Economic Growth

A global portfolio is likely to return only 5.3% a year over the next decade, compared to 6.7% in the past. Investors either need to lower their return expectations, or take more risk. Our total return methodology remains consistent with previous editions, with changes limited to the Alternatives section.

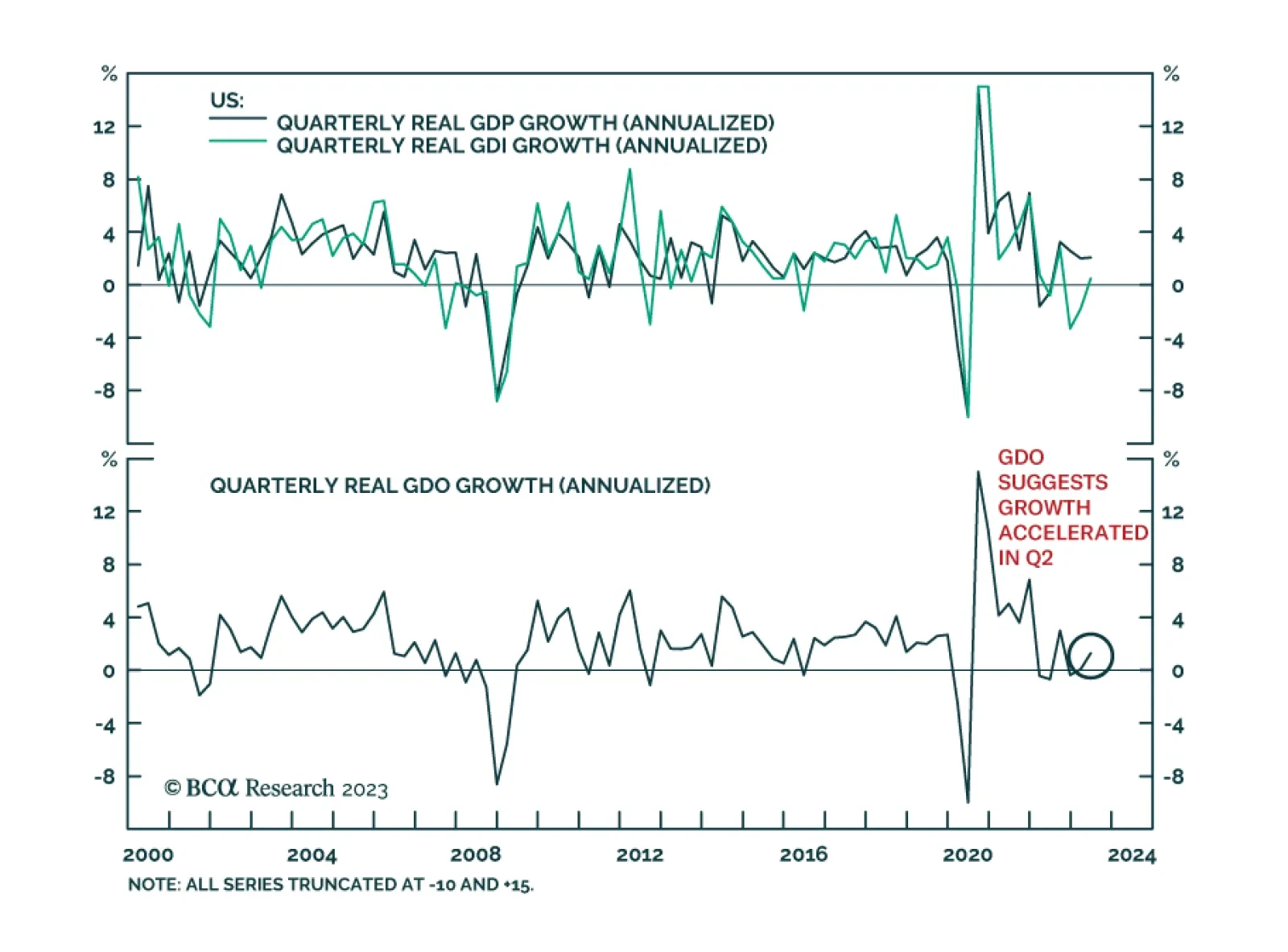

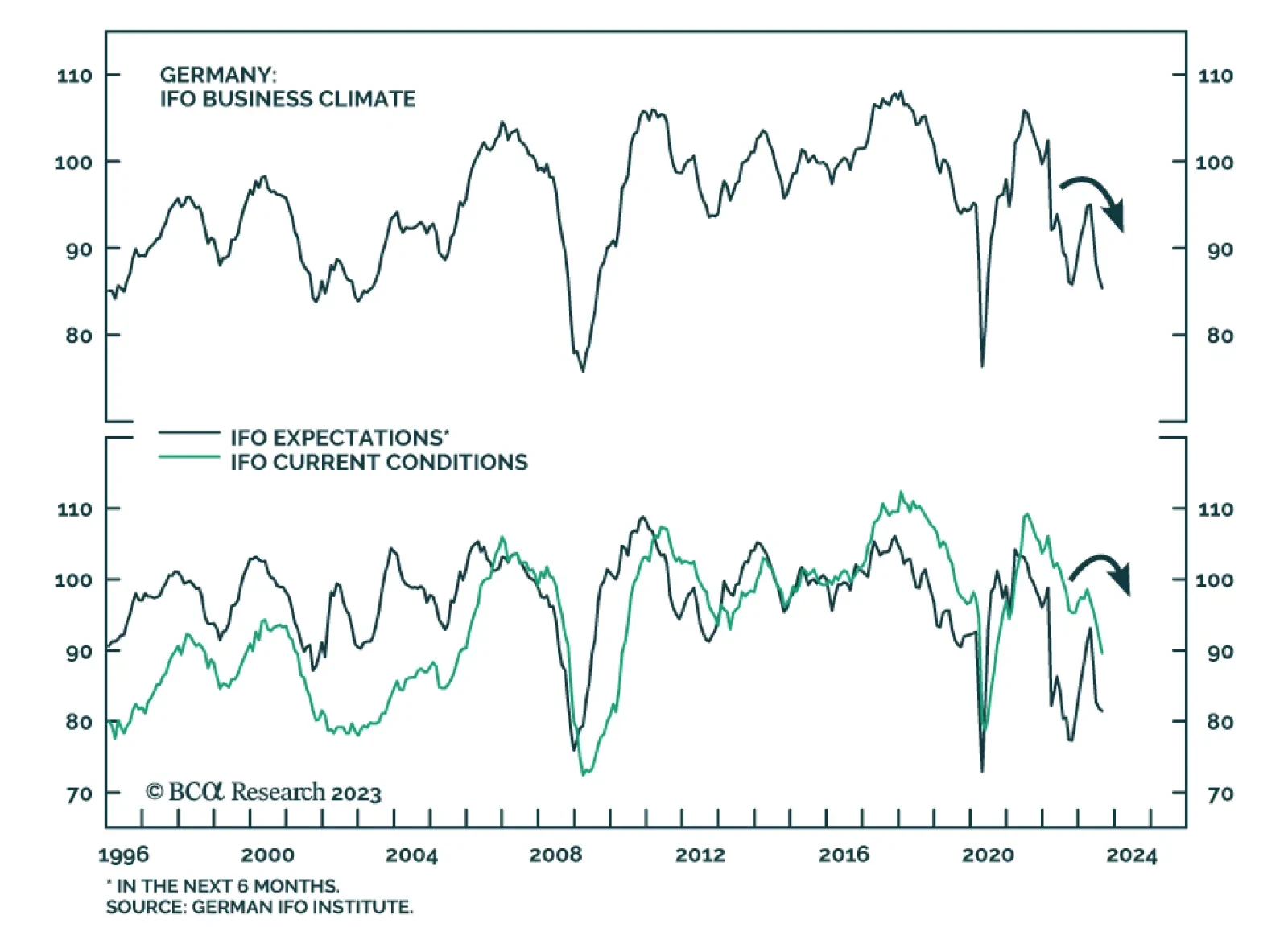

Today’s Strategy Report chartbook presents the data underpinning our view that both inflation and growth are slowing, likely pointing to a recession beginning sometime in the first half of next year. We are tactically equal weight across asset classes after being stopped out of our equity overweight on August 17th and expect our next move will be to underweight equities and overweight fixed income, in line with our twelve-month view.

China removed checks and balances in its political system to deal with a very dangerous economic transition. The transition is going badly, yet investors cannot rely on checks and balances to correct or prevent policy mistakes. The Taiwanese election is a looming bellwether.

In this report, we review our FX trade recommendations with suggestions on how to position for the next few months.

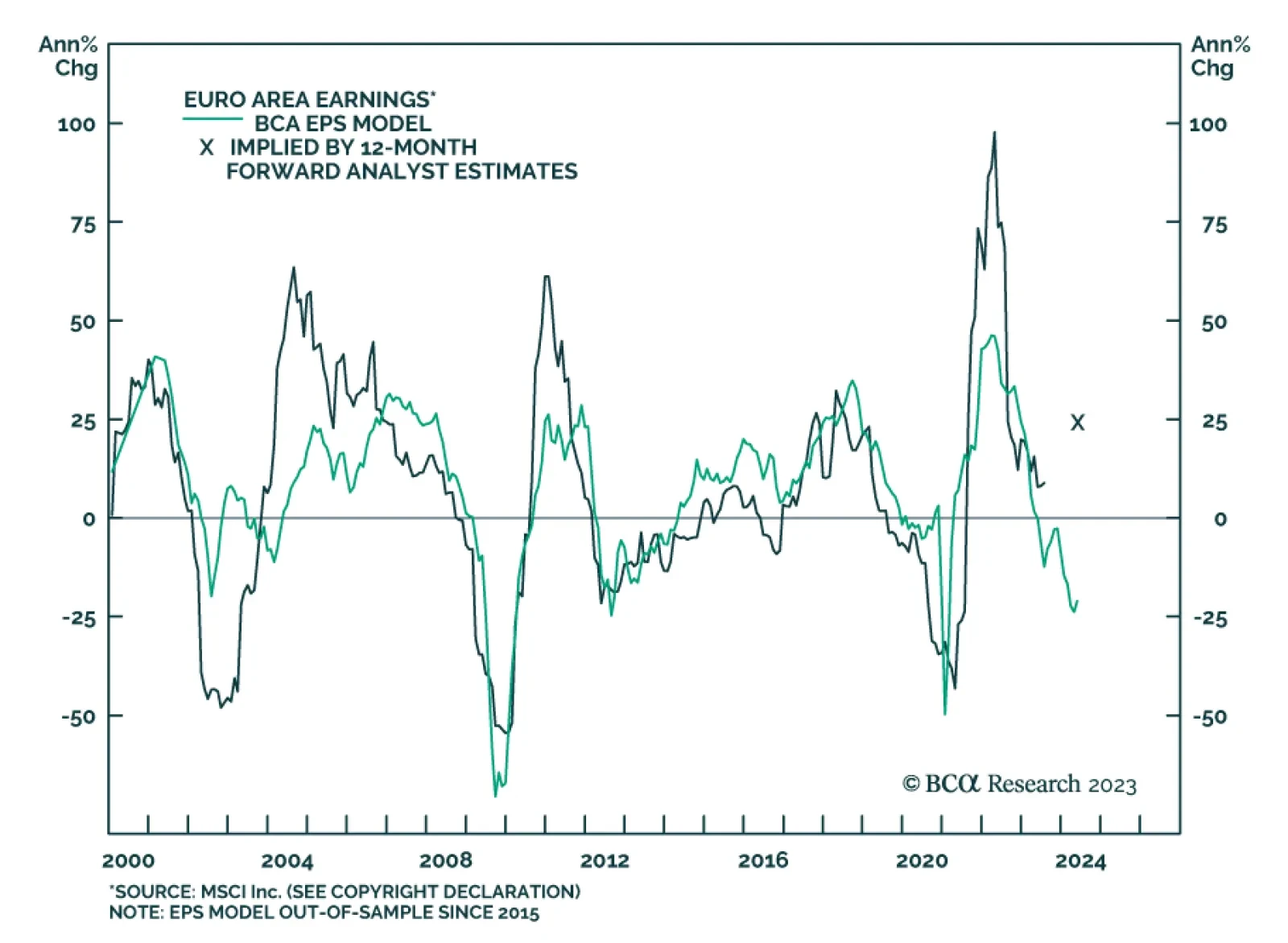

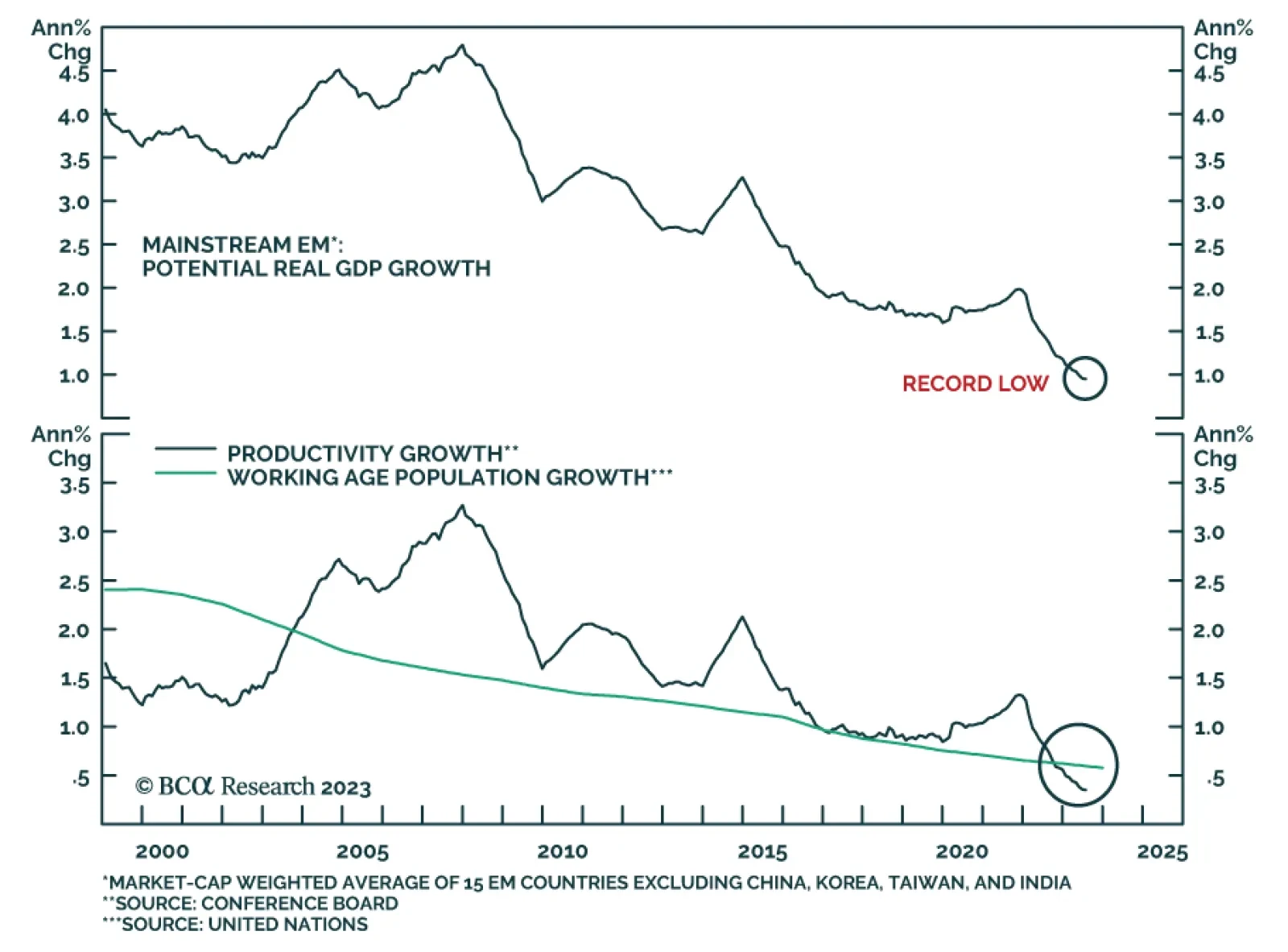

In part 2 of this series, we discuss mainstream EM equity valuations and present the results of our cross-country analysis. The goal is to identify overweights and underweights within an EM equity portfolio.