Economy

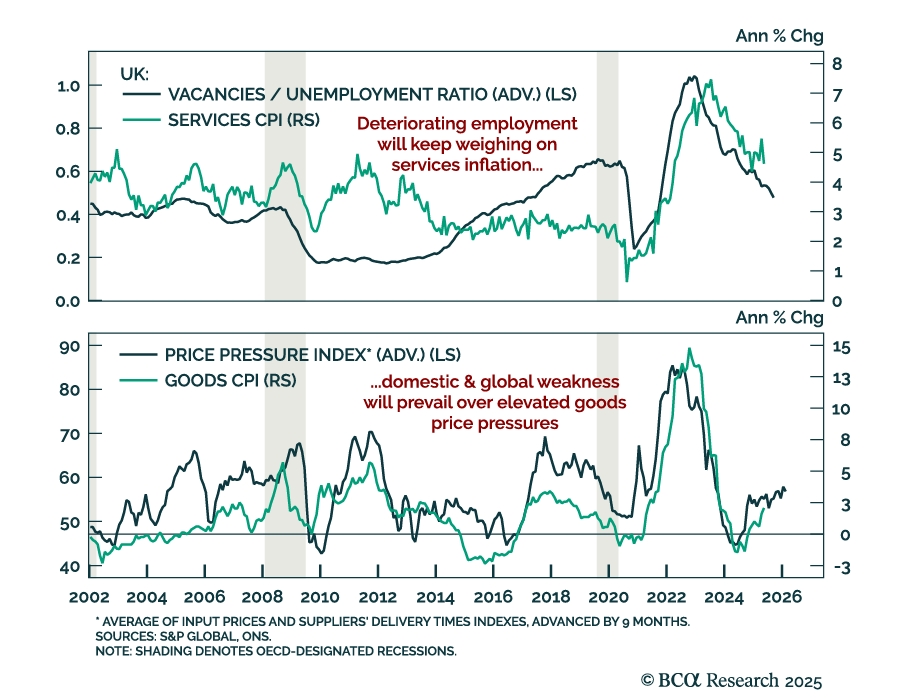

UK disinflation and labor market softening support our overweight in Gilts and short GBP trade. UK CPI came in slightly hotter than expected in May, with headline inflation at 3.4% y/y (vs. 3.5% in April) and core CPI meeting expectations at 3.5%, down from…

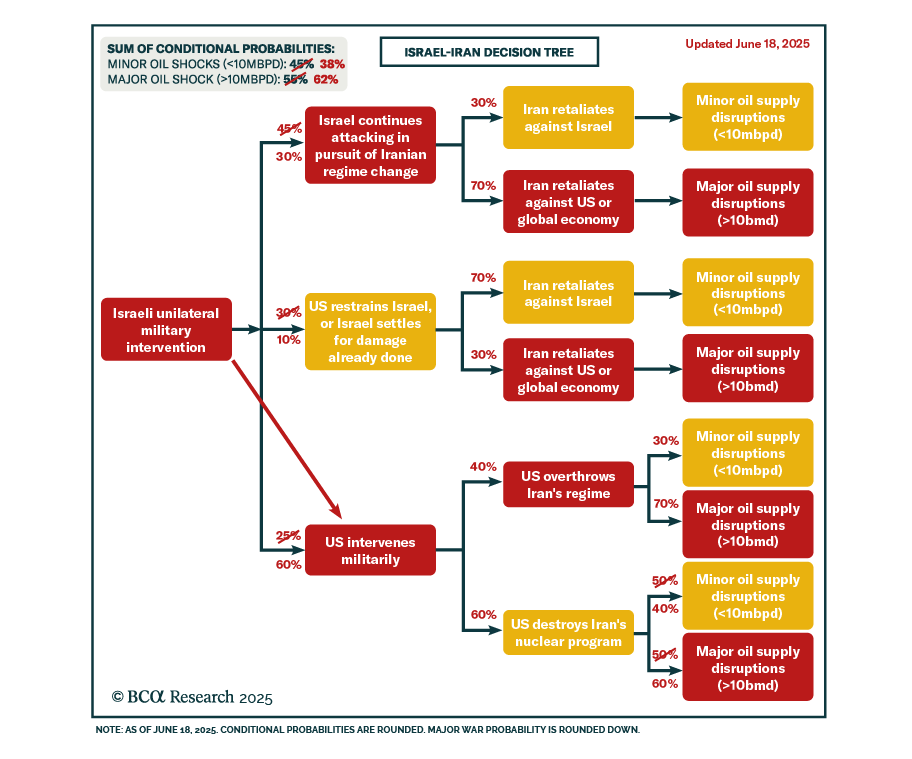

Our Geopolitical strategists expect US involvement in Israel’s military campaign against Iran, raising near-term risks to oil supply and market stability. Iran is likely to retaliate by targeting regional oil production and transport infrastructure,…

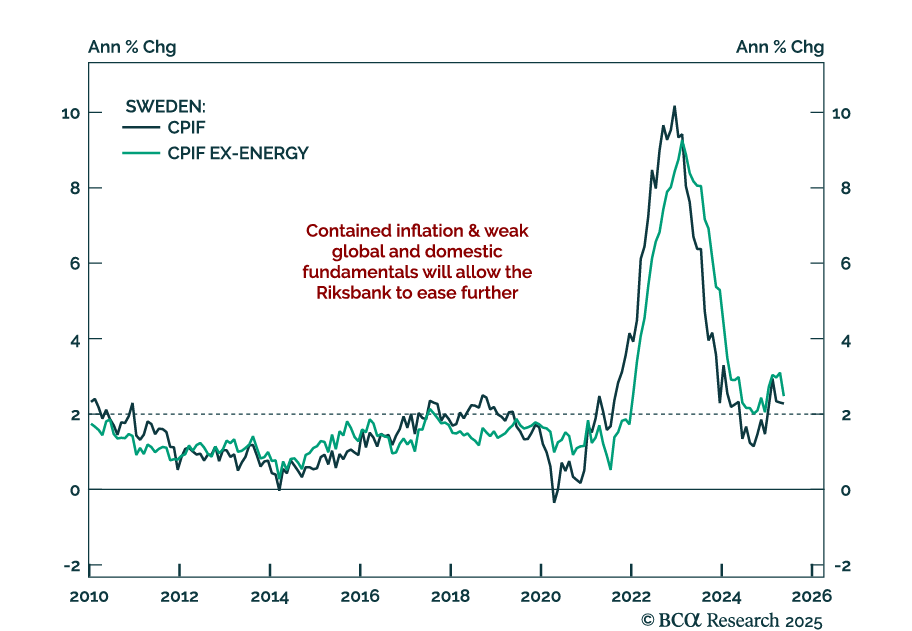

Sweden’s economic fragility and disinflation support further easing, reinforcing our long SEK rates and NOK/SEK trades. The Riksbank cut rates by 25 bps to 2.0% and projected an additional cut, consistent with prior OIS pricing. Forecasts for both headline…

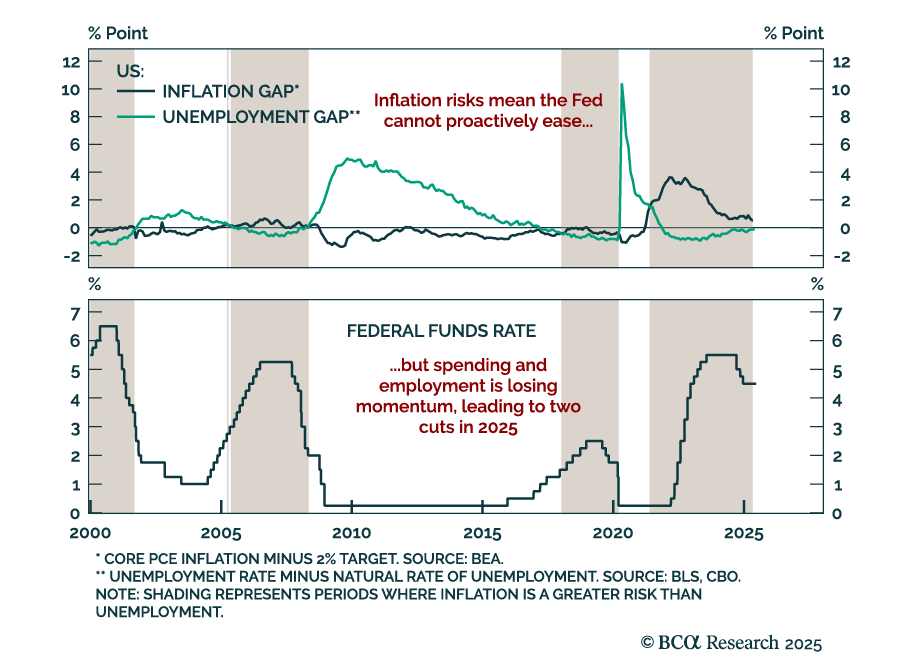

The Fed held rates steady between 4.25% to 4.5% and maintained a hawkish tilt despite soft data, reinforcing our long-duration and steepener trades. The updated dot plot showed upward revisions to both inflation and unemployment projections, as well as to…

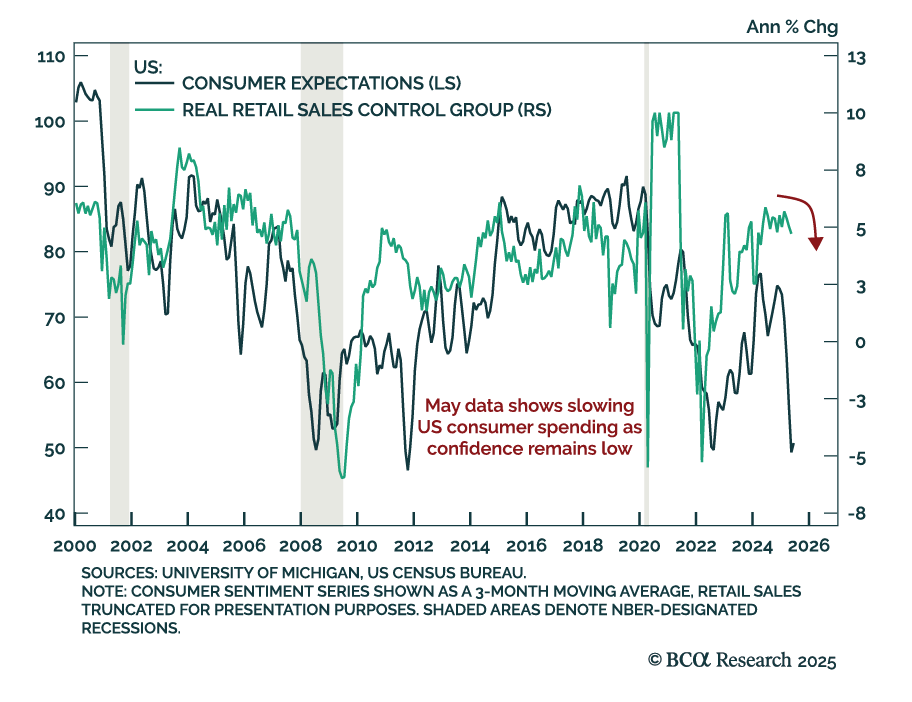

US May retail sales missed expectations, reinforcing our defensive allocation stance. Headline sales fell 0.9% m/m from a downwardly revised -0.1%. Core sales dropped 0.1%, while the control group rose 0.4%, beating estimates. Auto sales were especially weak…

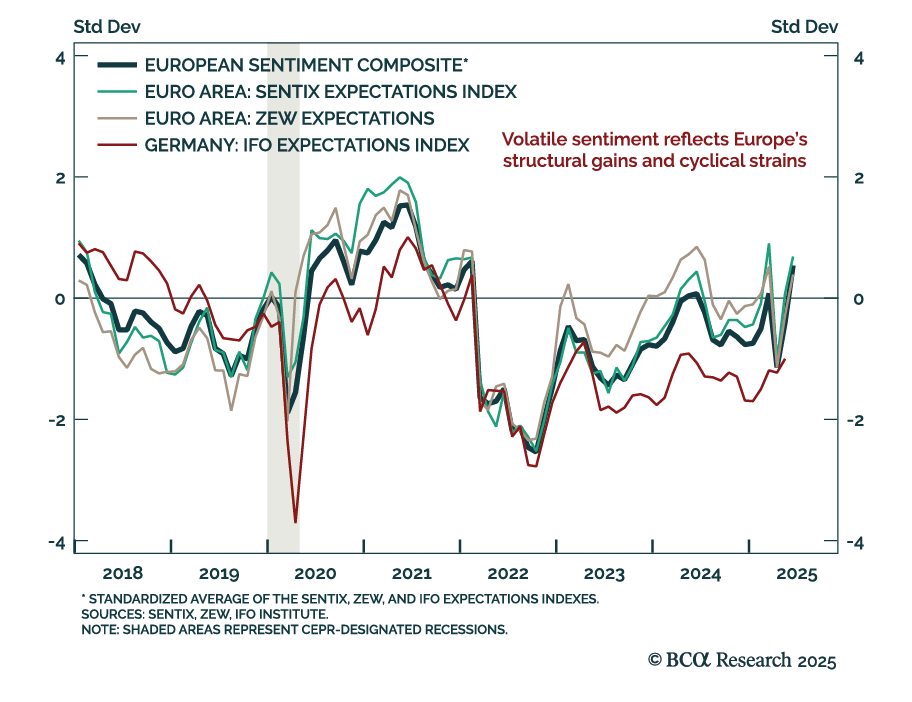

ZEW expectations jumped in May, but underlying macro fragility supports a cautious stance on eurozone assets. The ZEW expectations index for the euro area rose to 35.3 from 11.6, with Germany also beating expectations. The current situation component improved…

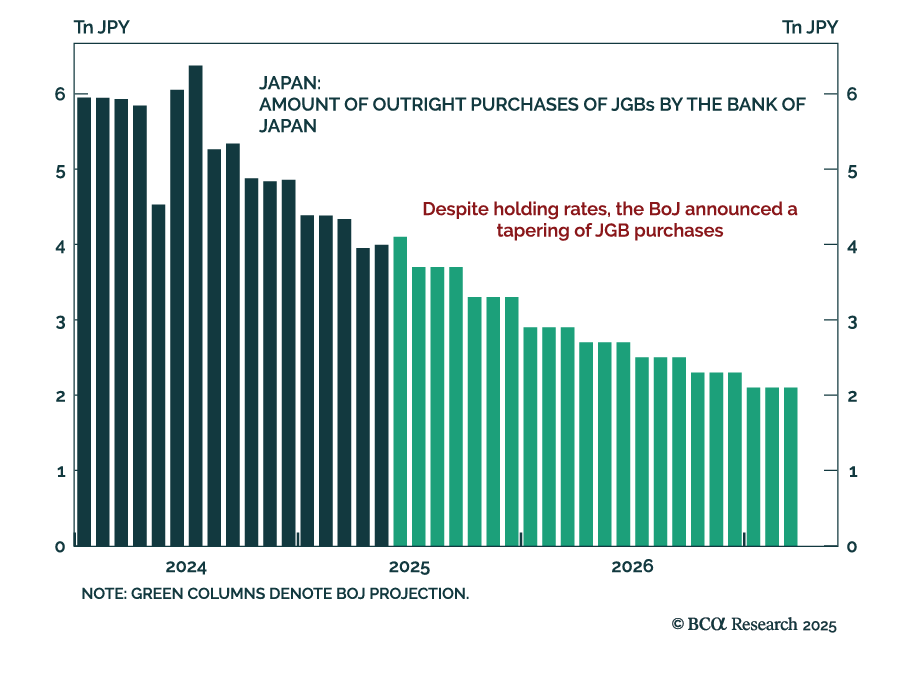

The BoJ’s decision to keep rates unchanged while announcing a tapering of bond purchases reinforces our underweight stance on JGBs and long bias on the yen. While the decision was broadly neutral, the reduction in asset purchases adds a hawkish undertone,…

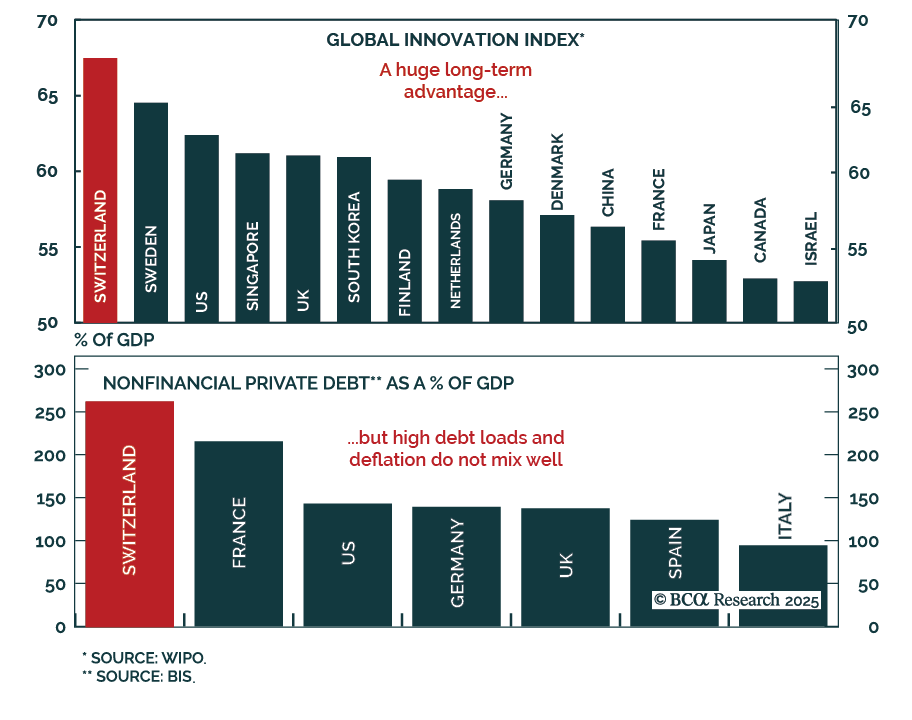

Our European Investment strategists believe Switzerland is no longer a tactical haven and recommend underweighting CHF and Swiss equities in favor of Swiss bonds. The country retains strong structural fundamentals: High productivity, innovation, robust…

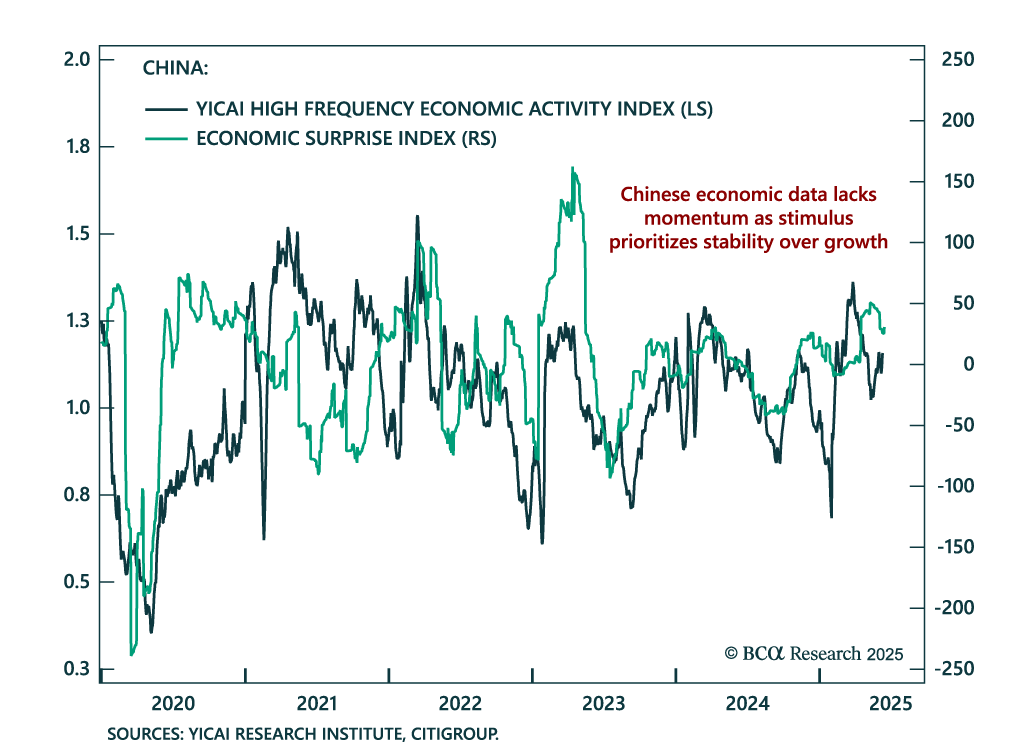

Household data beat in May, but China’s macro story remains fragile, reinforcing our overweight in local government bonds. Traditional supply-side activity decelerated, with industrial production and fixed asset investment both weaker, while retail sales and…

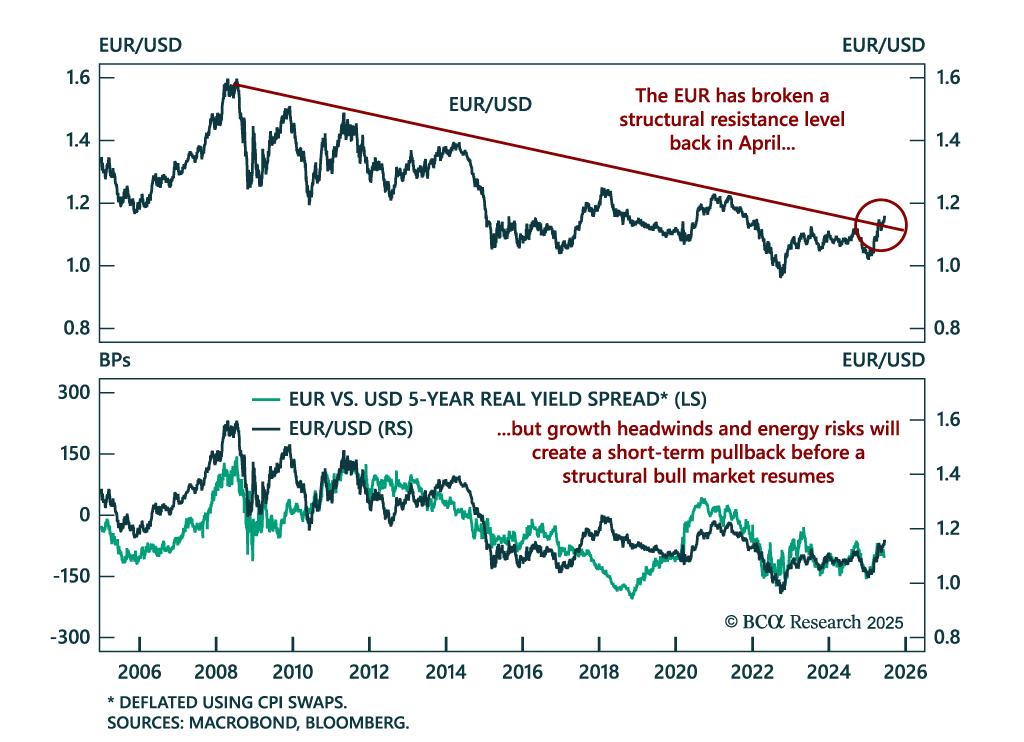

Short term euro upside is limited despite a structural bull case, as fragile growth, easing ECB policy, and geopolitical risks cap further gains. EUR/USD broke above structural resistance in April amid optimism over German stimulus and US political…