Emerging Markets

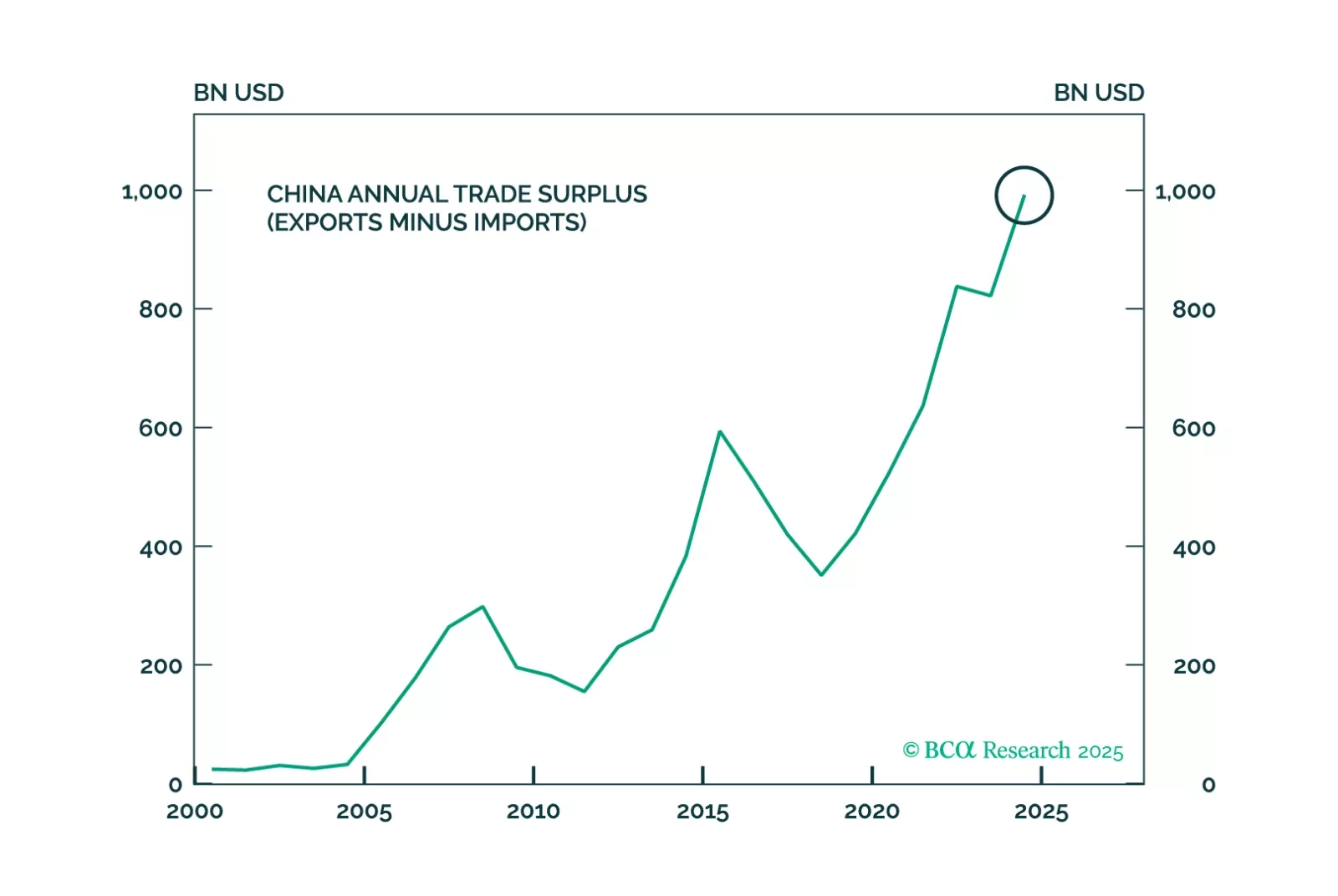

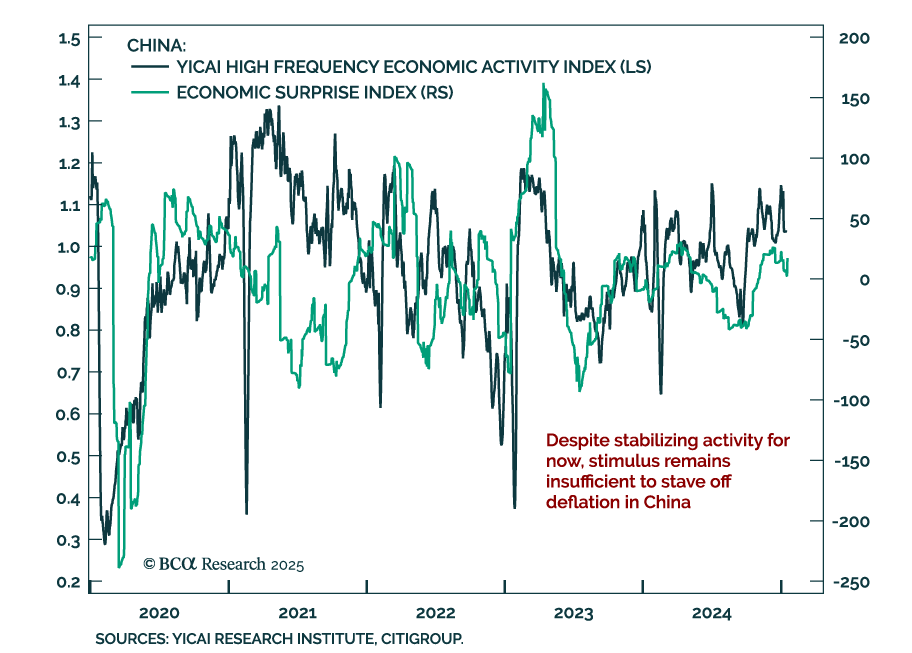

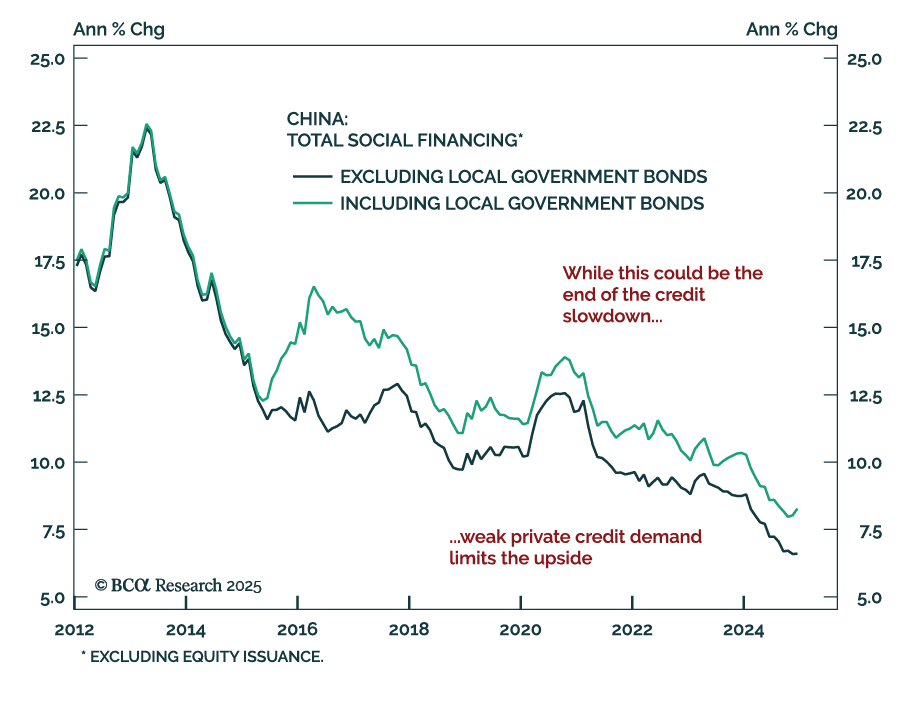

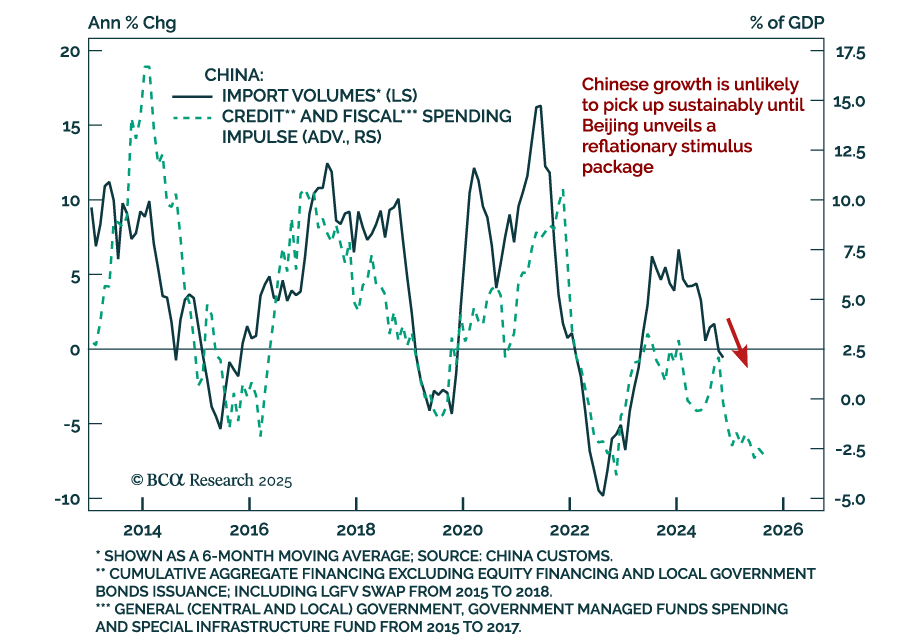

China barely hit its growth target in 2024 by shifting back to its old model of exports, racking up a record trade surplus with the world – right as Donald Trump walks back into the White House. Tariffs will elicit larger fiscal stimulus even as China rolls out innovations such as DeepSeek to meet its 2025 industrial goals, creating a volatile mix this year.

Global risk assets are engulfed in a wave of euphoria, which is pulling Europe higher along the way. However, risks still abound. How should investors adjust their allocation to Europe under these highly uncertain conditions?

There is no better way to gauge the macro policies of the new US administration than being privy to President Donald Trump’s discussions with the new Treasury Secretary, Scott Bessent. While we do not have inside information, we have put the pieces of the puzzle together to help clients see the big picture. This report presents our take on a hypothetical conversation between President Trump and Scott Bessent that led to the latter’s appointment as Treasury secretary.

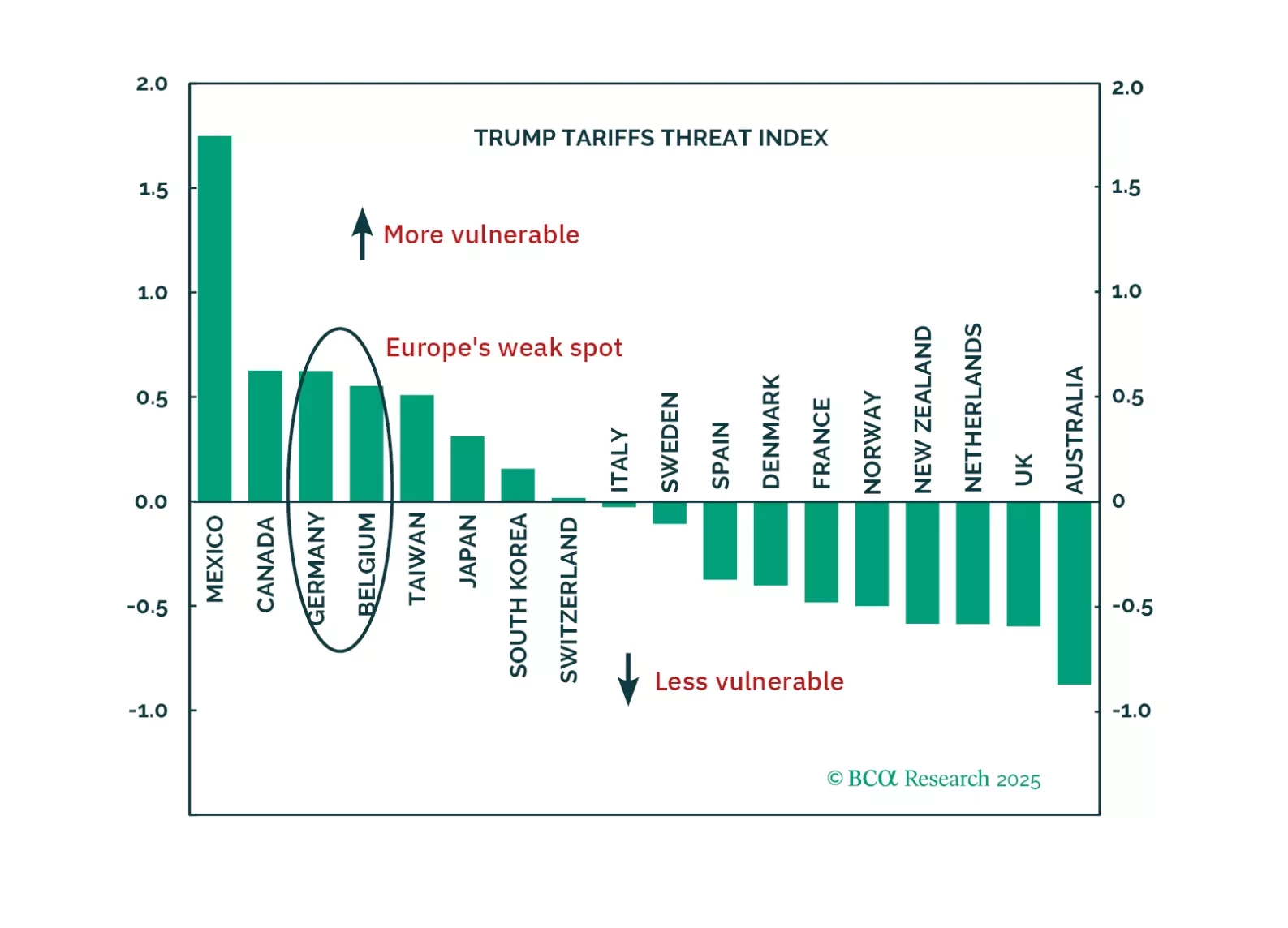

President Trump is about to be inaugurated. Investors often assume all his policies will hurt Europe, but the reality is more nuanced.

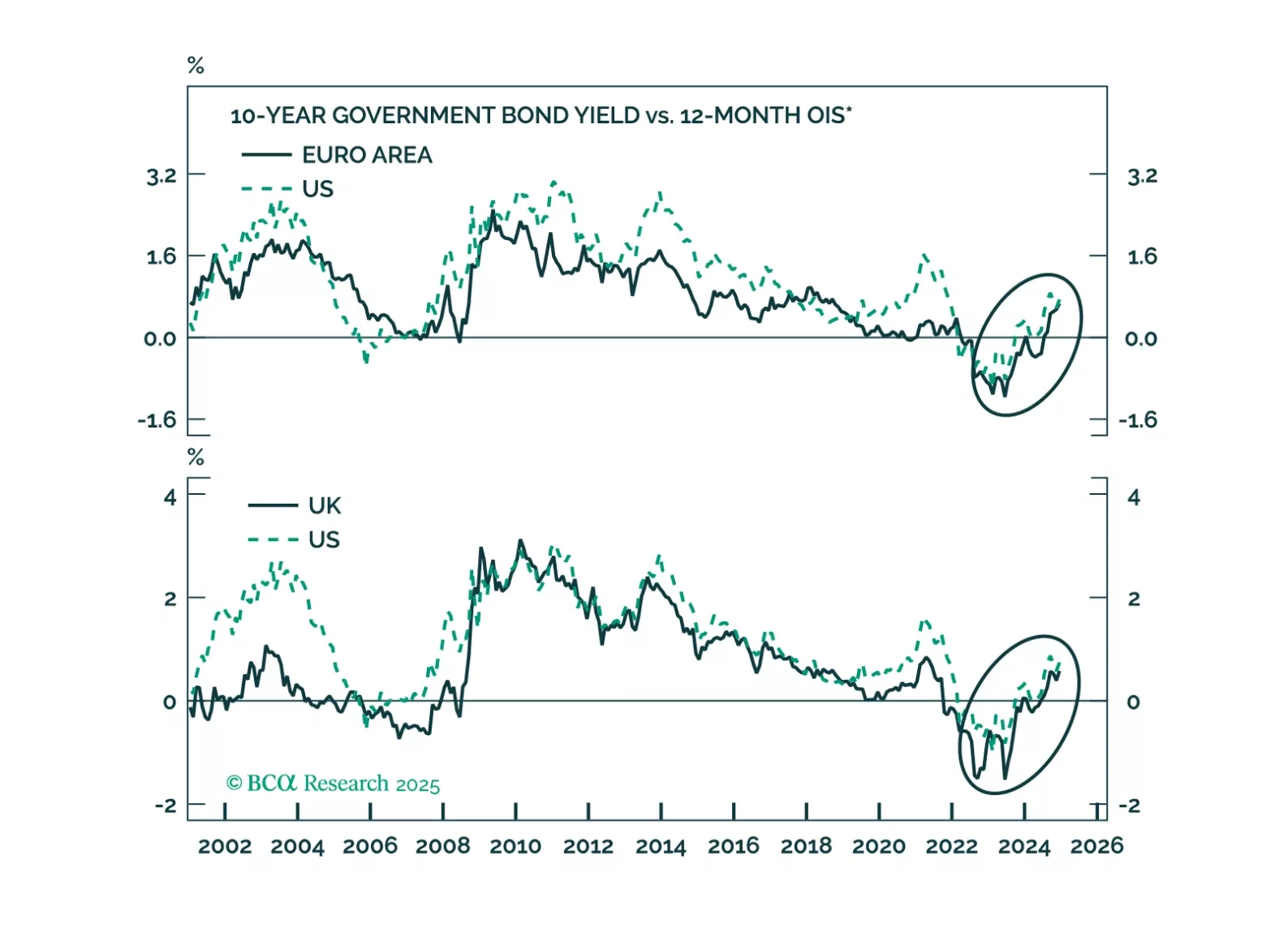

UK and German bonds are victims of the global bond market riots. Will European yields continue to move higher and will the euro and the pound find a floor anytime soon?