Emerging Markets

Outside of the real estate sector, Chinese activity was decent in January and February. Both industrial production and retail sales were slightly stronger than expected. The jobless rate ticked up to 5.4% while property investment was down -9.8%…

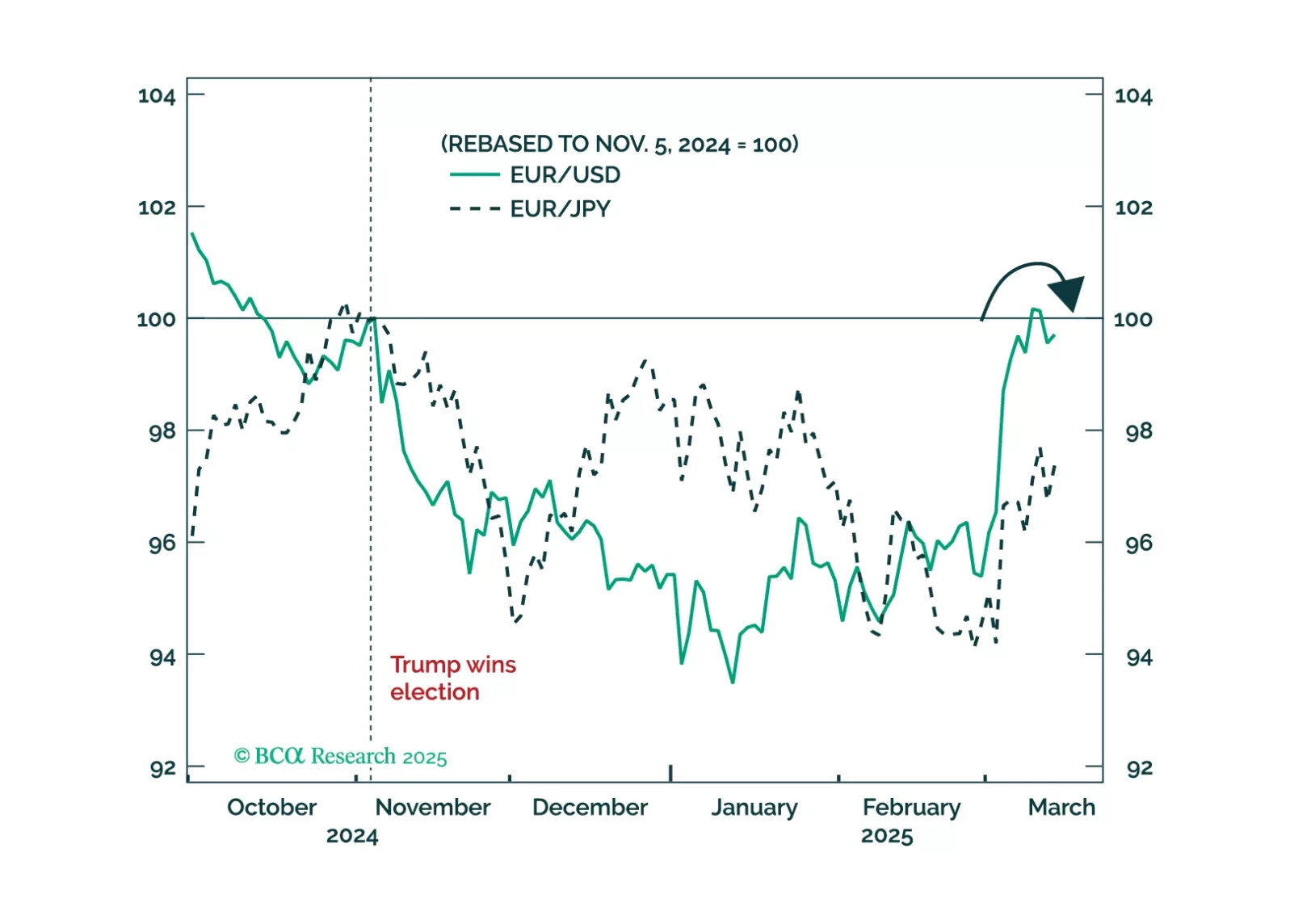

Trump’s foreign policy can be explained by rational US interests, but it requires settling the trade war with allies sooner rather than later. Book gains on EUR-USD for now.

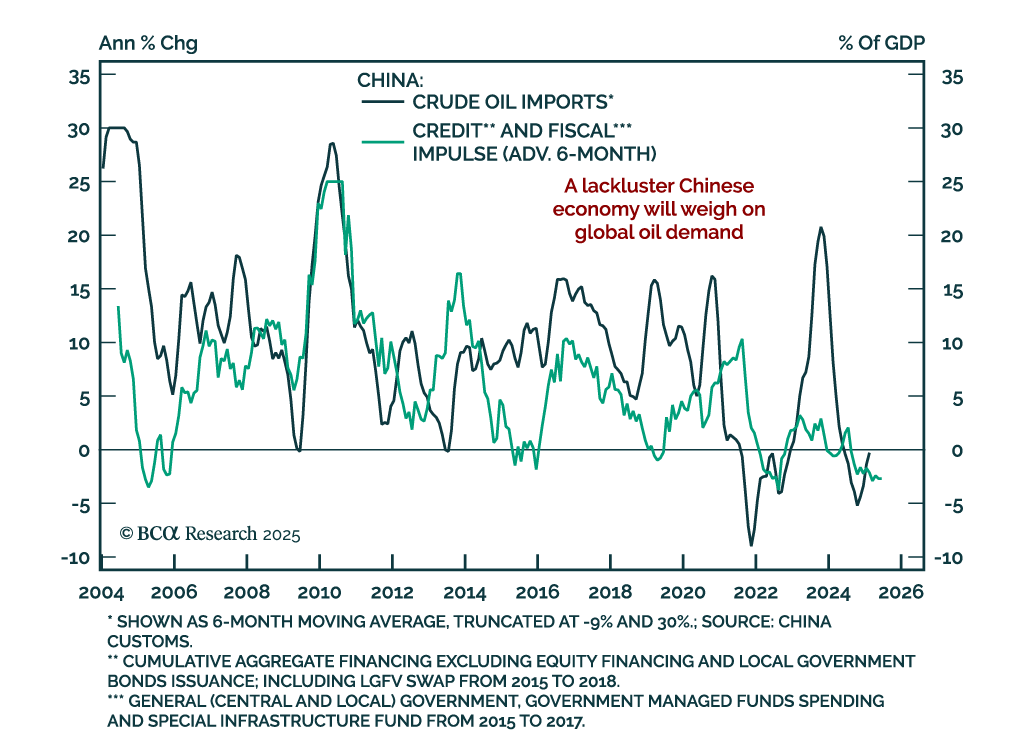

Our Commodities strategists assessed the outlook for oil as crude remains pulled between geopolitical and fundamentals forces. OPEC+’s decision to raise oil supply is driven more by geopolitics than economics. A sustained improvement in Chinese oil…

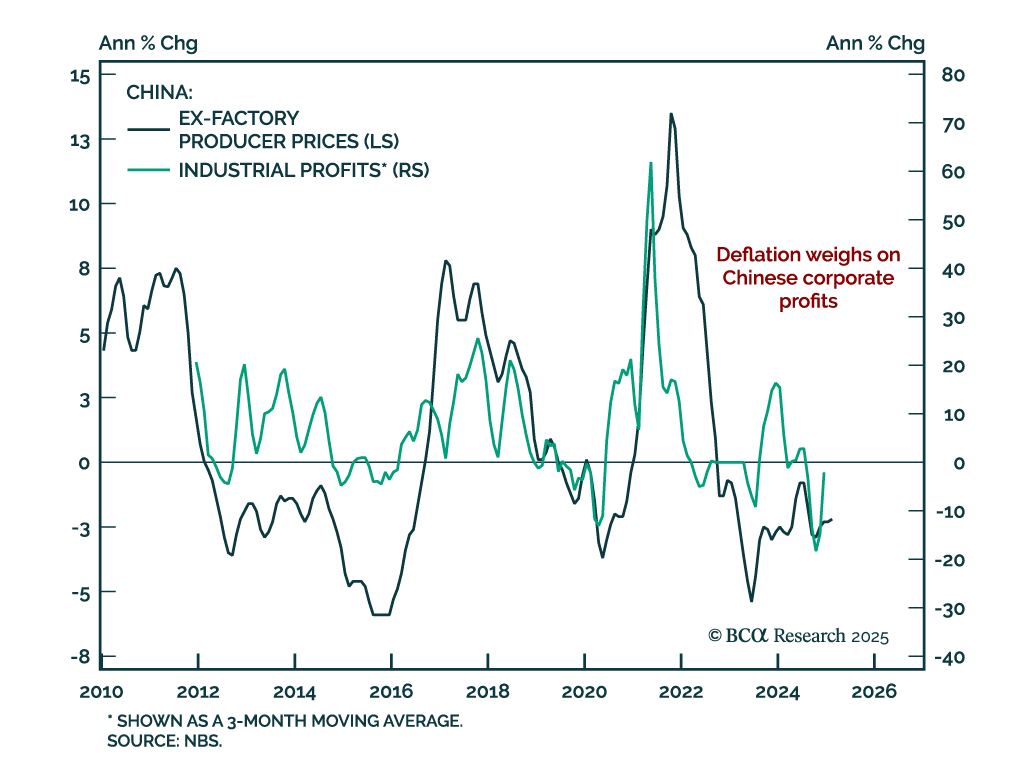

China’s February consumer prices fell 0.7% y/y after expanding on an annual basis in January. Producer price deflation stood at -2.2% y/y, roughly unchanged from a month prior. China’s first quarter data is heavily influenced by seasonality, as the shifting…

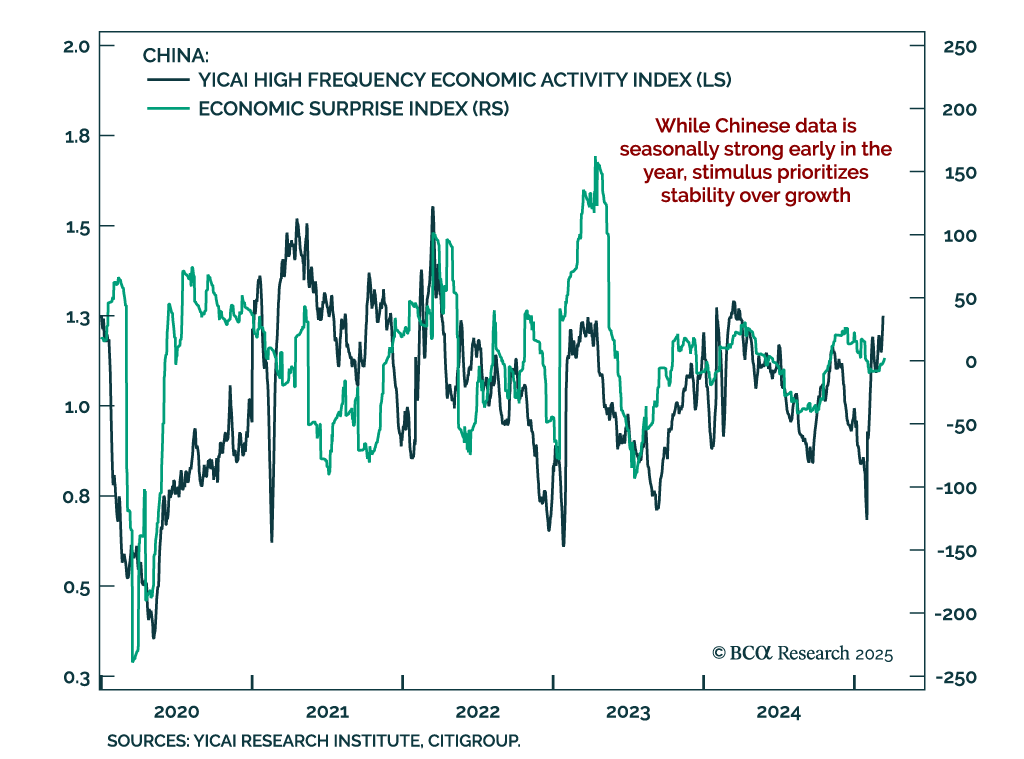

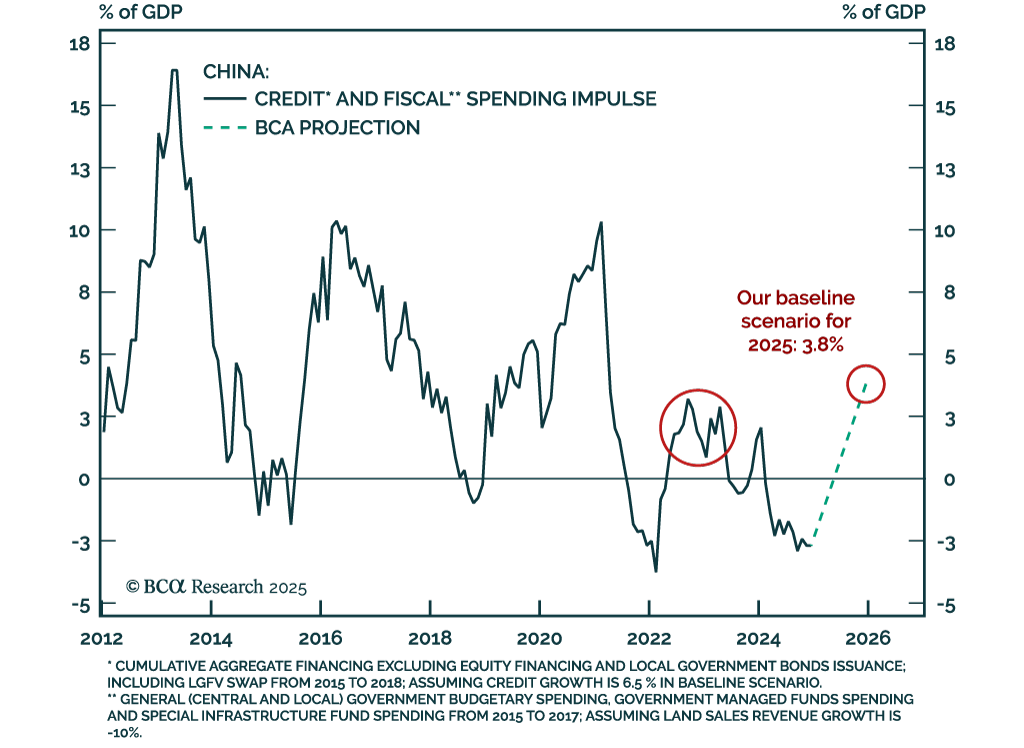

Our China and Emerging Markets strategists assessed China’s outlook after the National People’s Congress concluded last week. China’s latest fiscal stimulus is only marginally larger than last year’s, with a combined credit and fiscal impulse of 3.8% of…

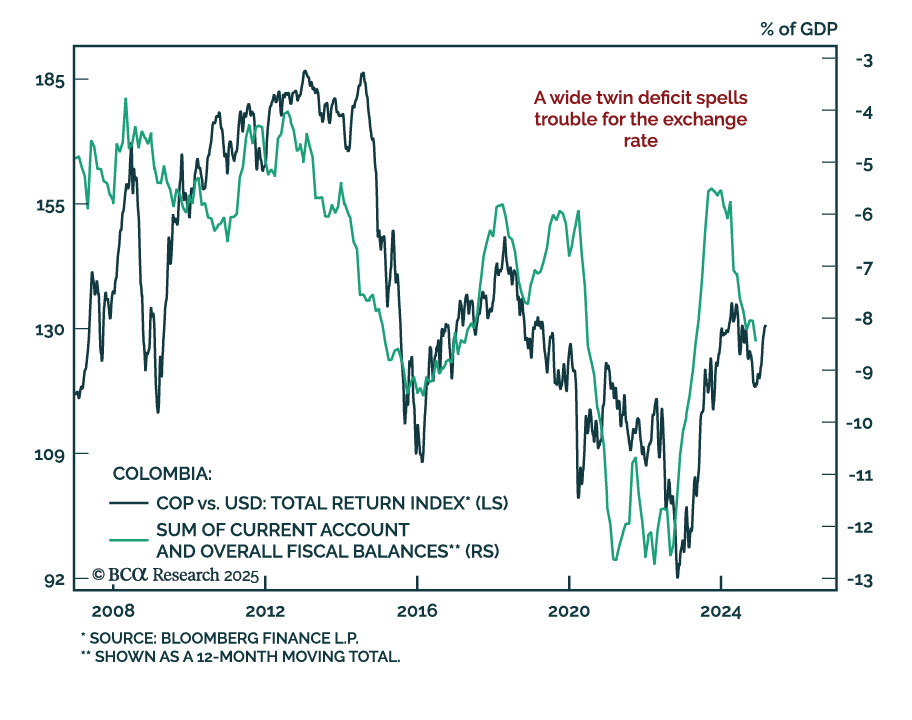

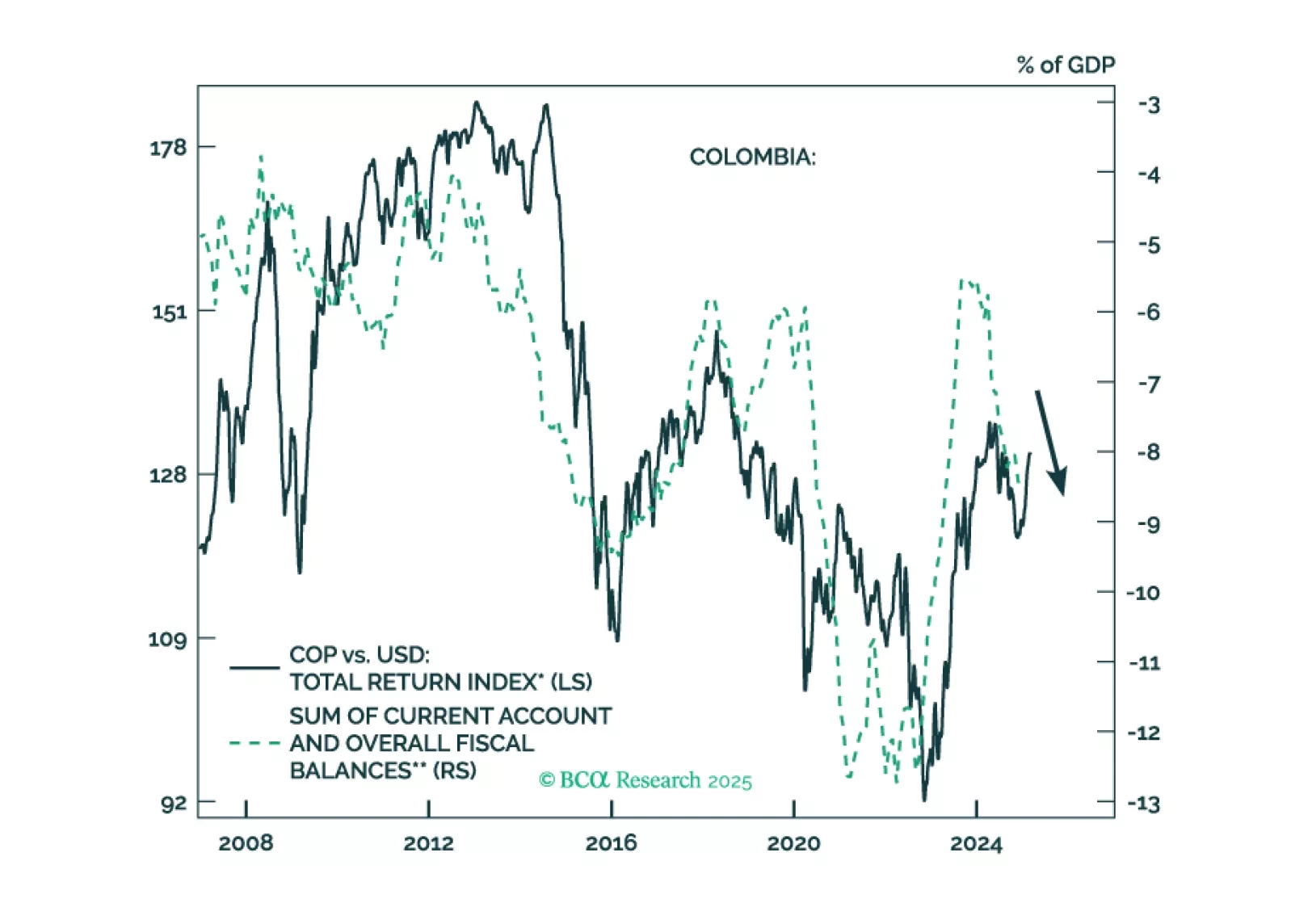

Our Emerging Markets strategists assessed Colombian assets after a significant rally. Colombia faces deep-rooted macroeconomic challenges that will not be easily reversed by a right-wing government in 2026. Public debt is on an unsustainable path, with…

Colombian financial markets have rallied on the expectation that a right-wing government will be elected in 2026. We take a contrarian bearish stance on the nation's financial markets. Colombia is suffering from two structural macro issues – unsustainable public debt and plunging energy exports – that will not be easily solved by a conservative administration in 2026. Continue underweighting Colombia within EM equity and fixed-income portfolios, continue shorting the COP versus the USD and the CLP, and bet on yield curve steepening.

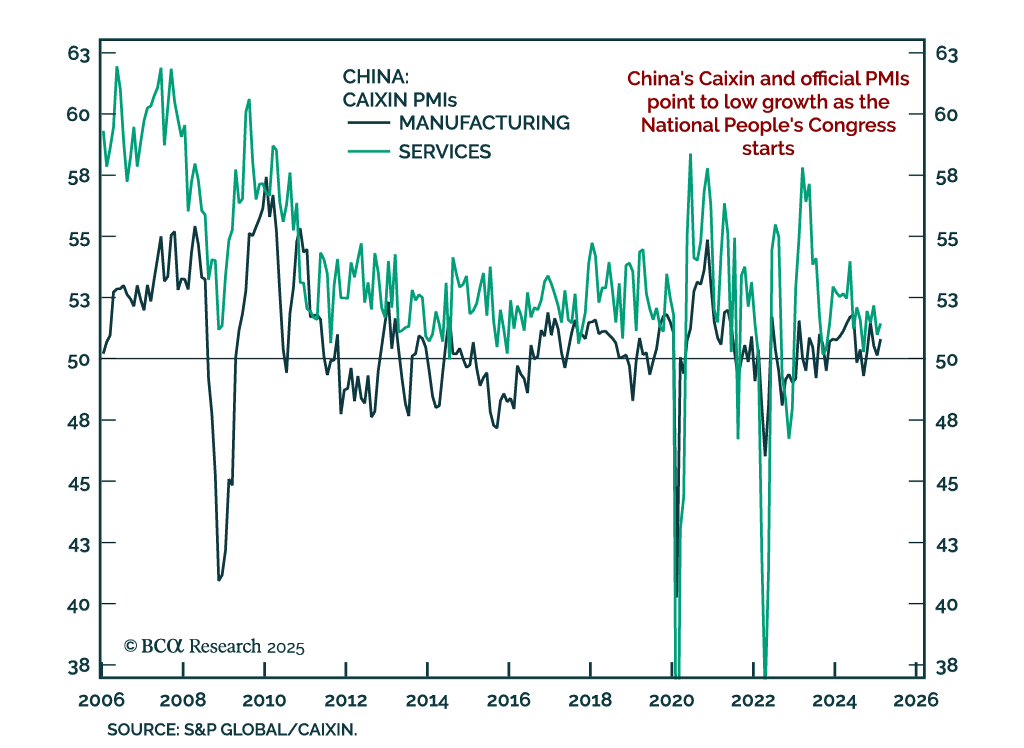

China’s February Caixin PMIs showed growth remains tepid. The composite ticked up to 51.5 from 51.1. Services are still showing a very faint expansion at 51.4, with manufacturing ticking up to 50.8. The message from the official NBS PMIs was similar.…

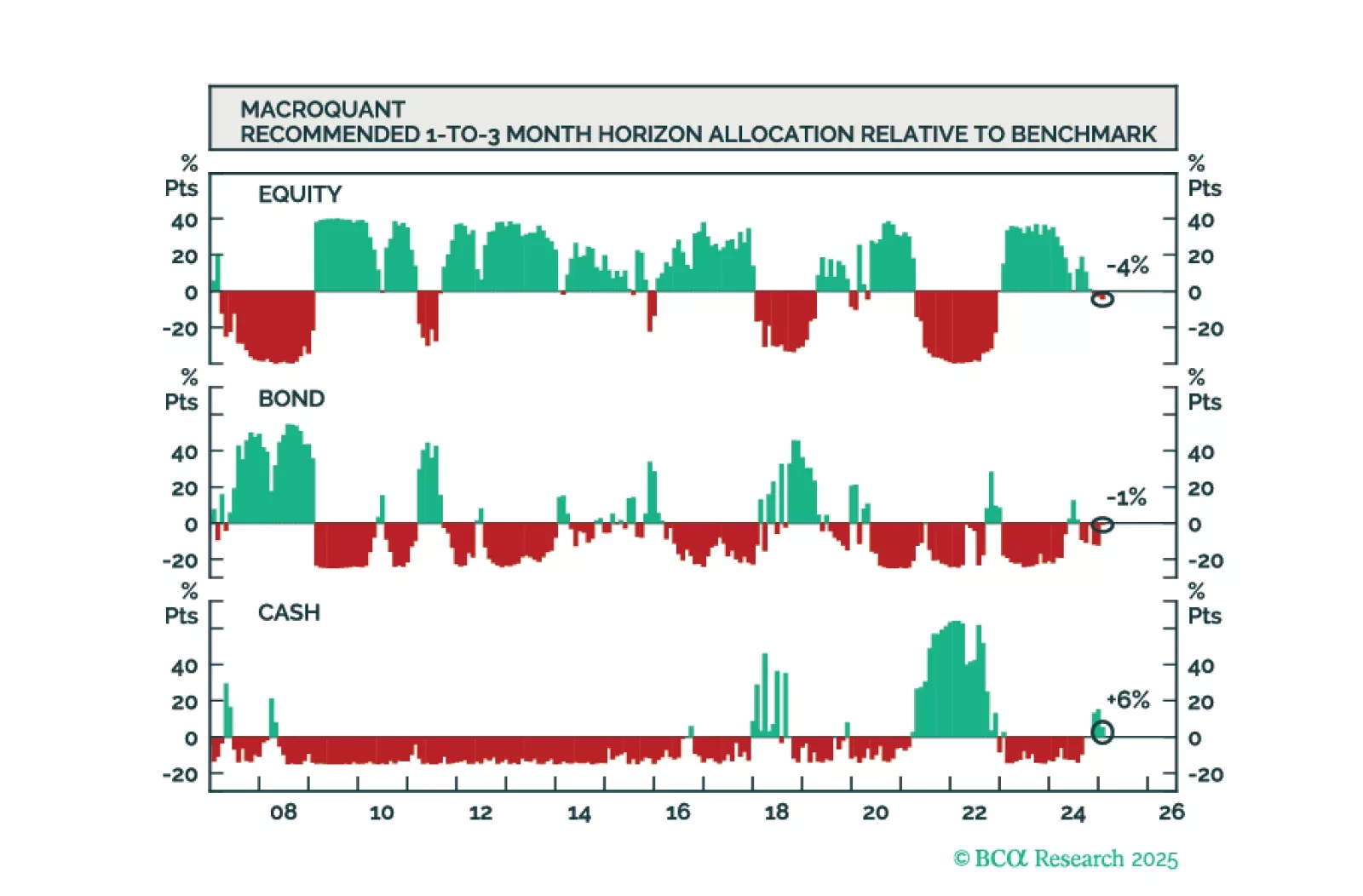

The MacroQuant model is no longer bullish on stocks but is not yet prepared to turn underweight. Subjectively, the Global Investment Strategy team is more bearish on equities than the model.