Economy

The Q3 earnings season is coming to an end. By Friday, 481 companies in the S&P 500 index had reported earnings. In aggregate, the results are generally favorable. The share of companies whose earnings exceeded analyst expectations (81.9%) is above the…

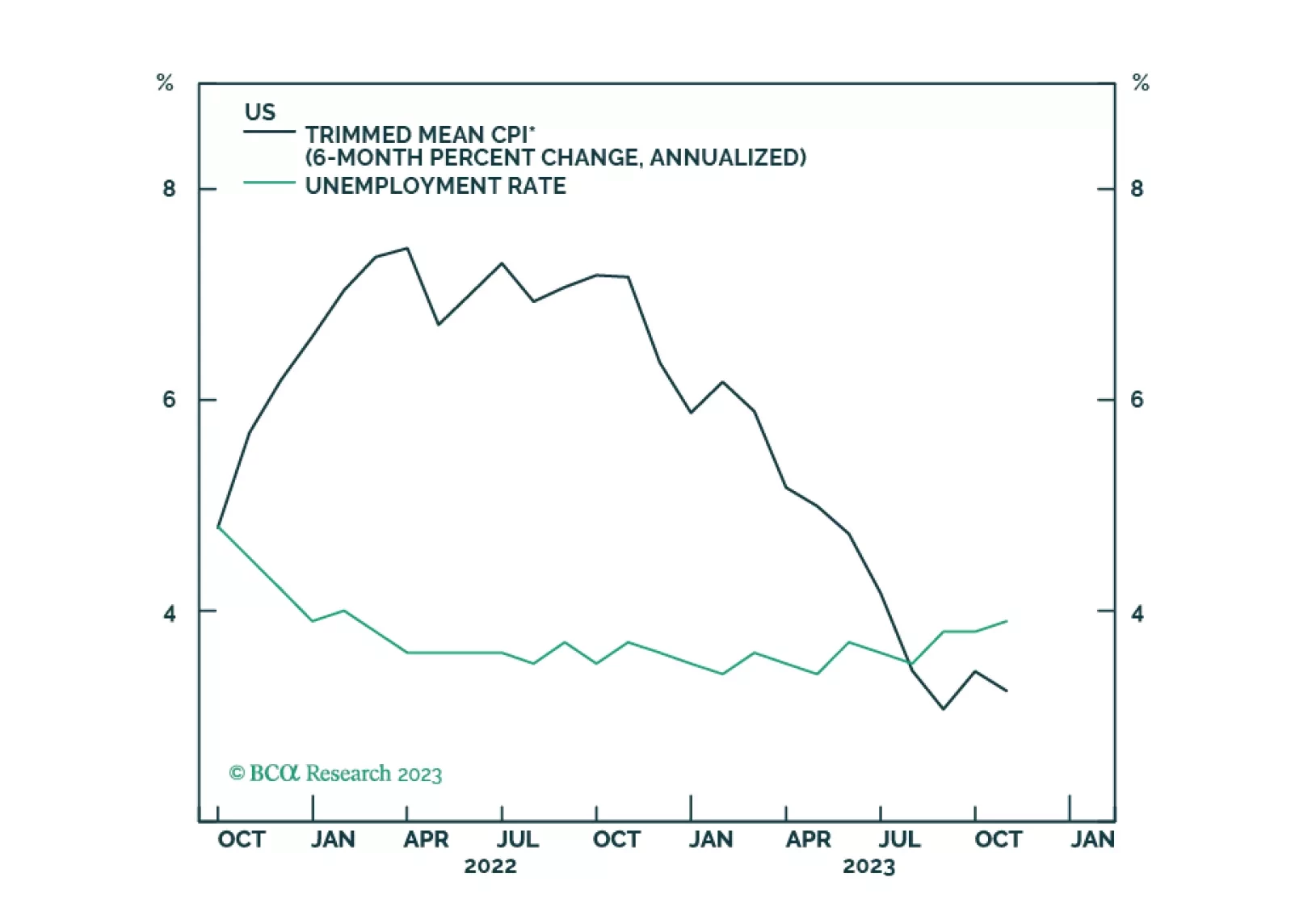

The US nonfarm payroll report is an important monthly data release that investors scrutinize for updates on the state of the US labor market and economy more broadly. In the current context, the updates help gauge whether the US economy is heading toward…

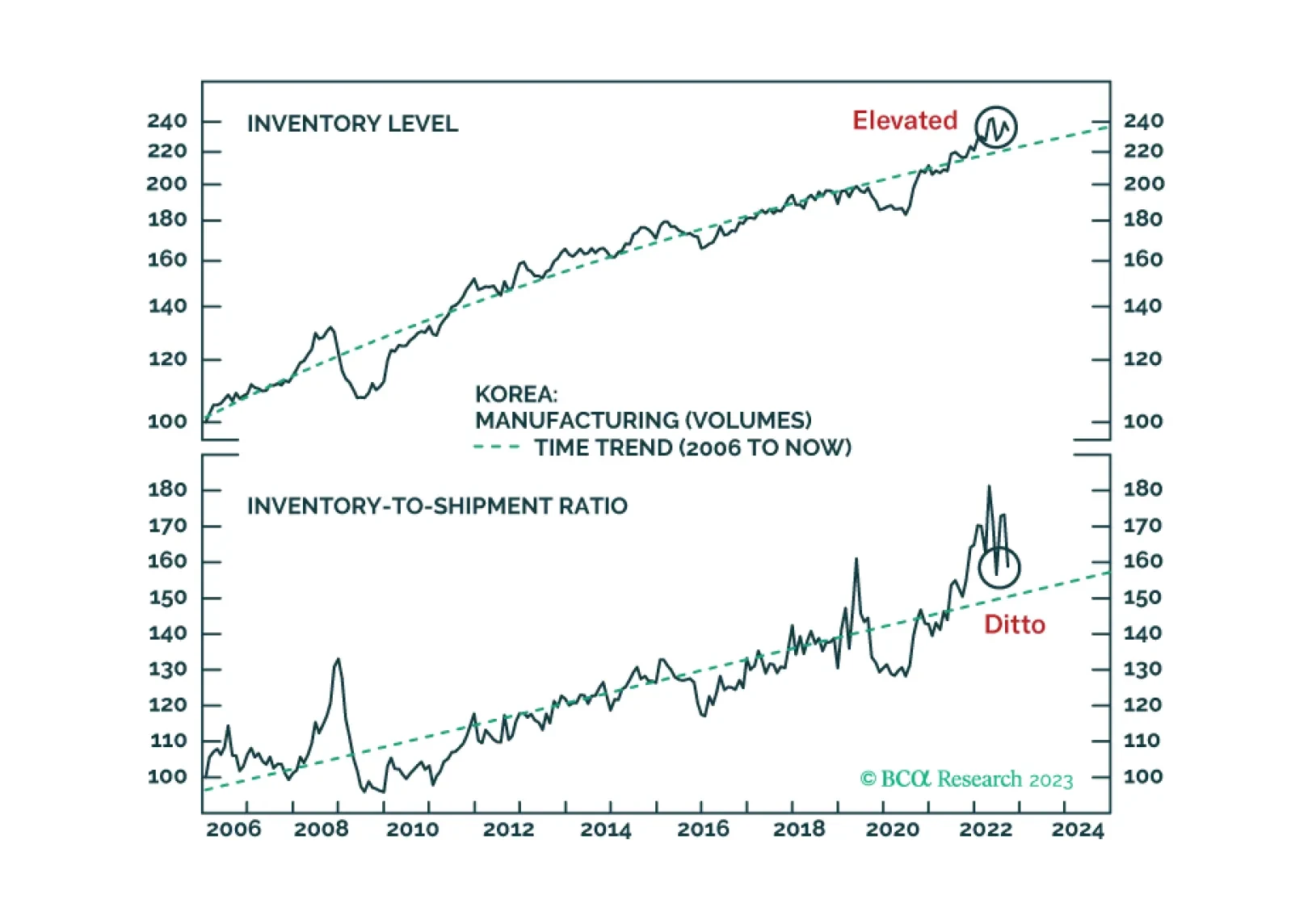

According to BCA Research's Emerging Markets Strategy service, investors should focus on fluctuations in final demand rather than inventories. A common narrative endorsed by many market participants is that inventory restocking worldwide will support the…

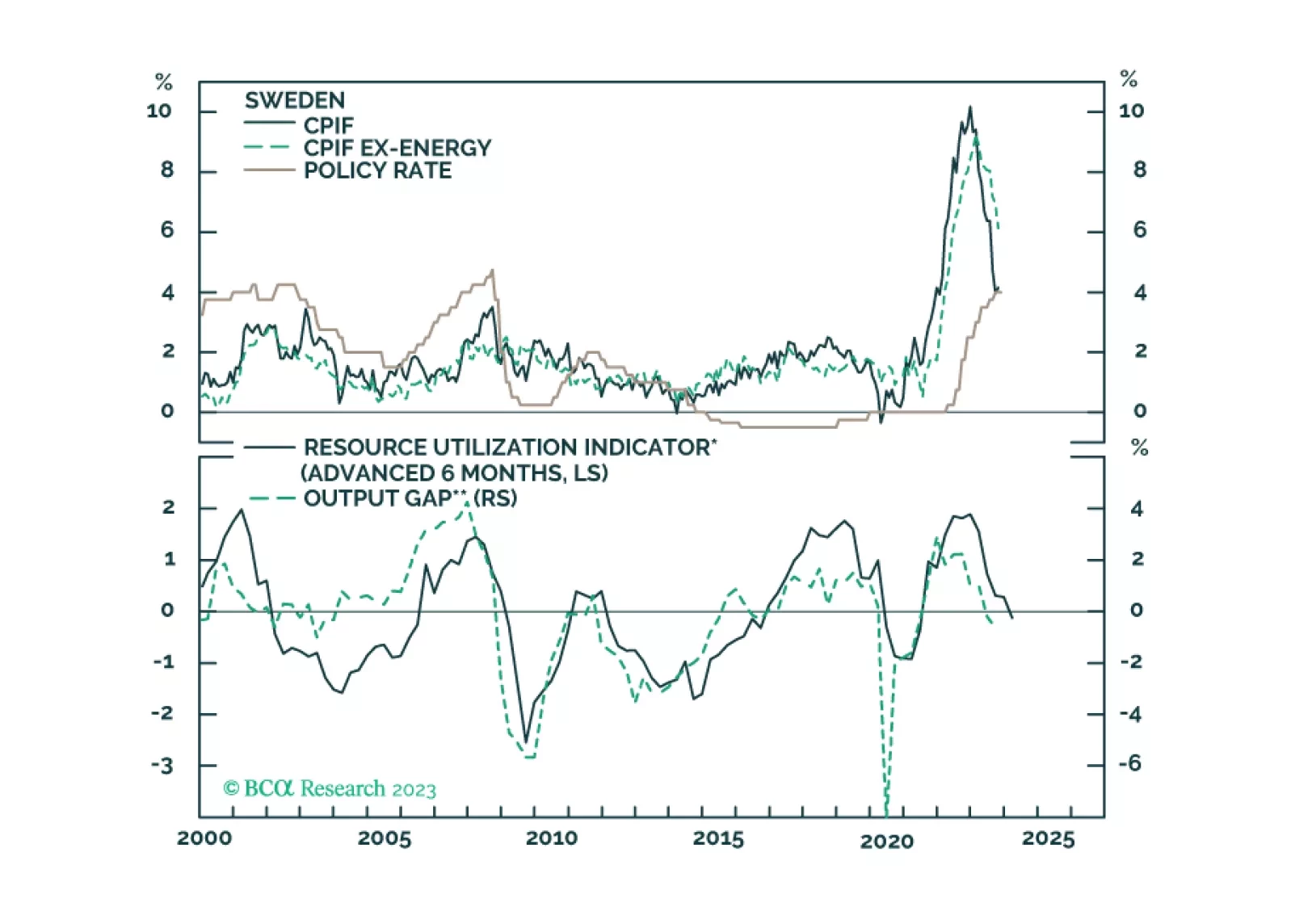

This report looks at the prospects for the Swedish krona, following the pause by the Riksbank.

Most developed market central banks have paused hiking interest rates. With interest-rate differentials having been the most important driver of currencies over the last two years or so, the focus might now shift to other factors. One such factor could be…

Our kinked Phillips curve framework predicted the immaculate disinflation of 2023. That same framework is now warning that the global economy is heading towards a recession in the second half of 2024.

European flash PMI estimates for November sent a slightly less pessimistic signal on Thursday. The Eurozone composite PMI climbed by 0.6 points to 47.1, beating expectations of a more muted increase to 46.8. Notably, both the manufacturing and services…

Global cyclical sectors are outperforming defensive sectors on a year-to-date basis. The bulk of this outperformance occurred in the first seven months of the year. Relative valuations contributed to this dynamic as last year's selloff was more pronounced…

BCA Research's Commodity & Energy Strategy service concludes that lithium demand will rise over the long run. Lithium prices are continuing the selloff that began earlier this year, which was caused by strong production and mining capex increases. …

Contrary to the prevalent belief in the global investment community, goods/merchandise inventories in the US and East Asia are rather elevated. Financial markets respond to final demand fluctuations, not inventory restocking. Global manufacturing/trade will continue contracting, even though the pace of contraction might moderate in the near run. We recommend that investors fade the current rally.