Elections

Highlights So What? Geopolitical risks are not about to ease. Why? Fiscal policy becomes less accommodative next year unless politicians act. Financial conditions give President Trump room to expand his tariff onslaught. Our Iran view is confirmed by rapid escalation of tensions – war risk is high. The odds of a no-deal Brexit have risen. Feature The AUD-JPY cross and copper-to-gold ratio – two market indicators that flag global growth and risk-on sentiment – are hovering over critical points at which a further breakdown would catalyze a renewed flight to quality (Chart 1). Chart 1Risk-On Indicators Breaking Down?

Risk-On Indicators Breaking Down?

Risk-On Indicators Breaking Down?

Global sentiment remains depressed amid a rash of negative economic surprises and bonds continue to rally despite a more dovish outlook from the Fed (Chart 2). Chart 2Global Sentiment Remains Depressed

Global Sentiment Remains Depressed

Global Sentiment Remains Depressed

The cavalry is on the way: European Central Bank President Mario Draghi oversaw a dramatic easing of monetary policy on June 18, driving the Italian-German sovereign bond spread down to levels not seen since before the populist election outcome of March 2018 (Chart 2, bottom panel). The Federal Reserve adjusted its policy rate projections to countenance an interest rate cut in the not-too-distant future. More needs to be done, however, to sustain the optimism that has propelled the S&P 500 and global equities upward since the volatility catalyzed by President Donald Trump’s announcement of a tariff rate hike on May 6. Political and geopolitical risks are higher, not lower, since that time as market-negative scenarios are playing out with U.S. policy, Iran, and Brexit, while we take a dim view of the end-game of the U.S.-China negotiations despite recent improvements. Fiscal And Trade Uncertainties This year’s growth wobbles have occurred in the context of expansive fiscal policy in the developed markets. Next year, however, the fiscal thrust (the change in the cyclically adjusted budget balance) is projected to decline in the U.S. and Japan and nearly to do so in Europe (Chart 3). We expect President Trump and the House Democrats to raise spending caps (or at least keep spending at current levels) and thus prevent the budget deficit from contracting in FY2020 – this is their only substantial point of agreement. But this at best neutralizes what would otherwise be a negative fiscal backdrop. Meanwhile it is not at all clear that Brussels will relax its scrutiny of member states seeking to cut taxes and boost spending, such as Italy. Japanese Prime Minister Abe Shinzo would need to arrange for the Diet to pass a new law to avoid the consumption tax hike from 8% to 10% on October 1. He can pull this off, especially if the U.S. trade war escalates – or if he decides to turn next month’s upper house election into a general election and needs to boost his popularity. But as things currently stand in law, the world’s third biggest economy will face a deep fiscal pullback next year (Chart 3, bottom panel). In short, DM fiscal policy will not really become contractionary in 2020, but this is a view and not yet a reality (Chart 4). Chart 3Fiscal Pullback Likely Next Year

Fiscal Pullback Likely Next Year

Fiscal Pullback Likely Next Year

Chart 4Only The U.S. Is Profligate

Only The U.S. Is Profligate

Only The U.S. Is Profligate

Meanwhile China’s stimulus is still in question – in fact it remains the major macro question this year. The efficacy of China’s stimulus is declining ... An escalating trade war will bring greater stimulus but also greater transmission problems. Since February we have argued that the Xi administration has shifted to sweeping fiscal-and-credit stimulus in the face of the unprecedented external threat posed by the Trump administration (Charts 5A and 5B). We expect China’s credit growth to continue its upturn in June and in H2. Ultimately, we think the whole package will be comparable to 2015-16 – and anything even close to that will prolong the global economic expansion. We do not see a massive 2008-style stimulus occurring unless relations with the U.S. completely collapse and a global recession occurs. Chart 5AStimulus Amid The Trade War

Stimulus Amid The Trade War

Stimulus Amid The Trade War

Chart 5

The catch – as we have shown – is that the efficacy of China’s stimulus is declining over time because of over-indebtedness and bearish sentiment in China’s private sector. These tepid animal spirits stem from epochal changes: Xi’s reassertion of communism and America’s withdrawal of strategic support for China’s rise. An escalating trade war will bring greater stimulus but also greater transmission problems. The magnitude of the tariffs that President Trump is threatening to impose on China, Mexico, the EU, and Japan is mind-boggling. We illustrate this with a simple simulation of duties collected as a share of total imports under different scenarios (Chart 6).

Chart 6

China and Mexico are fundamentally different from the EU and Japan and hence the threat of tariffs will continue to weigh on markets for Trump’s time in office – China because of a national security consensus and Mexico because of the Trump administration’s existential emphasis on curbing illegal immigration. But we still put the risk of auto tariffs (or other punitive measures) on Europe at 45% if Trump seals a China deal. The odds are lower for Japan but it is still at risk. Global supply chains are shifting – a new source of costs and uncertainty for companies – as a slew of recent news has highlighted. Already 40% of companies surveyed by the American Chamber of Commerce in China say they are relocating to Southeast Asia, Mexico, and elsewhere (Chart 7). If the G20 is a flop – or results in nothing more than a pause in tariffs for another three-month dialogue – relocations will gain steam, forcing companies’ bottom lines to take a hit.

Chart 7

Even in the best case, in which the Trump-Xi summit produces a joint statement outlining a “deal in principle” accompanied by a rollback of the May 10 tariff hike, uncertainty will persist due to President Trump’s unpredictability, China’s incentive to wait until after the U.S. election, and Trump’s incentive to corner the “China hawk” platform prior to the election. We maintain that, by November 2020, there is a roughly 70% chance of further escalation. At least the U.S.-China conflict is nominally improving. The same cannot be said for other geopolitical risks discussed below: the U.S. and Iran are flirting with war; the U.S. presidential election is injecting a steady trickle of market-negative news; the chances of a no-deal Brexit are rising; and Trump may turn on Europe at a moment when it lacks leadership. This list assumes that Russia takes advantage of American distraction by improving domestic policy rather than launching into a new foreign adventure – say in Ukraine or Kaliningrad. If there is any doubt as to whether political risk can outweigh more accommodative monetary policy, remember that President Trump actually can remove Chairman Jerome Powell. Legally he is only allowed to do so “for cause” as opposed to “at will.” But the meaning of this term is a debate that would go to the Supreme Court in the event of a controversial decision. Meanwhile the stock market would dive. Now, this is precisely why Trump will not try. But the implication, as with Congress and the border wall, is that Trump is constrained on domestic policy and hence tariffs are his most effective tool to try to achieve policy victories. With an ebullient stock market and a Fed that is adjusting its position, Trump can try to kill two birds with one stone: wring concessions from trade partners while forcing the FOMC to keep responding to rising external risks. Bottom Line: Central banks are riding to the rescue, but there is only so much they can do if global leaders are tightening budgets and imposing barriers on immigration and trade. We remain tactically cautious. Oh Man, Oh Man, Oman Iran has swiftly responded to the Trump administration’s imposition of “maximum pressure” on oil exports. The shooting down of an American drone that Tehran claims violated its airspace on June 20 is the latest in a spate of incidents, including a Houthi first-ever cruise missile attack on Abha airport in Saudi Arabia. Two separate attacks on tankers near the Strait of Hormuz (Map 1) demonstrate that Iran is threatening to play its most devastating card in the renewed conflict with the U.S.

Chart

Chart 8

Hormuz ushers through a substantial share of global oil demand and liquefied natural gas demand (Chart 8). The amount of spare pipeline capacity that the Gulf Arab states could activate in the event of a disruption is merely 3.9 million barrels per day, or 6 million if questionable pipelines like the outdated Iraqi pipeline in Saudi Arabia prove functional (Table 1). Table 1No Sufficient Alternatives To Hormuz

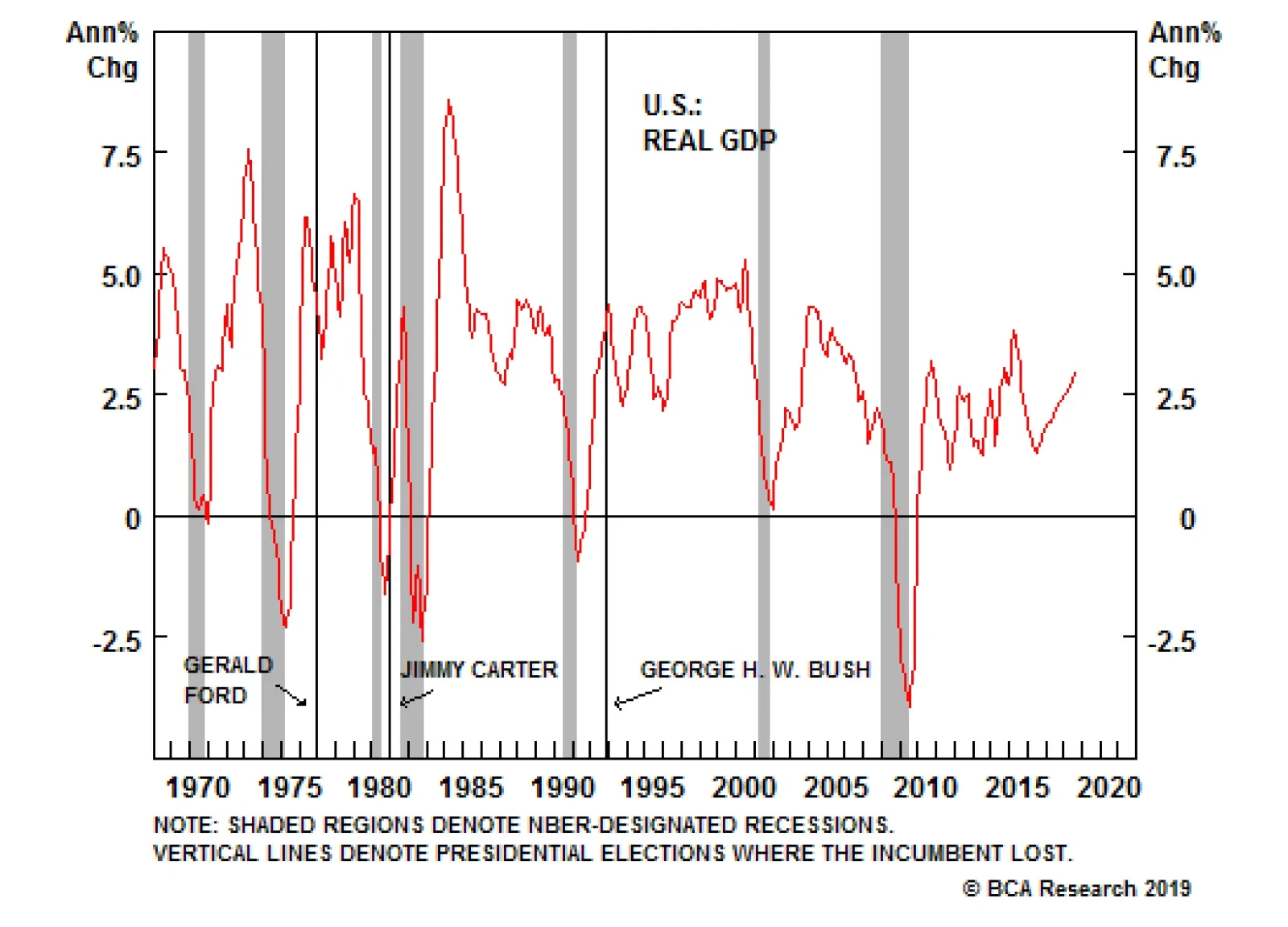

Escalation ... Everywhere

Escalation ... Everywhere

A conflict with Iran could cause the biggest oil shock of all time. Even if this spare capacity were immediately utilized, a conflict could cause the biggest oil shock of all time – considerably bigger than that of the Iranian Revolution (Chart 9).

Chart 9

We have shown in the past that Iran has the military capability of interrupting the flow of traffic in Hormuz for anywhere from 10 days to four months. A preemptive strike by Iran would be most effective, whereas a preemptive American attack would include targets to reduce Iran’s ability to retaliate via Hormuz. The impact on oil prices ranges from significant to devastating. Needless to say, blocking the Strait of Hormuz would initiate a war so Iran is attempting to achieve diplomatic goals with the threats themselves – it will only block the strait as a last resort, say if it is convinced that the U.S. is about to attack anyway. As the experience of President Jimmy Carter shows, Americans may rally around the flag during a crisis but they will also kick a president out of office for higher prices and an economic slowdown. President Trump cannot be unaware of this precedent. The intention of his Iran policy is to negotiate a “better deal” than the 2015 one – a deal that includes Iran’s regional power projection and ballistic missile capabilities as well as its nuclear program. The problem is that Trump has already been forced to deploy a range of forces to the region, including additional troops (albeit so far symbolic at 2,500) (Chart 10). He is also sending Special Representative for Iran, Brian Hook, to the region to rally support among Gulf Cooperation Council. The week after Hook will court Britain, Germany, and France, three of the signatories of the 2015 deal. Trump ran on a campaign of eschewing gratuitous wars in the Middle East – a popular stance among war-weary Americans (Chart 11) – but there is a substantial risk that he could get entangled in the region. First, he is adopting a more aggressive foreign policy to attempt to compensate for the lack of payoff in public opinion from the strong economy. Second, Iran is not shrinking from the fight, which could draw him deeper into conflict. Third, there is always a high risk of miscalculation when nations engage in such brinkmanship. Chart 10Is The 'Pivot To Asia' About To Reverse?

Is The 'Pivot To Asia' About To Reverse?

Is The 'Pivot To Asia' About To Reverse?

Chart 11

The Iranian response has been, first, to reject negotiations. When Trump sent a letter to Rouhani via Japanese Prime Minister Abe Shinzo, Abe was rebuffed – and one of the tankers attacked near Oman was a Japanese flagged vessel, the Kokuka Courageous. This is a posture, not a permanent position, as the Iranian release of an American prisoner demonstrates. But the posture can and will be maintained in the near term – with escalation as the result. Second, Iran is increasing its own leverage in any future negotiation by demonstrating that it can sow instability across the region and bring the global economy grinding to a halt. Iran cannot assume that Trump means what he says about avoiding war but must focus on the United States’ actions and capabilities. Cutting off all oil exports is a recipe for extreme stress within the Iranian regime – it is an existential threat. Therefore, the Iranians have signaled that the cost of a total cutoff will be a war that will cause a global oil price shock. The Iranian leaders are also announcing that they are edging closer to walking away from the 2015 nuclear pact (Table 2). If so, they could quickly approach “breakout” capacity in the uranium enrichment – meaning that they could enrich to 20% and then in short order enrich to 90% and amass enough of this fuel to make a nuclear device one year thereafter. The Trump administration has reportedly reiterated that this one-year limit is the U.S. government’s “red line,” just as the Obama administration had done. Table 2Iran Threatens To Walk Away From 2015 Nuclear Deal

Escalation ... Everywhere

Escalation ... Everywhere

This Iranian threat is a direct reaction to Trump’s decision in May not to renew the oil sanction waivers. Previously the Iranians had sought to preserve the 2015 deal, along with the Europeans, in order to wait out Trump’s first term. These developments push us to the brink of war. Iran is retaliating with both military force and a nuclear restart. This comes very close to meeting our conditions for an American (and Israeli) retaliation that is military in nature. Diagram 1 is an update of our decision tree that we have published since last year when Trump reneged on the 2015 deal. The window to de-escalate is closing rapidly. The Appendix provides a checklist for air strikes and/or the closure of Hormuz. Diagram 1Iran-U.S. Tensions Decision Tree

Escalation ... Everywhere

Escalation ... Everywhere

At very least we expect to see the U.S. attempt to create a large international fleet to assert freedom of navigation in the Persian Gulf and Strait of Hormuz. While Iran may lay low during a large show of force, it will later want to demonstrate that it has not been cowed. And it has the capacity to retaliate elsewhere, including in Iraq, an area we have highlighted as a major geopolitical risk to oil supply. The U.S. government has already reacted to recent threats there from Iranian proxies by pulling non-essential personnel. Iran has several incentives to test the limits of conflict if the U.S. insists on the oil embargo. First, tactically, it seeks to deter President Trump, take advantage of American war-weariness, drive a wedge between the U.S. and Europe, and force a relaxation of the sanctions. This would also demonstrate to the region that Iran has greater resolve than the United States of America. This goal has not been achieved by the recent spate of actions, so there is likely more conflict to come. Second, President Hassan Rouhani’s government is also likely to maintain a belligerent posture – at least in the near term – to compensate for its loss of face upon the American betrayal of the 2015 nuclear deal. Rouhani negotiated the deal against the warnings of hardline revolutionaries. The 2020 majlis elections make this an important political goal for his more reform-oriented faction. Negotiations with Trump can only occur if Rouhani has resoundingly demonstrated his superiority in the clash of wills. Structurally, Iran faces tremendous regime pressures in the coming years and decades because of its large youth population, struggling economy, and impending power transition from the 80 year-old Supreme Leader Ali Khamanei. A patriotic war against America and its allies – while not desirable – is a risk that Khamenei can take, as an air war is less likely to trigger regime change than it is to galvanize a new generation in support of the Islamic revolution. For oil markets the outcome is volatility in the near term – reflecting the contrary winds of trade war and global growth fears with rising supply risks. Because we expect more Chinese stimulus, both as the trade talks extend and especially if they collapse, we ultimately share BCA’s Commodity & Energy Strategy view that the path of least resistance for oil prices is higher on a cyclical horizon, as demand exceeds supply (Chart 12). We remain long EM energy producers relative to EM ex-China. Chart 12Crude Oil Supply-Demand Balance Should Send Prices Higher

Crude Oil Supply-Demand Balance Should Send Prices Higher

Crude Oil Supply-Demand Balance Should Send Prices Higher

Bottom Line: The risk of military conflict has risen materially. This also drastically elevates the risk of a supply shock in oil prices that would kill global demand. The U.S. Election Adds To Geopolitical Risk The 2020 U.S. election poses another political risk for the rising equity market. The Democratic Party’s first debate will be held on June 26-27. The leftward shift in the party will be on full display, portending a possible 180-degree reversal in U.S. policy if the Democrats should win the election, with the prospect of a rollback of Trump’s tax cuts and deregulation of health, finance, and energy. The uncertainty and negative impact on animal spirits will be modest if current trends persist through the debates. Former Vice President Joe Biden remains the frontrunner despite having naturally lost the bump to his polling support after announcing his official candidacy (Chart 13). Biden is a known quantity and a centrist, especially compared to the farther left candidates ranked second and third in popular support– Vermont Senator Bernie Sanders and Massachusetts Senator Elizabeth Warren.

Chart 13

Chart 14

Biden is not only beating Sanders in South Carolina, which underscores the fact that he is competitive in the South and hence has a broader path to the White House, but also in New Hampshire, where the Vermont native should be ahead (Chart 14). These states hold the early primaries and caucuses and if Biden maintains his large lead then he will start to appear inevitable very early in the primary campaign next year. Hence a poor showing in the debate on June 27 is a major risk to Biden – he should be expected to be eschew the limelight and play the long game. Elizabeth Warren, by contrast, has the most to gain as she appears on the first night and does not share a stage with the other heavy hitters. If she or other progressive candidates outperform then the market will be spooked. The market could begin to trade off the polls. All of these candidates are beating Trump in current head-to-head polling – Biden is even ahead in Texas (Chart 15). This means that any weakness from Biden does not necessarily offer the promise of a Trump victory and policy continuity.

Chart 15

The Democrats also have a powerful demographic tailwind. The just-released projections from the U.S. Census Bureau reveal how Trump’s narrow margins of victory in the swing states in 2016 are in serious jeopardy in 2020 as a result of demographics if he does not improve his polling among the general public (Chart 16).

Chart 16

We still give Trump the benefit of the doubt as the incumbent president amid an expanding economy, but it is essential to recognize that his popular approval rating is reminiscent of a president during recession – i.e. one who is about to lose the White House for his party (Chart 17).

Chart 17

Even if there is not a recession, an increase in unemployment is likely to cost him the election – and even a further decrease in unemployment cannot guarantee victory (Chart 18). This is why we see Trump making a bid to become a foreign policy president and seek reelection on the basis that it is unwise to change leaders amid an international crisis.

Chart 18

We still give Trump the benefit of the doubt ... but his popular approval rating is reminiscent of a president during recession. The race for the U.S. senate is extremely important for the policy setting from 2021. If Republicans maintain control, they will be able to block sweeping Democratic legislation – which is particularly relevant if a progressive candidate should win the White House. However, if Democrats can muster enough votes to remove a sitting president with a strong economy – including a strong economy in the key senate swing races (Chart 19) – then they will likely win over the senate as well. Chart 19Hard To Win The Senate In 2020 While Key States Prosper

Hard To Win The Senate In 2020 While Key States Prosper

Hard To Win The Senate In 2020 While Key States Prosper

Bottom Line: The 2020 election poses a double risk to the bull market. First, the Democratic primary campaign threatens sharp policy discontinuity, especially if and when developments cause Biden to drop in the polls (dealing a blow to centrism or the political establishment). Second, Trump’s vulnerability makes him more likely to act aggressive on the international stage, whether on trade, immigration, or national security, reinforcing the risks outlined above with regard to China, Iran, Mexico, and even Europe. Rising Odds Of A No-Deal Brexit Former Mayor of London and former foreign secretary Boris Johnson looks increasingly likely to seal the Conservative Party leadership contest in the United Kingdom. It is not yet a done deal, but the shift within the party in favor of accepting a “no deal” exit is clear. None of the remaining candidates is willing to forgo that option. The newest development advances us along our decision tree in Diagram 2, altering the conditional probabilities for this year’s events. We expect the next prime minister to try to push a deal substantially similar to outgoing Prime Minister Theresa May before attempting any kamikaze run as the October 31 deadline approaches. The attempt to leverage the EU’s economic weakness will not produce a fundamental renegotiation of the exit deal, but some element of diplomatic accommodation is possible as the EU seeks to maintain overall stability and a smooth exit if that is what the U.K. is determined to accomplish. Diagram 2Brexit Decision Tree

Escalation ... Everywhere

Escalation ... Everywhere

Hence the prospect of passing a deal substantially similar to outgoing Prime Minister Theresa May’s deal is about 30%, roughly equal to the chance of a delay (28%). These options are believable as the new leader will have precious little time between taking the reins and Brexit day. The EU can accept a delay because it ultimately has an interest in keeping the U.K. bound into the union. Public opinion polling is not conducive to the new prime minister seeking a new election unless the change of face creates a massive shift in support for the Conservatives, both by swallowing the Brexit Party and outpacing Labour. If the purpose is to deliver Brexit, then the risk of a repeat of the June 2017 snap election would seem excessive. Nevertheless, the Tories’ working majority in parliament is vanishingly small, at five MPs, so a shift in polling could change the thinking on this front. The pursuit of a no-deal exit would create a backlash in parliament that we reckon has a 21% chance of ending in a no-confidence motion and new election. Bottom Line: The odds of a crash Brexit have moved up from 14% to 21% as a result of the leadership contest. The threat that the U.K. will crash out of the EU is not merely a negotiating ploy, although it will be a last resort even for the new hard-Brexit prime minister. Public opinion is against a no-deal Brexit, as is the majority of parliament, but the risk to the U.K. and EU economies will loom large over global risk assets in the coming months. Investment Conclusions Political and geopolitical risks to the late-cycle expansion are rising, not falling. U.S. foreign policy remains the dominant risk but U.S. domestic policy pre-2020 is an aggravating factor. Easing financial conditions give President Trump more ammunition to use tariffs and sanctions. Meanwhile our view that this summer will feature “fire and fury” between the U.S. and Iran has been confirmed by the tanker attacks in Oman. Tensions will likely escalate from here. Ultimately, we believe Trump is more likely to back off from the Iran conflict than the China conflict. This is part of our long-term theme that the U.S. really is pivoting to China and geopolitical risk will rotate from the Middle East to East Asia. But as highlighted above, the risk of entanglement is very high due to Trump’s approach and Iran’s incentives to raise the stakes. Oil prices will not resume their upward drift until Chinese stimulus is reconfirmed – and even then they will continue to be volatile. We remain cautious and are maintaining our safe-haven tactical trades of long gold and long JPY/USD. Matt Gertken, Vice President Geopolitical Strategist mattg@bcaresearch.com Appendix

Image

Highlights The odds of universal health care legislation being enacted in the U.S. by 2022 are about 10%-15%. Former Vice President Joe Biden is the most likely Democratic candidate in 2020, but the alternative is most likely a progressive candidate seeking universal health care. Trump is slightly favored to win in 2020, but a Trump loss is likely to translate into full Democratic control of the U.S. government, making ambitious legislation more likely to pass Congress. An overweight portfolio allocation in the S&P health care index is a sensible and defensive move. Fear selling in health care stocks could easily return but would create an exploitable trading opportunity at this late stage of the cycle. We are executing the upgrade of the S&P health care index via an upgrade of the S&P health care equipment index, which has seen a material valuation de-rating at the same time as profits are expanding, to overweight. Feature Will The Democrats Win? Can They Pass Universal Health Care? “Medicare for All,” or government-led universal health care in the United States, is less likely to become the law of the land by 2022 than the market expects. We put the probability at around 10%-15%. Here’s why. The industry faces only two certainties: Americans are getting older and the federal government is increasing its involvement. The former is a secular driver for health care demand. The latter is an inference drawn from the fact that the Republican Party failed to repeal the Affordable Care Act, or Obamacare, even when it had full control of government. It is very unlikely that the Republicans will get another chance at repeal. It is also very unlikely that the public will tolerate the current status quo forever. The result is that the U.S. will eventually end up with a restored Obamacare or an altogether new system with a greater government role. The Republican failure to repeal was not idiosyncratic – it was not based on the fact that the late Senator John McCain, who cast the decisive vote on July 27, 2017, had been diagnosed with brain cancer earlier that year. Rather, it was structural – the repeal failed because (1) it is always extremely difficult to remove an entitlement once it has been given to voters and (2) a slim majority of Americans approved of Obamacare – and still do (Chart 1).

Chart 1

Republicans went on to dismantle aspects of Obamacare, including the problematic “individual mandate.” But they did so without replacing it. The result was a severe electoral defeat in the 2018 midterm elections, despite a huge drop in the unemployment rate (Chart 2) – which matters directly in a country where 49% get their health insurance through their employer. Health care was the single most important issue driving people to vote against the ruling party in November 2018, judging by both pre-election polls and exit polls (Charts 3 & 4). Chart 2Low Unemployment Has Not Solved Health Care Woes

Low Unemployment Has Not Solved Health Care Woes

Low Unemployment Has Not Solved Health Care Woes

Chart 3

Chart 4

The need for reform is manifest. It is widely known that the U.S. spends more than other countries on health care (Chart 5) and yet achieves worse results: preventable mortality is higher than in other countries that spend less (Chart 6). Democrats have tried to overhaul the system since 1993. Even President Trump is seeking to cap prescription drug prices and maintain the Obamacare requirement that health care insurers accept customers with “pre-existing conditions.”

Chart 5

Chart 6

Uncertainty has risen since the Republicans’ midterm defeat, which increases, or is seen as increasing, the odds of a Democratic victory in 2020. Such a victory would mark the third time in 12 years that American policy would witness a 180-degree reversal – and it would have a major impact on the health sector (Chart 7). Chart 7The Sector's Response To Major Political Events

The Sector's Response To Major Political Events

The Sector's Response To Major Political Events

In truth Trump is still favored to win in 2020, on the back of the incumbent advantage – as long as the economy holds up. But with a chronically weak approval rating, and narrow 2016 margins of victory and the aforementioned midterm losses in key swing states, his odds of reelection are probably not much better than 55%. Meanwhile the Democrats are swinging to the left and may not settle simply for restoring Obamacare. Left-wing or “progressive” candidates for the Democratic nomination are polling in line with traditional center-left candidates (Chart 8), which is highly unusual (even compared with the 2007-08 race). Candidates are crowding onto the democratic socialist bandwagon in the wake of Bernie Sanders’s formidable challenge to Hillary Clinton and her subsequent loss to Trump.

Chart 8

Could a progressive candidate win the nomination? Certainly. Former Vice President Joe Biden leads the pack at this early stage in the nomination process. He would seek to restore and build upon Obamacare. The second-ranked candidate is Sanders, whose initial proposal to create Medicare for All has transformed the national debate. Following Sanders are Senators Kamala Harris, who co-sponsored the latest version of the bill with Sanders, and Elizabeth Warren, an outspoken progressive who is also in favor of universal health care (Chart 9).

Chart 9

Sanders does have a path to winning the nomination, as the leading progressive candidate at a time when the party is becoming more progressive. He performs better than Biden in head-to-head polls against Trump in the key battleground states (Chart 10). Strategic voters will have trouble convincing fellow Democrats that they should not vote for him because he is unelectable: he has a clear electoral path to the White House via Michigan, Pennsylvania, and Wisconsin, where he performed well in 2016 and polls well today. If Sanders has a chance, then Medicare for All has a chance.

Chart 10

Because it is extremely difficult to unseat an incumbent president, a victory over Trump in 2020 is only likely to occur if there is a surge in voter turnout and Democratic Party support among (1) blue-collar workers who abandoned the Democrats for Trump in 2016, or (2) young voters, women, or minorities. Any such surge would also enable the Democrats to defend their senate seats while picking up Arizona, Colorado, and Maine, which are statewide elections that will be affected by the headline presidential race. And if the Democrats win 50 seats, they would get a majority in the senate, as the vice president would break any tie. With a majority, Senate Democrats could use the “nuclear option” to bypass the filibuster and drive through their priority legislation.1 This would set a new precedent with far-reaching consequences. But recent majority leaders have already begun eroding the filibuster and there is no hard constraint preventing a ruling party from removing it entirely. It is perfectly possible, and all the more likely if the nation sweeps a progressive candidate to power in a wave of enthusiasm for dramatic changes like universal health care. In other words, any victory against Trump is likely to entail full Democratic control of government. In this scenario, Democrats would have a very good chance of passing a major piece of legislation. Hence, if a progressive wins the nomination, and makes Medicare for All the policy priority, there is at least a 50/50 chance it will pass, probably more like 60%. The catch is that a progressive may not win the nomination. There is not decisive evidence that Americans really want Medicare for All. First, Americans tend to view their own health costs as “reasonable” (Chart 11). They are not, as a whole, clamoring for a single-payer system.

Chart 11

Second, while Americans say they support Medicare for All, that support evaporates when they learn about the various policies that it would necessitate, such as eliminating private health insurance and raising taxes (Chart 12).

Chart 12

Third, most Democrats are closer to Biden’s position than Sanders’s – they want to fix Obamacare rather than revolutionize the system (Chart 13).

Chart 13

Fourth, Colorado tried to pass its own version of Medicare for All on the state level in 2016. The bill’s advocates were handed a 79% defeat by voters. Colorado is a swing state so it is not an irrelevant experiment. Fifth, independents are not shifting to the left in a way that would validate the sharp leftward shift within the Democratic Party (Chart 14). Nominating Sanders or another progressive is more likely to lead to a loss in the general election than it is to ensure that universal health care gets passed. Chart 14Independents Not Swinging Dramatically To The Left

Independents Not Swinging Dramatically To The Left

Independents Not Swinging Dramatically To The Left

A simple back-of-the-envelope exercise suggests that odds of universal health care by 2022 are about 10%-15%. Nevertheless, we attempt a conservative, back-of-the-envelope method for estimating the probability of passage. It runs like this: There is a 50% chance a progressive wins the Democratic nomination. We assume that if Biden wins it is because Democratic voters prefer a restitution of Obamacare. There is a 45% chance that Trump loses the presidential election. We assume that for the Democrats to unseat an incumbent is difficult enough that they will also win the Senate. Under these circumstances, there is a 50%-60% chance that universal health care legislation passes – even though it will be very difficult to get it over the line. (Note that the ACA passed very narrowly at a time when the Democrats had a huge tailwind due to voters’ disenchantment after the global financial crisis). With these assumptions, the conditional probability of passage is around 13.5% (0.5 x 0.45 x 0.6 = 0.135) These odds can be moderated by boosting Trump to a 69% chance of reelection (the historical average for sitting presidents), which brings down the odds of ultimate passage to 9%. Note, however, that the bond market is pricing a 27% probability of a recession 12 months from now (Chart 15). If there is a recession, then President Trump is virtually assured to lose reelection and the Democratic victor will have a strong tailwind of public support. This will increase the chance that universal health care passes to 80%. (We still assume in this case that Biden would stick with Obamacare as he would not be committed to Medicare for All and it is not an economic stimulus package). The conditional probability would become 0.5 x 0.27 x 0.8 = 11%. Chart 15Probability Of Recession Is Rising NY Fed's Yield Curve Model Suggests That The Probability Of A Recession Is Still Quite Low

Probability Of Recession Is Rising NY Fed's Yield Curve Model Suggests That The Probability Of A Recession Is Still Quite Low

Probability Of Recession Is Rising NY Fed's Yield Curve Model Suggests That The Probability Of A Recession Is Still Quite Low

In other words, whether we upgrade Trump’s chances of winning or we upgrade the chances of a recession that kicks him out of office, the odds are roughly the same at 9%-11%. And they could be a bit higher at 14%. Medicare for All has a chance of becoming law, although it is not all that great. Bottom Line: With fairly conservative assumptions the odds range from 10%-15%. that the U.S. could legislate a sweeping overhaul of the health care system and new social entitlement by 2022. This is a serious risk to the industry. Health care equities have recovered the losses suffered since Sanders’s latest push for Medicare for All, which means that it is not pricing in a high probability of passage at present. Additional policy-related selloffs are likely between now and the spring of 2020, if and when the odds increase of Sanders (or another progressive) winning the Democratic nomination. Buy Into Health Care Weakness Regardless of the likelihood of passage, the faintest hint of the winds of change has brought about significant price changes in the relevant equities. In the lead up to the 2016 U.S. presidential election, Hillary Clinton, a health care reformer (though importantly NOT a Medicare for All advocate) was polling well ahead of Donald Trump. Health care stocks underperformed the broad market in anticipation of potential reforms resulting from a Clinton win (Chart 16). Two years after Donald Trump’s election, both S&P health care equipment and S&P managed health care have significantly outperformed with the effect most dramatic in the former. Chart 17 shows the reverse picture: a “blue wave” in the 2018 midterm elections was swiftly followed by the zenith for health care stocks as the market digested the implications of a Democratic House and the resulting higher probability of a similar sweep in 2020 in the Senate and executive branch. Chart 16Election Fear Creates Buying Opportunities...

Election Fear Creates Buying Opportunities...

Election Fear Creates Buying Opportunities...

Chart 17...And History Appears To Be Repeating Itself

...And History Appears To Be Repeating Itself

...And History Appears To Be Repeating Itself

Furthermore, our prior research shows that S&P health care has been the top performer in the last equity market surge to take place between the peak of the ISM manufacturing composite index and the beginning of the subsequent recession.2 This research was confirmed in a report last month analyzing sector returns after a Fed loosening cycle begins. The S&P health care index has historically outperformed from six months before a rate cut all the way to two years after easing policy.3#fn_3 As a reminder, the market has now priced in two rate cuts over the next year. We recommend an overweight position for the broad S&P 500 health care index as well as for health care equipment. BCA’s U.S. Equity Strategy has already moved to an overweight recommendation on the S&P managed health care index, a move that has netted our portfolio 12.4% of alpha. Today U.S. Equity Strategy is raising our recommendations on both the S&P health care equipment and, more importantly, the broad S&P health care index from neutral to overweight. Further, considering U.S. Equity Strategy’s recent portfolio changes, namely moving the S&P materials index to neutral, this upgrade of S&P health care to overweight moves our cyclicals vs. defensives style preference from overweight cyclicals to neutral. This move to the sidelines on the cyclical/defensive portfolio bent has netted modest gains of 2% since its October 2, 2017 inception. Equipping The World’s Hospitals Our upgrade of S&P health care equipment to overweight is not contingent upon earnings outperformance. Rather, it is a combination of overwrought investors having created a buying opportunity, combined with health care’s historic outperformance at the end of the business cycle. Nevertheless, an examination of the sector’s macro environment is revealing. The health care equipment index has recently completed an inventory clear-out cycle, as evidenced both by a slingshot rebound in the shipments-to-inventories ratio (second panel, Chart 18) and a recovery in industry pricing power (bottom panel, Chart 18). This is remarkable in the context of the deceleration in equipment fixed-investment growth that the industry has faced since reaching decade-highs in 2017 (third panel, Chart 18). The upshot is that steady pricing and resilient volume growth should deliver positive top-line growth. The margin picture has also dramatically improved: industrial production has been surging for the past year while hours worked have remained tepid (second and third panels, Chart 19). The combination has driven our productivity proxy to a multi-year high where it has recently diverged from the relative stock price (bottom panel, Chart 19). Chart 18Inventories Have Cleared

Inventories Have Cleared

Inventories Have Cleared

Chart 19Productivity Is Soaring

Productivity Is Soaring

Productivity Is Soaring

This underpins our thesis that health care stocks in general and health care equipment stocks in particular have recently suffered based on fear, not fundamentals, amidst a stable domestic demand environment and rosy profit picture. The export channel is at least as important to the S&P health care equipment index as the domestic demand environment. In fact, roughly 60% of sector revenues are generated outside the United States. The news on this front is encouraging. Europe, the other key market for domestically-manufactured health care equipment, has lately seen a pickup in new orders and coupled with the loss of momentum in the trade-weighted U.S. dollar signal that future export growth will remain upbeat (trade-weighted U.S. dollar shown inverted and advanced, bottom panel, Chart 20). The global PMI has historically led exports. While this series has turned down, it has been diverging from export growth for the past year. We believe this is a function of the early stages of a secular trend in health care equipment: the expansion of the EM safety net with health care at its core. The same demographic trend that has been driving the explosion of health care spending in the DM for the last 20 years is rapidly impacting the EM, namely an aging population. The UN projects that the share of the population aged 65 and older in the EMs will rise from roughly 7% this year to 16% in 2060, while population growth slows to below the replacement rate, a tectonic shift in the demographic landscape (Chart 21). Meanwhile, according to IMF data, EM health care spending is approximately 5% of GDP. By contrast, the DMs stand in excess of 14%. Chart 20The Export Valve Is Wide Open

The Export Valve Is Wide Open

The Export Valve Is Wide Open

Chart 21

A catch-up phase looms, driven by both demographics and an overall global harmonization of standard of care, resulting in a secular outperformance of internationally geared health care equipment manufacturers’ earnings. This bodes well for U.S. health care equipment providers who are the technology leaders and often the only source for equipping hospitals/clinics around the globe. Notwithstanding the bright outlook, fear selling in the S&P health care equipment index has driven a reversal in the two-year valuation rerating that the index has undergone (bottom panel, Chart 22). With the valuation retreating back to its historical range, our main concern that the index is too expensive has eroded. Further, the valuation decline is coming at a time when forward earnings growth has come out of hiding and is now slated to materially outgrow the broad market (middle panel, Chart 22). Chart 22Valuations Have Returned To Earth

Valuations Have Returned To Earth

Valuations Have Returned To Earth

Bottom Line: Something has to give in this equation and macro tailwinds suggest that a valuation re-rating phase looms. Accordingly, we are moving to an overweight recommendation on the S&P health care equipment index. This move pushes our S&P health care index to an above benchmark allocation and also moves our cyclical vs. defensive preference back to neutral. The ticker symbols for the stocks in the S&P health care equipment index are: BLBG: S5HCEP – ABT, MDT, DHR, BDX, SYK, ISRG, BSX, BAX, EW, ZBH, IDXX, RMD, TFX, HOLX, ABMD, VAR. BCA’s Geopolitical Strategy echoes the tenor of these recommendations and is going long the S&P 500 health care index and the health care equipment index versus the broad market. A Word On Pharma Between 1980 and 2000, pharma earnings expanded at a record clip, taking sector share prices into the stratosphere (top panel, Chart 23). Since the zenith in the early 2000’s, margins have been continually under pressure as R&D costs have outpaced volume gains (second panel, Chart 23). However, earnings growth has continued mostly uninterrupted as the industry has raised drug prices. Since 2015, however, price increases have flat lined and now they move at the same pace as overall inflation, though the current convoluted system keeps pricing mostly opaque (bottom panel, Chart 23). We think this is the new normal. The thesis of this report revolves upon a blue vs. red probability outcome. However, as noted, both parties seem united in the fight against high drug costs and Republicans under President Trump are not averse to government intervention to drive down prices. As such, we expect the pharma pricing headwinds to remain a secular trend, driven by outrage from both sides of the aisle and even universal coverage is not enough to bear the pressure. Accordingly, we reiterate our underweight recommendation. Chart 23Pharma Remains Underweight

Pharma Remains Underweight

Pharma Remains Underweight

Conclusion Universal health care will be negative for the U.S. budget deficit but positive for economic growth. As for the macroeconomic impact of universal health care, it is complex to assess because much would depend on the extent of any reduction in private health-related sectors. Almost certainly, the U.S. would adopt a parallel system where private health care remains available, but there inevitably would be some job losses in the insurance sector. And drug companies would face downward pressure on pricing. On the other hand, the marked increase in government spending would be stimulative. And we do not see future American administrations exercising a heretofore unknown fiscal discipline once such a new entitlement is established. Many families would enjoy a reduction in health care costs. Overall, it should be positive for economic growth. Matt Gertken, Vice President Geopolitical Strategy mattg@bcaresearch.com Chris Bowes, Associate Editor U.S. Equity Strategy ChrisB@bcaresearch.com Anastasios Avgeriou, U.S. Equity Strategist anastasios@bcaresearch.com Footnotes 1 The filibuster is a means of prolonging debate and obstructing a vote. It can be defeated if 60/100 senators vote to move to end debate (“cloture”). It effectively ensures that the three-fifths majority is the standard majority needed to pass legislation in the senate. However, it is possible for the senate majority leader, backed with a simple majority, to alter the senate rules and remove the filibuster, so legislation can be passed with a simple majority. But it would be an aggressive move and a historic precedent. 2 Please see BCA U.S. Equity Strategy Weekly Report, “Portfolio Positioning For A Late Cycle Surge” dated May 22, 2018, available at uses.bcaresearch.com. 3 Please see BCA U.S. Equity Strategy Weekly Report, “Sector Performance And Fed Loosening Cycles: A Historical Roadmap” dated May 6, 2019, available at uses.bcaresearch.com. Current Recommendations

Highlights Currency markets continue to fight a tug of war between weak incoming data but easier financial conditions. Our thesis remains that the path of least resistance for the dollar is down, but the rising specter of global market volatility suggests it could catapult to new highs before ultimately reversing. Most of our pro-cyclical trades have been put offside in this environment of rising volatility. Maintain tight stops until more evidence emerges that global growth has bottomed. Large net short positioning in the Swiss franc and yen, together with cheap valuations, make them attractive from a contrarian standpoint. Hold on to CHF/NZD positions recommended on April 26. Feature Our thesis remains that global growth is in a volatile bottoming process. However, incoming data pretty much across the globe has been very weak, with the latest specter of a global trade war suggesting that economic softness could linger for longer than we originally anticipated. Given the shifting market dynamics, it is important to revisit our thesis on how to be positioned in currency markets. We do so this week via the lens of the Australian dollar, one of the market’s favorite short positions. Future reports will focus on additional global growth barometers, and when to time the shift towards a more pro-cyclical stance. Positive Divergences Chart I-1Global Growth Barometers Flashing Amber

Global Growth Barometers Flashing Amber

Global Growth Barometers Flashing Amber

On the surface, most data points appear negative for the Aussie dollar. Typical reflation indicators such as commodity prices, emerging market currencies, and industrial share prices are breaking down after a nascent upturn earlier this year. One of our favorite indicators on whether or not easing liquidity conditions will lead to higher growth are the CRB Raw Industrials index-to-gold, copper-to-gold, and oil-to-gold ratios. It is disconcerting that these indicators have moved decidedly lower together with U.S. bond yields, another global growth barometer (Chart I-1). On a similar note, currencies in emerging Asia that sit closer to the epicenter of Chinese stimulus are breaking down. This suggests that so far, policy stimulus in China has not been sufficient to lift global growth, and/or the transmission mechanism towards higher growth is not working. Not surprisingly, the Australian dollar has been breaking down at a rapid pace, putting our long AUD/USD position offside. We will respect our stop-loss at 0.68 if breached, but a few indicators suggest the bearish view on the Australian dollar is very late: Chart I-2Australian Stocks Hitting New Highs

Australian Stocks Hitting New Highs

Australian Stocks Hitting New Highs

Election Results: The recent general election outcome was a big surprise to the market, and has eased risks to both the country’s banks and housing market. The center-left Labour party, which moved further to the left in this electoral cycle, was defeated by a substantial margin. This has a few important implications. First, “negative gearing” – the practice of using investment properties that are generating losses to offset one’s income tax bill – will remain in place. This was a big overhang on the housing market, which likely exacerbated the downturn in Aussie house prices. Second, the capital gains tax exemption from selling properties will probably not be reduced from 50% to 25%, as previously pledged. Finally, the Liberal-National coalition government will maintain the policy of reimbursing investors for corporate taxes paid by the underlying company. This keeps the incentive for retirees to own high dividend-yielding equities such as those of Australian banks. Australian equities hit a new cyclical high following the election results. This suggests the return on capital for Aussie companies may have inched higher following the more pro-market leadership shift (Chart I-2). At low levels of interest rates, fiscal policy is much more potent than monetary policy. Interest Rates: The latest Reserve Bank Of Australia (RBA) minutes suggest that rate cuts are back on the agenda. But the question is, with the markets pricing in two rate cuts by the end of this year, does it still pay to be short the Aussie dollar on widening interest rate differentials? More importantly, fiscal policy is set to become decisively loose this year. The new government is slated to introduce income tax cuts as early as July. This is skewed towards lower-income households, meaning the fiscal multiplier may be larger than what the Australian economy is normally accustomed to. Meanwhile, infrastructure spending will remain high, which will be very stimulative for growth in the short term. At low levels of interest rates, fiscal policy is much more potent than monetary policy, and the RBA will be loath to cut rates more than is currently expected by the market, at a time when consumer indebtedness remains quite high, and policy rates are already close to rock-bottom levels. The key for the RBA will be the job market, which at the moment remains a pillar of support for the Aussie economy. Job growth is accelerating, and labor force participation is hitting fresh highs (Chart I-3). So long as these trends continue, the RBA can afford to remain on the sidelines for a while longer. Meanwhile, while Aussie rates continue to drift downward, it has not been particularly profitable to buy U.S. Treasurys on a hedged basis (Chart I-4). Chart I-3Australia Employment Remains Robust

Australia Employment Remains Robust

Australia Employment Remains Robust

Chart I-4It is Expensive To Short The Aussie

It is Expensive To Short The Aussie

It is Expensive To Short The Aussie

Housing Market: For more than two decades, the Australian dollar has tended to be mostly driven by external conditions, especially the commodity cycle. But for the first time in several years, domestic factors have joined in to exert powerful downward pressure on the currency. The Australian Prudential Regulation Authority (APRA) has been on a mission to surgically deflate the overvalued housing market, while engineering a soft landing in the economy. Initially, their macro-prudential measures worked like a charm, as owner-occupied housing activity remained resilient relative to “investment-style” housing. What has become apparent now is that the soft landing intended by the authorities has rapidly morphed into a housing crash (Chart I-5). This is negative for consumption, both via the wealth effect and as well as for the outlook for residential construction activity. Chart I-5Could Australian Housing Bottom Soon?

Could Australian Housing Bottom Soon?

Could Australian Housing Bottom Soon?

The good news is that policy is supposed to become supportive for Aussie homebuyers at the margin, with the government slated to introduce new initiatives to help first-time homebuyers. Should labor market improvements continue, it will also help household income levels. Over the past few decades, house prices in Australia have generally staged V-shaped recoveries when at this level of contraction. Betting on at least some stabilization going forward seems reasonable. Commodity Prices: One bright spot for the Aussie dollar has been rising terms of trade. Admittedly, most measures of Chinese (and global) growth remain weak. However, there have been notable improvements in recent months that suggest economic velocity may be picking up: Production of electricity and steel, all inputs into the overall manufacturing value chain, are inflecting higher. Intuitively, these tend to lead overall industrial production. If these advance any further, they will begin to exceed GDP growth, indicating a renewed mini-cycle (Chart I-6). Production of electricity and steel, all inputs into the overall manufacturing value chain, are inflecting higher. In recent months, both steel and iron ore prices have been soaring. Many commentators have attributed these increases to supply bottlenecks and/or seasonal demand. However, it is evident from both the manufacturing data and the trend in prices that demand is also playing a role. Meanwhile, Beijing’s clear environmental push has lifted the share of liquefied natural gas in Australia’s export mix (Chart I-7). Given that the reduction – if not the outright elimination – of pollution is a long-term strategic goal in China, this will be a multi-year tailwind. As the market becomes more liberalized and long-term contracts are revised to reflect higher spot prices, the Aussie dollar will get a boost. Chart I-6Some Green Shoots From China

Some Green Shoots From China

Some Green Shoots From China

Chart I-7Australian LNG Will Buffet Terms Of Trade

Australian LNG Will Buffet Terms Of Trade

Australian LNG Will Buffet Terms Of Trade

Valuation: In terms of currency performance, a lot of the bad news already appears priced in to the Australian dollar, which is down 15% from its 2018 peak, and 38% from its 2011 peak. Meanwhile, Australian dollar short positions appeared to have already hit a nadir. This suggests outright short AUD bets are at risk from either upside surprises in global growth or simply the forces of mean reversion (Chart I-8). One of our favorite metrics for the Australian dollar’s fair value is its real effective exchange rate relative to its terms of trade. On this basis, the Aussie dollar is cheap by about 10% (Chart I-9). Chart I-8Short AUD: ##br##A Consensus Trade

Short AUD: A Consensus Trade

Short AUD: A Consensus Trade

Chart I-9AUD Is Attractive From A Terms Of Trade Perspective

AUD Is Attractive From A Terms Of Trade Perspective

AUD Is Attractive From A Terms Of Trade Perspective

China Credit Cycle: We have discussed at length how a revival in the Chinese credit cycle will help global and Australian growth. On the real estate front, residential property sales remain soft, but evidence from tier-1 and even tier-2 cities is signaling that this may be behind us, given robust sales. Over the longer term, the ebb and flow of property sales have usually been in sync across city tiers. A revival in the property market will support construction activity and investment. Chart I-10How Long Will The Weakness In China Last?

How Long Will The Weakness In China Last?

How Long Will The Weakness In China Last?

House prices have been rising to the tune of 10%-15% year-on-year, and may be sniffing an eventual pick-up in property volumes. Finally, Chinese retail sales including those of durable goods remain very weak. Car sales are deflating at the fastest pace in over two decades. But the latest VAT cut by the government is being passed through to consumers, with an increasing number of car manufacturers cutting retail prices. This should help retail sales (Chart I-10). Other Global Growth Barometers Investors looking for more clarity on the global growth picture from the April and May data prints remain in a quandary. And the preliminary European PMI numbers this morning offered no glimmers of hope. That said, the most volatile components of euro area growth tend to be investment and net exports. Should they both pick up on the back of stronger external demand, GDP could easily gravitate towards 1.5%-2%, pinning it well above potential. The German PMI is currently among the weakest in the euro zone. But forward-looking indicators suggest we may be on the cusp of a V-shaped bottom over the next month or so (Chart I-11). Chart I-11German Manufacturing Might Be At The Cusp Of A V-Shaped Recovery

German Manufacturing Might Be At The Cusp Of A V-Shaped Recovery

German Manufacturing Might Be At The Cusp Of A V-Shaped Recovery

The broad message is that global growth is in the midst of volatile bottoming process. However, before evidence of this fully unfolds, markets are likely to be swayed by the ebbs and flows of higher-frequency data. We recommend maintaining a pro-cyclical bias at the margin, but having tight stop losses as well as positions in both the Swiss franc and yen as insurance. Housekeeping Our buy-limit order on the British pound was triggered at 1.30 on March 29th. As we argued at the time, the pound was sitting exactly where it was after the 2016 referendum results, but the odds of a hard Brexit had significantly fallen. Since then, policy-induced volatility has led to a significant depreciation in the pound, with our position at risk of being stopped out at our 1.25 stop-loss this week. Given the rising specter of political volatility, we will respect our stop-loss if breached at 1.25. On the domestic front, economic surprises in the U.K. relative to both the U.S. and euro area continue to soar. The reality is that the pound and U.K. gilt yields should be much higher – solely on the basis of hard incoming data. Employment growth has been holding up very well, wages are inflecting higher, and the average U.K. consumer appears in decent shape (Chart I-12). The CPI data this week confirm that the domestic environment is hardly deflationary. That said, given the rising specter of political volatility, we will respect our stop-loss if breached at 1.25. Chart I-12Hold GBP/USD, But Stand Aside At 1.25

Hold GBP/USD, But Stand Aside At 1.25

Hold GBP/USD, But Stand Aside At 1.25

Chester Ntonifor, Foreign Exchange Strategist chestern@bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the U.S. have been soft: The Michigan consumer sentiment index jumped to 102.4 in May. However, the Chicago Fed national activity index fell to -0.45 in April. The Redbook index increased by 5.4% year-on-year in May. Existing home sales contracted by 0.4% month-on-month to 5.2 million in April. Moreover, new home sales fell by 6.9% month-on-month in April. The Markit composite index fell to 50.9 in April. The manufacturing and services PMI fell to 50.6 and 50.9 respectively. Importantly, this a just a nudge above the 50 boom/bust level. DXY index initially increased by 0.3%, then plunged on the weak PMI data, returning flat this week. The FOMC minutes released on Wednesday reiterated that the recent drop in core inflation is mostly transitory, and that no strong evidence exists for a rate change in either direction. With the forward market already pricing an 82% probability of a rate cut this year, any hawkish shift by the Fed will be a surprise. However, this will not necessarily be bullish for the dollar, if accompanied by a global growth bottom. We remain of the view that the path of least resistance for the dollar is down. Report Links: President Trump And The Dollar - May 9, 2019 Take Out Some Insurance - May 3, 2019 Currency Complacency Amid A Global Dovish Shift - April 26, 2019 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area have been mixed: Headline consumer price inflation was unchanged at 1.7% year-on-year in April, while core inflation increased to 1.3%. The current account balance narrowed to a surplus of 24.7 billion euros in March. However, this was above expectations. German GDP was unchanged at 0.6% year-on-year in Q1. The euro area Markit composite PMI was flat at 51.6 compared to the last reading of 51.5. Below the surface, both the manufacturing and services PMIs fell to 47.7 and 52.5, respectively. German composite PMI was held up at 52.4 by the services component that came in at 55. However, the manufacturing component fell to 44.3. German IFO current assessment dropped to 100.6 in May, and the business climate dropped to 97.9. In France, the Markit composite PMI came in at 51.3. The manufacturing and services PMIs both increased, to 50.6 and 51.7 respectively. This was the one bright spot in euro area data. EUR/USD has been flat this week, with recent data being on the softer side. The PMI data remain subdued, in particular. Meanwhile, political uncertainties continue to weigh on investors’ sentiment. Report Links: Take Out Some Insurance - May 3, 2019 Reading The Tea Leaves From China - April 12, 2019 Into A Transition Phase - March 8, 2019 The Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been mixed: Q1 annualized GDP grew by 2.1% quarter-on-quarter, well above estimates. Industrial production fell by 4.3% year-on-year in March, but was higher than the previous reading of -4.6% in February. Capacity utilization fell by 0.4% month-on-month in March. Exports contracted by 2.4% year-on-year in April, while imports increased by 6.4% year-on-year. The total trade balance thus narrowed from ¥528 billion to ¥64 billion. Notably, the exports to China fell by 6.3%, while exports to the U.S. increased by 9.6%. Machinery orders fell by 0.7% year-on-year in March. Nikkei manufacturing PMI fell below 50, coming in at 49.6 in May. USD/JPY fell by 0.5% this week. Yutaka Harada, a dovish member of the BoJ, warned during a news conference that by hiking the consumption tax rate at this critical juncture, Japan could risk sliding into a recession. With core CPI far from its 2% target, more monetary easing is probably exactly what the doctor ordered. Report Links: Beware Of Diminishing Marginal Returns - April 19, 2019 Tug OF War, With Gold As Umpire - March 29, 2019 A Trader’s Guide To The Yen - March 15, 2019 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data in the U.K. have been firm: The Rightmove house price index increased by 0.1% year-on-year in May. The orders component of the CBI industrial trends survey decreased to -10 in May. Retail sales increased by 3% year-on-year in April. Producer prices and input prices increased by 2.1% and 3.8%, year-on-year respectively in April. Headline inflation and core inflation increased by 2.1% and 1.8% year-on-year in April, both below expectations. GBP/USD decreased by 0.6% this week. Teresa May offered MPs a vote on a second referendum on Brexit, which considers a tighter customs union with the EU. The ongoing Brexit chaos has increased volatility in the pound. Report Links: Take Out Some Insurance - May 3, 2019 Not Out Of The Woods Yet - April 5, 2019 A Trader’s Guide To The Yen - March 15, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been mostly negative: ANZ Roy Morgan weekly consumer confidence index increased to 117.2 this week. Westpac leading index fell by 0.1% month-on-month in April. Completed construction work fell by 1.9% in Q1. AUD/USD fell by 0.3% this week. During this week’s federal election, the coalition government led by Prime Minister Scott Morrison won. Besides the political development, the RBA governor Philip Lowe gave a speech on Monday, highlighting external shocks to Australian economy. He also expressed the positive outlook for Australian economy in the second half of 2019 and 2020, supported by the ongoing capex in infrastructure and resources sectors, together with strong population growth. More importantly, he mentioned that the RBA would consider the case for lower interest rates, which is a dovish shift from previous speeches. We are long AUD/USD with a tight stop at 0.68. Report Links: Beware Of Diminishing Marginal Returns - April 19, 2019 Not Out Of The Woods Yet - April 5, 2019 Into A Transition Phase - March 8, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand have been mixed: Credit card spending growth missed expectations, coming in at 4.5% year-on-year in April. Retail sales increased by 0.7% quarter-on-quarter in Q1. Retail sales excluding autos increased by 0.7% quarter-on-quarter in Q1. NZD/USD fell by 0.3% this week. NZD/USD is currently trading at a 7-month low around 0.65. A bleak external picture is worrisome for the kiwi. We continue to favor the AUD/NZD cross, from a strategic standpoint. Report Links: Not Out Of The Woods Yet - April 5, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been solid: Retail sales increased by 1.1% month-on-month in March. In particular, retail sales excluding autos increased by 1.7% month-on-month, well above estimates. USD/CAD appreciated by 0.3% this week. The better-than-expected retail sales data in March sparked a small rally in the loonie. However, the rally proved to be short-lived following softer oil prices. Positive data surprises in Canada will have to be sustained for the loonie to find some measure of support. Report Links: Currency Complacency Amid A Global Dovish Shift - April 26, 2019 A Shifting Landscape For Petrocurrencies - March 22, 2019 Into A Transition Phase - March 8, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data in the Switzerland have been positive: Money supply (M3) growth was unchanged at 3.5% year-on-year in April. Industrial production increased by 4.3% year-on-year in Q1, albeit lower than the last reading of 5.1%. USD/CHF fell by 0.8% this week. As we argued in last week’s research note, the increasing global market volatility has reignited interest in the Swiss franc. We continue to recommend the franc as an insurance policy amid rising geopolitical risk. Report Links: What To Do About The Swiss Franc? - May 17, 2019 Beware Of Diminishing Marginal Returns - April 19, 2019 Balance Of Payments Across The G10 - February 15, 2019 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

There was little data out of Norway this week: The unemployment rate came in at 3.5% in March, well below consensus of 3.7% and the previous reading of 3.8%. USD/NOK fell by 0.4% this week. Rising geopolitical risks will be supportive of the oil market and put a floor under the krone. Aside from the U.S.-Iran tensions, the world faces the prospect of the loss of Venezuelan production, and significant outages in Libya, which are all bullish. Meanwhile, Norway remains one of few G10 countries that can hike interest rates in the near term. Report Links: Currency Complacency Amid A Global Dovish Shift - April 26, 2019 A Shifting Landscape For Petrocurrencies - March 22, 2019 Balance Of Payments Across The G10 - February 15, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data in Sweden have been positive: Capacity utilization increased by 0.5% in Q1. Moreover, the unemployment rate fell to 6.2% in April. This was well below expectations of 6.8% and the previous month’s reading of 7.1%. USD/SEK fell by 0.3% this week. While we favor both the NOK and SEK against the U.S. dollar, near-term factors are more bullish for the krone. Our long NOK/SEK position is currently 4.38% in the money. Stick with it. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Global Liquidity Trends Support The Dollar, But... - January 25, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Closed Trades

Highlights So What? Markets remain complacent about U.S.-China trade. Why? The U.S. has escalated the trade war by threatening sanctions on key Chinese tech firms. Chinese President Xi Jinping is preparing his domestic audience for protracted struggle. U.S. domestic politics do not prohibit, and likely encourage, a tough stance on China. Farmers are not a constraint on Trump — economic growth is. Go long spot gold and JPY-USD. Feature Markets remain complacent. Chart 1 suggests that while the combination of unilateral trade tariffs and spiking U.S. 10-year Treasury yields was enough to sink the S&P 500 in 2018, the former alone cannot do so today. Chart 1Tariffs Alone Not Enough To Sink Equities? Wrong.

Tariffs Alone Not Enough To Sink Equities? Wrong.

Tariffs Alone Not Enough To Sink Equities? Wrong.

Specifically, the increase in the Section 301 tariff rate from 10% to 25% on $200 billion worth of Chinese imports and the threat of a new 25% tariff on the remaining $300 billion worth of Chinese imports in just a month’s time has only led to a 3% pullback in equities since May 3. That was the last trading day prior to President Donald Trump’s infamous tweet about hiking the tariff. Unlike the trade war escalation in October through November of last year, the Federal Reserve is no longer hiking rates, China’s economic indicators have bottomed, and U.S. equity investors have now fully imbibed the “Art of the Deal.” The consensus holds that the escalation of trade tensions with China is contained within the context of Trump’s well-known routine of inflicting pain and then compromising. We would wager that the bond market is right and equities are wrong. Equities will converge to the downside, unless the market receives a concrete positive catalyst that improves the near-term outlook for U.S.-China relations and hence global trade. The problem is that for equities such a catalyst could happen at any time in the form of additional Chinese stimulus. Therefore, higher volatility is the only guaranteed outcome. The sudden onslaught of U.S. pressure makes it harder for Chinese President Xi Jinping to offer structural concessions to his American counterpart without looking weak. It was easier to do so when the threat of tariffs was under wraps, as was the case between December 1 and May 5. This new obstacle informed our decision to close out our long China equities and long copper trades and downgrade our end-June trade deal probability from 50% to 40%. But the escalation of tensions makes stimulus more likely to surprise to the upside, which will at least partially offset the negative hit to global sentiment and the trade outlook. Waiting For A Positive Political Intervention Three negative geopolitical catalysts loom in plain sight, while investors are still waiting on a positive catalyst. The negatives: China has not yet announced retaliation to the U.S. Commerce Department’s blacklisting of Huawei and a handful of other Chinese tech firms; the U.S. could implement the blacklist within three months, increasing the risk of a broader “tech blockade” against China; and the U.S. authorities are prepared to extend tariffs to all Chinese goods in one month. Meanwhile there are no high-level talks currently scheduled between the principal Chinese and American negotiators as we go to press. This could change quickly. But if negotiating teams do not hold substantive meetings with positive reports afterwards, then investors cannot be sure that Presidents Donald Trump and Xi Jinping will speak to each other, let alone finalize a substantive trade deal, at the G20 in Japan on June 28-29. The macro backdrop is hardly encouraging: global export volumes are contracting and the dollar’s fall may be arrested amid a huge spike in global policy uncertainty. Any rebound in the greenback will pile additional pressure onto trade flows, at least until the market sees a substantial increase in Chinese stimulus (Chart 2). Furthermore, it is concerning that President Trump, a businessman president and champion of American manufacturing, is raising tariffs at a time when lending and factory activity are already slowing in the politically vital Midwestern states (Chart 3). The implication is that he is unfazed by economic risks and therefore less predictable. He is pursuing long-term national foreign policy objectives at the expense of everything else. This may be patriotic but it will be painful for global equity investors. Chart 2Trump Unfazed By Deteriorating Global Economy

Trump Unfazed By Deteriorating Global Economy

Trump Unfazed By Deteriorating Global Economy

Chart 3Economic Activity Is Already Slowing

Economic Activity Is Already Slowing

Economic Activity Is Already Slowing

Chart 4Markets Blasé About Looming Risks

Markets Blasé About Looming Risks

Markets Blasé About Looming Risks

It is not only the S&P 500 that is failing to register the dangerous combination of weak global trade and escalating U.S.-China strategic conflict. Our colleague Anastasios Avgeriou of the BCA U.S. Equity Strategy points out that the “Ted spread,” the premium charged on interbank lending over the risk-free rate, is as docile as the safe-haven Japanese yen (Chart 4). President Xi Jinping, however, is not so blasé. He took a trip to Jiangxi province on May 20 to declare that China is embarking on a “new Long March.” This is a reference to the legendary strategic withdrawal executed by the early Chinese Communist Party in its civil war against the nationalists in 1934-35. It was an 8,000-mile slog across the rugged terrain of western and central China, peppered with battles against warlords and nationalists, in which nearly nine-tenths of the communist troops never made it. It is a historical event of immense propagandistic power used to celebrate the CPC’s resilience and ultimate triumph over corrupt and capitalist forces backed by imperialist Western powers. Most importantly, the Long March culminated in Mao Zedong’s consolidation of power over the party and ultimately the nation. In short, President Xi just told President Trump to “bring it on,” as he apparently believes that a conflict with the U.S. will strengthen his rule. The S&P 500 and the “Ted spread” are failing to register the dangerous combination of weak global trade and escalating U.S.-China strategic conflict. Trump, meanwhile, operates on a much shorter time horizon. He is coming closer to impeachment, as House Speaker Nancy Pelosi sharpens her rhetoric and negotiations over a bipartisan infrastructure bill collapse. Impeachment will fail and in the process will most likely help Trump’s reelection chances. But gridlock at home means that one of our top five “Black Swan” risks for 2019 is now being activated: Trump is at risk of becoming a lame duck and is therefore looking for conflicts abroad as a way of stirring up support at home. Bottom Line: The bad news in the trade war is all-too-apparent while good news is elusive. Yet key “risk off” indicators have hardly responded. We recommend going long JPY-USD on a cyclical basis on the expectation that the market will continue to have indigestion until a positive catalyst emerges in the trade talks. Trump’s Trade War Calculus

Chart 5