Emerging Markets

Chinese activity indicators were mixed in November, reflecting the dynamic of a resilient supply side coupled with weak demand. Industrial production growth was roughly flat at 5.4% y/y vs. 5.3% in October, while retail sales slowed down to 3.0% y/y from…

China’s November monetary and credit data were disappointing. New yuan loans increased by 580 bln, nearly half the expected amount. Total social financing rose by 2.3 tln instead of the expected 2.7 tln. Finally, M2 growth slowed to 7.1% y/y from 7.5% in…

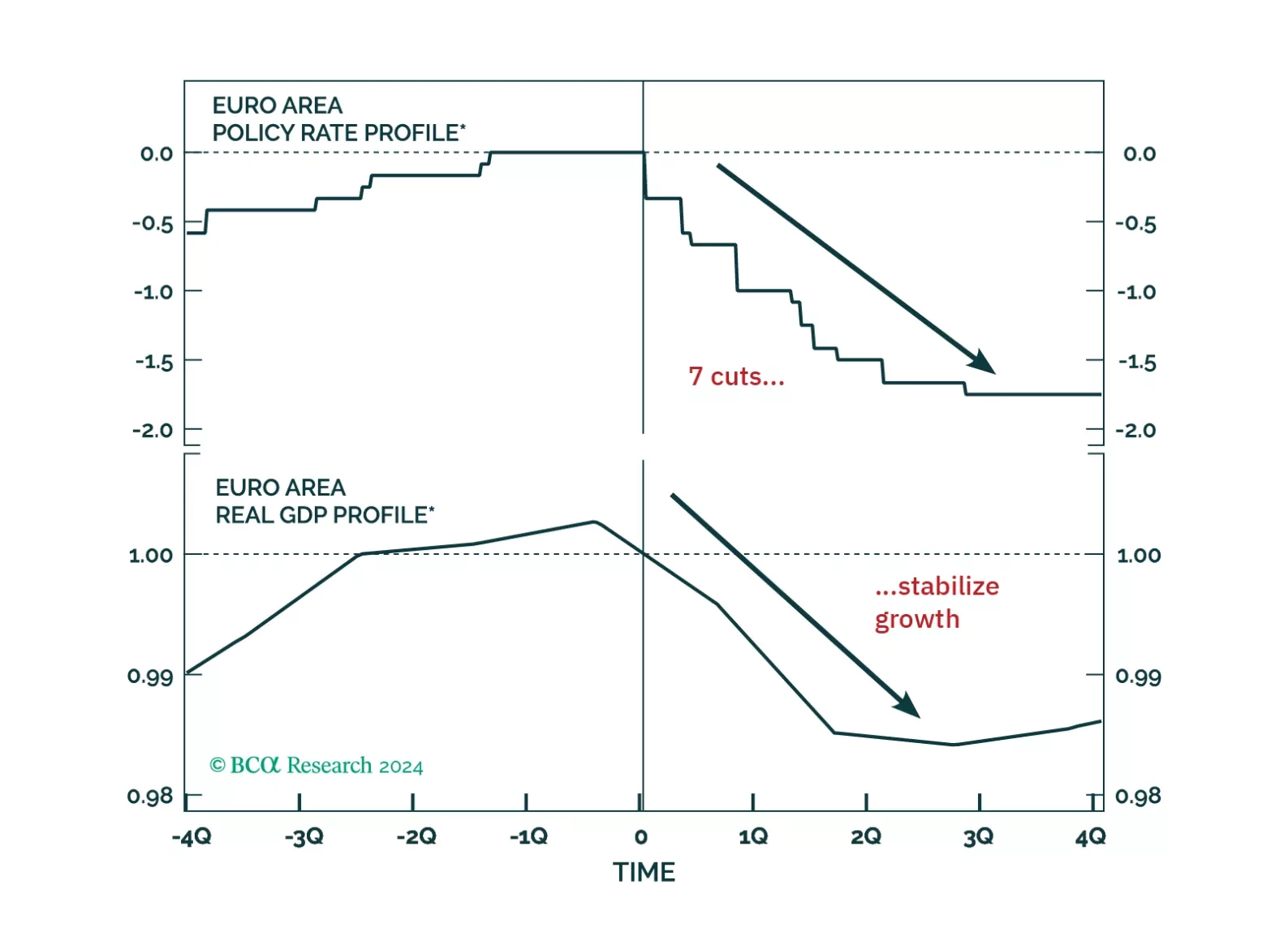

For our last publication of the year, we explore five key themes that will dominate the European macro landscape and markets next year. While the start of 2025 will be challenging for European assets, the latter part will offer some much-needed relief.

What is new? EMS is preparing the ground for a potential change in its USD view sometime in H1 2025. This will be a major milestone as EMS has been structurally bullish on the USD since the spring of 2011.

The USD has steamrolled both DM and EM currencies since the US election. Among the victims was the Chinese yuan, with USDCNY strengthening towards 7.3, a multi-year resistance level, from 7.11 on the day of the election. The CNY weakened further Wednesday…

- Congress will pass tax cuts by end of 2025 producing a fiscal thrust of about 0.9% of GDP in 2026.

- Trump will count on that stimulus as a basis for slapping tariffs on leading trade partners.

- China will retaliate against Trump and stimulate its domestic economy, while pursuing stronger trade ties with other countries. Europe will also retaliate.

- Geopolitical risk will shift from Ukraine-Russia to Israel-Iran, where the conflict will continue to escalate until a crisis point is reached within 2025.

China’s November trade balance increased to CNY 692.8 bln on the back of slowing-but-still-growing exports (down to 5.8% y/y from 11.2% in October), and a worsening imports contraction (-4.7% y/y vs. -3.7% in October). In Japan, growth in machine tools orders…

Chinese deflationary pressures intensified in November, with CPI ticking down to 0.2% y/y from 0.3% in October. Producer prices deflation eased, with prices falling 2.5% y/y, less than -2.9% y/y a month prior. The weak data prompted a Politburo statement…

The November Caixin services PMI ticked down to 51.5, which along with a rising manufacturing PMI pushed the composite up to 52.3 from 51.9. Components such as new orders and employment also ticked down, and output prices fell to 49.6. Services also weakened…

South Korea is undergoing political turmoil, with President Yoon attempting to declare martial law. The situation is fluid and can change quickly, but there are a few investment takeaways. As we pointed a few weeks back, BCA expects geopolitical tensions…