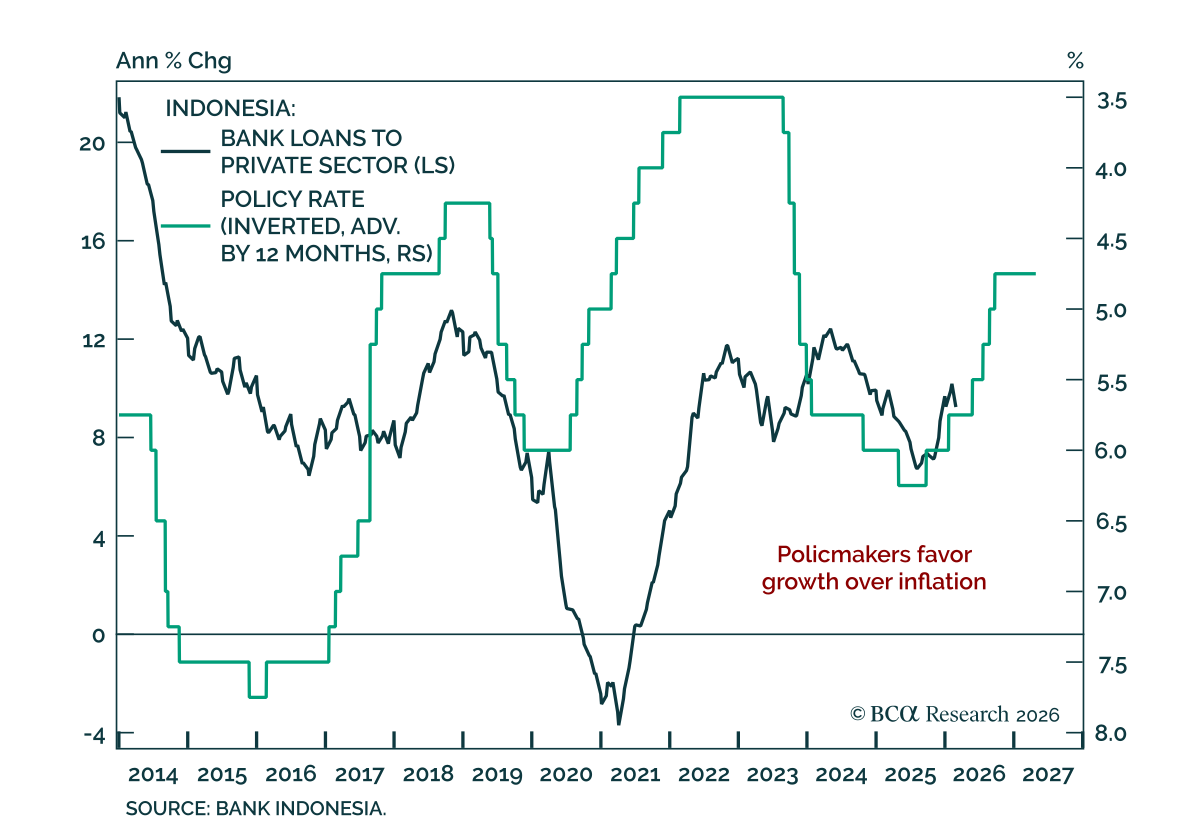

Emerging Markets

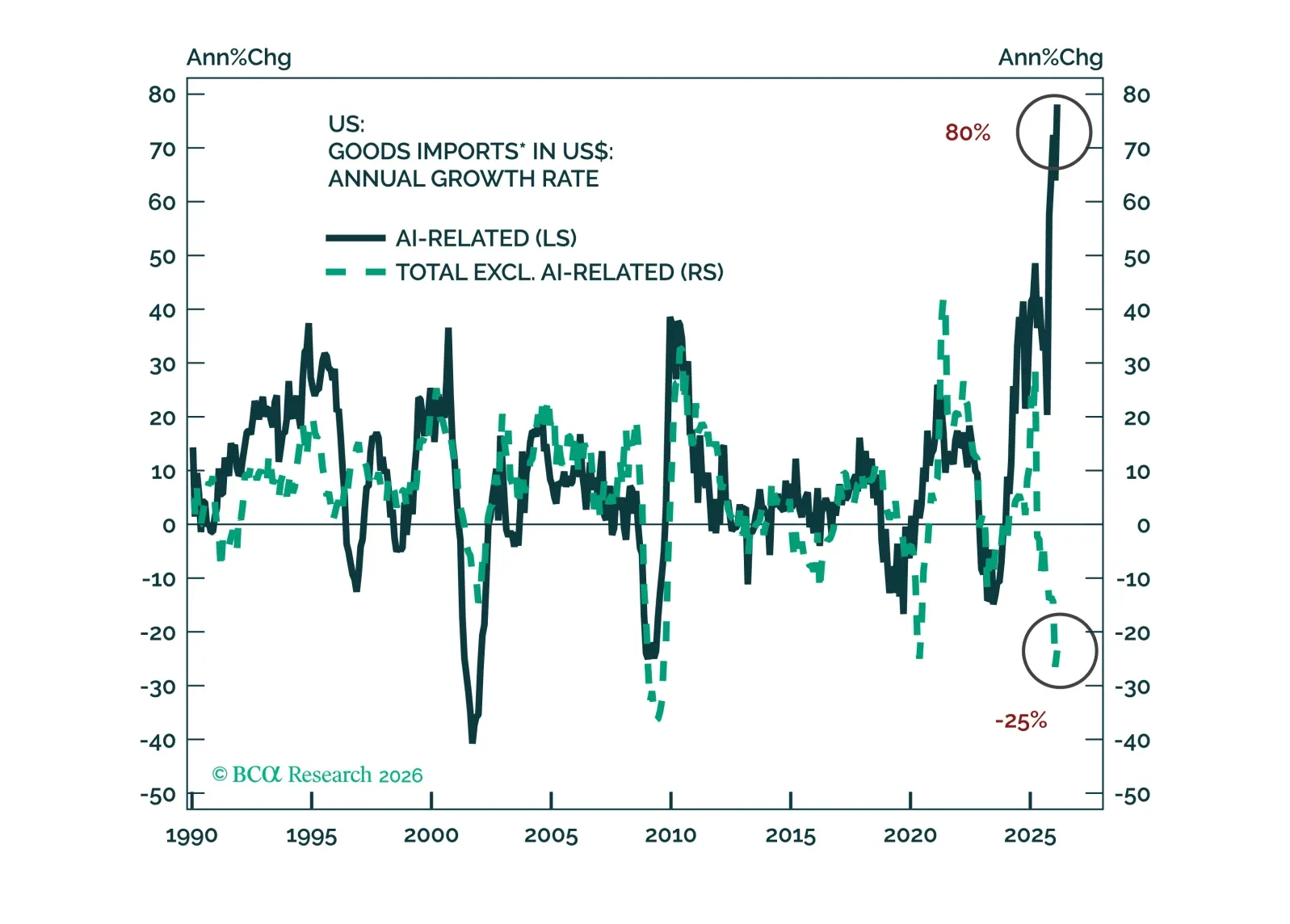

Global trade has held up despite US non-AI import volumes contracting by 25% over the past 12 months. The strength in global trade has concentrated in two areas: (1) imports of AI-related hardware and (2) developing countries’ imports, especially from China. Will these continue?

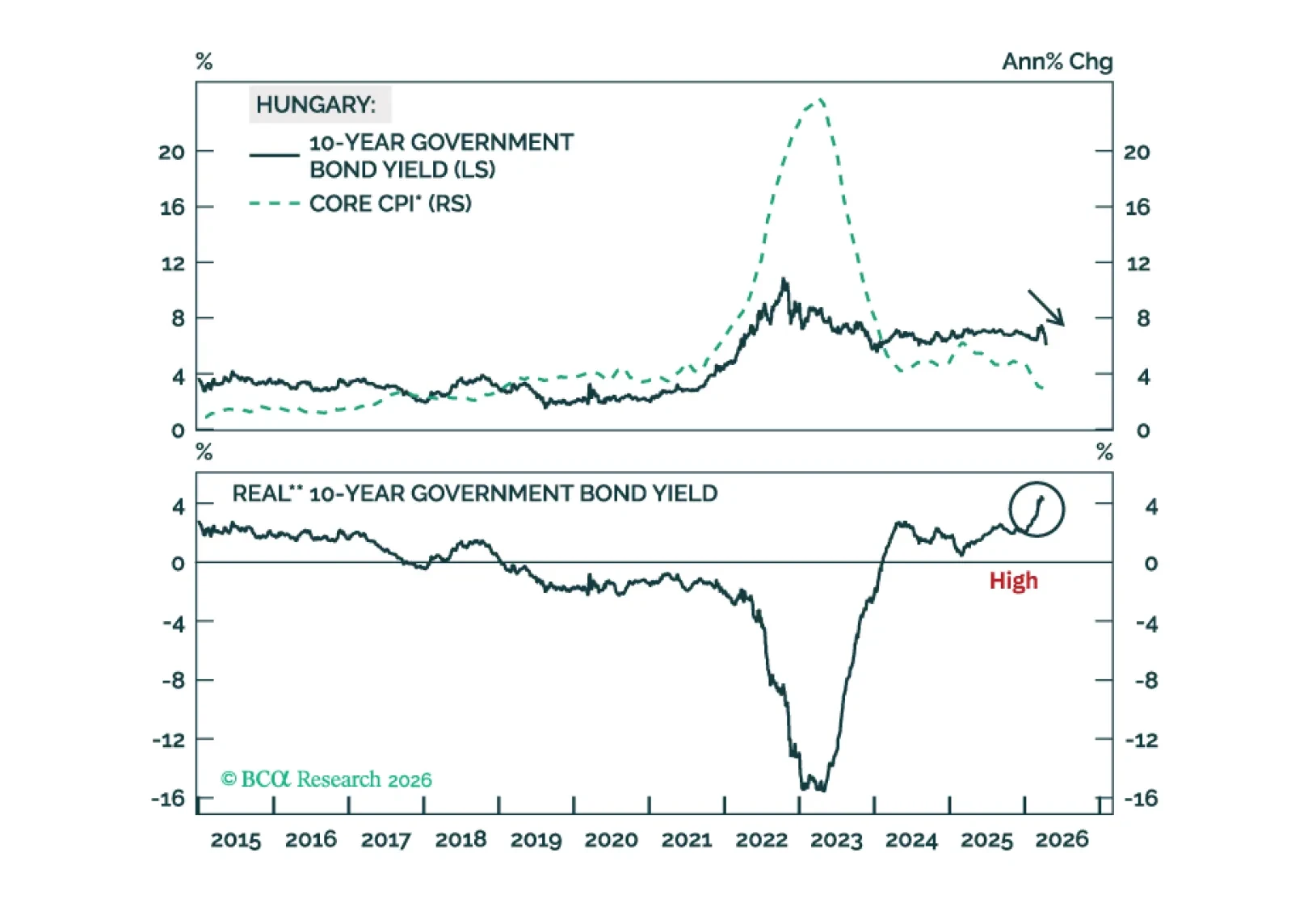

Hungary’s growth outlook has improved as the election of a new government will likely unlock significant EU funds for the country. Currency traders should go long the Hungarian forint / short US dollar.

The relief rally in stocks can continue a while longer. However, much can still go wrong. As such, we are retaining a 12-month underweight to stocks but are moving to neutral on a short-term tactical horizon.

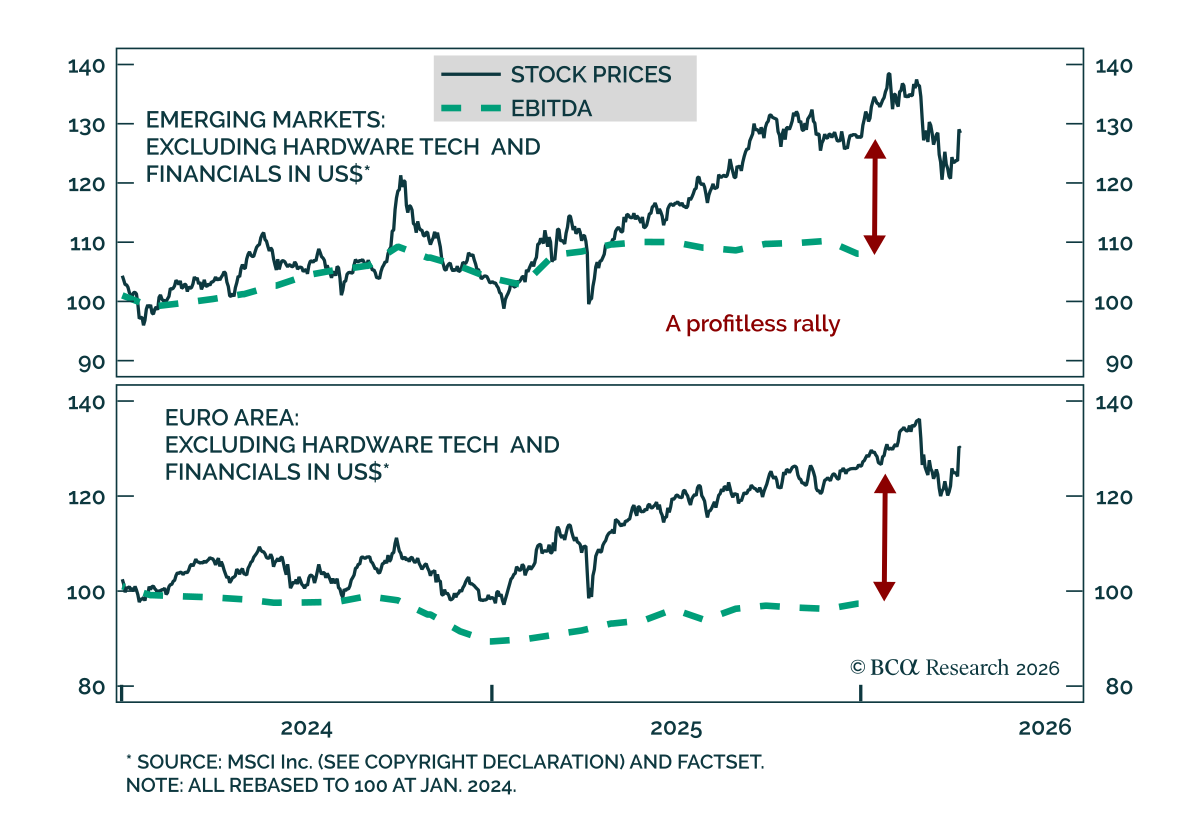

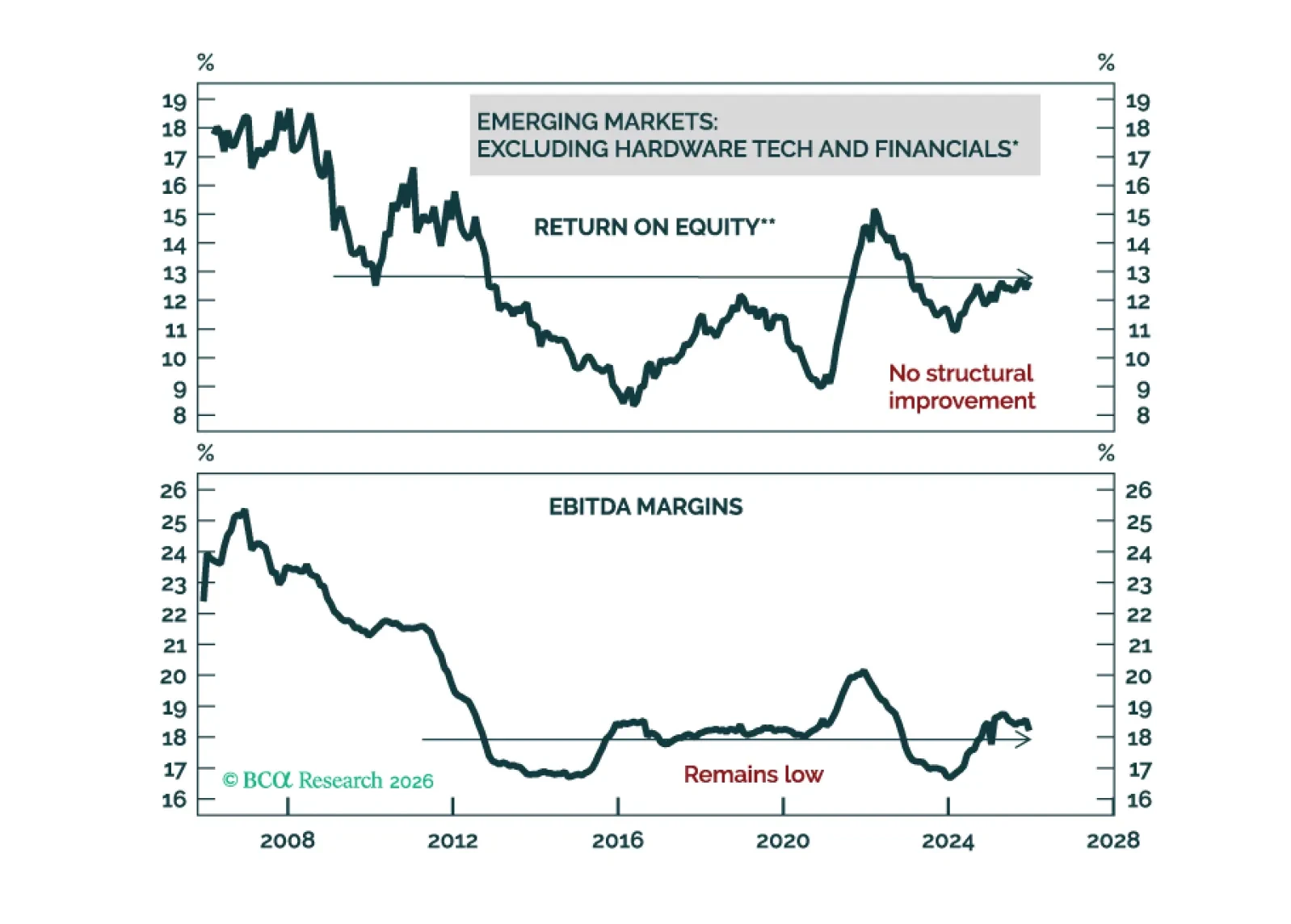

Outside Asian semiconductor producers, EM corporate earnings and profitability have seen little improvement. Despite the ceasefire in the Middle East, the medium-term outlook for EM stocks is still unattractive.

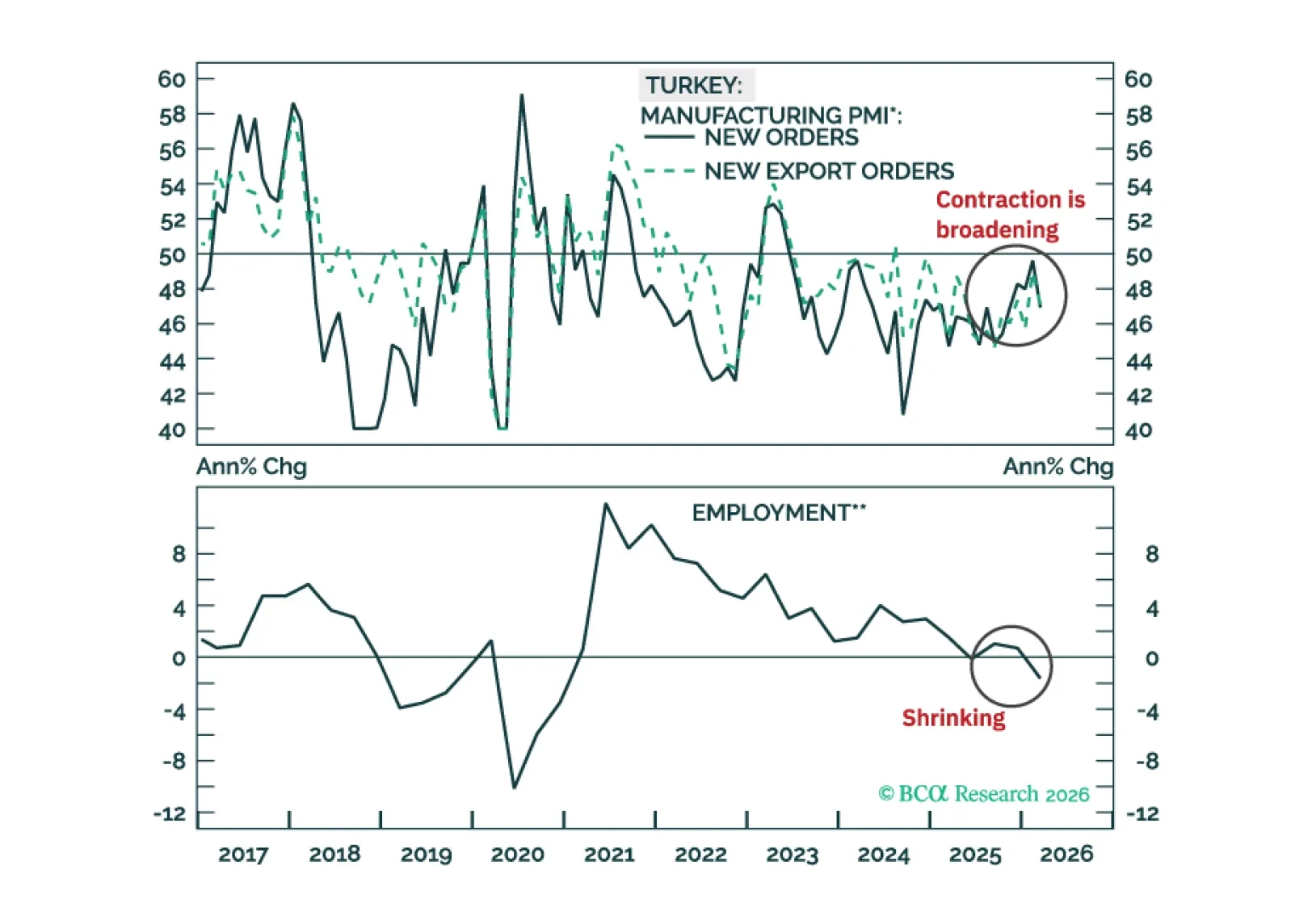

The Turkish financial markets will struggle in the very near term, but beyond that, the cyclical disinflation process will resume. Fixed-income investors should put Turkish 2-year local currencybonds on a ‘buy’ watch list.

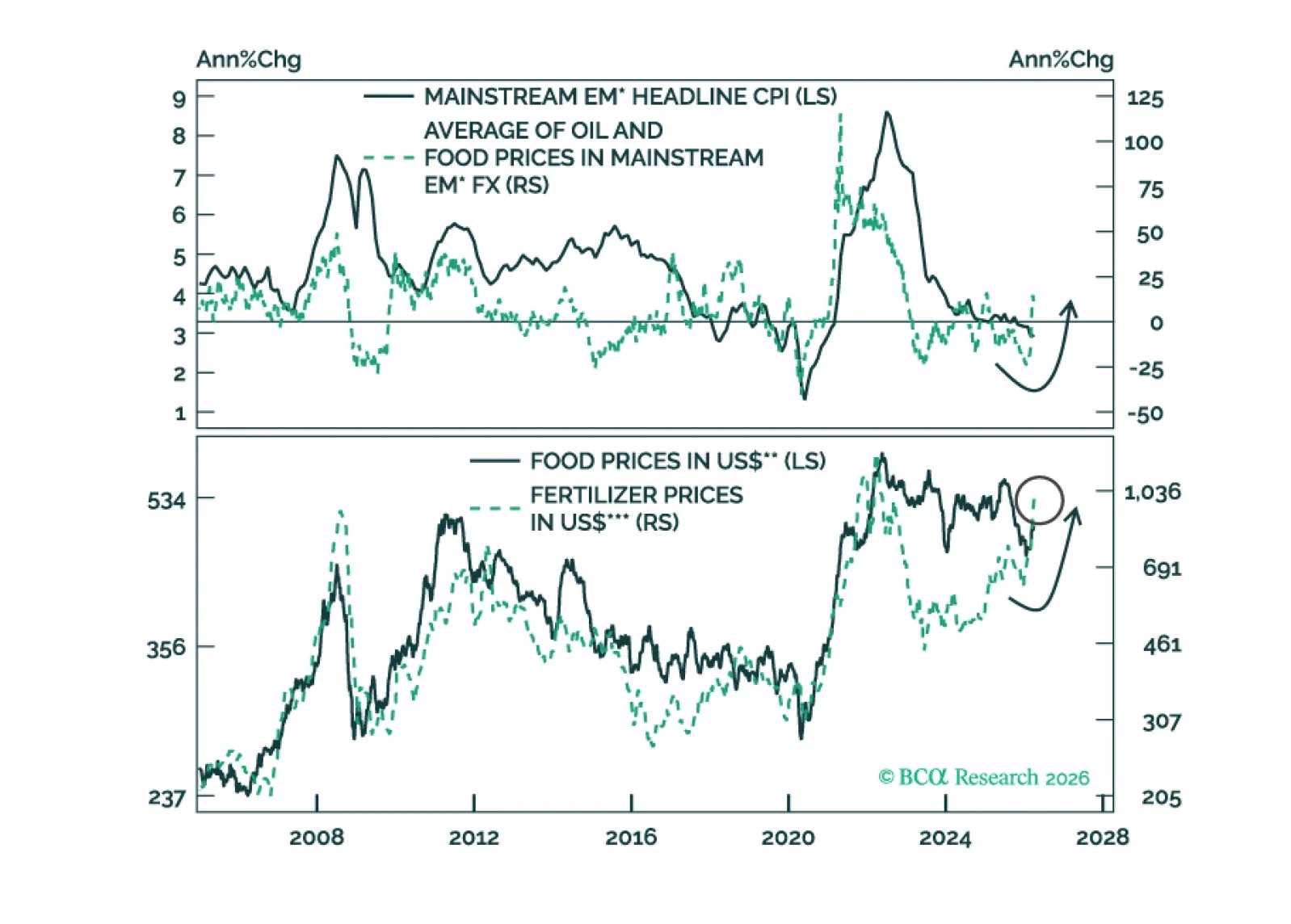

The global risk-off phase will persist. It is too early to buy local-currency bonds in Mainstream EM, but it is not too late to sell EM sovereign and corporate credit (USD bonds).

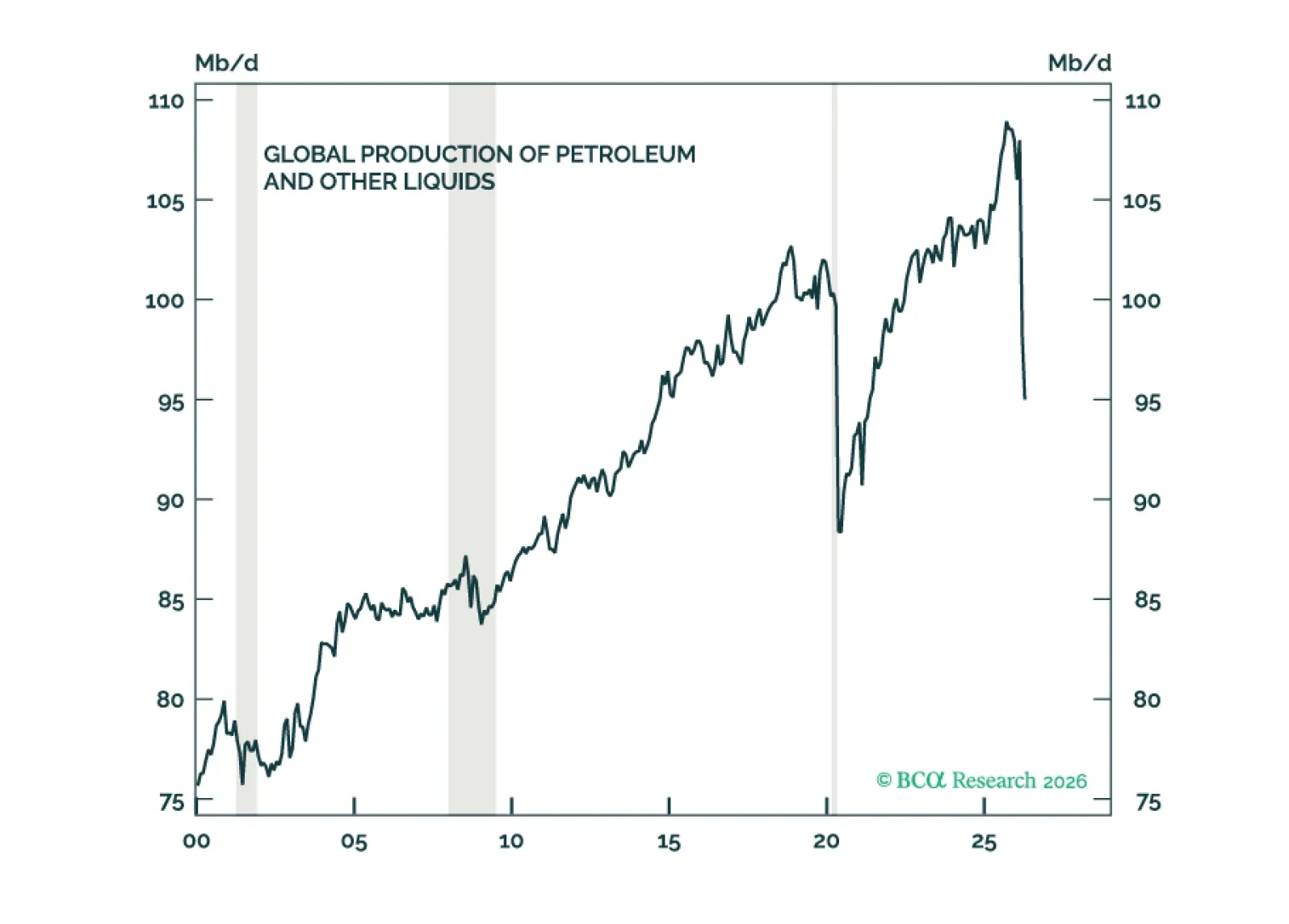

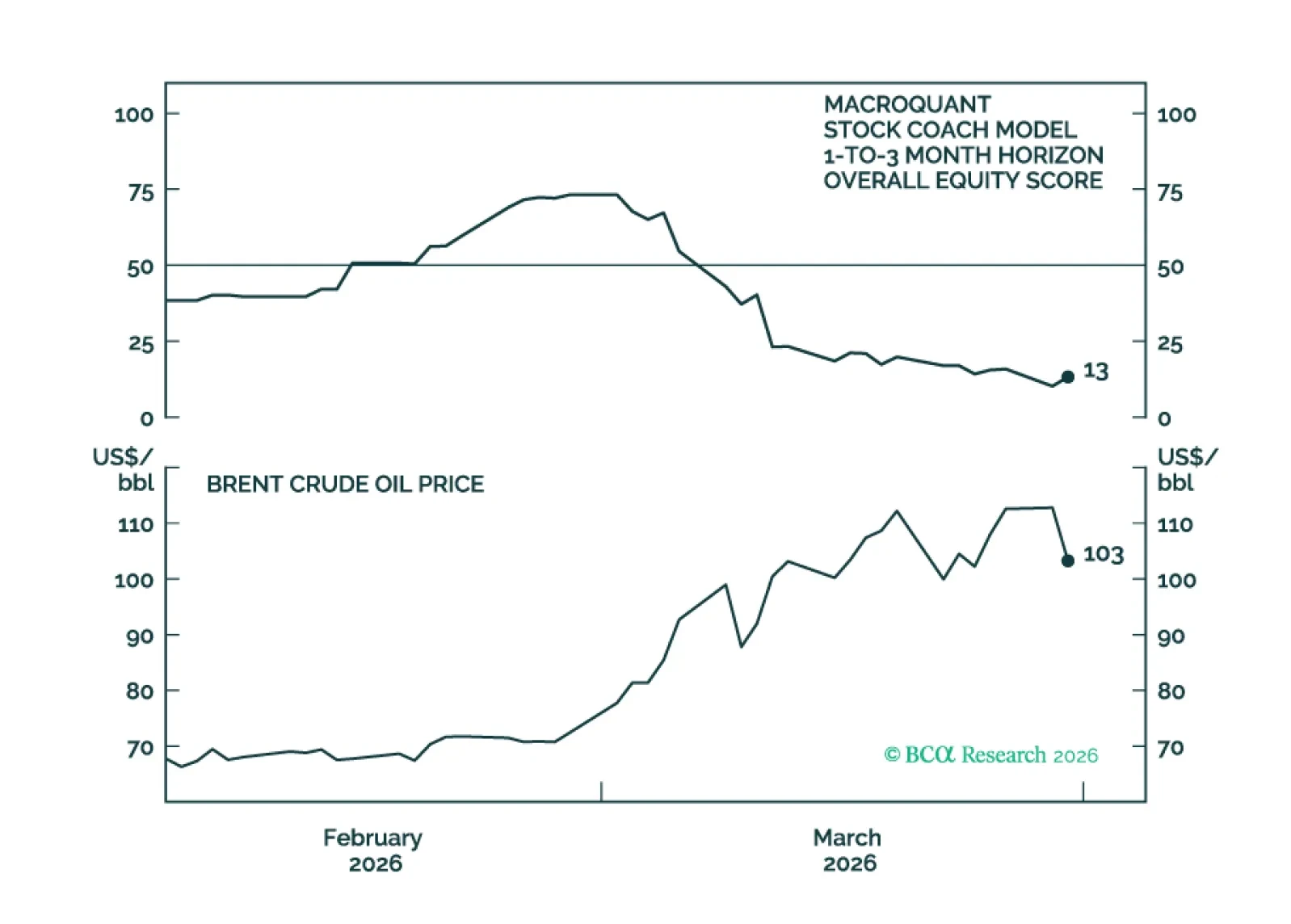

MacroQuant recommends a strong underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, has become neutral-to-slightly positive on the US dollar, has downgraded gold to neutral and copper to a strong underweight, and is bullish on oil.