Economy

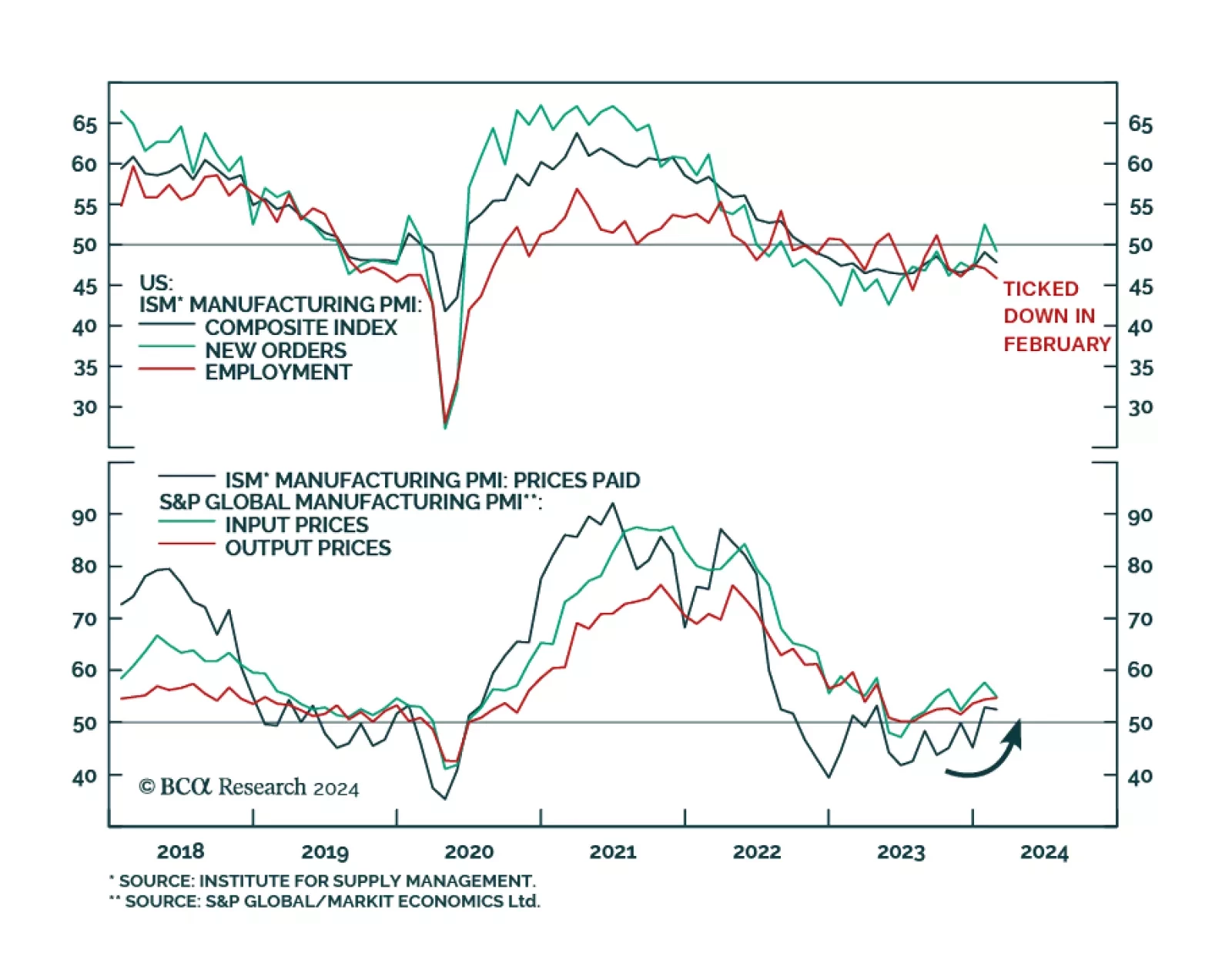

The US ISM manufacturing PMI release for February disappointed consensus expectations. The headline index relapsed to 47.8 after climbing to a 15-month high of 49.1 in January, falling below expectations of a continued slowdown in the pace of contraction to…

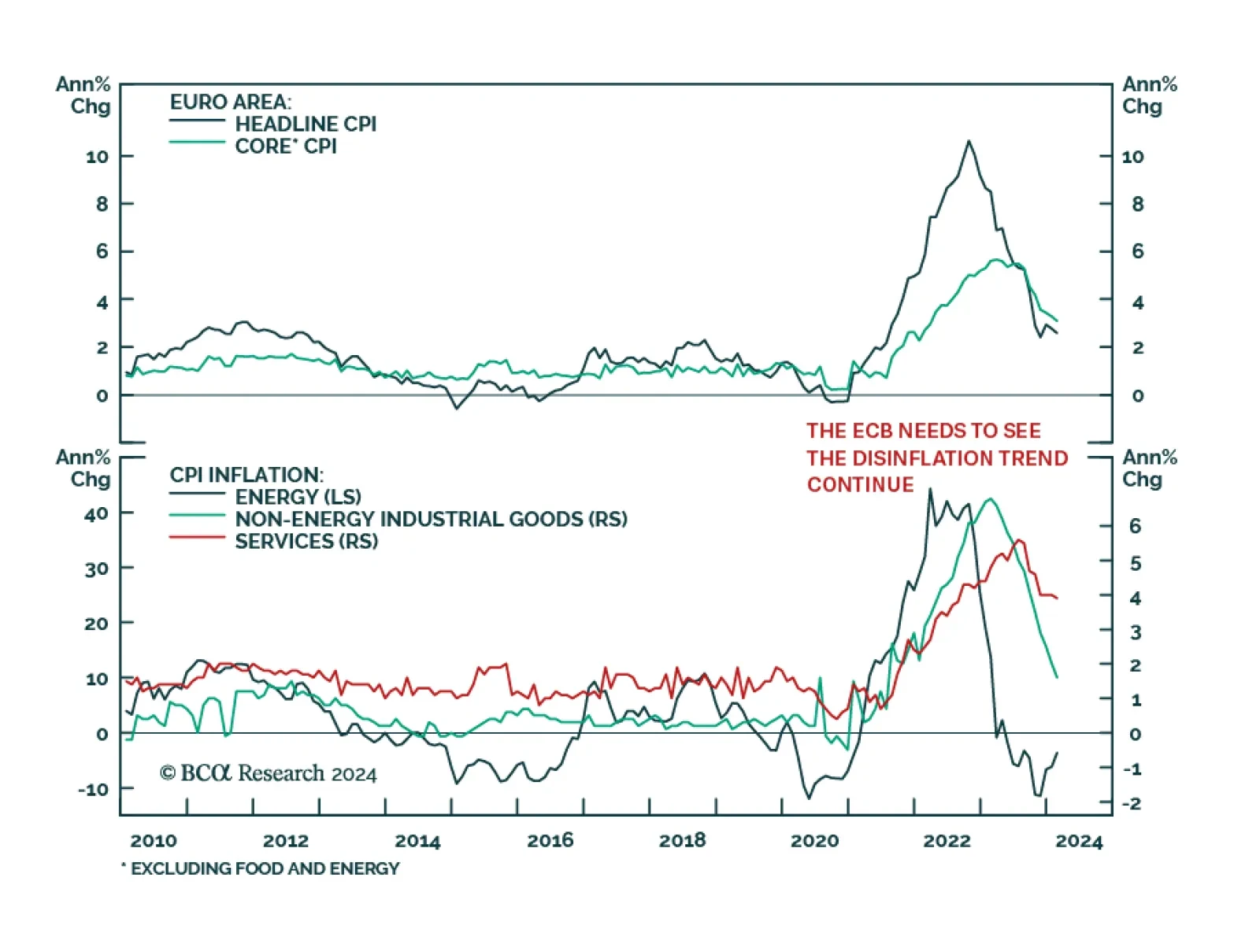

The preliminary Eurozone inflation release suggests that price pressures eased by less than anticipated in February. Headline CPI inflation slowed from 2.8% y/y to 2.6% y/y (slightly above expectations of 2.5% y/y. Similarly, although the core inflation gauge…

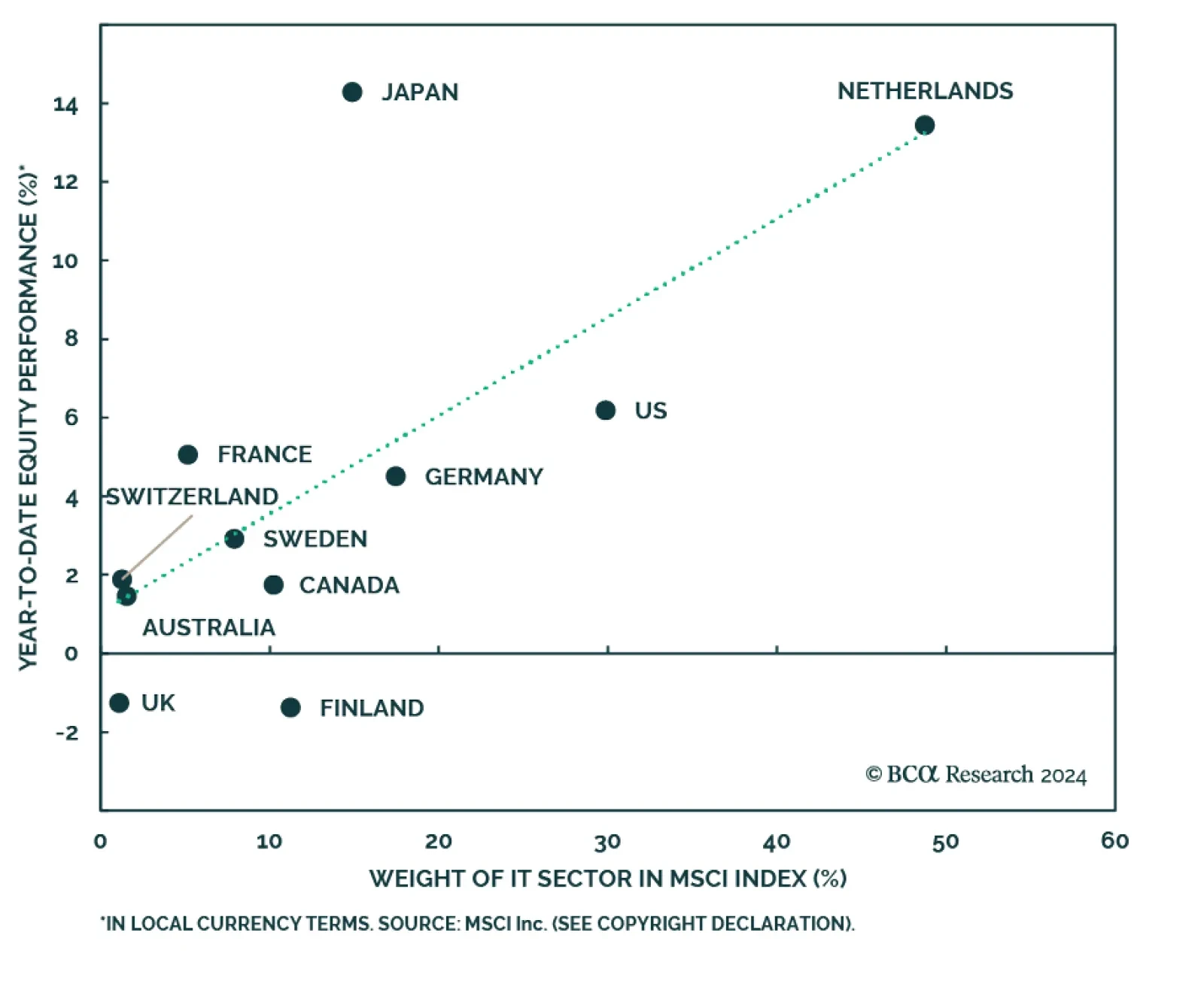

As we highlighted in a previous Insight, the breadth of the US equity rally has been relatively narrow, led by extremely strong gains among Big Tech stocks. Tech is still the best performing sector, with the S&P IT price index up 12% year-to-date on top…

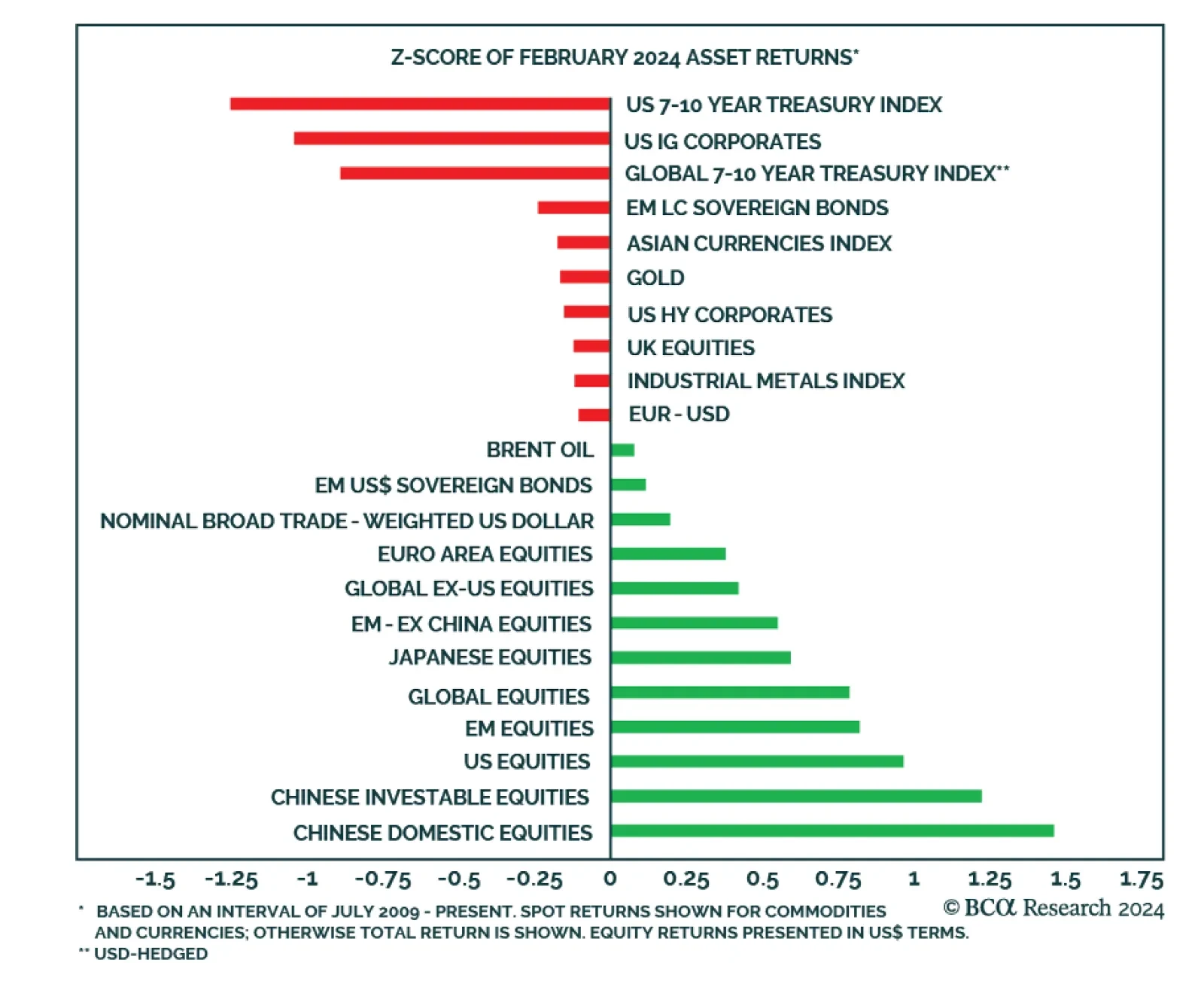

The global equity rally – which fizzled at the start of the year – picked up steam again in February with nearly all major regions posting above average returns. After having underperformed last year, Chinese stocks led their global counterparts in terms of…

According to BCA Research’s Geopolitical Strategy and The Bank Credit Analyst services, trade policy under a second Trump presidency represents the greatest cyclical risk to investors. In 2018, the Trump administration’s trade war with China and several…

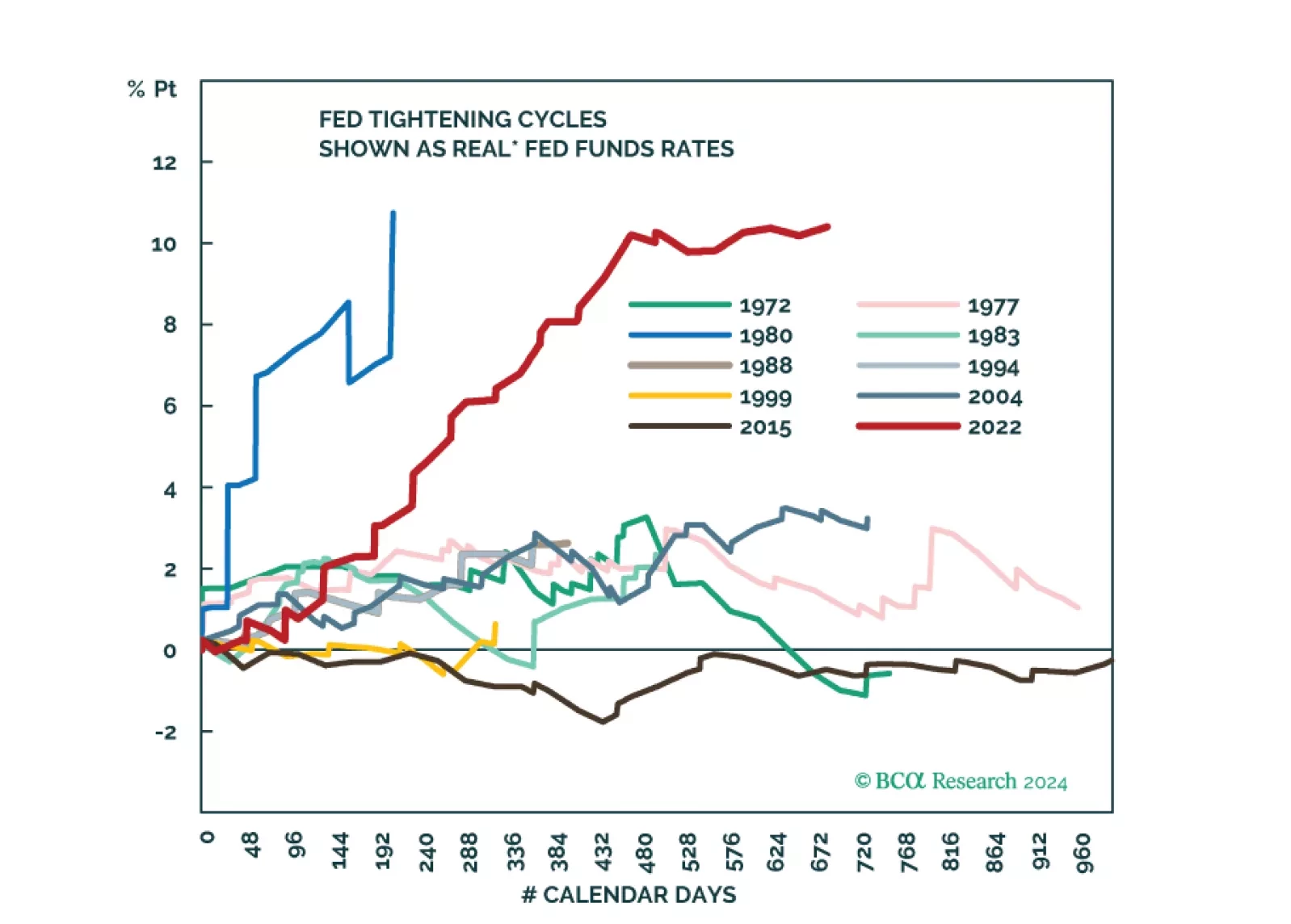

Amid patchy global growth, the US economy remains resilient. However, tight monetary policy will eventually trigger a recession in the US too. The stock market rally has been very narrow. Stay underweight risk assets.

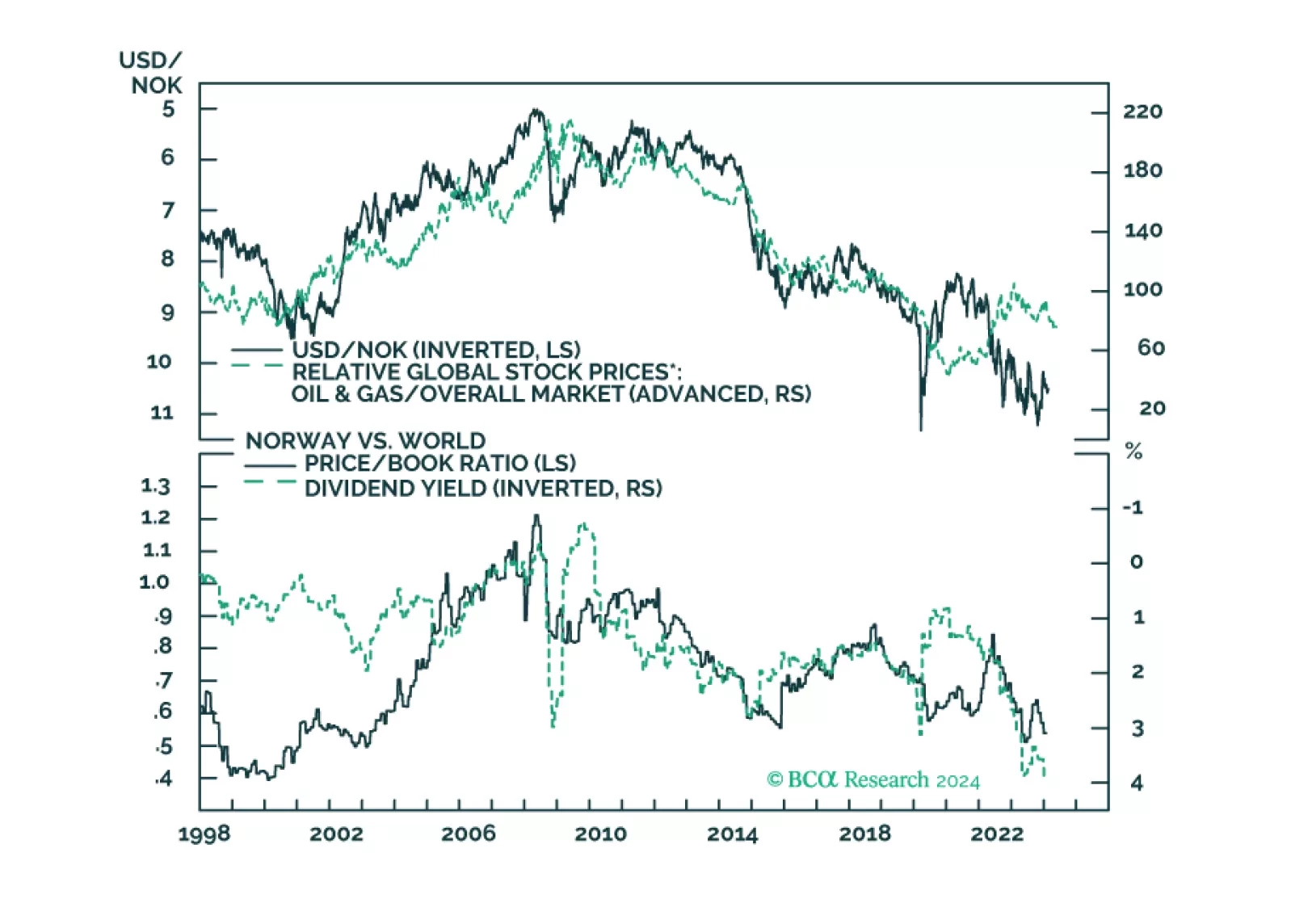

In this insight, we provide an update on the Norwegian krone, with attractive trade ideas over a long-term horizon. Shorter-term, our neutral-to-positive view on the dollar keeps us on the sidelines for USD/NOK.

Despite the economy being on the verge of a recession, the South African Reserve Bank will not ease policy meaningfully. Doing so will accentuate the currency depreciation, which, in turn, will push up bond yields – an outcome the central bank would like to prevent.

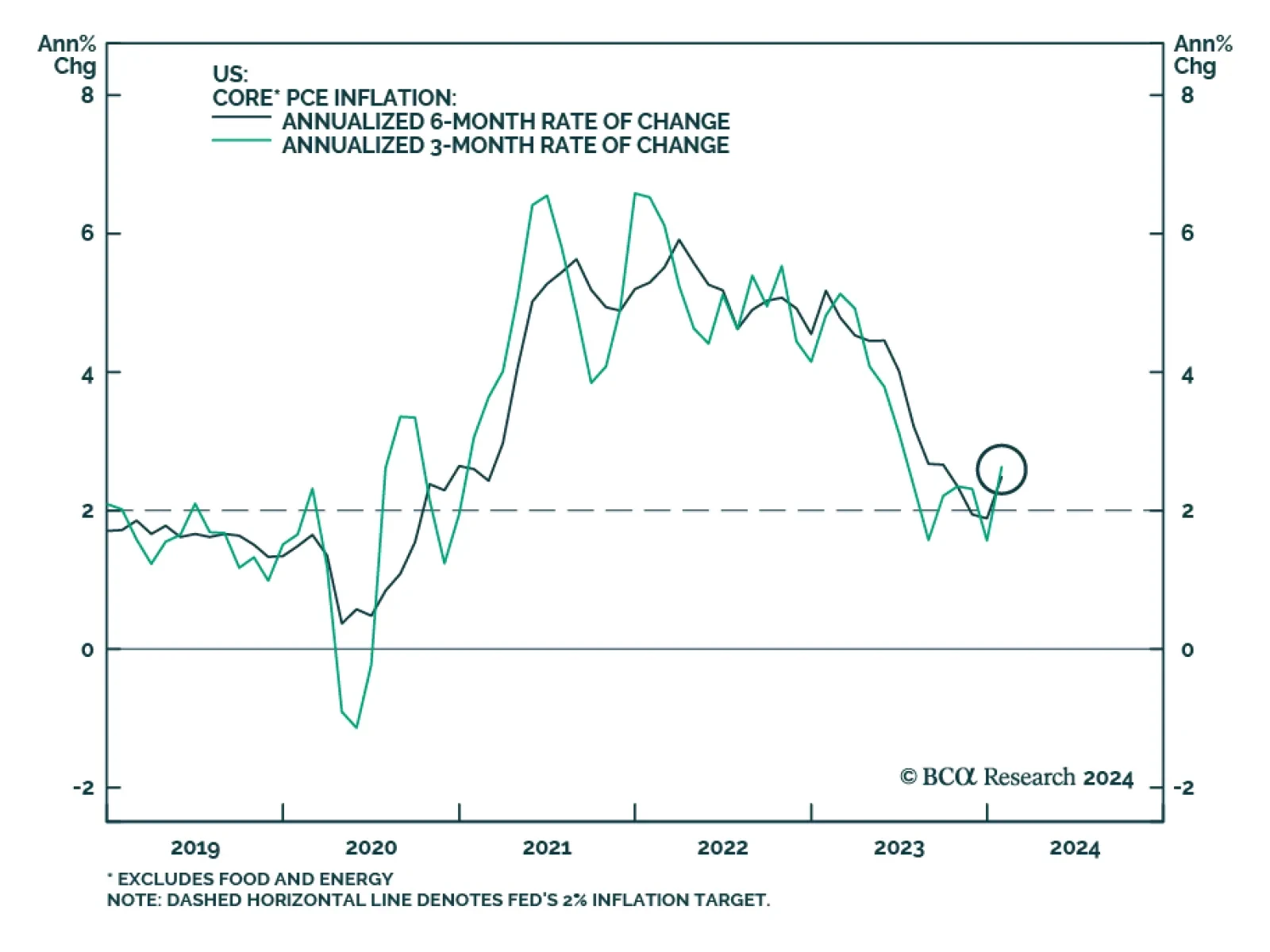

Aside from the 1.0% m/m jump in personal income – which beat expectations of a 0.4% m/m rise – the US January Personal Income and Outlays report was broadly in line with consensus estimates. Nominal personal spending growth decelerated from 0.7% m/m to 0.2%…

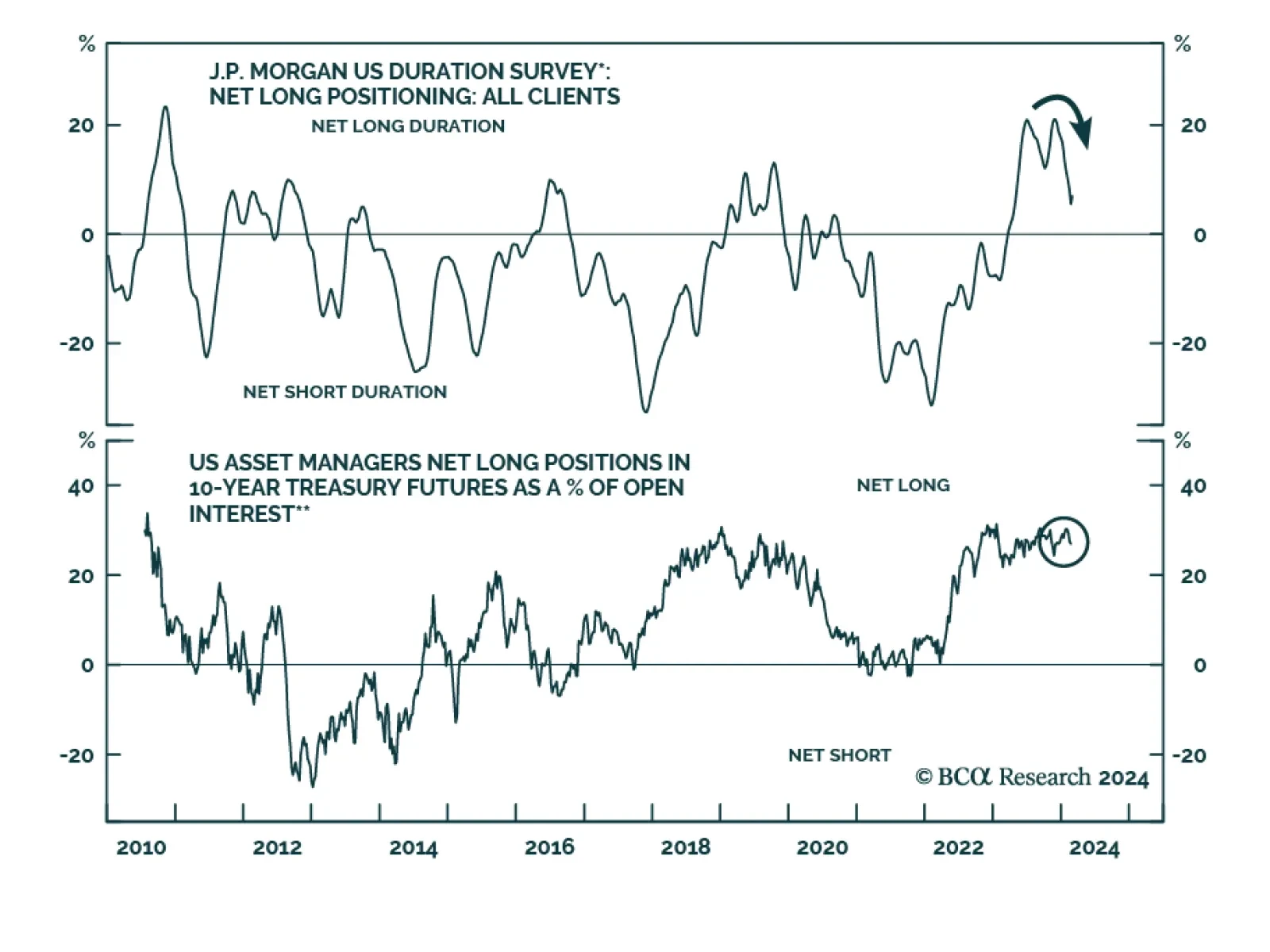

In a recent report, our US Bond strategists argued that while the year-to-date increase in yields has made Treasures more attractive, conditions are not yet in place to extend duration. Instead, they expect that there will be a better opportunity later this…