Emerging Markets

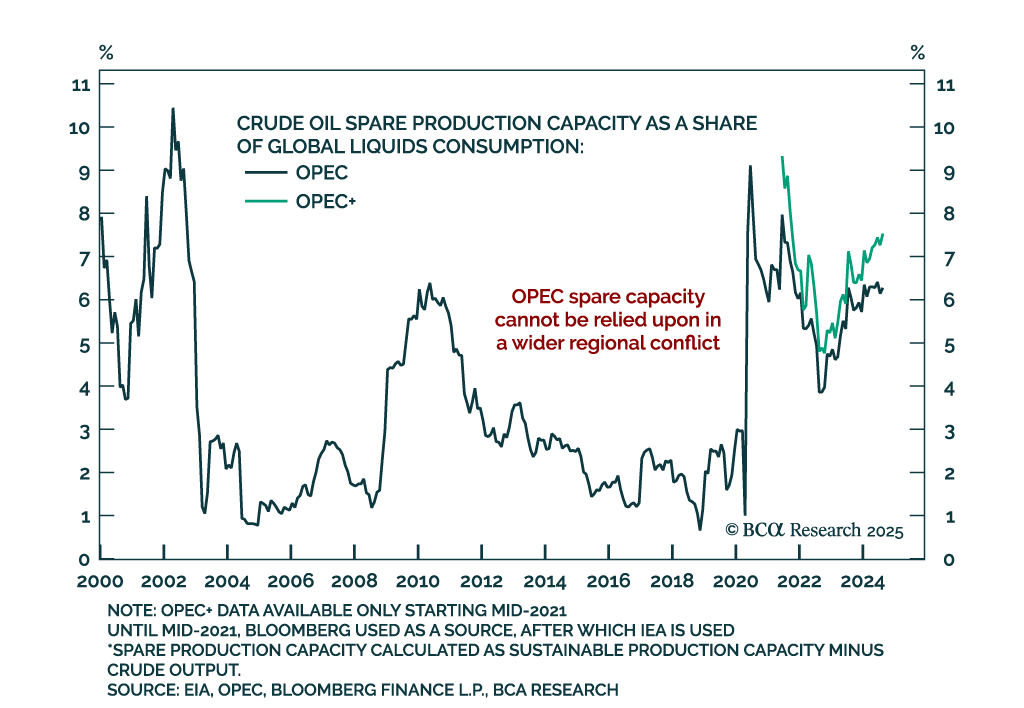

The Israel-Iran conflict is escalating, raising the odds of a major oil supply shock and reinforcing the case for cash, US equity overweight, and tactical energy exposure. Our Chart Of The Week comes from Matt Gertken, Chief Geopolitical and US Political…

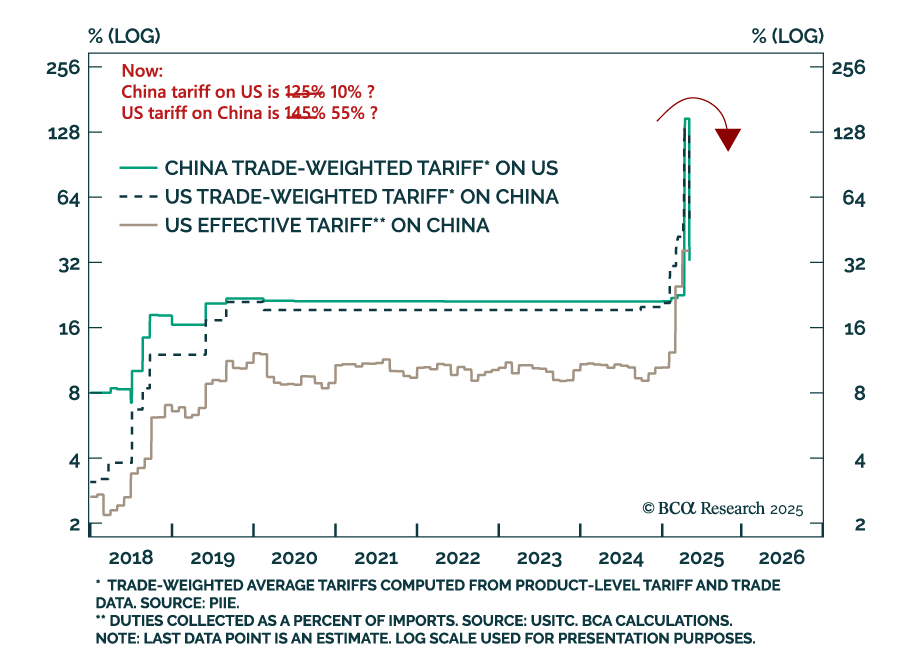

BCA’s China Investment strategists see limited upside for Chinese equities and favor bonds, as trade tensions ease but domestic headwinds persist. This week’s US-China trade talks in London lowered the risk of near-term escalation or new retaliatory tariffs,…

The US-China tariff deal confirms one thing: markets are still priced for perfection, with little upside even if a recession is dodged. The London negotiations yielded a partial agreement: The US will reduce tariffs, and China will remove export restrictions…

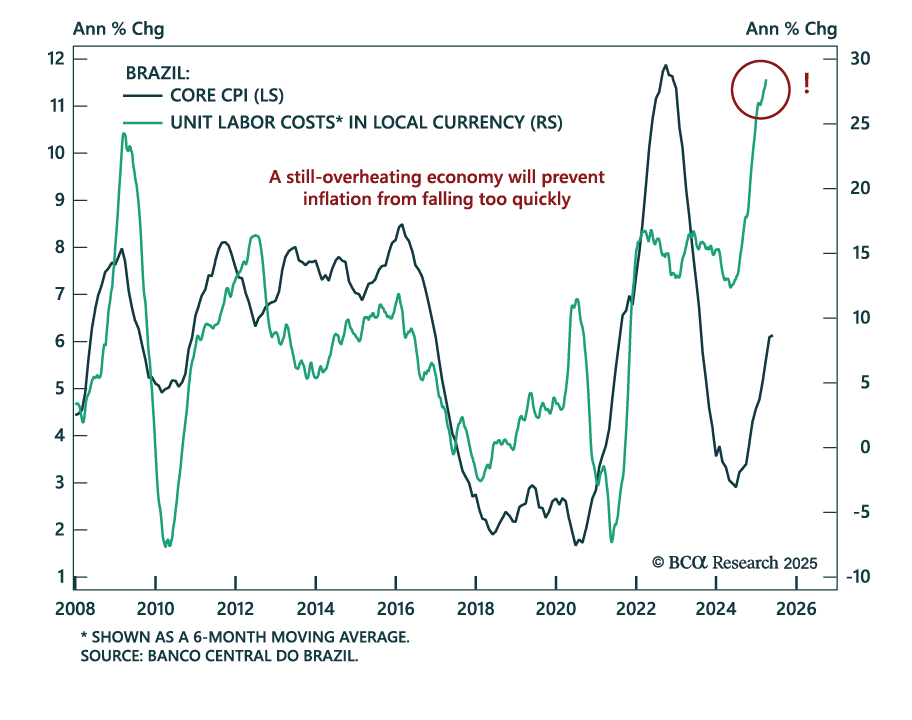

The May Brazilian CPI suggests that price pressures may have reached a peak, but do not expect immediate monetary easing to support fixed income markets. Headline CPI slowed to 5.3% y/y from 5.5% April, but core CPI remained flat at 6.1%. Despite…

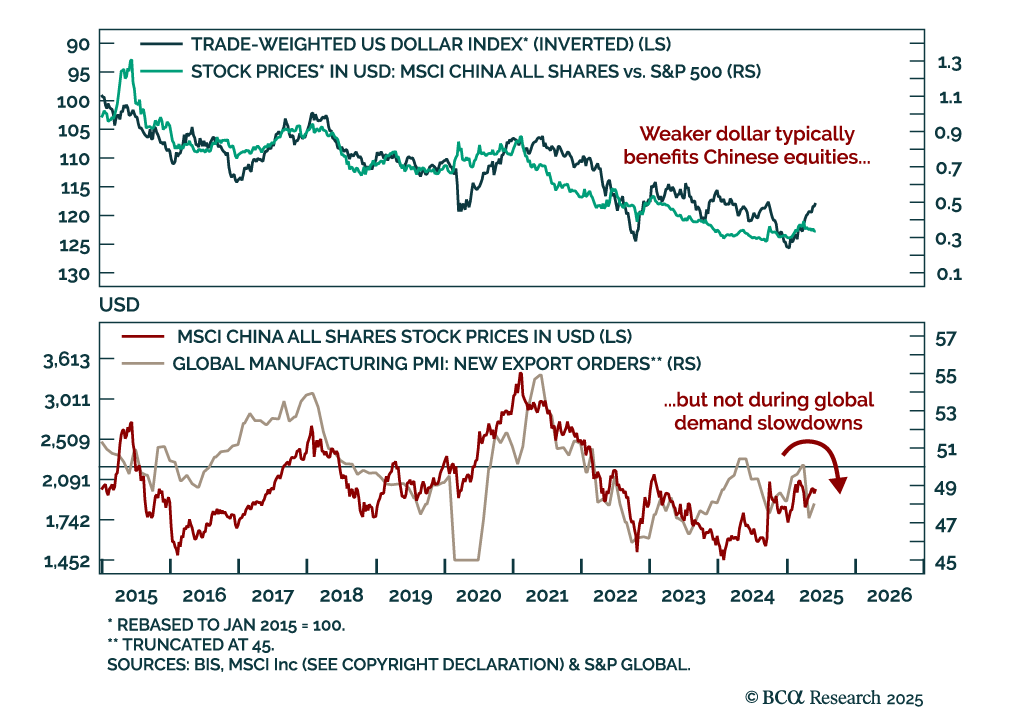

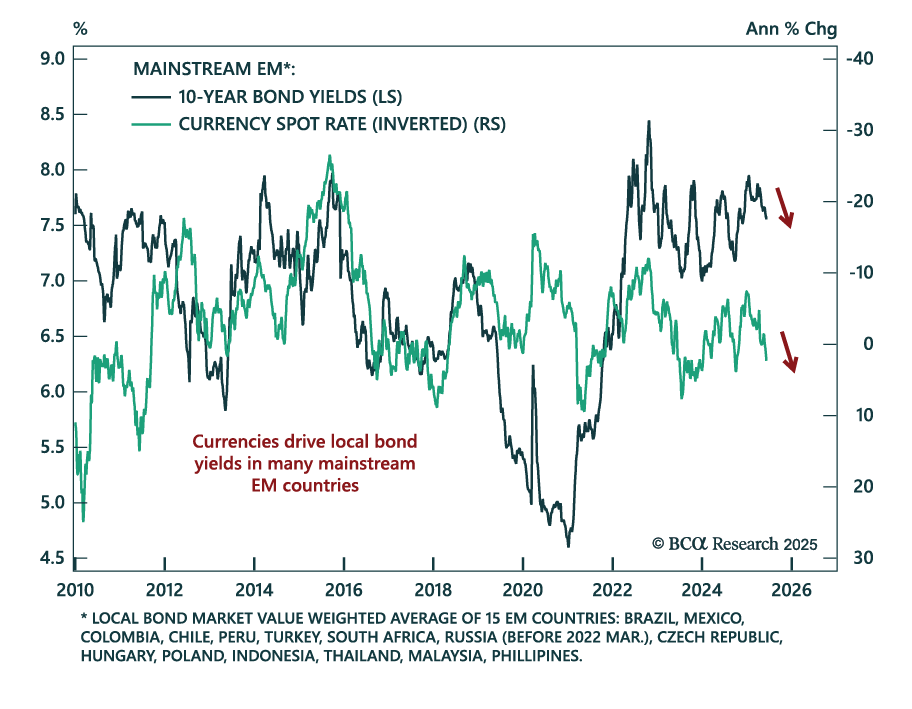

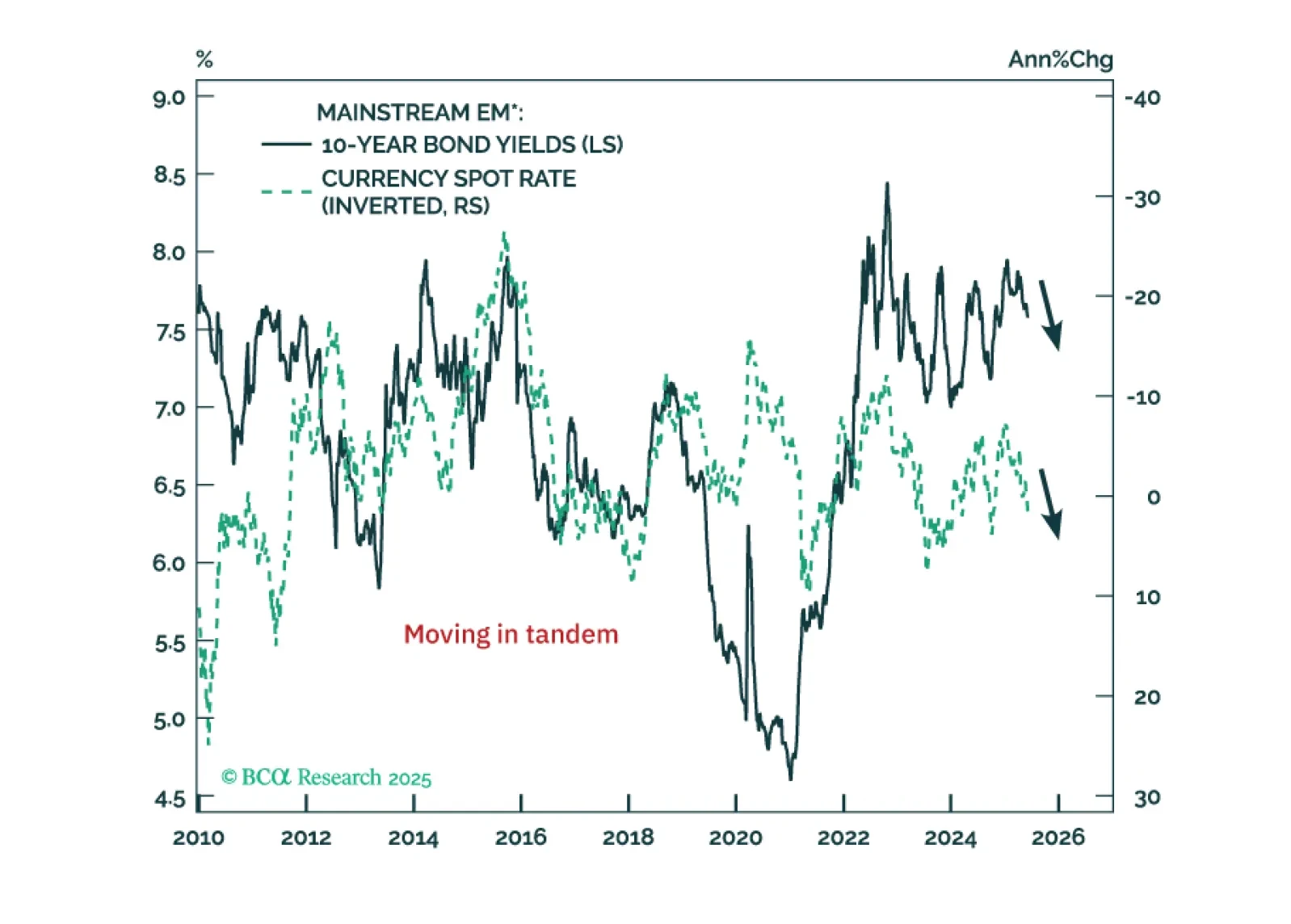

BCA’s EM strategists argue that a global macro shift is underway: A weaker US dollar will drive a retrenchment in US domestic demand and imports. Unlike previous cycles, dollar depreciation will be deflationary for the rest of the world rather than…

Unlike in past episodes, US dollar weakness will be deflationary, not reflationary, for the rest of the world. In this context, EM local currency bonds offer a superior risk-reward profile. Stay long domestic bonds in select EM countries.

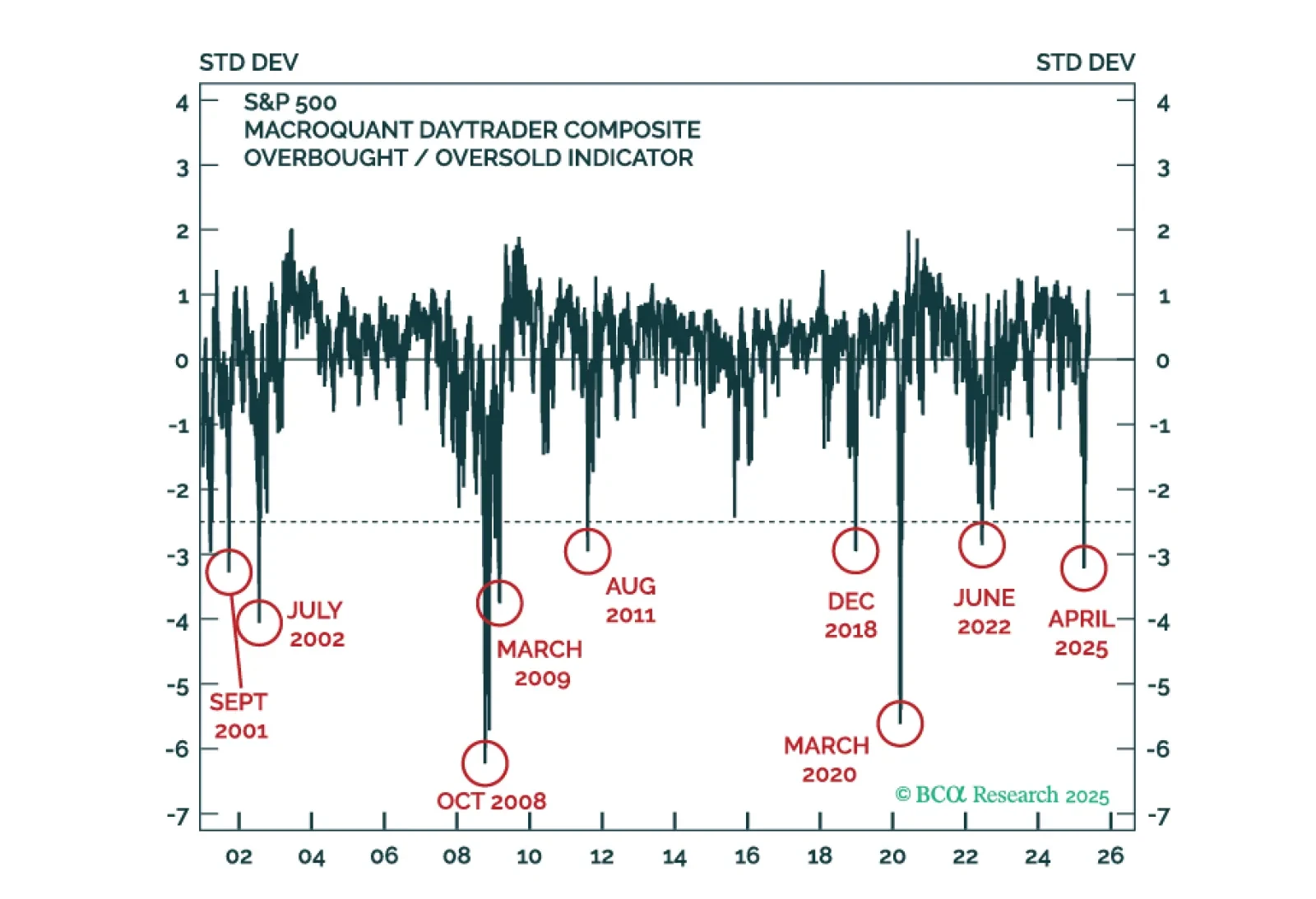

MacroQuant warns that US equities are pricing in very little economic risk. The model is shunning equities and recommends a large overweight to cash.

MacroQuant warns that US equities are pricing in very little economic risk. The model is shunning equities and recommends a large overweight to cash.

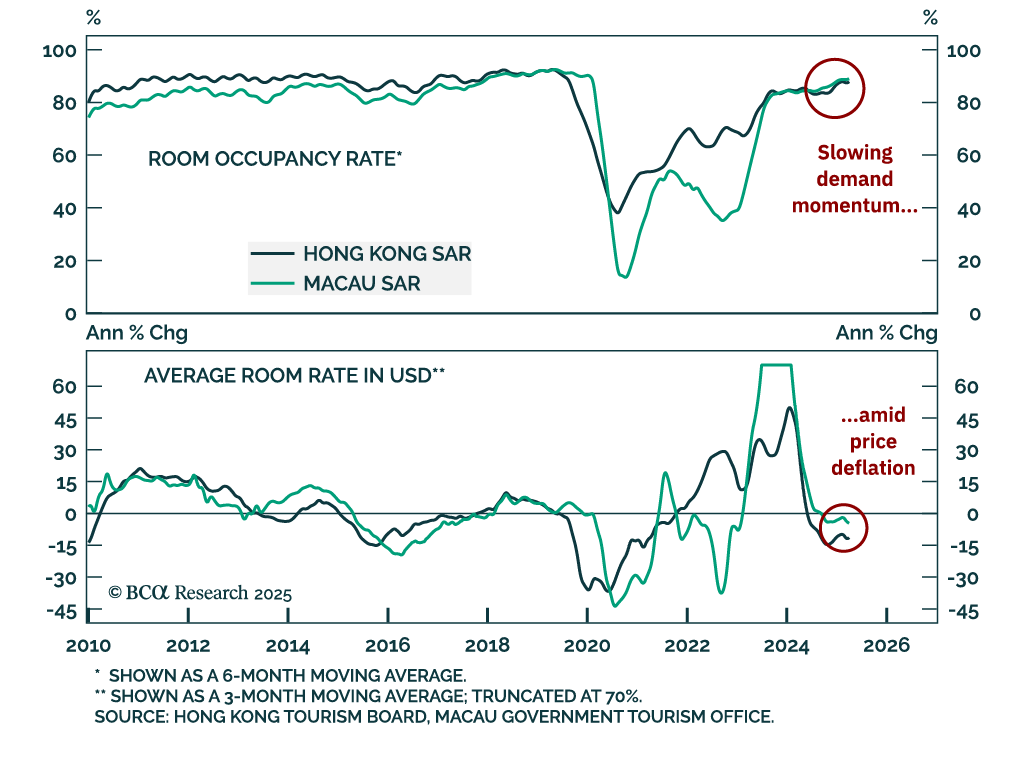

China’s tourism sector has rebounded meaningfully since the January 2023 COVID reopening; however, investors should not be complacent about the outlook for tourism stocks. The double-digit revenue growth of the Chinese tourism industry over the past…