Economic Growth

The S&P 500 reached our 4,500 mid-year target last week, but the bears have yet to capitulate and stocks could melt up so we are placing a trailing stop on our tactical overweight instead of downgrading equities outright.

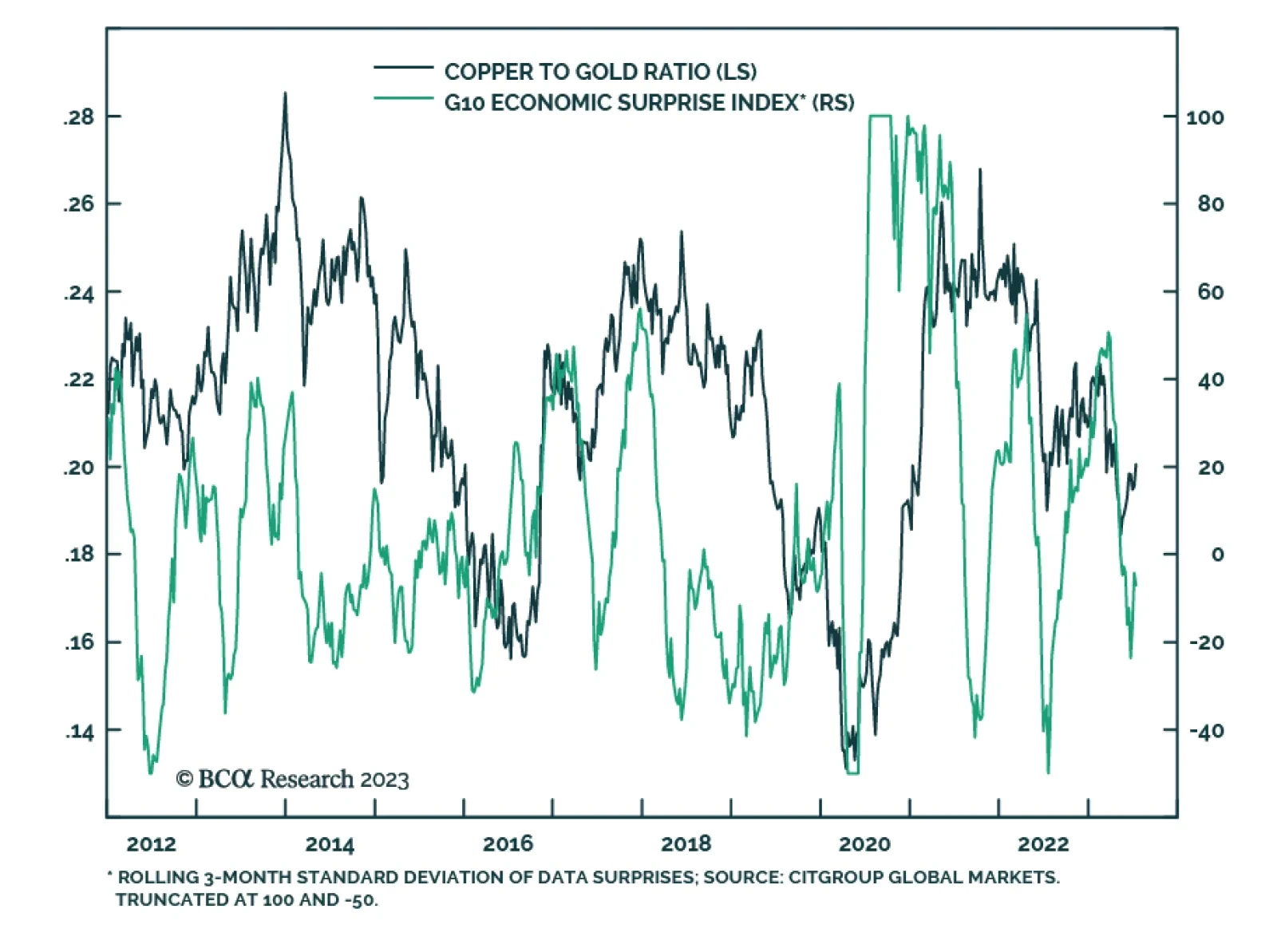

In recent months, the European and US economies have greatly diverged, with the Euro Area massively disappointing while the US has surprised to the upside. Can this dichotomy continue or is it Europe’s turn to shine?

In this report, we explore Brazil’s inflation and monetary policy outlook, the Lula administration’s back-and-forth between pragmatism and populism, and how these factors will affect Brazilian financial markets going forward. All in all, we believe Brazilian risk assets will be in a trading range relative to their EM peers in the next 12 months.

Falling inflation enables central banks to pause rate hikes, which is good news. But time goes on. Restrictive monetary policy, Chinese debt-deflation, energy supply shocks, US and global policy uncertainty, and extreme geopolitical risks will undermine hopes of a soft landing and beautiful disinflation.