Elections

Highlights So What? Our best and worst calls of 2018 cast light on our methodology and 2019 forecasts. Why? Our clients took us to task for violating our own methodology on the Iranian oil sanctions. Sticking to our guns would have paid off with long Russian equities versus EM. We correctly called China’s domestic policy, the U.S.-China trade war, Europe, the U.S. midterms, and relative winners in emerging markets. Feature It has been a tradition for BCA’s Geopolitical Strategy, since our launch in 2012, to highlight our best and worst forecasts of the year.1 This will also be the final publication of the year, provided that there is no global conflagration worthy of a missive between now and January 9, when we return to our regular publication schedule. We wish all of our clients a great Holiday Season. And especially all the very best in 2019: lots of happiness, health, and hefty returns. Good luck and good hunting. The Worst Calls Of 2018 A forecasting mistake is wasted if one learns nothing from the error. This is why we take our mistakes seriously and why we always begin the report card with our zingers. Our overall performance in 2018 was … one of our best. The successes below will testify to this. However, we made three notable errors. A Schizophrenic Russia View Our worst call of the year was to panic and close our long Russian equities relative to emerging markets trade in the face of headline geopolitical risks. In early March, we posited that Russia was a “buy” relative to the broad EM equity index due to a combination of cheap valuations, strong macro fundamentals, orthodox policy, and an end to large-scale geopolitical adventurism. This call ultimately proved to be correct (Chart 1). Chart 1Russian Stocks Outperformed In The End

Russian Stocks Outperformed In The End

Russian Stocks Outperformed In The End

What went wrong? The main risk to our view, that the U.S. Congress would pursue an anti-Russia agenda regardless of any Russian sympathies in the Trump White House, materialized in the wake of the poisoning of former Russian military intelligence officer Sergei Skripal with a Novichok nerve agent in the United Kingdom. As fate would have it, the incident occurred just before our bullish report went to clients! The ensuing international uproar and sanctions caused a selloff. Our bullish thesis did not rest exclusively on geopolitics, but a thaw in West-Russia relations did form the main pillar of the view. Our Russia Geopolitical Risk Index, which had served us well in the past, was pricing as low of a level of geopolitical risk as one could hope for in the post-Crimea environment (Chart 2). Naturally the measure jumped into action following the Skripal incident. Chart 2Geopolitical Risk Was Low Prior To Skripal

Geopolitical Risk Was Low Prior To Skripal

Geopolitical Risk Was Low Prior To Skripal

The timing of our call was therefore off, but we should have stuck with the overall view. The U.S. imposed preliminary sanctions that lacked teeth. While Washington accepted the U.K.’s assessment that Moscow was behind the poisoning, the weakness of the sanctions also signaled that the U.S. did not consider the incident worthy of a tougher position. There are now two parallel sanction processes under way. The first round of sanctions announced in August gave Russia 90 days to comply and adopt “remedial measures” regarding the use of chemical and biological weapons. On November 9, the U.S. State Department noted that Russia had not complied with the deadline. The U.S. is now expected to impose a second round of sanctions that will include at least three of six punitive actions: Opposition to development aid and assistance by international financial institutions (think the IMF and the World Bank); Downgrading diplomatic relations; Additional restrictions on exports to Russia (high-tech exports have already been barred by the first round of sanctions); Restrictions on imports from Russia; A ban on landing rights in the U.S. for Russian state-owned airlines; Prohibiting U.S. banks from purchasing Russian government debt. While the White House was expected to have such sanctions ready to go on the November 9 deadline, it has dragged its feet for almost two months now. This suggests that President Trump continues to hold out for improved relations with President Putin. A visit by President Putin to Washington remains possible in Q1 2019. As such, we would expect the White House to adopt some mix of the first five items on the above list, hardly a crushing response from Moscow’s perspective. The U.S. Congress, however, has a parallel process in the form of the Defending American Security from Kremlin Aggression Act of 2018 (DASKAA). Introduced in August by Senator Lindsey Graham, a Russia hawk, the legislation would put restrictions on Americans buying Russian sovereign debt and curb investments in Russian energy projects. The bill also includes secondary sanctions on investing in the Russian oil sector, which would potentially ensnare European energy companies collaborating with Russia in the energy sector. There was some expectation that Congress would take up the bill ahead of the midterm election, but nothing came of it. Even with the latest incident – the seizing of two Ukrainian naval vessels in the Kerch Strait – we have yet to see action. While we expect the U.S. to do something eventually, the White House approach is likely to be tepid while the congressional approach may be too draconian to pass into law. And with Democrats about to take over the House, and likely demand even tougher sanctions against Russia, the ultimate legislation may be too bold for President Trump to sign into legislation. The point is that Russia has acted antagonistically towards the West in 2018, but in small enough increments that the response has been tepid. Given the paucity of Russian financial and trade links with the U.S., Washington’s sanctions would only bite if they included the dreaded “secondary sanction” implications for third party sovereigns and firms – particularly European, which do have a lot of business in Russia. This is highly unlikely without major Russian aggression. We cannot completely ignore the potential for such aggression in 2019, especially with President Putin’s popularity in the doldrums (Chart 3) and a contentious Ukrainian election due for March 31. However, we outlined the constraints against Russia in 2014, amidst the Ukrainian crisis, and we do not think that these constraints have been reduced (they may have only grown since then). Chart 3Non-Negligible Risk Of Russian Aggression

Non-Negligible Risk Of Russian Aggression

Non-Negligible Risk Of Russian Aggression

Regardless of the big picture for 2019, we could have faded the risks in 2018 and stuck to the fundamentals. Russia is up 17.2% against EM year-to-date. The lesson here, therefore, is to find re-entry points into a well-founded view despite market volatility. Chart 1 shows that Russian equities climbed the proverbial “wall of worry” relative to EM in 2018. Doubting Jair Bolsonaro Our list of mistakes keeps us in the EM universe where we underestimated Jair Bolsonaro’s chances of winning the presidency in Brazil. The answer to the question we posed in the title of our September report – “Brazil: Can The Election Change Anything?” – was a definitive “yes.” Since the publication of that report, BRL/USD is up 2.9% and Brazilian equities are up 18.5% relative to EM (Chart 4). Chart 4Bolsonaro Rally Losing Its Luster Already

Bolsonaro Rally Losing Its Luster Already

Bolsonaro Rally Losing Its Luster Already

To our credit, the question of Bolsonaro’s electoral chances elicited passionate and pointed internal debate. But our clients did not see the internal struggle, just the incorrect external output! A bad call is a bad call, no matter how it is assembled on the intellectual assembly line. That said, we still think that our report is valuable. It sets out the constraints facing Bolsonaro in 2019. He has to convince the left-leaning median voter that meaningful pension reform is needed; bully a fractured Congress into painful structural reforms; and overcome an unforgiving macro context of tepid Chinese stimulus and a strong USD. If the Bolsonaro administration wastes the good will of the investment community over the next six months, we expect the market’s punishment to be swift and painful. In fact, Chart 4 notes that the initial Bolsonaro rally has already lost most of its shine. Brazilian assets are still up since the election, but the gentle slope could become a steep fall if Bolsonaro stumbles. The market is priced for political perfection. To be clear, we are not bearish on Bolsonaro. We believe that, relative to EM, he will be a positive for Brazil. However, the market is currently betting that he will win by two touchdowns, whereas we think he will squeak by with a last-second field goal. The difference between the two forecasts is compelling and we have expressed it by being long MXN/BRL.2 Not Sticking To Our Method In The Case Of Iran Throughout late-2017 and 2018 we pointed out that President Trump’s successful application of “maximum pressure” against North Korea could become a market-relevant risk if he were emboldened to try the same strategy against Iran. For much of the year, this view was prescient. As investors realized the seriousness of President Trump’s strategy, a geopolitical risk premium began to seep into oil prices, as illustrated in Chart 5 by the red bar.

Chart 5

Every time we spoke to clients or published reports on this topic, we highlighted just how dangerous a “maximum pressure” strategy would be in the case of Iran. We stressed that Iran could wreak havoc across Iraq and other parts of the Middle East and even drive up oil prices to the point of causing a “geopolitical recession in 2019.” In other words, we stressed the extraordinary constraints that President Trump would face. To their credit many of our clients called us out on the inconsistency: our market call was über bullish oil prices, while our methodology emphasized constraints over preferences. We were constantly fielding questions such as: Why would President Trump face down such overwhelming constraints? We did not have a very good answer to this question other than that he was ideologically committed to overturning the Iranian nuclear deal. In essence, we doubted President Trump’s own ideological flexibility and realism. That was a mistake and we tip our hat to the White House for recognizing the complex constraints arrayed against it. President Trump realized by October how dangerous those constraints were and began floating the idea of sanction waivers, causing the geopolitical risk premium to drain from the market (Chart 6). To our credit, we highlighted sanction waivers as a key risk to our view and thus took profit on our bullish energy call early. Chart 6Sanction Waivers Caused A Collapse In Oil Prices

Sanction Waivers Caused A Collapse In Oil Prices

Sanction Waivers Caused A Collapse In Oil Prices

That said, our clients have taken the argument further, pointing out that if we were wrong on Trump’s ideological flexibility with Iran, we may be making the same mistake when it comes to China. However, there is a critical difference. Americans are more concerned about conflict with North Korea than with Iran (Chart 7), while China is the major concern about trade (Chart 8).

Chart 7

Chart 8

Second, railing against the Iran deal did not get President Trump elected, whereas his protectionist rhetoric – specifically regarding China – did (Chart 9). Getting anything less than the mother-of-all-deals with Beijing will draw down Trump’s political capital ahead of 2020 and open him to accusations of being “weak” and “surrendering to China.” These are accusations that the country’s other set of protectionists – the Democrats – will wantonly employ against him in the next general election. Chart 9Protectionism, Not Iran, Helped Trump Get Elected

Protectionism, Not Iran, Helped Trump Get Elected

Protectionism, Not Iran, Helped Trump Get Elected

Ultimately, if we have to be wrong, we are at least satisfied that our method stood firm in the face of our own fallibility. We are doubly glad to see our clients using our own method against our views. This is precisely what we wanted to accomplish when we began BCA’s Geopolitical Strategy in March 2012: to revolutionize finance by raising the sophistication with which it approaches geopolitics. That was a lofty goal, but we do not pretend to hold the monopoly on our constraint-based methodology. In the end, our market calls did not suffer due to our error. We closed our long EM energy-producer equities / EM equities for a gain of 4.67% and our long Brent / short S&P 500 for a gain of 6.01%. However, our latter call, shorting the S&P 500 in September, was based on several reasons, including concerns regarding FAANG stocks, overstretched valuations, and an escalation of the trade war. Had we paired our S&P 500 short with a better long, we would have added far more value to our clients. It is that lost opportunity that has kept us up at night throughout this quarter. We essentially timed the S&P 500 correction, but paired it with a wayward long. The Best Calls Of 2018 BCA’s Geopolitical Strategy had a strong year. We are not going to list all of our calls here, but only those most relevant to our clients. Our best 2018 forecast originally appeared in 2017, when in April of that year we predicted that “Political Risks Are Understated In 2018.” Our reasoning was bang on: U.S. fiscal policy would turn strongly stimulative (the tax cuts would pass and Trump would be a big spender) and thus cause the Fed to turn hawkish and the USD to rally, tightening global monetary policy; Trump’s trade war would re-emerge in 2018; China would reboot its structural reform efforts by focusing on containing leverage, thus tightening global “fiscal” policy. In the same report we also predicted that Italian elections in 2018 would reignite Euro Area breakup risks, but that Italian policymakers would ultimately be found to be bluffing, as has been our long-running assertion. Throughout 2018, our team largely maintained and curated the forecasts expressed in that early 2017 report. We start the list of the best calls with the one call that was by far the most important for global assets in 2018: economic policy in China. The Chinese Would Over-Tighten, Then Under-Stimulate Getting Chinese policy right required us, first, to predict that policy would bring negative economic surprises this year, and second, once policy began to ease, to convince clients and colleagues that “this time would be different” and the stimulus would not be very stimulating. In other words, this time, China would not panic and reach for the credit lever of the post-2008 years (Chart 10), but would maintain its relatively tight economic, financial, environmental, and macro-prudential oversight, while easing only on the margin. Chart 10No Massive Credit Stimulus In 2018

No Massive Credit Stimulus In 2018

No Massive Credit Stimulus In 2018

This is precisely what occurred. BCA Foreign Exchange Strategy’s “China Play Index,” which is designed to capture any reflation out of Beijing, collapsed in 2018 and has hardly ticked up since the policy easing announced in July (Chart 11). Chart 11Weak Reflation Signal From China

Weak Reflation Signal From China

Weak Reflation Signal From China

Our view was based on an understanding of Chinese politics that we can confidently say has been unique: From March 2017, we highlighted the importance of the 2017 October Party Congress, arguing that President Xi Jinping would consolidate his power and redouble his attempts to “reform” the economy by reining in dangerous imbalances. We explicitly characterized the containment of leverage as the most market-relevant reform to focus on. We stringently ignored the ideological debate about the nature of reform in China, focusing instead on the major policy changes afoot. We identified very early on how the rising odds of a U.S.-China conflict would embolden Chinese leadership to double-down on painful structural reforms. Will China maintain this disciplined approach in 2019? That is yet to be seen. But we are arming ourselves and clients with critical ways to identify when and whether Beijing’s policy easing transforms into a full-blown “stimulus overshoot”: First, we need to see a clear upturn in shadow financing to believe that the Xi administration has given up on preventing excess debt. Assuming that such a shift occurs, and that overall credit improves, it will enable us to turn bullish on global growth and global risk assets on a cyclical, i.e., not merely tactical, horizon (Chart 12). Chart 12A Shadow Lending Surge Would Mean A Big Policy Shift

A Shadow Lending Surge Would Mean A Big Policy Shift

A Shadow Lending Surge Would Mean A Big Policy Shift

Second, our qualitative checklist will need to see a lot more “checks” in order to change our mind. Short of an extraordinary surge in bank and shadow bank credit, there needs to be a splurge in central and especially local government spending (Table 1). The mid-year spike in local governments’ new bond issuance in 2018 was fleeting and fell far short of the surge that initiated the large-scale stimulus of 2015. Frontloading these bonds in 2019 will depend on timing and magnitude. Table 1A Credit Splurge, Or Government Spending Splurge, Is Necessary For Stimulus To Overshoot

BCA Geopolitical Strategy 2018 Report Card

BCA Geopolitical Strategy 2018 Report Card

Third, we would need to see President Xi Jinping make a shift in rhetoric away from the “Three Battles” of financial risk, pollution, and poverty. Having identified systemic financial risk as the first of the three ills, Xi needs to make a dramatic reversal of this three-year action plan if he is to clear the way for another credit blowout. Trade War Would Reignite In 2018 It paid off to stick with our trade war alarmism in 2018. We correctly forecast that the U.S. and China would collide over trade and that their initial trade agreement – on May 20 – was insubstantial and would not last. In the event it lasted three days. Our one setback on the trade front was to doubt the two sides would agree to a trade truce at the G20. However, by assigning a subjective 40% probability, we correctly noted the fair odds of a truce. We also insisted that any truce would be temporary, which ended up being the case. We may yet be vindicated if the March 1 deadline produces no sustainable deal, as we forecast in last week’s Strategic Outlook. That said, correct geopolitical calls do not butter our bread at BCA. Rather, we are paid to make market calls. To that end, we would point out that we correctly assessed the market-relevance of the trade conflict, fading S&P 500 risks and focusing on the effect on global risk assets. Will this continue into 2019? We think so. We do not see trade conflict as the originator of ongoing market turbulence (Chart 13) and would expect the U.S. to outperform global equities again over the course of 2019 (Chart 14). This view may appear wrong in Q1, as the market digests the Fed backing off from hawkish rhetoric, the ongoing trade negotiations, and the likely seasonal uptick in Chinese credit data in the beginning of the calendar year. Chart 13Yields, Not Trade War, Drove Stocks

Yields, Not Trade War, Drove Stocks

Yields, Not Trade War, Drove Stocks

Chart 14U.S. Stocks Will Resume Outperformance

U.S. Stocks Will Resume Outperformance

U.S. Stocks Will Resume Outperformance

However, any stabilization in equity markets would likely serve to ease financial conditions in the U.S., where economic and inflation conditions remain firmly in tightening territory (Chart 15). As such, the Fed pause is likely to last no more than a quarter, maybe two at best, leading to renewed carnage in global risk assets if our view on Chinese policy stimulus – tepid – remains valid through the course of 2019. Chart 15If Financial Conditions Ease, Tightening Will Be Back On

If Financial Conditions Ease, Tightening Will Be Back On

If Financial Conditions Ease, Tightening Will Be Back On

Europe (All Of It… Again) In 2017, our forecasting track record for Europe was stellar. This continued in 2018, with no major setbacks: Populism in Italy: Our long-held view has been that Europe’s chief remaining risks lay in Italian populists coming to power. We predicted in 2016 that this would eventually happen and that they would then be proven to be bluffing. This is essentially what happened in 2018. Matteo Salvini’s Lega is surging in the polls because its leader has realized that a combination of hard anti-immigrant policy and the softest-of-soft Euroskepticism is a winning combination. We believe that investors can live with this combination. Our only major fault in forecasting European politics and assets this year was to close our bearish Italy call too early: we booked our long Spanish / short Italian 10-year government bond trade for a small loss in August, before the spread between the two Mediterranean countries blew out to record levels. That missed opportunity could have also made it on our “worst calls” list as well.

Chart 16

Pluralism in Europe: To get the call on Italy right, we had to dabble in some theoretical work. In a somewhat academic report, we showed that political concentration was on the decline in the developed world (Chart 16), but especially in Europe (Chart 17). Put simply, lower political concentration suggests that a duopoly between the traditional center-left and center-right parties is breaking down. Contrary to the conventional wisdom, we argued that Europe’s parliamentary systems would enable centrist parties to adopt elements of the populist agenda, particularly on immigration, without compromising the overall stability of European institutions. As such, political pluralism, or low political concentration, is positive for markets.

Chart 17

Immigration crisis is over: For centrist parties to be able to successfully adopt populist immigration policy, they needed a pause in the immigration crisis. This was empirically verifiable in 2018 (Chart 18). Chart 18European Migration Crisis Is Over

European Migration Crisis Is Over

European Migration Crisis Is Over

Merkel’s time has run out: Since early 2017, we had cautioned clients that Angela Merkel’s demise was afoot, but that it would be an opportunity, rather than a risk, when it came. It finally happened in 2018 and it was not a market moving event. The main question for 2019 is whether German policymakers, and Europe as a whole, will use the infusion of fresh blood in Berlin to reaccelerate crucial reforms ahead of the next global recession. Brexit: Since early 2016, we have been right on Brexit. More specifically, we were corrent in cautioning investors that, were Brexit to occur, “the biggest loser would be the Conservative Party, not the EU.” As with the previous two Conservative Party prime ministers, it appears that the question of the U.K.’s relationship with the EU has completely drained any political capital out of Prime Minister Theresa May’s reign. We suspect that the only factor propping up the Tories in the polls is that Jeremy Corbyn is the leader of Her Majesty’s Most Loyal Opposition. We have also argued that soft Brexit would ultimately prove to be “illogical” and that “Bregret” would begin to seep in, as it now most clearly has. We parlayed these rising geopolitical risks and uncertainties by shorting cable in the first half of the year for a 6.21% gain. Malaysia Over Turkey And India Over Brazil Not all was lost for our EM calls this year. We played Malaysia against Turkey in the currency markets for a 17.44% gain, largely thanks to massively divergent governance and structural reform trajectories after Malaysia’s opposition won power for the first time in the country’s history. Second, we initiated a long Indian / short Brazilian equity view in March that returned 27.54% by August. This was a similar play on divergent structural reforms, but it was also a way to hedge our alarmist view on trade. Given India’s isolation from global trade and insular financial markets, we identified India as one of the EM markets that would remain aloof of protectionist risks. We could have closed the trade earlier for greater gain, but did not time the exit properly. Midterm Election: A Major Democratic Victory Our midterm election forecast was correct: Democrats won a substantial victory. Even our initial call on the Senate, that Democrats had a surprisingly large probability of picking up seats, proved to be correct, with Republicans eking out just two gains in a year when Democrats were defending 10 seats in states that Trump carried in 2016. What about our all-important call that the election would have no impact on the markets? That is more difficult to assess, given that the S&P 500 has in fact collapsed in the lead-up to and aftermath of the election. However, we see little connection between the election outcome and the stock market’s performance. Neither do our colleagues or clients, who have largely stopped asking about the Democrats’ policy designs. In 2019, domestic politics may play a role in the markets. Impeachment risk is low, but, if it rears its head, it could prompt President Trump to seek relevance abroad, as his predecessors have done when they lost control of domestic policy. In addition, the Democratic Party’s sweeping House victory may suggest a political pendulum swing to the left in the 2020 presidential election. We will discuss both risks as part of our annual Five Black Swans report in early 2019. U.S. domestic politics was a collection of Red Herrings during much of President Obama’s presidency, and has produced strong tailwinds under President Trump (tax cuts in particular). This may change in 2019, with considerable risk to investors, and asset prices, ahead. Marko Papic, Senior Vice President Chief Geopolitical Strategist marko@bcaresearch.com Matt Gertken, Vice President Geopolitical Strategy mattg@bcaresearch.com Roukaya Ibrahim, Editor/Strategist roukayai@bcaresearch.com Ekaterina Shtrevensky, Research Analyst ekaterinas@bcaresearch.com Footnotes 1 For our 2019 Outlook, please see BCA Geopolitical Strategy Strategic Outlook, “2019 Key Views: Balanced On A Knife’s Edge,” dated December 14, 2018, available at gps.bcaresearch.com. For our past Strategic Outlooks, please visit gps.bcaresearch.com. 2 In part we like this cross because we also think that Mexico’s newly elected president, Andrés Manuel López Obrador, is priced to lose by two touchdowns, whereas he may merely lose by a last-second field goal.

Highlights So What? Our best and worst calls of 2018 cast light on our methodology and 2019 forecasts. Why? Our clients took us to task for violating our own methodology on the Iranian oil sanctions. Sticking to our guns would have paid off with long Russian equities versus EM. We correctly called China’s domestic policy, the U.S.-China trade war, Europe, the U.S. midterms, and relative winners in emerging markets. Feature It has been a tradition for BCA’s Geopolitical Strategy, since our launch in 2012, to highlight our best and worst forecasts of the year.1 This will also be the final publication of the year, provided that there is no global conflagration worthy of a missive between now and January 9, when we return to our regular publication schedule. We wish all of our clients a great Holiday Season. And especially all the very best in 2019: lots of happiness, health, and hefty returns. Good luck and good hunting. The Worst Calls Of 2018 A forecasting mistake is wasted if one learns nothing from the error. This is why we take our mistakes seriously and why we always begin the report card with our zingers. Our overall performance in 2018 was … one of our best. The successes below will testify to this. However, we made three notable errors. A Schizophrenic Russia View Our worst call of the year was to panic and close our long Russian equities relative to emerging markets trade in the face of headline geopolitical risks. In early March, we posited that Russia was a “buy” relative to the broad EM equity index due to a combination of cheap valuations, strong macro fundamentals, orthodox policy, and an end to large-scale geopolitical adventurism. This call ultimately proved to be correct (Chart 1). Chart 1Russian Stocks Outperformed In The End

Russian Stocks Outperformed In The End

Russian Stocks Outperformed In The End

What went wrong? The main risk to our view, that the U.S. Congress would pursue an anti-Russia agenda regardless of any Russian sympathies in the Trump White House, materialized in the wake of the poisoning of former Russian military intelligence officer Sergei Skripal with a Novichok nerve agent in the United Kingdom. As fate would have it, the incident occurred just before our bullish report went to clients! The ensuing international uproar and sanctions caused a selloff. Our bullish thesis did not rest exclusively on geopolitics, but a thaw in West-Russia relations did form the main pillar of the view. Our Russia Geopolitical Risk Index, which had served us well in the past, was pricing as low of a level of geopolitical risk as one could hope for in the post-Crimea environment (Chart 2). Naturally the measure jumped into action following the Skripal incident. Chart 2Geopolitical Risk Was Low Prior To Skripal

Geopolitical Risk Was Low Prior To Skripal

Geopolitical Risk Was Low Prior To Skripal

The timing of our call was therefore off, but we should have stuck with the overall view. The U.S. imposed preliminary sanctions that lacked teeth. While Washington accepted the U.K.’s assessment that Moscow was behind the poisoning, the weakness of the sanctions also signaled that the U.S. did not consider the incident worthy of a tougher position. There are now two parallel sanction processes under way. The first round of sanctions announced in August gave Russia 90 days to comply and adopt “remedial measures” regarding the use of chemical and biological weapons. On November 9, the U.S. State Department noted that Russia had not complied with the deadline. The U.S. is now expected to impose a second round of sanctions that will include at least three of six punitive actions: Opposition to development aid and assistance by international financial institutions (think the IMF and the World Bank); Downgrading diplomatic relations; Additional restrictions on exports to Russia (high-tech exports have already been barred by the first round of sanctions); Restrictions on imports from Russia; A ban on landing rights in the U.S. for Russian state-owned airlines; Prohibiting U.S. banks from purchasing Russian government debt. While the White House was expected to have such sanctions ready to go on the November 9 deadline, it has dragged its feet for almost two months now. This suggests that President Trump continues to hold out for improved relations with President Putin. A visit by President Putin to Washington remains possible in Q1 2019. As such, we would expect the White House to adopt some mix of the first five items on the above list, hardly a crushing response from Moscow’s perspective. The U.S. Congress, however, has a parallel process in the form of the Defending American Security from Kremlin Aggression Act of 2018 (DASKAA). Introduced in August by Senator Lindsey Graham, a Russia hawk, the legislation would put restrictions on Americans buying Russian sovereign debt and curb investments in Russian energy projects. The bill also includes secondary sanctions on investing in the Russian oil sector, which would potentially ensnare European energy companies collaborating with Russia in the energy sector. There was some expectation that Congress would take up the bill ahead of the midterm election, but nothing came of it. Even with the latest incident – the seizing of two Ukrainian naval vessels in the Kerch Strait – we have yet to see action. While we expect the U.S. to do something eventually, the White House approach is likely to be tepid while the congressional approach may be too draconian to pass into law. And with Democrats about to take over the House, and likely demand even tougher sanctions against Russia, the ultimate legislation may be too bold for President Trump to sign into legislation. The point is that Russia has acted antagonistically towards the West in 2018, but in small enough increments that the response has been tepid. Given the paucity of Russian financial and trade links with the U.S., Washington’s sanctions would only bite if they included the dreaded “secondary sanction” implications for third party sovereigns and firms – particularly European, which do have a lot of business in Russia. This is highly unlikely without major Russian aggression. We cannot completely ignore the potential for such aggression in 2019, especially with President Putin’s popularity in the doldrums (Chart 3) and a contentious Ukrainian election due for March 31. However, we outlined the constraints against Russia in 2014, amidst the Ukrainian crisis, and we do not think that these constraints have been reduced (they may have only grown since then). Chart 3Non-Negligible Risk Of Russian Aggression

Non-Negligible Risk Of Russian Aggression

Non-Negligible Risk Of Russian Aggression

Regardless of the big picture for 2019, we could have faded the risks in 2018 and stuck to the fundamentals. Russia is up 17.2% against EM year-to-date. The lesson here, therefore, is to find re-entry points into a well-founded view despite market volatility. Chart 1 shows that Russian equities climbed the proverbial “wall of worry” relative to EM in 2018. Doubting Jair Bolsonaro Our list of mistakes keeps us in the EM universe where we underestimated Jair Bolsonaro’s chances of winning the presidency in Brazil. The answer to the question we posed in the title of our September report – “Brazil: Can The Election Change Anything?” – was a definitive “yes.” Since the publication of that report, BRL/USD is up 2.9% and Brazilian equities are up 18.5% relative to EM (Chart 4). Chart 4Bolsonaro Rally Losing Its Luster Already

Bolsonaro Rally Losing Its Luster Already

Bolsonaro Rally Losing Its Luster Already

To our credit, the question of Bolsonaro’s electoral chances elicited passionate and pointed internal debate. But our clients did not see the internal struggle, just the incorrect external output! A bad call is a bad call, no matter how it is assembled on the intellectual assembly line. That said, we still think that our report is valuable. It sets out the constraints facing Bolsonaro in 2019. He has to convince the left-leaning median voter that meaningful pension reform is needed; bully a fractured Congress into painful structural reforms; and overcome an unforgiving macro context of tepid Chinese stimulus and a strong USD. If the Bolsonaro administration wastes the good will of the investment community over the next six months, we expect the market’s punishment to be swift and painful. In fact, Chart 4 notes that the initial Bolsonaro rally has already lost most of its shine. Brazilian assets are still up since the election, but the gentle slope could become a steep fall if Bolsonaro stumbles. The market is priced for political perfection. To be clear, we are not bearish on Bolsonaro. We believe that, relative to EM, he will be a positive for Brazil. However, the market is currently betting that he will win by two touchdowns, whereas we think he will squeak by with a last-second field goal. The difference between the two forecasts is compelling and we have expressed it by being long MXN/BRL.2 Not Sticking To Our Method In The Case Of Iran Throughout late-2017 and 2018 we pointed out that President Trump’s successful application of “maximum pressure” against North Korea could become a market-relevant risk if he were emboldened to try the same strategy against Iran. For much of the year, this view was prescient. As investors realized the seriousness of President Trump’s strategy, a geopolitical risk premium began to seep into oil prices, as illustrated in Chart 5 by the red bar.

Chart 5

Every time we spoke to clients or published reports on this topic, we highlighted just how dangerous a “maximum pressure” strategy would be in the case of Iran. We stressed that Iran could wreak havoc across Iraq and other parts of the Middle East and even drive up oil prices to the point of causing a “geopolitical recession in 2019.” In other words, we stressed the extraordinary constraints that President Trump would face. To their credit many of our clients called us out on the inconsistency: our market call was über bullish oil prices, while our methodology emphasized constraints over preferences. We were constantly fielding questions such as: Why would President Trump face down such overwhelming constraints? We did not have a very good answer to this question other than that he was ideologically committed to overturning the Iranian nuclear deal. In essence, we doubted President Trump’s own ideological flexibility and realism. That was a mistake and we tip our hat to the White House for recognizing the complex constraints arrayed against it. President Trump realized by October how dangerous those constraints were and began floating the idea of sanction waivers, causing the geopolitical risk premium to drain from the market (Chart 6). To our credit, we highlighted sanction waivers as a key risk to our view and thus took profit on our bullish energy call early. Chart 6Sanction Waivers Caused A Collapse In Oil Prices

Sanction Waivers Caused A Collapse In Oil Prices

Sanction Waivers Caused A Collapse In Oil Prices

That said, our clients have taken the argument further, pointing out that if we were wrong on Trump’s ideological flexibility with Iran, we may be making the same mistake when it comes to China. However, there is a critical difference. Americans are more concerned about conflict with North Korea than with Iran (Chart 7), while China is the major concern about trade (Chart 8).

Chart 7

Chart 8

Second, railing against the Iran deal did not get President Trump elected, whereas his protectionist rhetoric – specifically regarding China – did (Chart 9). Getting anything less than the mother-of-all-deals with Beijing will draw down Trump’s political capital ahead of 2020 and open him to accusations of being “weak” and “surrendering to China.” These are accusations that the country’s other set of protectionists – the Democrats – will wantonly employ against him in the next general election. Chart 9Protectionism, Not Iran, Helped Trump Get Elected

Protectionism, Not Iran, Helped Trump Get Elected

Protectionism, Not Iran, Helped Trump Get Elected

Ultimately, if we have to be wrong, we are at least satisfied that our method stood firm in the face of our own fallibility. We are doubly glad to see our clients using our own method against our views. This is precisely what we wanted to accomplish when we began BCA’s Geopolitical Strategy in March 2012: to revolutionize finance by raising the sophistication with which it approaches geopolitics. That was a lofty goal, but we do not pretend to hold the monopoly on our constraint-based methodology. In the end, our market calls did not suffer due to our error. We closed our long EM energy-producer equities / EM equities for a gain of 4.67% and our long Brent / short S&P 500 for a gain of 6.01%. However, our latter call, shorting the S&P 500 in September, was based on several reasons, including concerns regarding FAANG stocks, overstretched valuations, and an escalation of the trade war. Had we paired our S&P 500 short with a better long, we would have added far more value to our clients. It is that lost opportunity that has kept us up at night throughout this quarter. We essentially timed the S&P 500 correction, but paired it with a wayward long. The Best Calls Of 2018 BCA’s Geopolitical Strategy had a strong year. We are not going to list all of our calls here, but only those most relevant to our clients. Our best 2018 forecast originally appeared in 2017, when in April of that year we predicted that “Political Risks Are Understated In 2018.” Our reasoning was bang on: U.S. fiscal policy would turn strongly stimulative (the tax cuts would pass and Trump would be a big spender) and thus cause the Fed to turn hawkish and the USD to rally, tightening global monetary policy; Trump’s trade war would re-emerge in 2018; China would reboot its structural reform efforts by focusing on containing leverage, thus tightening global “fiscal” policy. In the same report we also predicted that Italian elections in 2018 would reignite Euro Area breakup risks, but that Italian policymakers would ultimately be found to be bluffing, as has been our long-running assertion. Throughout 2018, our team largely maintained and curated the forecasts expressed in that early 2017 report. We start the list of the best calls with the one call that was by far the most important for global assets in 2018: economic policy in China. The Chinese Would Over-Tighten, Then Under-Stimulate Getting Chinese policy right required us, first, to predict that policy would bring negative economic surprises this year, and second, once policy began to ease, to convince clients and colleagues that “this time would be different” and the stimulus would not be very stimulating. In other words, this time, China would not panic and reach for the credit lever of the post-2008 years (Chart 10), but would maintain its relatively tight economic, financial, environmental, and macro-prudential oversight, while easing only on the margin. Chart 10No Massive Credit Stimulus In 2018

No Massive Credit Stimulus In 2018

No Massive Credit Stimulus In 2018

This is precisely what occurred. BCA Foreign Exchange Strategy’s “China Play Index,” which is designed to capture any reflation out of Beijing, collapsed in 2018 and has hardly ticked up since the policy easing announced in July (Chart 11). Chart 11Weak Reflation Signal From China

Weak Reflation Signal From China

Weak Reflation Signal From China

Our view was based on an understanding of Chinese politics that we can confidently say has been unique: From March 2017, we highlighted the importance of the 2017 October Party Congress, arguing that President Xi Jinping would consolidate his power and redouble his attempts to “reform” the economy by reining in dangerous imbalances. We explicitly characterized the containment of leverage as the most market-relevant reform to focus on. We stringently ignored the ideological debate about the nature of reform in China, focusing instead on the major policy changes afoot. We identified very early on how the rising odds of a U.S.-China conflict would embolden Chinese leadership to double-down on painful structural reforms. Will China maintain this disciplined approach in 2019? That is yet to be seen. But we are arming ourselves and clients with critical ways to identify when and whether Beijing’s policy easing transforms into a full-blown “stimulus overshoot”: First, we need to see a clear upturn in shadow financing to believe that the Xi administration has given up on preventing excess debt. Assuming that such a shift occurs, and that overall credit improves, it will enable us to turn bullish on global growth and global risk assets on a cyclical, i.e., not merely tactical, horizon (Chart 12). Chart 12A Shadow Lending Surge Would Mean A Big Policy Shift

A Shadow Lending Surge Would Mean A Big Policy Shift

A Shadow Lending Surge Would Mean A Big Policy Shift

Second, our qualitative checklist will need to see a lot more “checks” in order to change our mind. Short of an extraordinary surge in bank and shadow bank credit, there needs to be a splurge in central and especially local government spending (Table 1). The mid-year spike in local governments’ new bond issuance in 2018 was fleeting and fell far short of the surge that initiated the large-scale stimulus of 2015. Frontloading these bonds in 2019 will depend on timing and magnitude. Table 1A Credit Splurge, Or Government Spending Splurge, Is Necessary For Stimulus To Overshoot

BCA Geopolitical Strategy 2018 Report Card

BCA Geopolitical Strategy 2018 Report Card

Third, we would need to see President Xi Jinping make a shift in rhetoric away from the “Three Battles” of financial risk, pollution, and poverty. Having identified systemic financial risk as the first of the three ills, Xi needs to make a dramatic reversal of this three-year action plan if he is to clear the way for another credit blowout. Trade War Would Reignite In 2018 It paid off to stick with our trade war alarmism in 2018. We correctly forecast that the U.S. and China would collide over trade and that their initial trade agreement – on May 20 – was insubstantial and would not last. In the event it lasted three days. Our one setback on the trade front was to doubt the two sides would agree to a trade truce at the G20. However, by assigning a subjective 40% probability, we correctly noted the fair odds of a truce. We also insisted that any truce would be temporary, which ended up being the case. We may yet be vindicated if the March 1 deadline produces no sustainable deal, as we forecast in last week’s Strategic Outlook. That said, correct geopolitical calls do not butter our bread at BCA. Rather, we are paid to make market calls. To that end, we would point out that we correctly assessed the market-relevance of the trade conflict, fading S&P 500 risks and focusing on the effect on global risk assets. Will this continue into 2019? We think so. We do not see trade conflict as the originator of ongoing market turbulence (Chart 13) and would expect the U.S. to outperform global equities again over the course of 2019 (Chart 14). This view may appear wrong in Q1, as the market digests the Fed backing off from hawkish rhetoric, the ongoing trade negotiations, and the likely seasonal uptick in Chinese credit data in the beginning of the calendar year. Chart 13Yields, Not Trade War, Drove Stocks

Yields, Not Trade War, Drove Stocks

Yields, Not Trade War, Drove Stocks

Chart 14U.S. Stocks Will Resume Outperformance

U.S. Stocks Will Resume Outperformance

U.S. Stocks Will Resume Outperformance

However, any stabilization in equity markets would likely serve to ease financial conditions in the U.S., where economic and inflation conditions remain firmly in tightening territory (Chart 15). As such, the Fed pause is likely to last no more than a quarter, maybe two at best, leading to renewed carnage in global risk assets if our view on Chinese policy stimulus – tepid – remains valid through the course of 2019. Chart 15If Financial Conditions Ease, Tightening Will Be Back On

If Financial Conditions Ease, Tightening Will Be Back On

If Financial Conditions Ease, Tightening Will Be Back On

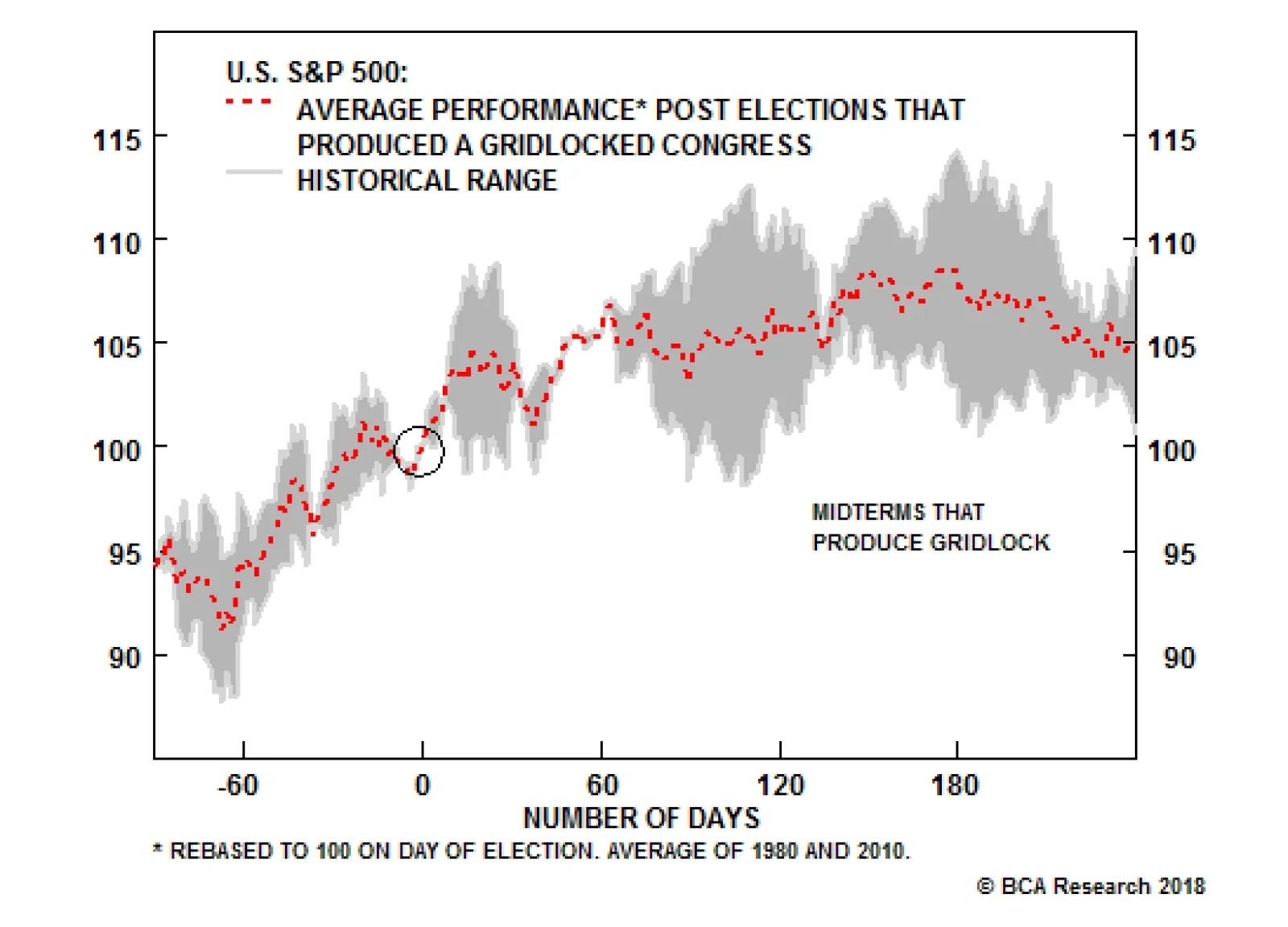

Europe (All Of It… Again) In 2017, our forecasting track record for Europe was stellar. This continued in 2018, with no major setbacks: Populism in Italy: Our long-held view has been that Europe’s chief remaining risks lay in Italian populists coming to power. We predicted in 2016 that this would eventually happen and that they would then be proven to be bluffing. This is essentially what happened in 2018. Matteo Salvini’s Lega is surging in the polls because its leader has realized that a combination of hard anti-immigrant policy and the softest-of-soft Euroskepticism is a winning combination. We believe that investors can live with this combination. Our only major fault in forecasting European politics and assets this year was to close our bearish Italy call too early: we booked our long Spanish / short Italian 10-year government bond trade for a small loss in August, before the spread between the two Mediterranean countries blew out to record levels. That missed opportunity could have also made it on our “worst calls” list as well.

Chart 16

Pluralism in Europe: To get the call on Italy right, we had to dabble in some theoretical work. In a somewhat academic report, we showed that political concentration was on the decline in the developed world (Chart 16), but especially in Europe (Chart 17). Put simply, lower political concentration suggests that a duopoly between the traditional center-left and center-right parties is breaking down. Contrary to the conventional wisdom, we argued that Europe’s parliamentary systems would enable centrist parties to adopt elements of the populist agenda, particularly on immigration, without compromising the overall stability of European institutions. As such, political pluralism, or low political concentration, is positive for markets.

Chart 17

Immigration crisis is over: For centrist parties to be able to successfully adopt populist immigration policy, they needed a pause in the immigration crisis. This was empirically verifiable in 2018 (Chart 18). Chart 18European Migration Crisis Is Over

European Migration Crisis Is Over

European Migration Crisis Is Over

Merkel’s time has run out: Since early 2017, we had cautioned clients that Angela Merkel’s demise was afoot, but that it would be an opportunity, rather than a risk, when it came. It finally happened in 2018 and it was not a market moving event. The main question for 2019 is whether German policymakers, and Europe as a whole, will use the infusion of fresh blood in Berlin to reaccelerate crucial reforms ahead of the next global recession. Brexit: Since early 2016, we have been right on Brexit. More specifically, we were corrent in cautioning investors that, were Brexit to occur, “the biggest loser would be the Conservative Party, not the EU.” As with the previous two Conservative Party prime ministers, it appears that the question of the U.K.’s relationship with the EU has completely drained any political capital out of Prime Minister Theresa May’s reign. We suspect that the only factor propping up the Tories in the polls is that Jeremy Corbyn is the leader of Her Majesty’s Most Loyal Opposition. We have also argued that soft Brexit would ultimately prove to be “illogical” and that “Bregret” would begin to seep in, as it now most clearly has. We parlayed these rising geopolitical risks and uncertainties by shorting cable in the first half of the year for a 6.21% gain. Malaysia Over Turkey And India Over Brazil Not all was lost for our EM calls this year. We played Malaysia against Turkey in the currency markets for a 17.44% gain, largely thanks to massively divergent governance and structural reform trajectories after Malaysia’s opposition won power for the first time in the country’s history. Second, we initiated a long Indian / short Brazilian equity view in March that returned 27.54% by August. This was a similar play on divergent structural reforms, but it was also a way to hedge our alarmist view on trade. Given India’s isolation from global trade and insular financial markets, we identified India as one of the EM markets that would remain aloof of protectionist risks. We could have closed the trade earlier for greater gain, but did not time the exit properly. Midterm Election: A Major Democratic Victory Our midterm election forecast was correct: Democrats won a substantial victory. Even our initial call on the Senate, that Democrats had a surprisingly large probability of picking up seats, proved to be correct, with Republicans eking out just two gains in a year when Democrats were defending 10 seats in states that Trump carried in 2016. What about our all-important call that the election would have no impact on the markets? That is more difficult to assess, given that the S&P 500 has in fact collapsed in the lead-up to and aftermath of the election. However, we see little connection between the election outcome and the stock market’s performance. Neither do our colleagues or clients, who have largely stopped asking about the Democrats’ policy designs. In 2019, domestic politics may play a role in the markets. Impeachment risk is low, but, if it rears its head, it could prompt President Trump to seek relevance abroad, as his predecessors have done when they lost control of domestic policy. In addition, the Democratic Party’s sweeping House victory may suggest a political pendulum swing to the left in the 2020 presidential election. We will discuss both risks as part of our annual Five Black Swans report in early 2019. U.S. domestic politics was a collection of Red Herrings during much of President Obama’s presidency, and has produced strong tailwinds under President Trump (tax cuts in particular). This may change in 2019, with considerable risk to investors, and asset prices, ahead. Marko Papic, Senior Vice President Chief Geopolitical Strategist marko@bcaresearch.com Matt Gertken, Vice President Geopolitical Strategy mattg@bcaresearch.com Roukaya Ibrahim, Editor/Strategist roukayai@bcaresearch.com Ekaterina Shtrevensky, Research Analyst ekaterinas@bcaresearch.com Footnotes 1 For our 2019 Outlook, please see BCA Geopolitical Strategy Strategic Outlook, “2019 Key Views: Balanced On A Knife’s Edge,” dated December 14, 2018, available at gps.bcaresearch.com. For our past Strategic Outlooks, please visit gps.bcaresearch.com. 2 In part we like this cross because we also think that Mexico’s newly elected president, Andrés Manuel López Obrador, is priced to lose by two touchdowns, whereas he may merely lose by a last-second field goal.

Highlights The Reserve Bank of Australia (RBA) may consider a rate hike in 2019 if additional tightening of labor markets leads to higher wage inflation, which would help lift core inflation back to the midpoint of the RBA’s 2-3% target band. Reflation in China could also embolden the RBA to tighten monetary policy – though the odds of a more aggressive stimulus package will decline as long as China’s overall economy remains stable and the U.S. maintains its tariff ceasefire. The Labor Party is favored to win the federal election, which is most likely to occur in May. This is a low-conviction view, as polls are tight and economic improvement will help the ruling Liberal-National Coalition. Feature 2018 has been a challenging year for global financial markets, as investors have had to deal with greater economic uncertainty, less dovish central banks and more volatile asset prices. One country that has bucked the trend to some degree is Australia. The nation has famously avoided a recession since 1991 and last saw a tightening of monetary policy in 2010. While the recession streak is unlikely to be broken in 2019, there are growing risks that the era of interest rate tranquility will soon end. In this Special Report, jointly published with our colleagues at BCA Geopolitical Strategy, we update our views on Australia for 2019 – a year when the investment backdrop has the potential to become far more interesting, and volatile, due to election year uncertainty and a potential shift to a more hawkish bias for monetary policy. The Bond Outlook: What To Watch To Turn Bearish BCA Global Fixed Income Strategy has maintained an overweight stance on Australian government bonds since the end of 2017. That high-conviction view stemmed from our expectation that the Reserve Bank of Australia (RBA) would keep policy rates on hold for longer due to sluggish economic growth and underwhelming inflation. This recommendation has performed well, with Australian government bonds returning 2.4% (currency-hedged into U.S. dollars) in 2018 year-to-date, beating the Bloomberg Barclays Global Treasury index by 190bps. The benchmark 10-year Australian government is now yielding 36bps below the equivalent 10-year U.S. Treasury yield, the tightest spread since 1980 (Chart 1). Chart 1Australian Bonds Have Outperformed

Australian Bonds Have Outperformed

Australian Bonds Have Outperformed

Looking ahead, we still have a positive opinion on Australian debt relative to its global peers over the next six months. The RBA is unlikely to make any adjustments to the Cash Rate - which remains at a highly-accommodative level of 1.5% - without seeing some signs of accelerating inflation in both the Q4 2018 and Q1 2019 CPI reports. This is especially true given the political uncertainty with another federal election due by May 18,1 which could change the outlook for fiscal policy (as we discuss later in this report) and impact the RBA’s economic projections. In our view, the RBA will only be able to seriously consider an interest rate hike, warranting a downgrade of our recommended overweight stance, if all three of the following conditions occur: Australia’s underemployment rate falls below 8% China’s economy shows convincing evidence of reacceleration, especially in commodity-intensive industries like construction Core CPI inflation rises back to at least the midpoint of the RBA’s 2-3% target band We will now discuss each of these in turn. Underemployment Australia is a fairly open economy with a large export sector, but consumer spending is still the largest share of GDP (60%) so it matters most for growth. On that front, real consumption has grown in a narrow and uninspiring range between 2-3% over the past five years. Anemic wages and disposable incomes have been the problem, with the growth of both (in nominal terms) struggling to grow faster than low realized inflation, which now sits below the RBA’s inflation target range of 2-3% (Chart 2). Households have been forced to deploy a greater share of that modest income growth just to maintain spending, with the savings rate plunging from 8% at the end of 2014 to 1% this year and consumer debt piling up. Chart 2An Income-Fueled Pickup In Consumer Spending

An Income-Fueled Pickup In Consumer Spending

An Income-Fueled Pickup In Consumer Spending

The dynamics may be changing in a more positive direction, however. Growth rates of nominal wage (+2.3%) and disposable income (+3.1%) have accelerated this year to a pace faster than inflation. With real incomes perking up, the year-over-year growth rate of real consumer spending growth accelerated to 3% in Q3/2018, driving real GDP growth to similar levels. A sustained pickup in wage growth is necessary before the RBA would even contemplate a rate hike. For that to occur, there must be decisive evidence of a tightening Australian labor market and increased resource utilization. While the headline unemployment rate of 5.0% is below the OECD’s estimate of the full employment NAIRU for Australia (5.3%), broader measures of labor market slack are still at elevated levels. Specifically, the “underemployment” rate, which includes workers who are working fewer hours than they would like or at jobs below their skill levels, is still at an elevated 8.3% (Chart 3). That is down from the peak of just below 9% seen in early 2017, but well above the 2012 trough near 7% (when wage growth was close to 4%). Chart 3UNDERemployment Rate Matters More For Australian Wages

UNDERemployment Rate Matters More For Australian Wages

UNDERemployment Rate Matters More For Australian Wages

Australian wage growth tends to correlate more with the underemployment rate than the traditional unemployment rate (middle panel). This suggests that the recent blip higher in wage growth could be the beginning of a new trend, given that it has occurred alongside the recent drop in underemployment. Already, underemployment is back below the levels that prevailed when the RBA did its last interest rate cut back in 2016 (bottom panel). A further dip lower in the underemployment rate to below the 8% threshold would likely confirm that wage growth has more upside. That outcome would give the RBA greater confidence that consumer spending will gain more strength even with a low savings rate, and that CPI inflation will return back into the target range – both outcomes that would justify some removal of the RBA’s highly stimulative monetary accommodation. China Stimulus The main connection from China’s economy to Australia is through Chinese demand for Australian exports. There is also an indirect, but very important, link between Chinese demand boosting industrial commodity prices. The latter boosts Australian growth through positive terms-of-trade effects and increased capital spending in commodity-related sectors like mining. Iron ore is the most important of those commodities, representing 18% of total Australian goods exports, with 85% of those iron ore exports going to China. Australian export growth has decelerated during 2018 from the very robust 15% year-over-year pace to a still solid 10% rate. This has mirrored the trends seen in many other economies, where exports have slowed alongside diminished demand from China. If Chinese authorities change their current policy trajectory, and embrace more aggressive fiscal and credit stimulus, then they will reaccelerate the country’s flagging demand, which should benefit Australian exporters. If the increase in spending occurs in commodity-intensive parts of China’s economy, like construction, then Australia can also benefit from a terms-of-trade impact if commodity prices rise. However, BCA’s Geopolitical Strategy and China Investment Strategy remain skeptical that China will launch a major economic stimulus package along the lines of what occurred in 2015-16. That surge not only boosted Chinese GDP and import demand but also triggered a boost to global industrial commodity prices that benefitted many commodity exporters, including Australia. In recent months, there has been a pickup in overall Chinese import growth, as well as some acceleration of higher frequency growth indicators like the Li Keqiang index (Chart 4). Australian exports to China have not picked up though, and Chinese iron ore imports are contracting. Part of that is due to the elevated levels of Chinese iron ore inventories. More likely, there is little demand for additional iron ore given China’s reform agenda and the struggles of its construction sector (which accounts for roughly 35% of Chinese steel demand). Chart 4China Stimulus Not Helping Australia...Yet?

China Stimulus Not Helping Australia...Yet?

China Stimulus Not Helping Australia...Yet?

Our colleagues at BCA China Investment Strategy2 have noted that both weakening sales and tighter funding sources for real estate developers point to declining growth in property starts and construction. This will be negative for construction-related commodity markets and construction-related machinery. This is coming at a time when the Chinese government is trying specifically to address over-indebted industries like construction. As for the U.S.-China trade truce, a permanent de-escalation of tensions – which has not yet occurred – could provide a boost to Australian export demand, as with other export-focused countries. But the negative impact of bilateral U.S.-China tariffs on the global economy is much smaller than that of China’s attempt to limit indebtedness. Moreover, a trade truce will remove China’s primary incentive to adopt more aggressive stimulus. Nevertheless, from the RBA’s perspective, any boost to China’s construction-related activity would have a big impact on Australia’s economy and would strengthen the case for a rate hike in 2019. Core Inflation Australia’s headline CPI inflation has struggled to hit even the bottom end of the RBA’s 2-3% target band since 2015, reaching only 1.9% in Q3 of this year (Chart 5). The story is even worse for inflation excluding food and energy, with core CPI inflation now only at 1.2% after having drifted lower in two consecutive quarters. Both market-based and survey-based measures of inflation expectations are also hovering near 2%. Chart 5Australian Inflation Well Below RBA Target

Australian Inflation Well Below RBA Target

Australian Inflation Well Below RBA Target

When breaking down the CPI into tradeables (i.e. more globally-focused) and non-tradeables (i.e. more domestically-focused), the two types of inflation have not been accelerating at the same time since the 2009-11 period. Since then, faster tradeables inflation has occurred alongside slowing non-tradeables inflation, and vice versa. While volatility on the tradeables side should be expected given the correlation to swings in commodity prices and the Australian dollar, the weakness in non-tradeables is more directly related to the spare capacity in the domestic economy. Therefore, if wage growth continues to pick up as the labor market tightens, then non-tradeables inflation should follow suit and boost Australian CPI inflation back towards the RBA target range. The implication for the RBA is that a move in core CPI inflation back towards 2.5% (the midpoint of the RBA band), occurring after an acceleration in wage growth as described above, would give the central bank confidence that a higher Cash Rate is required. Bottom Line: The RBA has kept interest rates on hold for over two years, but may consider a rate hike in 2019 if additional tightening of labor markets leads to higher wage inflation, which would help lift core inflation back to the midpoint of the RBA’s 2-3% target band. A more aggressive fiscal and monetary stimulus package in China, while not our base case, would also embolden the RBA to tighten monetary policy. Risks From Australian Banks? Throughout 2018, the Australian financial industry has had to endure the slings and arrows of a government inquiry into its questionable business practices and misconduct. Revelations of bribery, fraud, the charging of fees for no service and from the accounts of deceased people, as well as board-level deception of regulators, have roiled Australia's financial sector since the explosive inquiry began in February. The final report of the Australian Financial Services Royal Commission will be published in February, but the impact is already being felt throughout the industry. Bank CEOs have been publically shamed, while other senior financial sector executives have been forced from their jobs. The chairman of National Australia Bank stated before the inquiry that customers’ trust in lenders had been “pretty well eroded to zero”, and that it could take as long as a decade to successfully overhaul the culture within the banks. The biggest impacts from the Commission will come through hits to banks’ earnings and funding costs, as well as the potential impact on lending standards for new loans. Australian banks will be less profitable because of fines, customer refunds, setting aside provisions for potential misconduct penalties and the government wanting increased competition. If banks also choose to be more conservative with the marking of loans, then higher loan-loss provisions could be an additional drag on bank earnings. Already, Australian bank stocks have severely underperformed the overall domestic market, and there has been some slowing of domestic credit growth (Chart 6). There are also signs of bank funding stresses from contracting bank deposit growth (second panel) and wider offshore funding costs like relatively elevated LIBOR-OIS spreads (bottom panel). Considering how heavily Australian banks rely on offshore funding, any squeeze in those markets could severely influence the availability of credit within the Australian economy. Chart 6Australian Banks Under Some Stress...

Australian Banks Under Some Stress...

Australian Banks Under Some Stress...

Looking ahead, if banks do tighten up their lending standards in response to the criticism and findings of the Commission, that will be from a starting point of very accommodative levels. In other words, getting a loan will likely still be “easy”, rather than “incredibly easy”. The reason is that Australian bank balance sheets remain in excellent condition. Credit crunches begin when banks are undercapitalized and are forced to retrench new loan activity as losses on existing loans pile up. That is not the case in Australia, where the major banks have Tier 1 capital ratios in the 10-12% range and non-performing loans are a tiny share of total lending. In our view, a true credit crunch would likely only occur after the Australian housing bubble bursts and the economy enters a severe downturn. That outcome would most likely be triggered by monetary policy tightening via multiple RBA rate hikes. Importantly, some of the steam has already been taken out of Australian house prices thanks to changes in regulations on new lending (Chart 7), potentially reducing some of the immediate risks to growth from a sharp plunge in home values. Chart 7...But No Credit Crunch Expected

...But No Credit Crunch Expected

...But No Credit Crunch Expected

Bottom Line: In 2019, the Australian government and its key financial regulators will have to work together to enforce responsible lending without triggering a catastrophic property market unwind. RBA policymakers are less likely to hike rates given their desire to maintain financial stability in the aftermath of the Commission – or at least until the inflation story forces their hand, as outlined in this report. The Federal Election: Polling Slightly Favors Labor Scandals in the financial sector are of utmost importance to the other major factor that could make 2019 a year of significant change in Australia: the federal election that looms most likely in the spring. Parliament is balanced on a knife’s edge, with the Australian Liberal Party’s loss of former Prime Minister Malcolm Turnbull’s parliamentary seat in a Sydney by-election on October 20. The ruling Liberal-National Coalition no longer has a majority and must rely on independent MPs to survive any no-confidence vote. This precarious situation suggests that the election could come even sooner than May and that the slightest twist in the campaign could deliver at least a small majority to either of the top two parties. Indeed, at this early stage, a high-conviction view on the election outcome is not warranted. After all, the 2016 election was decided in the Coalition’s favor only after a shift in opinion in the final month! Chart 8Labor Party Narrowly Leads All-Party Opinion Polls

A Year Of Change In Australia?

A Year Of Change In Australia?

Nevertheless, with all due caveats, our baseline case is for a Labor majority in 2019, however slim it may be.3 Labor is slightly ahead of the Coalition in the primary opinion polling, which includes all parties (Chart 8). In two-party preference polling, Labor has gradually widened its general lead since the July 2016 election and now holds a 10% advantage in the federal polls – albeit only a 6% lead when a moving average is taken (Chart 9). Labor is also winning or tied in every major state. Chart 9Labor Has Large Lead In Two-Party Preference Polls

A Year Of Change In Australia?

A Year Of Change In Australia?

The dramatic shift in polling since August is significant because that is when the knives came out and the Coalition ousted Turnbull in favor of the current Prime Minister Scott Morrison. The purpose of this move was to give the party a facelift ahead of the election. It is true that public opinion views Morrison as the preferred prime minister to Labor’s Bill Shorten. Shorten has a negative net approval rating and has never been viewed as an inspiring politician, while Morrison is just barely net positive. This perception works against Labor’s lead in the party polling – which is very competitive anyway – and suggests the election will be close. Critically, the Liberal-National Coalition’s polling as a whole has not benefited from the change in leadership. And in fact the data does not support the two major Australian parties’ abiding belief that a leadership coup will boost their popularity: Australia has seen four of these coups since 2010, two from Labor and two from the Coalition, and the party in question lost an average of 8% of the popular vote and 14 seats in parliament in the succeeding election (Table 1). Table 1Intra-Party Coups Don’t Win Votes

A Year Of Change In Australia?

A Year Of Change In Australia?

Turnbull’s ouster also calls attention to another detrimental factor for the Coalition: the challenge on the right flank from minor and anti-establishment parties. Pauline Hanson’s One Nation has a relatively low support rate both historically and in today’s race, currently at 8%, but anti-establishment feeling may have forced the Coalition into an error. Judging by the party’s weak polling since August, the negative response to Turnbull’s ouster has been more detrimental than the nomination of Morrison, an immigration hardliner and social conservative, has been beneficial. Meanwhile, Labor’s momentum has been corroborated by a string of surprise victories in by-elections and a sweeping win in the Victoria state elections on November 24. In the latter case, the party not only defended its hold on government, as one might expect in this progressive state, but exceeded expectations to win 56 seats out of 88 in the lower House, while the Coalition lost nearly half of its seats, falling from 37 to 21. Still, Labor’s lead is by no means decisive. In the average of the various primary polls its edge over the Coalition is within the margin of error. Moreover, the Coalition holds more “safe” (uncompetitive) seats than Labor.4 The bottom line is that a small swing in either party’s favor can produce a thin majority. The Coalition’s best case is the economy. But as concerns about unemployment and job creation recede, voters will make other demands. The top issues in recent polling are the cost of living, health care, housing affordability, and wages. Some polls also emphasize social mobility and climate change and renewable energy. Will Shorten’s Labor Party be able to capture the median voter? It is highly significant that the party has taken a rightward turn on immigration and taxes even as it holds out a more left-wing agenda on health, education, regulation, and social benefits. Immigration has played a major role in Australian politics and Labor is currently positioned near the political center – in other words, if Morrison hardens his line to guard against populists, he risks over-hardening and moving away from the median voter (Chart 10). Shorten has proposed a large bipartisan task force to determine the proper limits to immigration and how to deal with congestion and infrastructure pressures. Shorten’s platform also calls attention to abuse of temporary visas by foreign workers. Chart 10Labor Is Not Too Soft On Immigration

A Year Of Change In Australia?

A Year Of Change In Australia?

On taxes, Shorten has attempted to separate small and big companies, again in a bid for the political center. When Prime Minister Morrison sought to establish his anti-tax credentials (Chart 11), Shorten met him halfway and proposed relief for middle class families and small and medium-sized enterprises. Yet he doubled down on higher taxes for multinational corporations and high-income earners. Chart 11Liberal-National Coalition Cutting Corporate Tax Rates

A Year Of Change In Australia?

A Year Of Change In Australia?

Critically, the latter redistributive stances are more in line with the median voter than the Liberal Party’s more conservative, supply-side, tax cut agenda. All of Australia’s parties, including the increasingly popular “minority parties,” have a more favorable attitude toward redistribution than the Coalition, which is the outlier (Chart 12). Indeed, the National Party is closer in line with the others than the Liberals, highlighting the divisions within the Coalition that have been jeopardizing votes. As for tax cuts on middle income earners and small businesses, Labor’s acceptance of them speaks to voter concerns about living costs, jobs, and wages. Chart 12The Coalition Is Out Of Synch On Taxes

A Year Of Change In Australia?

A Year Of Change In Australia?

Labor is also closer to the median voter on the aforementioned financial sector scandals. The Coalition stands to suffer because it has developed a reputation for being too cozy with the banks (Chart 13). This is one of the biggest perceived differences between the two major parties – in addition to the negative perception of intra-Coalition betrayal – and it is possibly one of the most salient issues in the election. This presents a serious danger for the Coalition. Chart 13Banks: The Coalition’s Ball And Chain

A Year Of Change In Australia?

A Year Of Change In Australia?

What would a Labor government bring? The market will be jittery about Shorten’s attempts to increase tax revenue, which threatens a non-negligible tightening of fiscal policy. Shorten wants to raise taxes on high income earners; remove or lower deductions and discounts (such as on capital gains); crack down on tax evasion; and tighten control over a range of tax practices specific to Australia (limiting “negative gearing” and cutting cash refunds for “franking credits”). He is also taking a tough position on banks and the energy sector. At the same time, it is clear from Labor’s proposals in 2016 (Chart 14) that there will be a hefty amount of new spending coming down the pike if a Labor government is formed – primarily on education, health, infrastructure and job training. The tax cuts that Shorten does support will go to those with a higher propensity to consume, as well as to SMEs that are responsible for job creation. Chart 14Labor’s Spending Plans Unlikely To Change Much

A Year Of Change In Australia?

A Year Of Change In Australia?

Ultimately, Australia’s recent history, taken in consideration with the global business cycle, does not suggest that the Labor Party is all that much more fiscally profligate than the Coalition – but the current budget balance does suggest that there is substantial room to increase deficits, which is convenient for a government that is predisposed to give voters more services (Chart 15). Hence fiscal easing is the path of least resistance - one that could make the RBA even more comfortable in raising interest rates if the conditions laid out earlier in this report come to pass. Chart 15Australia's Next Government Will Have Room To Spend!

Australia's Next Government Will Have Room To Spend!

Australia's Next Government Will Have Room To Spend!