Economy

The undercurrents of global financial markets signal deteriorating global growth conditions. There is little cash on the sidelines in the US, the Euro Area, and Japan. If the budding bear market resembles the 2000-2003 one, EM stock prices are unlikely to outperform global equities in the initial leg but could outperform in the latter stage of the global selloff.

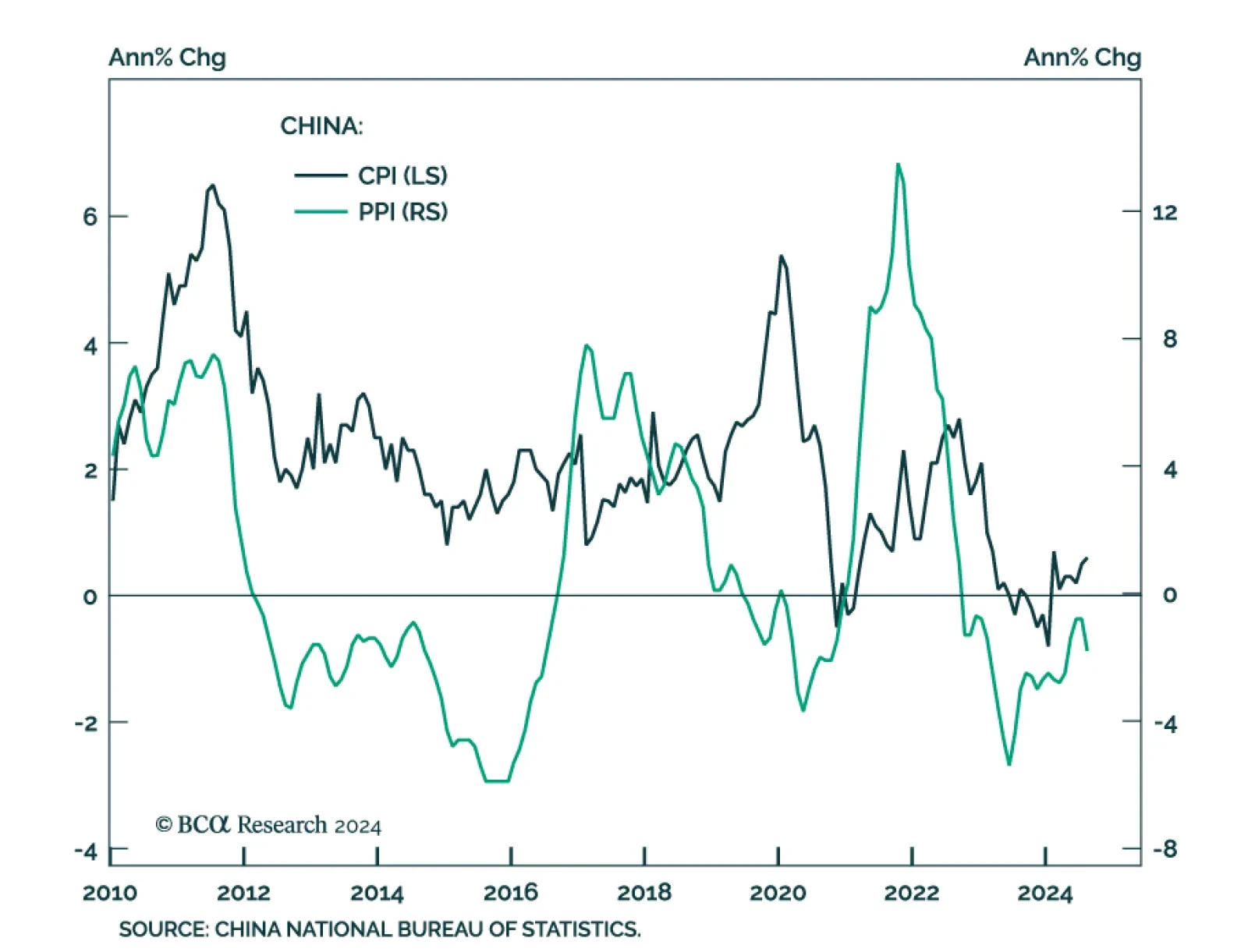

China’s CPI and PPI both surprised to the downside in August. Consumer prices grew from 0.5% y/y to 0.6%, below the 0.7% anticipated. However, a 2.8% y/y surge in food prices (the fastest pace so far this year) overstates this headline figure. Core CPI…

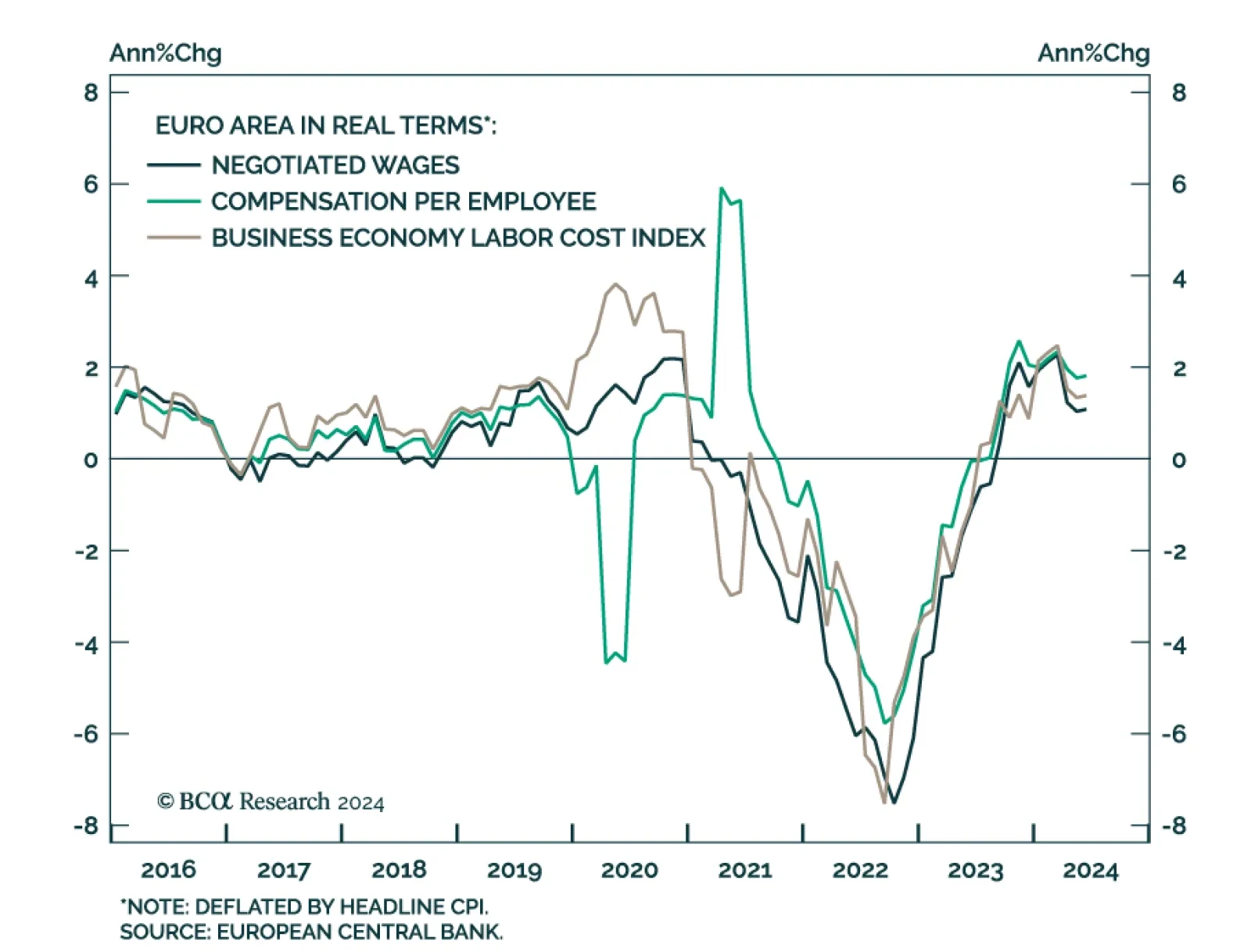

Eurozone GDP’s final estimate indicates that growth was slower than expected in Q2. Output grew 0.2% q/q in Q2, compared to 0.3% previously reported. A significant downward revision to capex (2.2% contraction against 1.8% previously estimated) drove the…

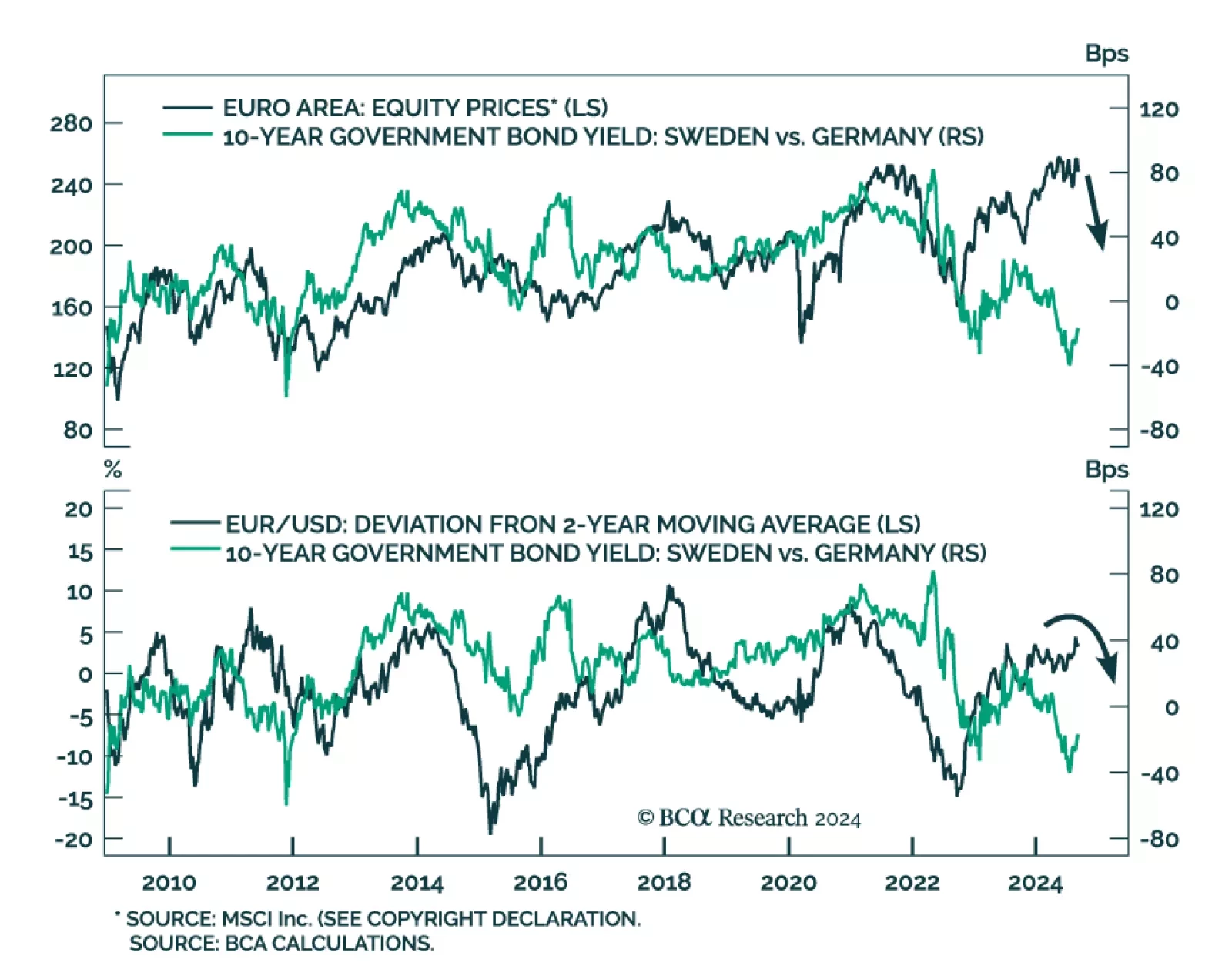

The Swedish economy’s cyclicality and sensitivity to global trade make it a reliable bellwether for global growth. Sweden is facing significant domestic weakness. Employment growth declined by 0.14% y/y in July and households’ debt burden stands at 155% of…

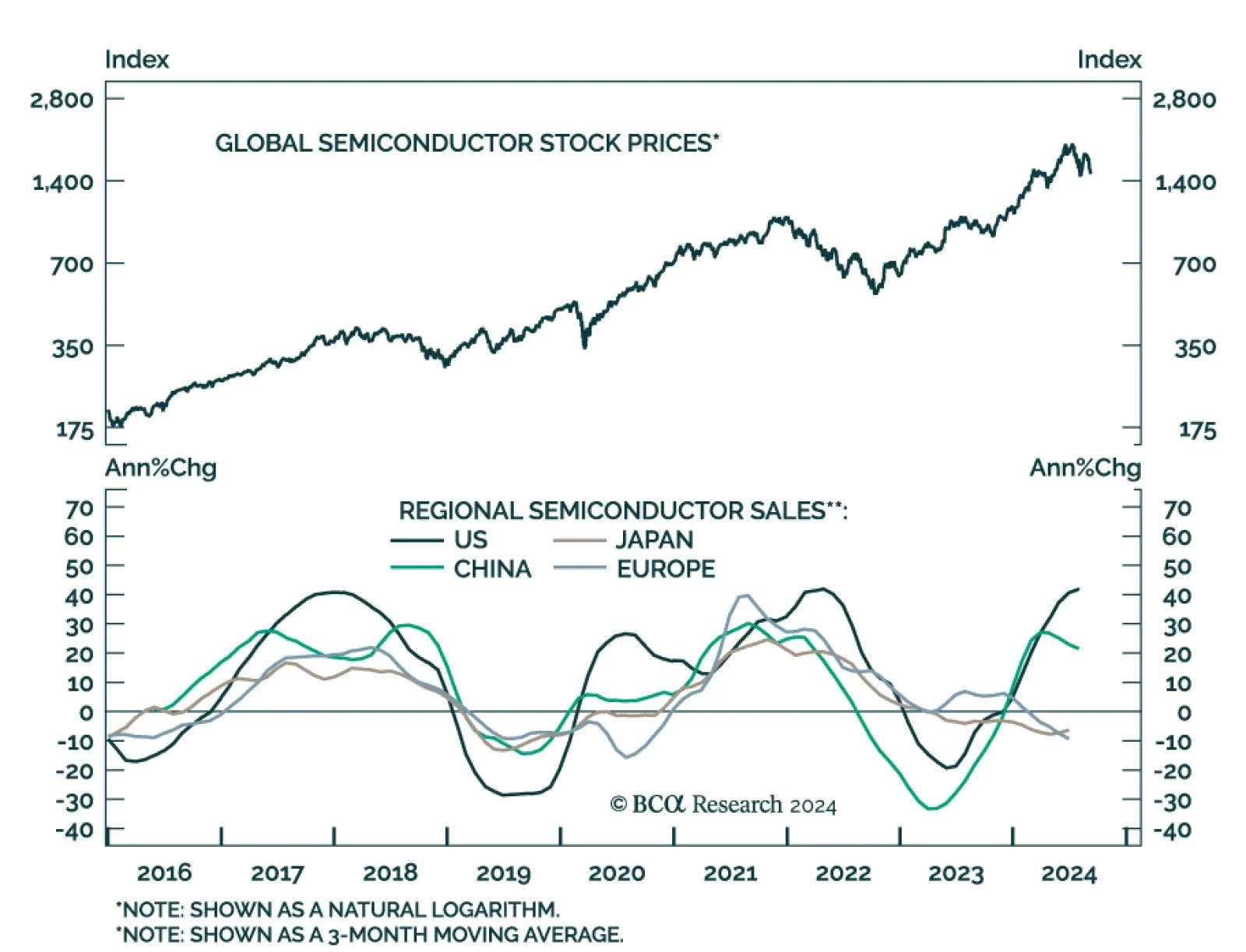

Global semiconductor stocks have returned 50% YTD in USD terms, and a whopping 200% since their September 2022 lows. However, they may have peaked back in July. Our Emerging Market strategists highlight a significant bifurcation between the revenues of…

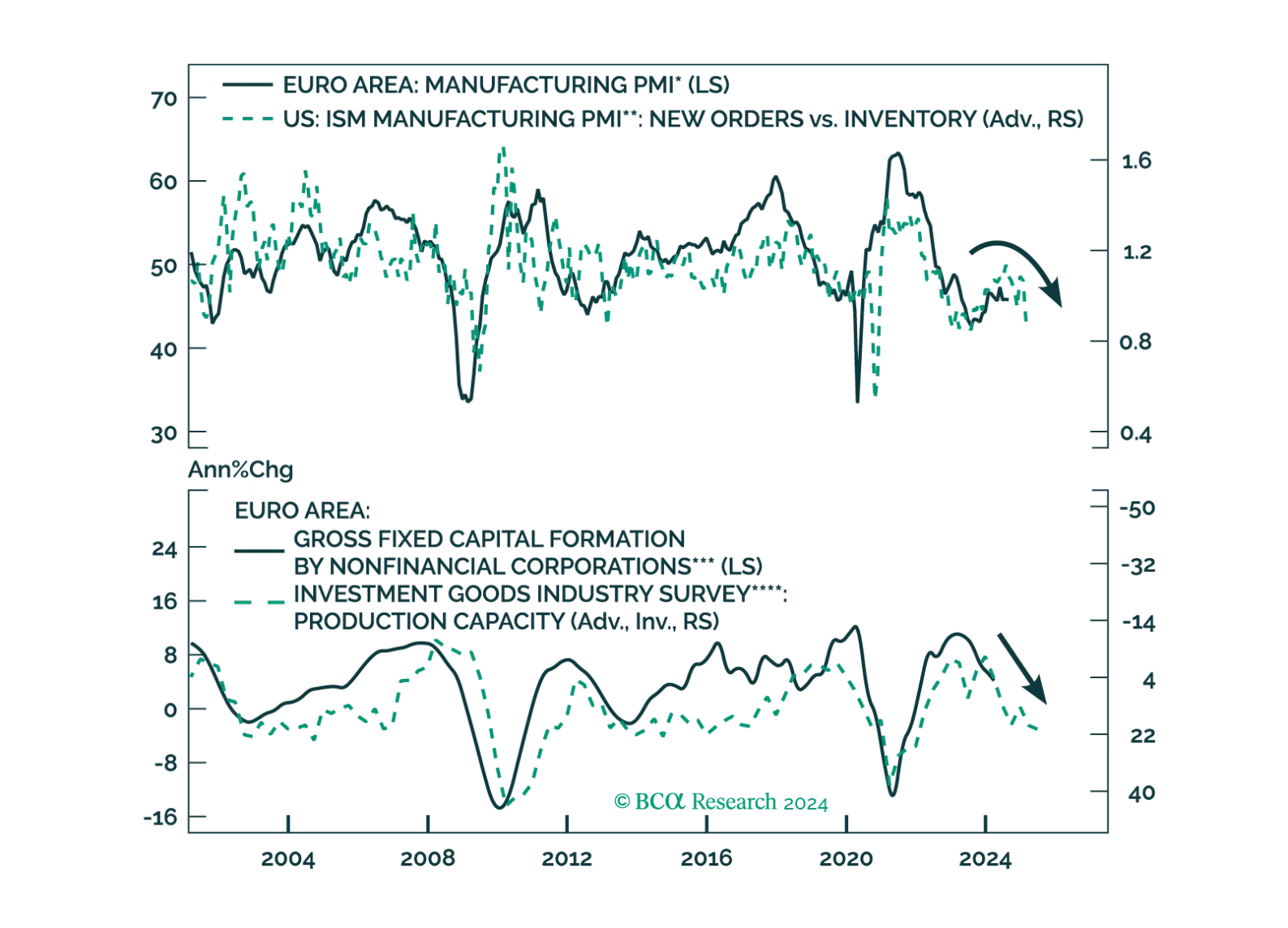

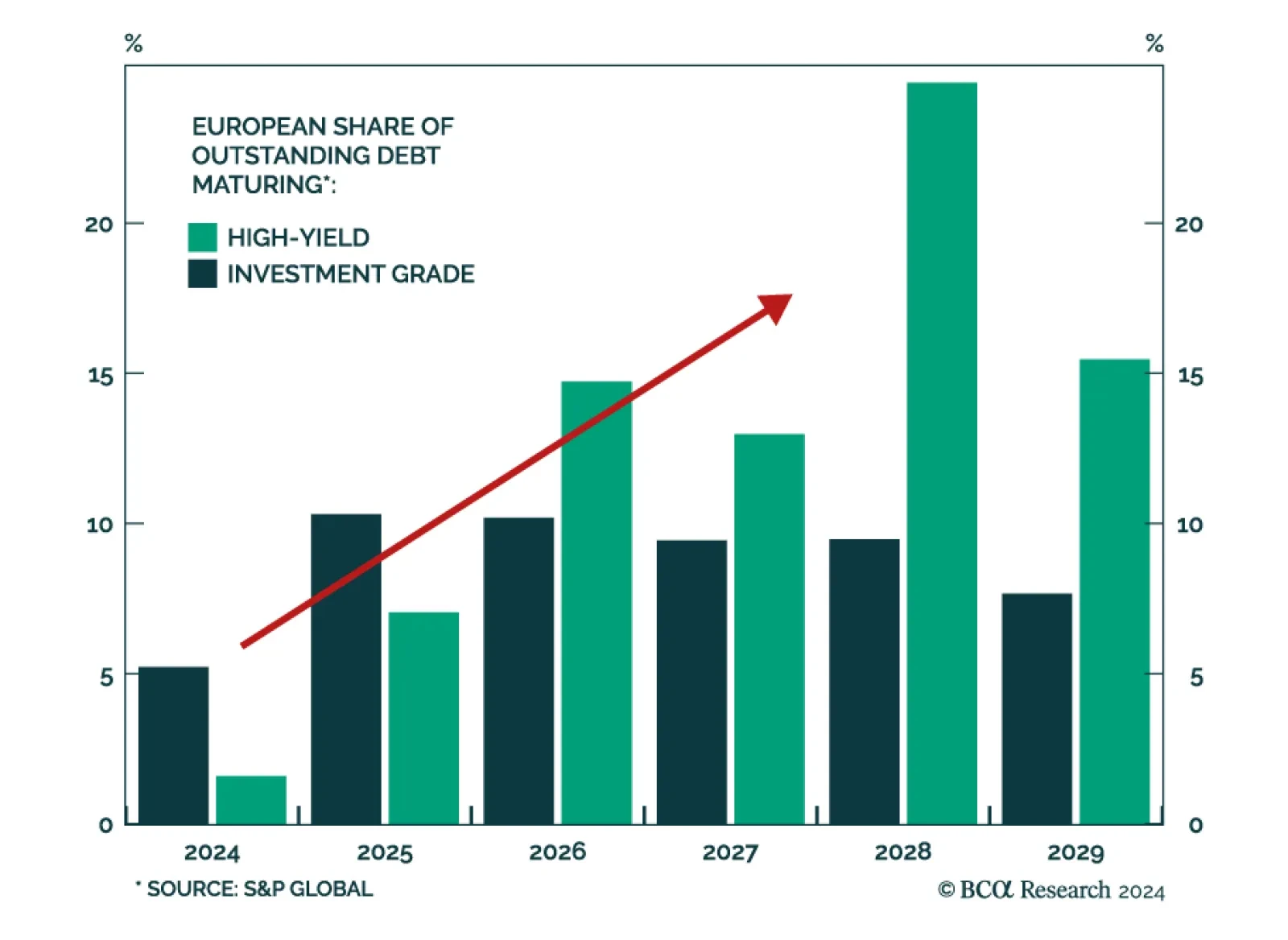

Crucial leading indicators of the global and European economies continue to deteriorate. How should investors position their European portfolios to benefit from these trends?

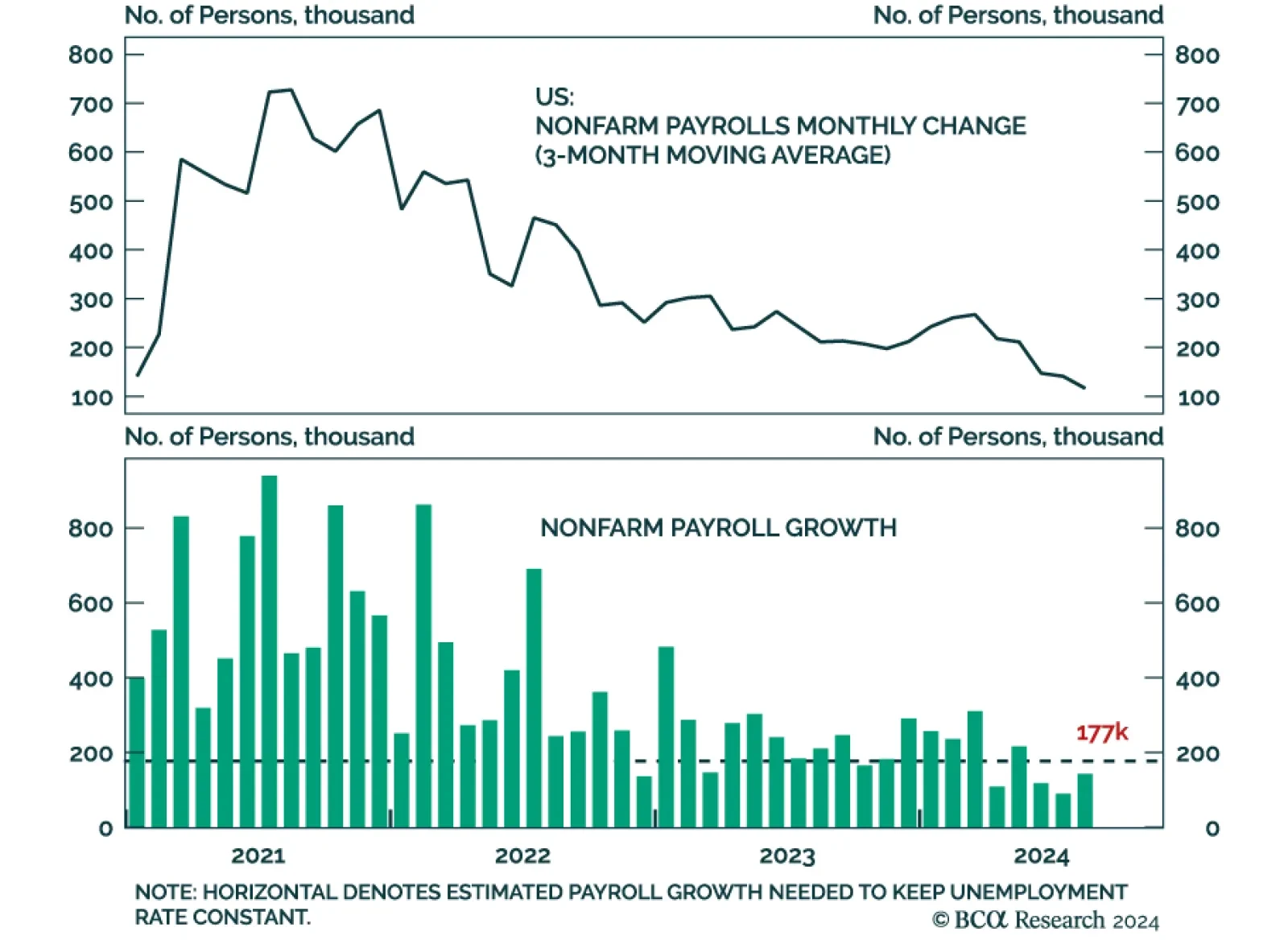

August nonfarm payrolls expanded by 142 thousand workers, from a downwardly revised 89 thousand and below expectations of 165 thousand. Payroll growth fell to a four-year-low of 116 thousand on a 3-month moving average basis. Notably, pro-cyclical…

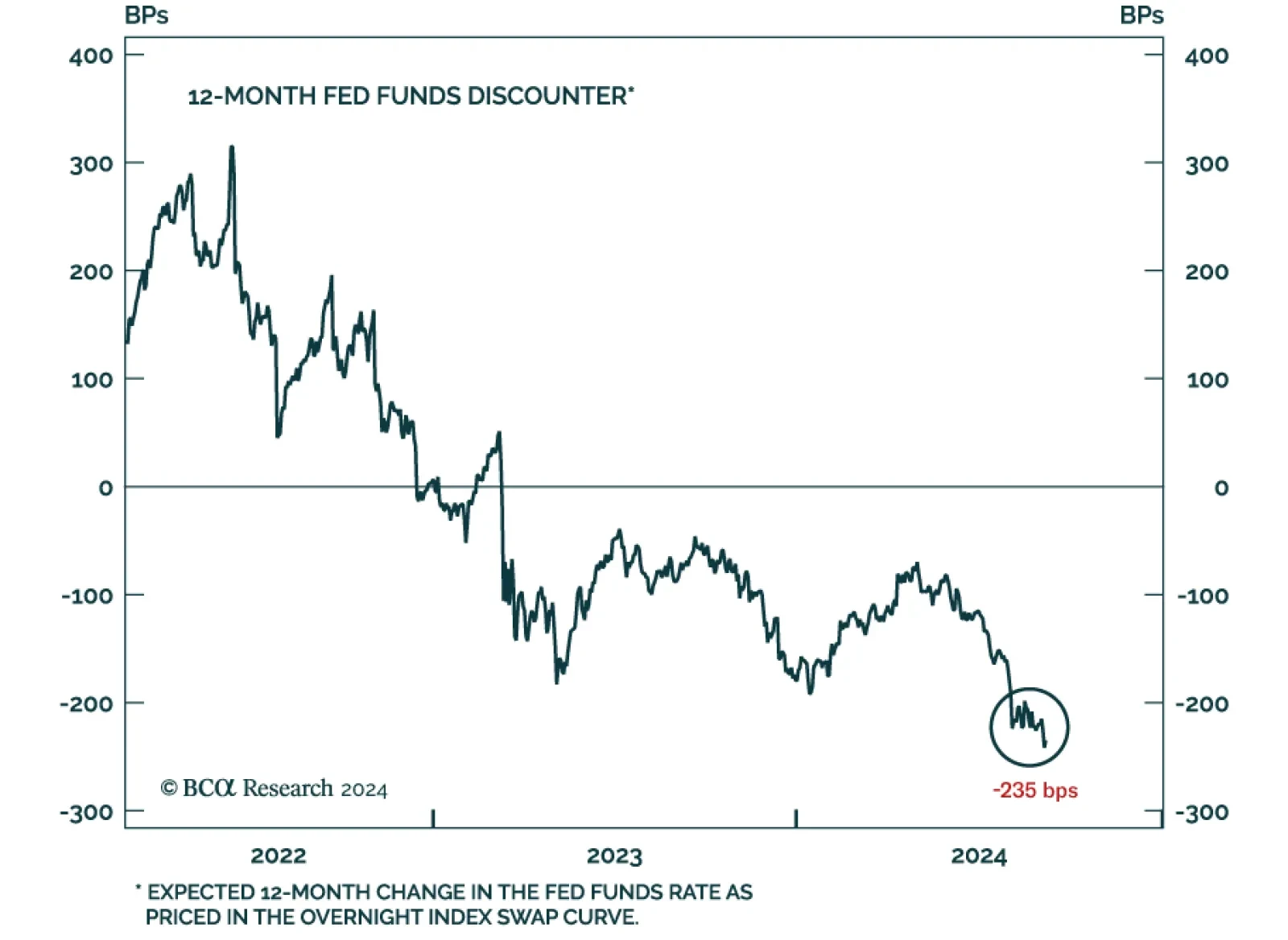

The July Employment Situation report had already cemented the case for a September rate cut and Chairman Powell’s Jackson Hole comments dispelled any remaining doubt about an imminent monetary easing cycle. All the labor market data released since then…

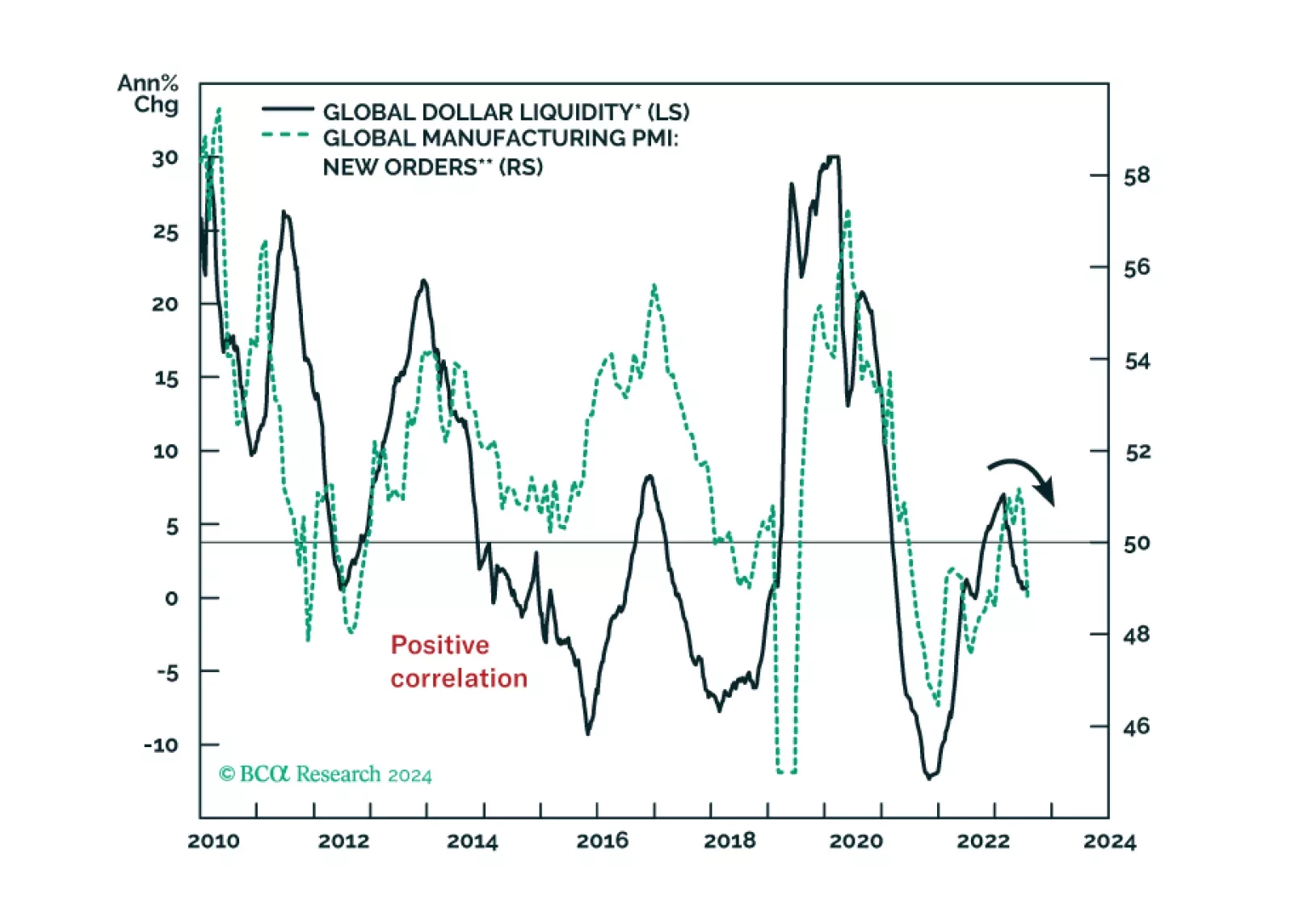

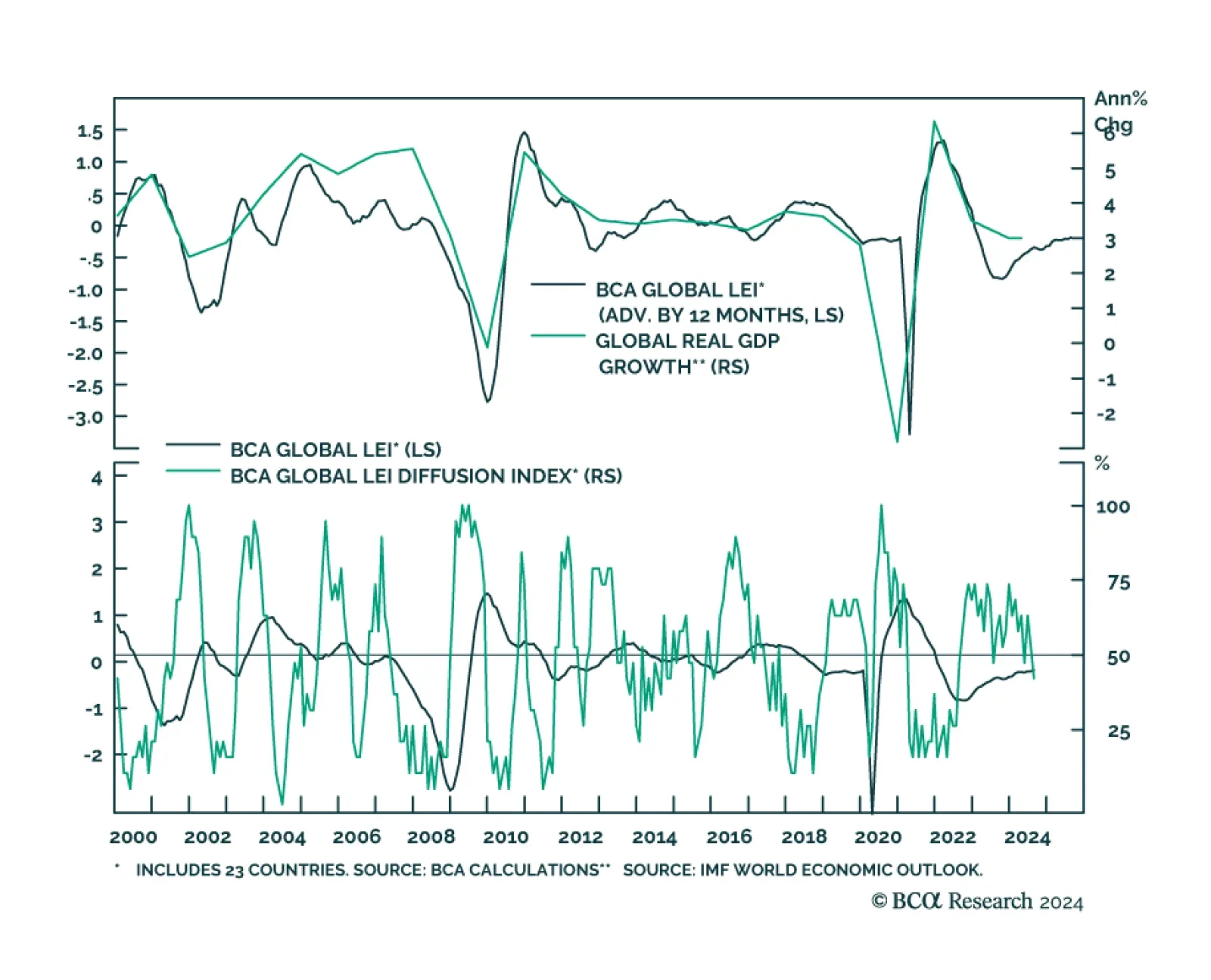

BCA’s Global Leading Economic Indicator, a GDP-weighted average of the standardized leading indicators of 23 DM and EM economies, has had a good track record of predicting year-on-year changes in the IMF global real GDP growth series. The Global LEI has…

The pro-cyclical Eurozone economy is highly exposed to a global downturn, which we expect will materialize by early 2025. The ECB is behind the curve and we thus expect it to ease more aggressively than markets expect next year. A dovish surprise in 2025…