Economy

In Section II, Jonathan shows how valuation-adjusted fundamental momentum has been a successful tool for ranking global sectors.

In Section I, Doug highlights that benchmark positioning in equities, fixed income and cash is now recommended. Still, the US macro situation warrants continual monitoring, given weakening labor market momentum. In Section II, Jonathan shows how valuation-adjusted fundamental momentum has been a successful tool for ranking global sectors.

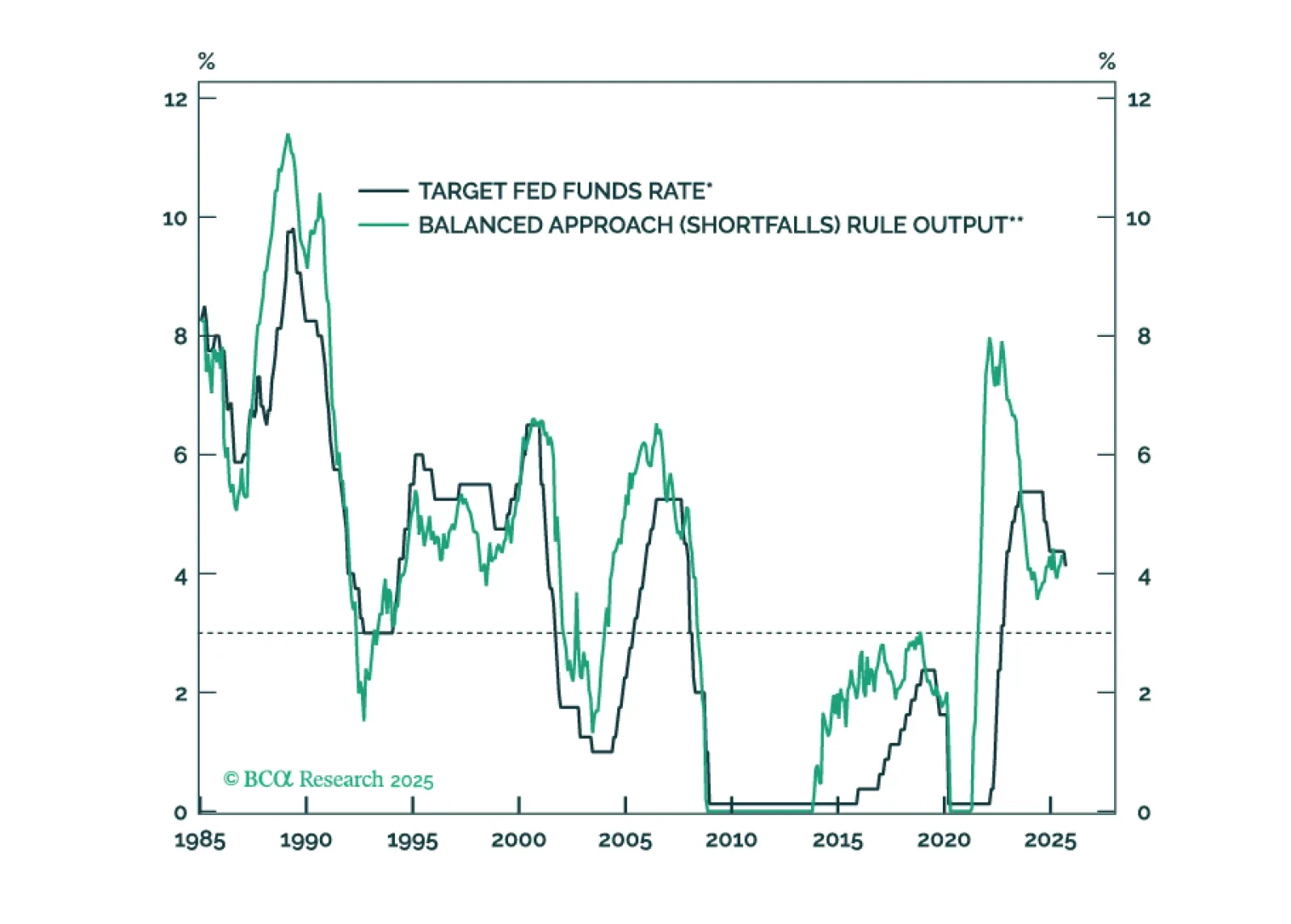

This week’s US Bond Strategy Special Report takes a look at the two most provocative papers presented at last month’s Jackson Hole conference.

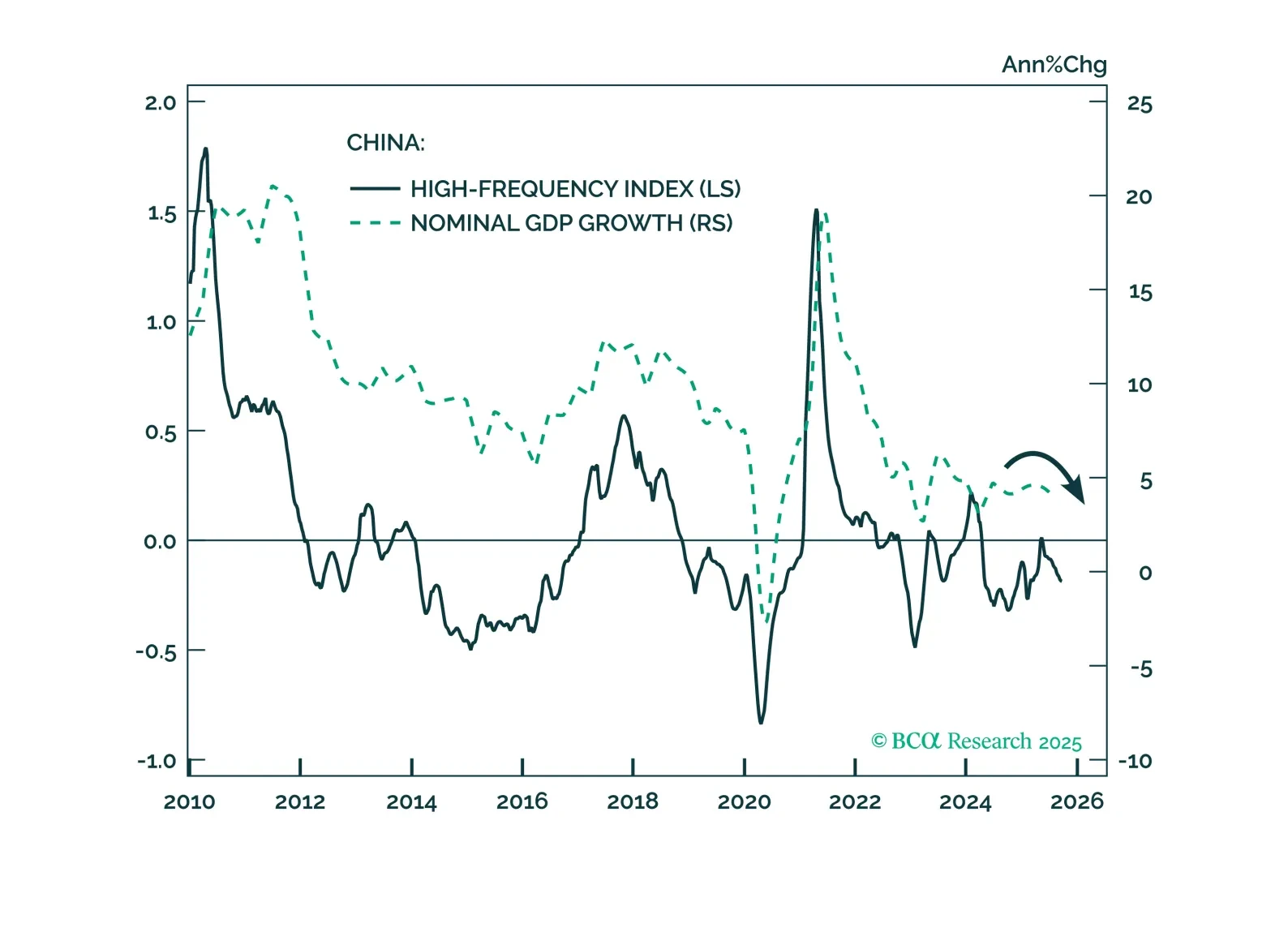

Our high-frequency indicators show China’s growth momentum weakening further in September, increasing the likelihood of new stimulus in the weeks ahead. We remain tactically cautious on Chinese equities, but strategically constructive on offshore Chinese shares.