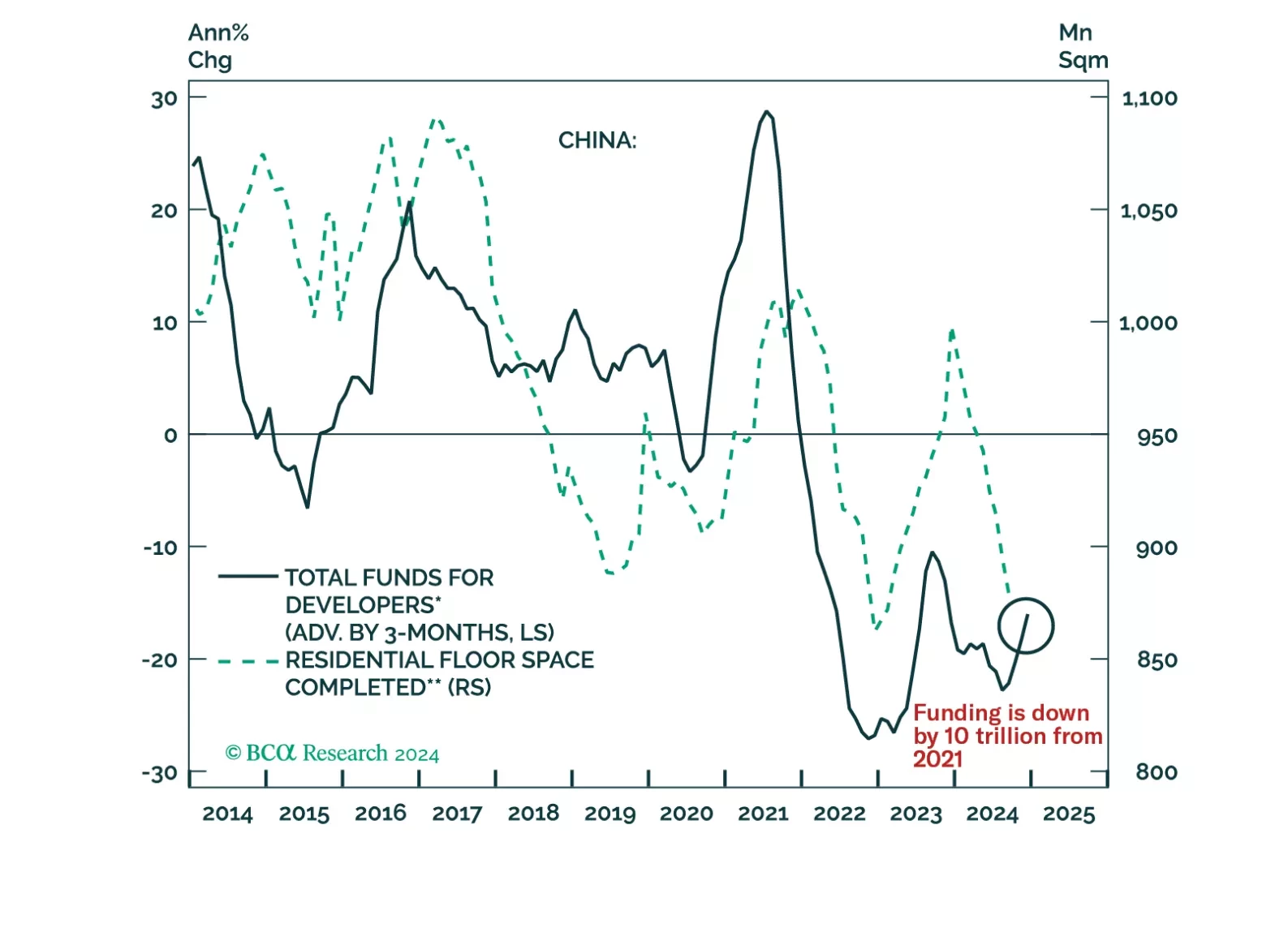

We spent last week visiting our clients in China. In this report, we share some of the key questions from the client meetings as well as our responses.