Emerging Markets

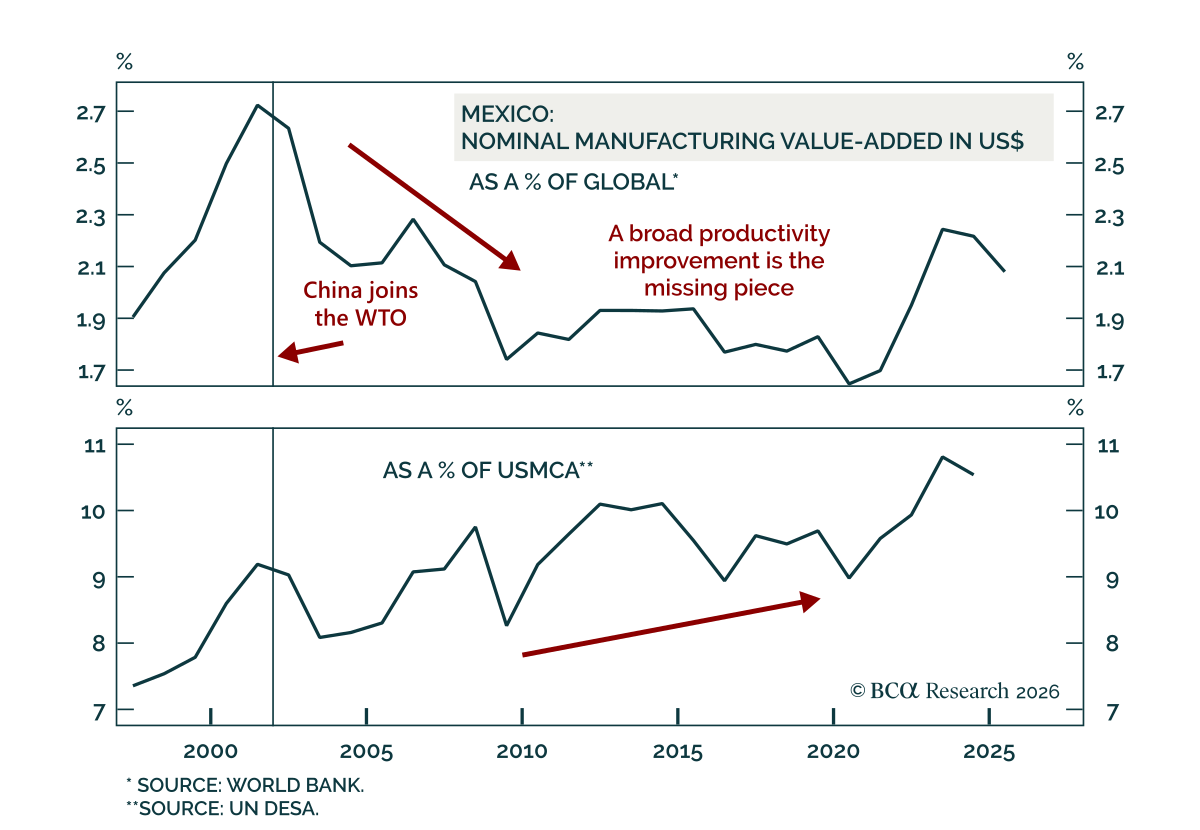

Mexico still looks attractive on a cyclical horizon, but the lack of productivity growth argues against a secular bull market. Our Chart Of The Week comes from Max Malak, from our Emerging Markets team. Our EM team is bullish on Mexican assets: Tariff…

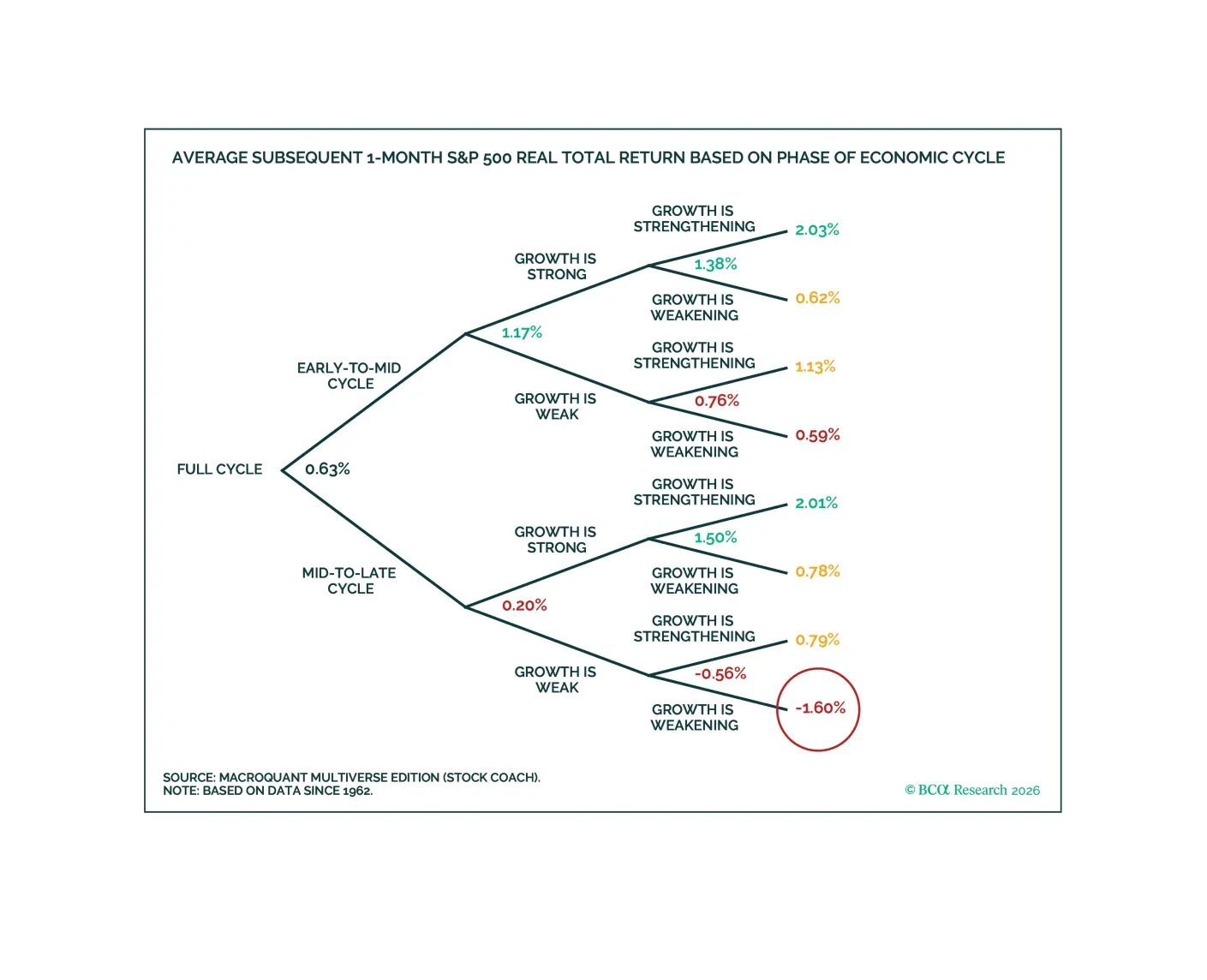

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

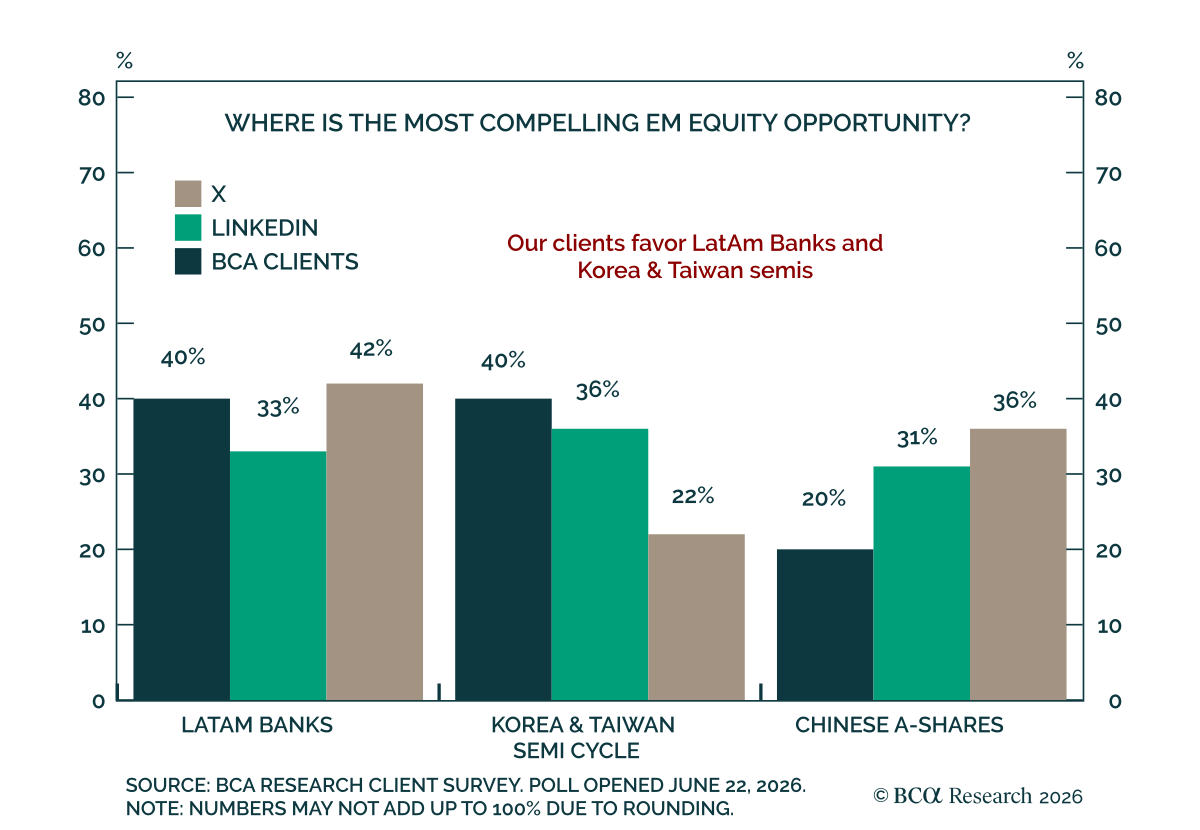

Our clients are most constructive on LatAm Banks and the Korea & Taiwan semi cycle. In last week's poll, we asked where investors see the greatest upside across three EM themes. BCA clients are split evenly between LatAm Banks and Korea & Taiwan (40%…

Our EM strategists view Korea’s equity tantrum as a warning for global risk assets and recommend taking profits and downgrading Korean stocks. Korea has become the most extreme expression of the global equity rally, driven by semiconductor momentum, high-beta…

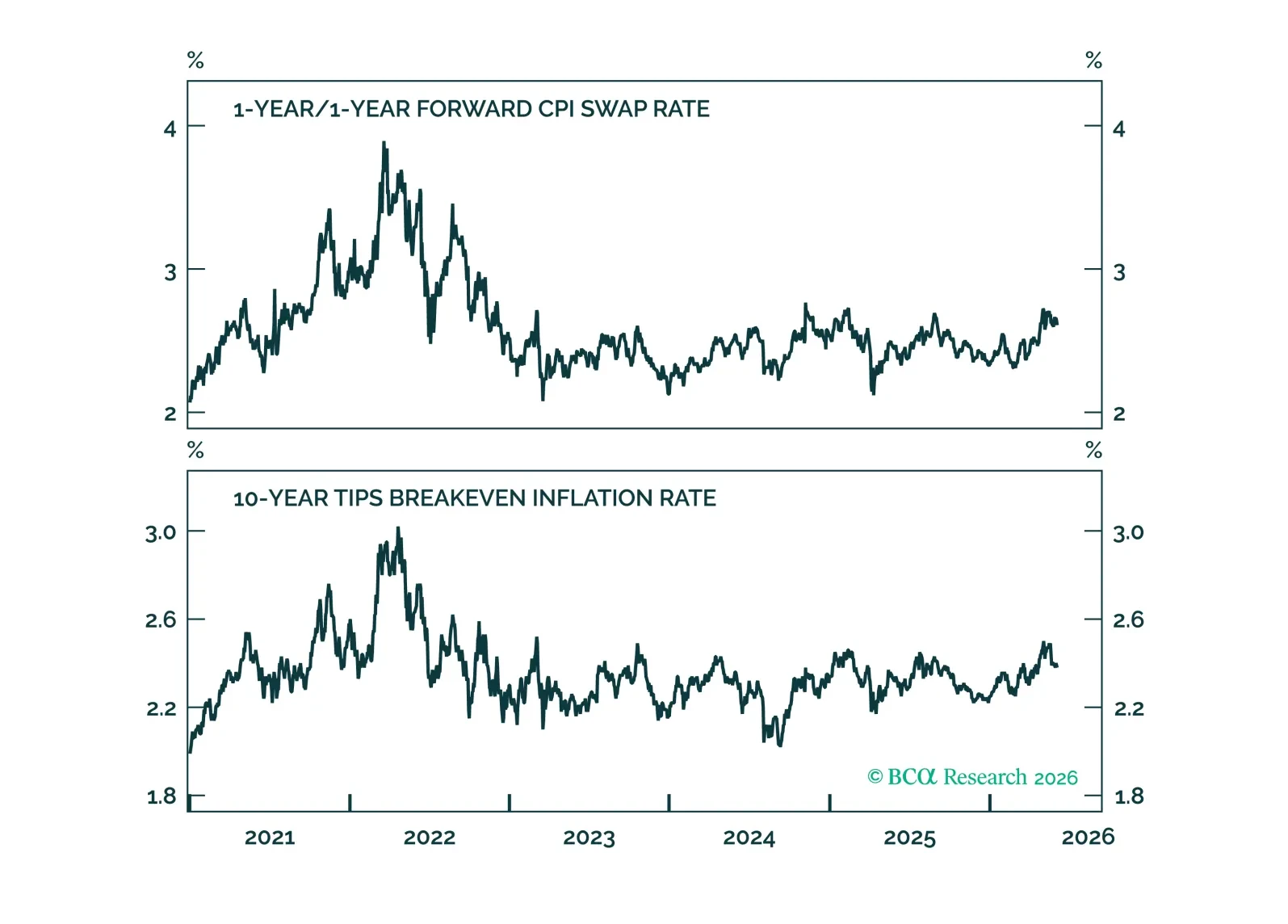

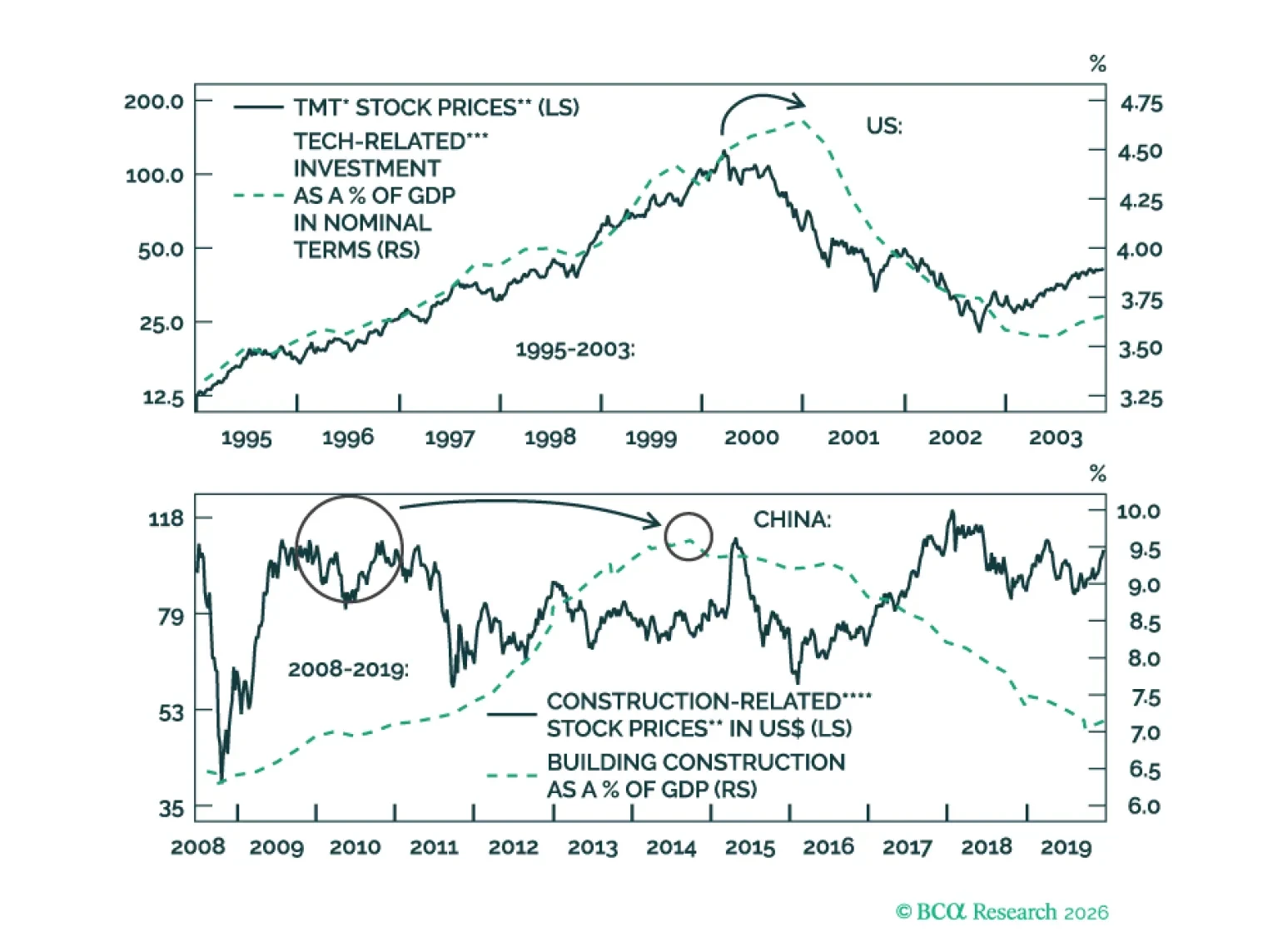

AI is transformative, yet tech stocks may not produce positive returns. Market cycles have not disappeared. Greed and fear will still produce large share price fluctuations. Meanwhile, US inflation is the key near-term risk. Global non-tech capex aspirations also look overstated.

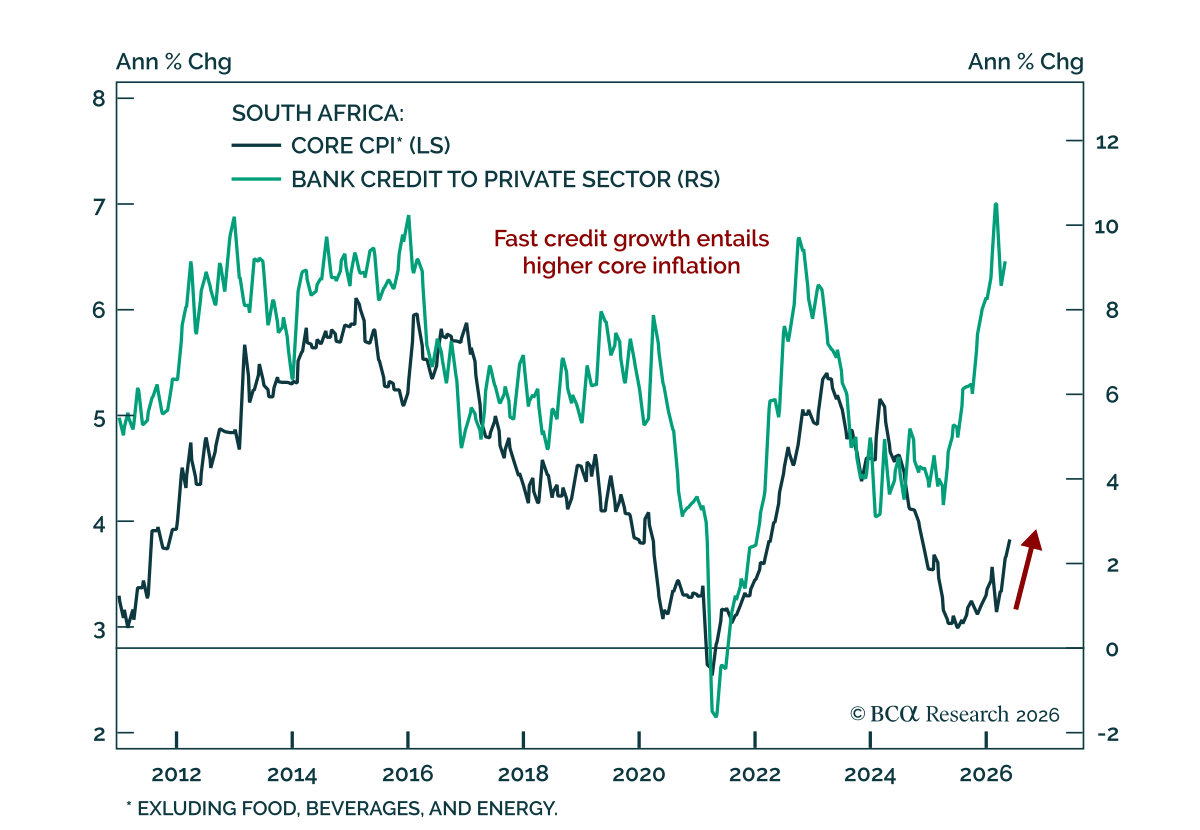

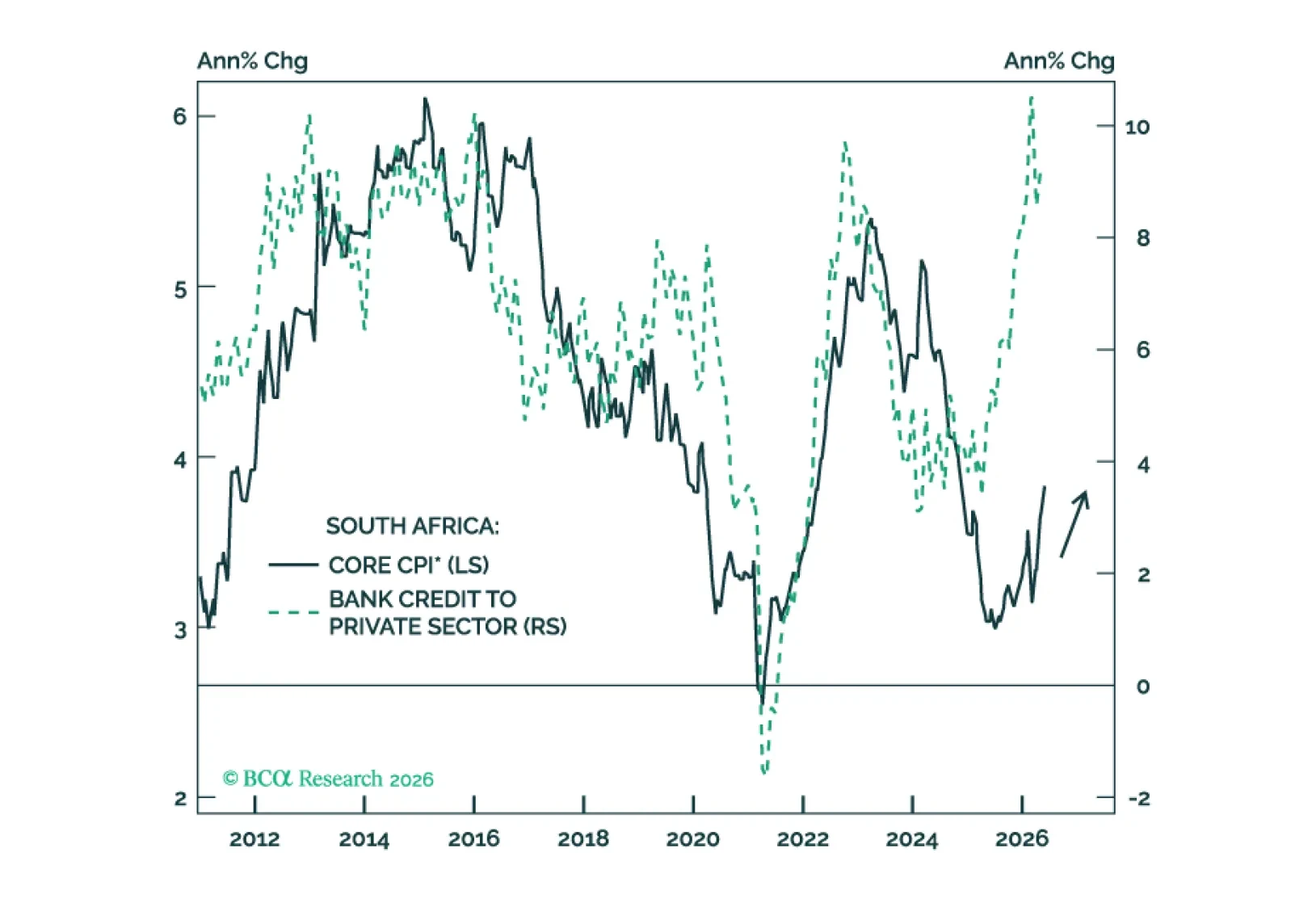

Our EM strategists warn that South African assets are vulnerable to a stagflationary squeeze. Although reform efforts are ambitious, they are slow to materialize as the country faces rising inflation and slowing growth. Higher energy and food prices as well…

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

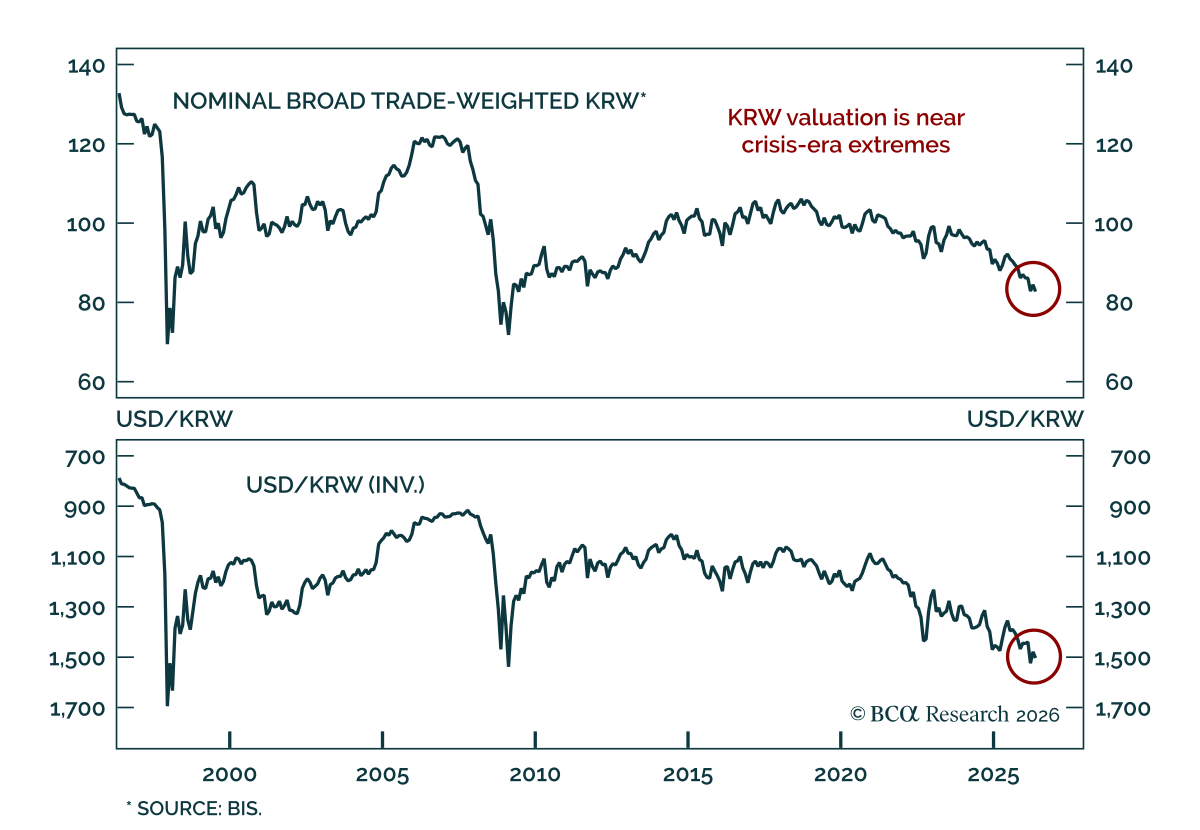

Our FX and EM strategists see the Korean won as increasingly mispriced, and recommend positioning for appreciation. KRW weakness is driven by unfavorable portfolio flows, not by any deterioration in Korea's growth or external position. Flow-driven weakness of…