Economic Growth

Executive Summary Italy’s right-wing alliance, led by Brothers of Italy, will likely outperform in the upcoming election. The new government will prioritize the economy, posing a risk to the EU’s united front against Russia. It is conducive to an eventual ceasefire, which is marginally positive for risk assets in 2023. We recommend investors underweight Italian assets on a tactical basis. China’s political risks will remain elevated until Xi consolidates power this fall, positive news will come after, if at all. Geopolitical risk in the Taiwan Strait will remain high and persistent until China and the US reach a new understanding. Separately, we are booking a 9% gain on our long US equities relative to UAE equities trade. Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Tactical Recommendation Inception Date Return LONG US / UAE EQUITIES (CLOSED) 2022-03-11 9.0% Bottom Line: Italy’s political turmoil suggests a more pragmatic policy toward Russia going forward. Europe’s energy cutoff will also motivate governments to negotiate with Russia. Feature In this report we update our GeoRisk Indicators, with a special focus on Italy’s newest political turmoil. Italy Over the past several months, we have argued that Italy was a source of political risk within the European Union and that the market underestimated the probability of an early Italian election. In the past two weeks, this forecast has become a reality (Chart 1). Chart 1Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

The grand coalition under Prime Minister Mario Draghi had fulfilled its two main purposes – to distribute EU recovery funds and secure an establishment politician in the Italian presidency. At the same time, headline inflation hit 8.5% in June, the highest since 1986, even as the Italian and global economy slowed down, Italian government bonds sold off, and Russia induced an energy crisis. The stagflationary economic environment is biting hard and the different coalition members are looking to their individual interests ahead of election season. On July 14, Giuseppe Conte, the former prime minister, pulled its populist Five Star Movement (M5S) out of Mario Draghi’s national unity government, triggering a new round of political turmoil in Italy. Draghi’s first resignation was rejected by Italian President Mattarella later that day. However, on July 21, the League and Forza Italia also defected from the grand coalition. After Draghi’s plan of reviving the coalition collapsed, President Mattarella accepted his resignation and called for a snap election to be held on September 25, ten months ahead of the original schedule. Based on the latest public opinion polls, right-wing political parties are well-positioned for the upcoming election. The far-right Brothers of Italy is now the front runner in the election race and is expected to win around 23% of the votes. Another far-right party, the League, is the third most popular party, with nearly 15% support despite a drop in support during its time within the grand coalition. In addition, the center-right Forza Italia receives 8.5% of the support. Together, the right-wing conservative bloc amounts to 46.5% of voting intentions. There is still positive momentum for Brothers of Italy to harvest more support given that they are the flag-bearer for anti-incumbent sentiment amid the stagflationary economy. By contrast, the left-wing parties – the Democrats, the Left, and the Greens – only command about 27%. The possibility of an extended left-wing coalition, even with the inclusion of the M5S, is looking slim. On July 25, Enrico Letta, the leader of the Democratic Party, publicly expressed his anger against party leader Giuseppe Conte and ruled out any electoral pact with the M5S because of the recent political chaos they caused. He stressed that the Democratic Party would seek ties with parties that had remained loyal to Draghi’s national unity. However, there are not many parties left for the Democrats to partner with. Apart from the Left and the Greens, the Democrats’ best chance would be the center-left Action Party and Italia Viva, which is led by Matteo Renzi, who served as the secretary of the Democratic Party from 2013 to 2018. However, these four parties are small and will not enable the Democrats to form a government. Courting M5S is the Democrats’ only chance to set up an alternative to the right-wing bloc, but that will require the election to force the two parties together. Related Report Geopolitical StrategyLe Pen And Other Hurdles (GeoRisk Update) The Democratic Party was the biggest supporter of Draghi’s government, while the Brothers of Italy were the sole major opposition. Thus the September 25 election will be a race between these two major parties. Both are expected to outperform current polling, as they will attract the most supporters from each side. The other right-wing parties, Forza Italia and the League, will at least perform in line with their polling, while the other left-wing parties will underperform. In the meantime, M5S’ popularity will continue to decline – the party is bruised over its role in Draghi’s coalition and divided over how to respond to the Ukraine war. Foreign policy is a major factor in this election. Italy has the highest share of citizens in the Eurozone who support solving the Russia-Ukraine conflict through peaceful dialogue (52% versus the Eurozone average of 35%). Italy has long maintained pragmatic relations with Russia, including the Putin administration, as it imported 40% of its natural gas from there prior to 2022. The EU is struggling to maintain a united front against Russia, and war policy will be a key focal point among the different parties. Draghi and the Democratic Party are the strongest supporters of the EU’s oil embargo on Russia and decision to send arms to support Ukraine. On the other side, the right-wing Forza Italia and the League have been more equivocal due to their traditional friendship with Russia. What’s more important is the stance of the Brothers of Italy on Russia, as it is the largest party now and will probably lead a right-wing government after the election. On July 27, the three right-wing parties struck a deal to officially form an alliance in the upcoming election and whichever party wins the most votes would determine the next prime minister if the alliance wins. This deal puts Giorgia Meloni, the leader of Brothers of Italy, one step closer to becoming Italy’s first female PM. Giorgia Meloni, unlike her right-wing peers, has endorsed Draghi’s hawkish stance towards Russia. Recently, she stressed that Italy would keep sending arms to Ukraine if her party forms a government after the election. However, Meloni’s speech could be a tactical move to win the election more than an unshakeable policy position. First, like the other two right-wing parties, the Brothers of Italy have had close connections with Russia. After the 2018 Russian presidential election, Meloni congratulated Putin and claimed his victory was “the unequivocal will of Russians.” In addition, she is close to Prime Minister Viktor Orban of Hungary and National Rally leader Marine Le Pen of France, both of whom have criticized the EU’s decision to provide military support to Kyiv. Hence her sharp change of stance this year seems calculated to avoid accusations of being pro-Russian. But that does not preclude a more pragmatic approach to Russia once in office. Second, Meloni has compromised other far-right positions to broaden her voter base. She has reversed the party’s original anti-EU stance and claimed it does not seek to leave the EU, as most European anti-establishment parties have had to do in order to make themselves electable. Being the only female in the election race, Meloni also pledged to protect women’s access to safe abortions in Italy, also a softer stance than before. Even if the Brothers of Italy distance themselves from some unpopular right-wing positions, including on Ukraine, they probably cannot form a government on their own. They will need to court Forza Italia and the League. These two parties prefer a more pragmatic approach to Russia and a peaceful resolution to the war. Thus while it will be hard to find a middle ground on the issue of Ukraine, the election will likely prevent Italy from taking a more confrontational stance toward Russia. It will probably do the opposite. Consider the context in which the next Italian government will operate. Russia declared on July 25 that it will further reduce natural gas supplies to Europe through Nord Stream 1, as we expected, bringing pipeline flows to 20% of its full capacity. Energy prices will go up even as European economic activity and industry will suffer greater strains. If Meloni is elected as the new prime minister this September, she will have to keep talking tough on Russia while simultaneously seeking a solution to soaring energy prices and economic crisis. This solution will be diplomacy – unless Russia seeks to expand its invasion all the way to Moldova. A right-wing victory is the most likely outcome based on opinion polling, the negative cyclical economy, and the underlying structural factors supporting populism in Italy that we have monitored for years. Such a coalition will not be pro-Russian but it will be pragmatic and focused on salvaging Italy’s economy, which means it will be highly inclined toward diplomacy. If Russia halts its military advance – does not attempt to conquer southwestern Ukraine to Moldova – then this point will be greatly reinforced. Italy will become a new veto player within the European Union when it comes to any major new sanctions on Russia. While Europeans will continue diversifying their energy mix away from Russia, it will be much harder for the EU to implement a natural gas embargo in the coming years if Italy as well as Hungary oppose it. Even if we are wrong, and the Democratic Party or other left-wing parties surprise to the upside in the election, the new coalition will most likely have to focus on mitigating the economic crisis and thus pursuing diplomacy with Russia. That is, as long as Russia pushes for a ceasefire after it achieves its military aims in Donetsk, the last holdout within the south-southeastern territories Russia is trying to conquer. Bottom Line: Due to persistent political uncertainty, we recommend investors underweight Italian stocks and bonds at least until a new government takes shape, which could take months even after the election. However, government bonds will remain vulnerable if a right-wing coalition assumes power, since it will pursue loose fiscal policies and will eschew structural reforms. Overall Italy’s early elections will lead to a new government that is focused on short-term economic growth, likely including pragmatism toward Russia. From an investment point of view that will not be a negative development, though much depends on whether Russia expands its invasion or declares victory after Donetsk. Russia Market-based measures of Russian geopolitical risk are rebounding after subsiding from peak levels hit during the invasion of Ukraine in February (Chart 2). Chart 2Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

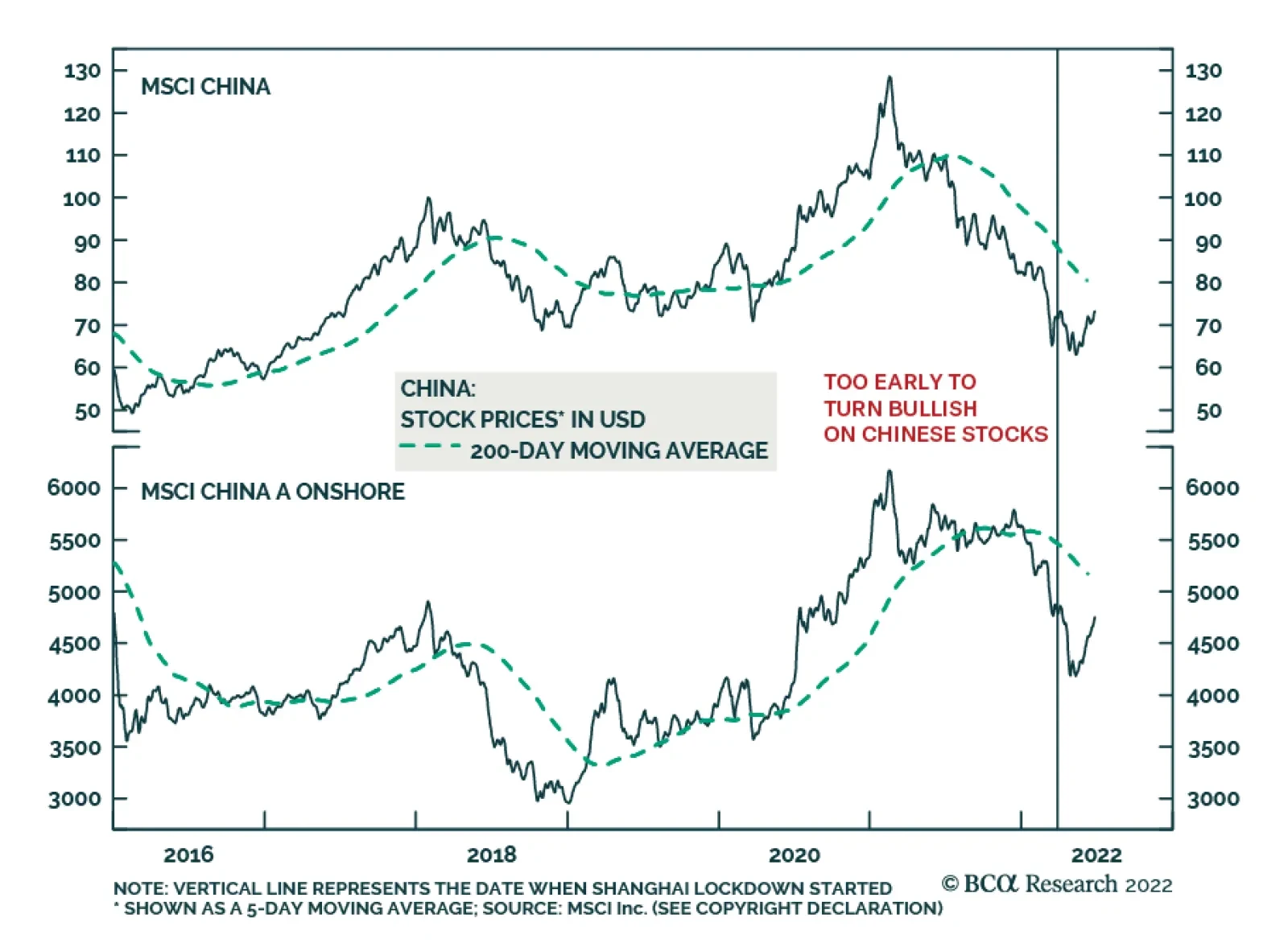

Russia’s continued tightening of natural gas supplies (and food exports) this week is precisely what we predicted would happen despite a wave of wishful thinking from investors over the past month. The optimists claimed that Russia would resume Nord Stream 1 pipeline flows after a regular “maintenance” period. They also said that Canada’s cooperation in resolving some “technical” issues around turbines would stabilize natural gas supply. The truth is that Russia is seeking to achieve its war aims in Ukraine. Until it has achieved its aims, it will use a range of leverage, including tightening food and energy supplies. Most likely Russia will halt the advance after completing the conquest of the Donbas region and land-bridge to Crimea. Then it will seek to legitimize its conquests through a ceasefire agreement. However, it could launch a new phase of the war to try to take Odessa and Transniestria, which would cement European resolve, even in Italy, and trigger a new round of sanctions. Bottom Line: Russia faces a fork in the road once it completes the conquest of Donetsk. Most likely it will declare victory and start pushing for a ceasefire late this year or early next year. Movement toward a ceasefire would reduce geopolitical risk for global financial markets in 2023. But there is still a substantial risk that Russia could expand the invasion to eastern Moldova, which would escalate the overarching Russia-West conflict and sustain the high level of geopolitical risk for markets. China Chinese political and geopolitical risk will continue to rise and the bounce in Chinese relative equity performance is faltering as we expected (Chart 3). Chart 3China: GeoRisk Indicator

China: GeoRisk Indicator

China: GeoRisk Indicator

China’s leaders will hold their secretive annual meeting at Beidaihe in August ahead of the critical Communist Party national congress this fall. General Secretary Xi Jinping is attempting to cement himself as the paramount leader in China, comparable to Chairman Mao Zedong, transforming China’s governance from that of single-party rule to single-person rule. The reversion to autocratic government is coinciding with a historic economic slowdown consisting of cyclical factors (weak domestic demand, weakening foreign demand, draconian Covid-19 restrictions) and structural factors (labor force contraction, property sector bust, social change and unrest). Both Xi and US President Biden face major domestic political challenges in the coming months with the party congress and the US midterm election. Hence they are holding talks to try to stabilize relations. But we do not think they will succeed. China cannot reject Russia’s strategic overture, while the US cannot afford to re-engage with a China that is partnering with Russia in a challenge to the liberal-democratic world order. In addition, US policies are erratic and the US cannot credibly promise China that it will not pursue a containment strategy even if China offers trade concessions. Bottom Line: China-related political and geopolitical risks will remain very high until at least after the twentieth party congress. At that point we expect President Xi to loosen a range of policies to stabilize the economy and foreign trade relations. These policies may bring positive news in 2023, though China’s biggest macroeconomic and geopolitical problems remain structural in nature and we remain underweight Chinese assets. Taiwan For many years we have warned of a “fourth Taiwan Strait crisis” due to the unsustainable geopolitical situation between China, Taiwan, and the United States. After the war in Ukraine we argued that the US would try to boost its strategic deterrence around Taiwan, since it failed to deter Russia from invading Ukraine, but that the increased commitment to Taiwan would in fact provoke China (Chart 4). Chart 4Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Until the US and China reach a new understanding over Taiwan, we argued that the region would be susceptible to rising tensions and crisis points that would send investors fleeing from risky assets, especially risky regional assets. It is possible that we have arrived at this crisis now, with House Speaker Nancy Pelosi making preparations to visit Taiwan, China pledging “forceful” countermeasures if she does, President Biden suggesting that the US military thinks Pelosi should not visit, and Biden and Xi preparing for a phone conversation. In essence China is giving an ultimatum and setting a new bar, and a very low bar, for taking some kind of action on Taiwan, i.e. the mere visit of a US House speaker, which has happened before (House Speaker Newt Gingrich in 1997). China’s purpose is to lay the groundwork for preventing the US from upgrading Taiwan relations in any more substantial way, whether political or military. If the Biden administration calls off the Pelosi visit, then American relations with Taiwan will have been curtailed, at least for this administration. If Biden goes forward with the visit, then Beijing will need to respond with an aggressive show of force to prevent any future president from repeating the exercise or building on it. And if this show threatens US personnel or security, a full-blown diplomatic or military crisis could ensue. While we doubt it would lead to full-scale war, it could lead to a frightening confrontation. Biden may want to stabilize relations with China, since he is primarily focused on countering Russia, but his options are limited. China cannot save him from inflation but it can solidify the public perception that he is weak. Hence he is more likely to maintain his administration’s hawkish approach. Biden’s approval rating is 38% and his party faces a drubbing in the midterm elections. A confrontation with Russia, China, Iran, or anyone else would likely help his party by producing a public rally around the flag. Any unilateral concessions will merely strengthen Xi’s power consolidation at the party congress, which is detrimental to US interests. Only if the Biden administration pursues a dovish policy of re-engagement that is subsequently confirmed by the 2024 presidential election will there be potential for a substantial US-China economic re-engagement. We are pessimistic. Bottom Line: Taiwan-related geopolitical risk will rise in the short run. If there is a new US-China understanding over Taiwan, then regional and global geopolitical risk will decline over the medium term. But we remain short Taiwanese assets. Investment Takeaways Investors should remain defensively positioned until the US midterm election ends with congressional gridlock; the Chinese party congress is over and Xi Jinping launches a broad pro-growth policy; and Russia starts pushing for a ceasefire in Ukraine. We also expect that markets will need to get over new, unexpected oil supply shocks arising from the failure of US-Iran nuclear negotiations, which remains off the radar and therefore a source of negative surprises. Any US-Iran nuclear deal would be a major positive surprise that postpones this risk for a few years. Having said that, we are booking a 9% gain on our long US versus UAE equity trade for technical reasons. Democrats have reached a deal to pass a budget reconciliation bill in an effort to mitigate midterm election losses. This development reinforces the 65% odds of passage that we have maintained for this bill’s passage in our US Political Strategy reports since last year. Yushu Ma Research Analyst yushu.ma@bcaresearch.com Matt Gertken Chief Geopolitical Strategist mattg@bcaresearch.com Appendix UK Chart 5UK: GeoRisk Indicator

United Kingdom: GeoRisk Indicator

United Kingdom: GeoRisk Indicator

Germany Chart 6Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France Chart 7France: GeoRisk Indicator

France: GeoRisk Indicator

France: GeoRisk Indicator

Spain Chart 8Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Canada Chart 9Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Australia Chart 10Australia: GeoRisk Indicator

Australia: GeoRisk Indicator

Australia: GeoRisk Indicator

Korea Chart 11Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Brazil Chart 12Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Turkey Chart 13Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

South Africa Chart 14South Africa: GeoRisk Indicator

South Africa: GeoRisk Indicator

South Africa: GeoRisk Indicator

Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Regional Geopolitical Risk Matrix "Batting Average": Geopolitical Strategy Trades Geopolitical Calendar

Executive Summary Iran Reaches Nuclear Breakout

Biden And Putin Court The Middle East

Biden And Putin Court The Middle East

The next geopolitical crisis will stem from the Middle East. The US, Russia, and China are striving for greater influence there and Iran’s nuclear quest is reaching a critical juncture. The risk of US-Israeli attacks against Iran remains 40% over the medium term and will rise sharply if Iran attempts to construct a deliverable nuclear device. Saudi Arabia may increase oil production but only if global demand holds up, which OPEC will assess at its August 3 meeting. Global growth risks will prevail in the short term and reduce its urgency. Russia will continue to squeeze supplies of energy and food for the outside world. The restart of Nord Stream 1 and the Turkey-brokered grain export proposal are unreliable signals. Russia’s aim is victory in Ukraine and any leverage will be used. The US may be done with the Middle East but the Middle East may not be done with the US. Structurally we remain bullish on gold and European defense stocks but we are booking 17% and 18% gains on our current trades. The deterioration in global growth and likely pullback in inflation will temporarily undercut these trades. Tactical Recommendation Inception Date Return LONG GOLD (CLOSED) 2019-06-12 17.1% LONG EUROPEAN AEROSPACE & DEFENSE / EUROPEAN TECH EQUITIES (CLOSED) 2022-03-18 17.9% Bottom Line: Global demand is weakening, which will weigh on bond yields and commodities. Yet underlying oil supply constraints persist – and US-Iran conflict will exacerbate global stagflation. Feature Chart 1Equity Volatility And Oil Price Volatility

Equity Volatility And Oil Price Volatility

Equity Volatility And Oil Price Volatility

US President Joe Biden visited Saudi Arabia last week in a belated attempt to make amends with OPEC, increase oil production, and reduce inflation ahead of the midterm election. Biden also visited Israel to deter Iran, which is the next geopolitical crisis that markets are underrating. Meanwhile Russian President Vladimir Putin went to Iran on his second trip outside of Russia since this year’s invasion of Ukraine. Putin sought an ally in his conflict with the West, while also negotiating with Turkish President Recep Erdogan, who sought to position himself as a regional power broker. In this report we analyze Biden’s and Putin’s trips and what they mean for the global economy and macro investors. Macroeconomics is bearish for oil in the short term but geopolitics is bullish for oil in the short-to-medium term. The result is volatility (Chart 1). OPEC May Pump More Oil But Not On Biden’s Time Frame Here are the important developments from Biden’s trip: A credible threat against Iran: The US and Israel issued a joint declaration underscoring their red line against Iranian nuclear weaponization.1 Meanwhile the Iranians claimed to have achieved “nuclear breakout,” i.e. enough highly enriched uranium to construct a nuclear device (Chart 2). A balance-of-power coalition to contain Iran: Israel and Saudi Arabia improved relations on the margin. Each took action to build on the strategic détente between Israel and various Arab states that is embodied in the 2020 Abraham Accords.2 This strategic détente has staying power because it is a self-interested attempt by the various nations to protect themselves against common rivals, particularly Iran (Chart 3). Biden also tried to set up a missile defense network with Israel and the Arabs, although it was not finalized.3 Chart 2Iran Reaches Nuclear Breakout

Biden And Putin Court The Middle East

Biden And Putin Court The Middle East

A reaffirmed US-Saudi partnership: The US and Saudi Arabia reaffirmed their partnership despite a rocky patch over the past decade. The rocky patch arises from US energy independence, China’s growth, and US attempts to normalize ties with Iran (Chart 4). These trends caused the Saudis to doubt US support and to view China as a strategic hedge. Chart 3Iran: Surrounded And Outgunned

Biden And Putin Court The Middle East

Biden And Putin Court The Middle East

President Biden came into office aiming to redo the Iran deal and halt arms sales to Saudi Arabia. Since then he has been chastened by high energy prices, a low approval rating, and hawkish Iranian policy. On this trip he came cap in hand to the Saudis in a classic example of geopolitical constraints. If the US-Iran deal is verifiably dead, then US-Saudi ties will improve sustainably. (Though of course the Saudis will still do business with China and even start trading with China in the renminbi.) What global investors want to know is whether the Saudis and OPEC will pump more oil. The answer is maybe someday. The Saudis will increase production to save the global business cycle but not the Democrats’ election cycle. They told Biden that they will increase production only if there is sufficient global demand. Global Brent crude prices have fallen by 6% since May, when Biden booked his trip, so the kingdom is not in a great rush to pump more. Its economy is doing well this year (Chart 5). Chart 4Drivers Of Saudi Anxiety

Drivers Of Saudi Anxiety

Drivers Of Saudi Anxiety

Chart 5Saudis Won't Pump If Demand Is Weak

Saudis Won't Pump If Demand Is Weak

Saudis Won't Pump If Demand Is Weak

At the same time, if global demand rebounds, the Saudis will not want global supply constraints to generate punitive prices that cap the rebound or kill the business cycle. After all, a global recession would deplete Saudi coffers, set back the regime’s economic reforms, exacerbate social problems, and potentially stir up political dissent (Chart 6). Related Report Geopolitical StrategyThird Quarter Geopolitical Outlook: Thunder And Lightning Hence the Saudis will not increase production substantially until they have assessed the global economy and discussed the outlook with the other members of the OPEC cartel in August and September, when the July 2021 agreement to increase production expires. We expect global demand to weaken as Europe and China continue to struggle. Our Commodity & Energy Strategist Bob Ryan argues that further escalation in the energy war between the EU and Russia could push prices above $220 per barrel by Q4 2023, whereas an economic collapse could push Brent down to $60 per barrel. His base case Brent price forecast remains $110 per barrel on average in 2022 and $117 per barrel in 2023 (Chart 7). Chart 6Saudis Will Pump To Prevent Recession

Saudis Will Pump To Prevent Recession

Saudis Will Pump To Prevent Recession

Chart 7BCA's July 2022 Oil Price Forecast

BCA's July 2022 Oil Price Forecast

BCA's July 2022 Oil Price Forecast

The geopolitical view suggests upside oil risks over the short-to-medium time frame but the macroeconomic view suggests that downside risks will be priced first. Bottom Line: Saudi Arabia may increase production but not at any US president’s beck and call. The Saudis are not focused on US elections, they benefit from the current level of prices, and they do not suffer if Republicans take Congress in November. The downside risk in oil prices stems from demand disappointments in global growth (especially China) rather than any immediate shifts in Saudi production discipline. Volatility will remain high. US-Iran Talks: Dying But Not Dead Yet In fact the Middle East underscores underlying and structural oil supply constraints despite falling global demand. While Iran is a perennial geopolitical risk, the world is reaching a critical juncture over the next couple of years. Investors should not assume that Iran can quietly achieve nuclear arms like North Korea. Since August 2021 we have argued that the US and Iran would fail to put back together the 2015 nuclear deal (the Joint Comprehensive Plan of Action or JCPA). This failure would in turn lead to renewed instability across the Middle East and sporadic supply disruptions as the different nations trade military threats and potentially engage in direct warfare. This forecast is on track after Biden’s and Putin’s trip – but we cannot yet say that it is fully confirmed. Biden’s joint declaration with Israeli Prime Minister Yair Lapid closed any daylight that existed between the US and Israel. Given that there was some doubt about the intentions of Biden and the Democrats, it is now crystal clear that the US is determined to prevent Iran from getting nuclear weapons even if it requires military action. The US specifically said that it will use “all instruments of national power” to prevent that outcome. Chart 8Iran Not Forced To Capitulate

Iran Not Forced To Capitulate

Iran Not Forced To Capitulate

Judging by the tone of the statement, the Israelis wrote the document and Biden signed it.4 Biden’s foreign policy emphasizes shoring up US alliances and partnerships, which means letting allies and partners set the line. Israel’s Begin Doctrine – which says that Israel is willing to attack unilaterally and preemptively to prevent a hostile neighbor from obtaining nuclear weapons – has been reinforced. The US is making a final effort to intimidate Iran into rejoining the deal. By clearly and unequivocally reiterating its stance on nuclear weapons, and removing doubts about its stance on Israel, there is still a chance that the Iranian calculus could change. This is possible notwithstanding Ayatollah Khamenei’s friendliness with Putin and criticisms of western deception.5 After all, why would the Iranians want to be attacked by the US and Israeli militaries? Iran will need to think very carefully about what it does next. Khamenei just turned 83 years old and is trying to secure the Islamic Republic’s power transition and survival after his death. Here are the risks: Iran’s economy, buoyed by the commodity cycle, is not so weak as to force Khamenei to capitulate. Back in 2015 oil prices had collapsed and his country was diplomatically isolated. Today the economy has somewhat weathered the storm of the US’s maximum pressure sanctions (Chart 8). Iran is in bad shape but it has not been brought to its knees. Another risk is that Khamenei believes the American public lacks the appetite for war. Americans say they are weary of Middle Eastern wars and do not feel particularly threatened by Iran. However, this would be a miscalculation. US war-weariness is nearing the end of its course. The US engages in a major military expedition roughly every decade. Americans are restless and divided – and the political elite fear populism – so a new foreign distraction is not as unlikely as the consensus holds. Moreover a nuclear Iran is not an idle threat but would trigger a regional nuclear arms race and overturn the US grand strategy of maintaining a balance of power in the Middle East (as in other regions). In short, the US government can easily mobilize the people to accept air strikes to prevent Iran from going nuclear because there is latent animosity toward Iran in both political parties (Chart 9). Chart 9Risk: Iran Overrates US War-Weariness

Biden And Putin Court The Middle East

Biden And Putin Court The Middle East

Another risk is that Iran forges ahead believing that the US and Israel are unwilling or unable to attack and destroy its nuclear program. The western powers might opt for containment like they did with North Korea or they might attack and fail to eliminate the program. This is hard to believe but Iran clearly cannot accept US security guarantees as an alternative to a nuclear deterrent when it seeks regime survival. At the same time Russia is courting Iran, encouraging it to join forces against the American empire. Iran is planning to sell drones to Russia for use in Ukraine, while Russia is maintaining nuclear and defense cooperation with Iran. Putin’s trip highlighted a growing strategic partnership despite a low base of economic ties (Chart 10).6 Chart 10Russo-Iranian Ties

Russo-Iranian Ties

Russo-Iranian Ties

Chart 11West Vulnerable To Middle East War

Biden And Putin Court The Middle East

Biden And Putin Court The Middle East

While Russia does not have an interest in a nuclear-armed Iran, it is not afraid of Iran alone, and it would benefit enormously if the US and Israel got bogged down in a new war that destabilized the Middle East. Oil prices would rise, the US would be distracted, and Europe would be even more vulnerable (Chart 11). Chart 12China's Slowdown And Dependency On Middle East

China's Slowdown And Dependency On Middle East

China's Slowdown And Dependency On Middle East

China’s interest is different. It would prefer for Iran to undermine the West by means of a subtle and long-term game of economic engagement rather than a destabilizing war in the region that would upset China’s already weak economy. However, Beijing will not join with the US against Iran, especially if Iran and Russia are aligned. Ultimately China needs to access Iranian energy reserves via overland routes so that it gains greater supply security vis-à-vis the American navy (Chart 12). Since June 2019, we have maintained 40% odds of a military conflict with Iran. The logic is outlined in Diagram 1, which we have not changed. Conflict can take various forms since the western powers prefer sabotage or cyber-attacks to outright assault. But in the end preventing nuclear weapons may require air strikes – and victory is not at all guaranteed. We are very close to moving to the next branch in Diagram 1, which would imply odds of military conflict rise from 40% to 80%. We are not making that call yet but we are getting nervous. Diagram 1Iran Nuclear Crisis: Decision Tree

Biden And Putin Court The Middle East

Biden And Putin Court The Middle East

Moreover it is the saber rattling around this process – including an extensive Iranian campaign to deter attack – that will disrupt oil distribution and transport sooner rather than later. Bottom Line: The US and Iran could still find diplomatic accommodation to avoid the next step in our decision tree. Therefore we are keeping the odds of war at a subjective 40%. But we have reached a critical juncture. The next step in the process entails a major increase in the odds of air strikes. Putin’s Supply Squeeze Will Continue As we go to press, financial markets are reacting to President Putin’s marginal easing of Russian political pressure on food and energy supplies. First, Putin took steps toward a deal, proposed by Turkish President Erdogan, to allow Ukrainian grain exports to resume from the Black Sea. Second, Putin allowed a partial restart of the Nord Stream 1 natural gas pipeline, after a total cutoff occurred during the regular, annual maintenance period. However, these moves should be kept into perspective. Nord Stream 1 is still operating at only 40% of capacity. Russia reduced the flow by 60% after the EU agreed to impose a near-total ban on Russian oil exports by the end of the year. Russia is imposing pain on the European economy in pursuit of its strategic objectives and will continue to throttle Europe’s natural gas supply. Russia’s aims are as follows: (1) break up European consensus on Russia and prevent a natural gas embargo from being implemented in future (2) pressure Europe into negotiating a ceasefire in Ukraine that legitimizes Russia’s conquests (3) underscore Russia’s new red line against NATO military deployments in Finland and Sweden. Europe, for its part, will continue to diversify its natural gas sources as rapidly as possible to reduce Russia’s leverage. The European Commission is asking countries to decrease their natural gas consumption by 15% from August to March. This will require rationing regardless of Russia’s supply squeeze. The collapse in trust incentivizes Russia to use its leverage while it still has it and Europe to try to take that leverage away. The economic costs are frontloaded, particularly this winter. The same goes for the Turkish proposal to resume grain exports. Russia will continue to blockade Ukraine until it achieves its military objectives. The blockade will be tightened or loosened as necessary to achieve diplomatic goals. Part of the reason Russia invaded in the first place was to seize control of Ukraine’s coast and hold the country’s ports, trade, and economy hostage. Bottom Line: Russia’s relaxation of food and energy flows is not reliable. Flows will wax and wane depending on the status of strategic negotiations with the West. Europe’s economy will continue to suffer from a Russia-induced supply squeeze until Russia achieves a ceasefire in Ukraine. So will emerging markets that depend on grain imports, such as Turkey, Egypt, and Pakistan. Investment Takeaways The critical juncture has arrived for our Iran view. If Iran does not start returning to nuclear compliance soon, then a fateful path of conflict will be embarked upon. The Saudis will not give Biden more oil barrels just yet. But they may end up doing that if global demand holds up and the US reassures them that their regional security needs will be met. First, the path for oil over the next year will depend on the path of global demand. Our view is negative, with Europe heading toward recession, China struggling to stimulate its economy effectively, and the Fed unlikely to achieve a soft landing. Second, the path of conflict with Iran will lead to a higher frequency of oil supply disruptions across the Middle East that will start happening very quickly after the US-Iran talks are pronounced dead. In other words, oil prices will be volatile in a stagflationary environment. In addition, while inflation might roll over for various reasons, it is not likely to occur because of any special large actions by Saudi Arabia. The Saudis are waiting on global cues. Of these, China is the most important. We are booking a 17% gain on our long gold trade as real rates rise and China’s economy deteriorates (Chart 13). This is in line with our Commodity & Energy Strategy, which is also stepping aside on gold for now. Longer term we remain constructive as we see a secular rise in geopolitical risk and persistent inflation problems. Chart 13Book Gains On Gold ... For Now

Book Gains On Gold ... For Now

Book Gains On Gold ... For Now

We are booking an 18% gain on our long European defense / short European tech trade. Falling bond yields will benefit European tech (Chart 14). We remain bullish on European and global defense stocks. Chart 14Book Gains On EU Defense Vs Tech ... For Now

Book Gains On EU Defense Vs Tech ... For Now

Book Gains On EU Defense Vs Tech ... For Now

Chart 15Markets Underrate Middle East Geopolitical Risk

Biden And Putin Court The Middle East

Biden And Putin Court The Middle East

Stay long US equities relative to UAE equities. Middle Eastern geopolitical risk is underrated (Chart 15). Matt Gertken Chief Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 The White House, “The Jerusalem U.S.-Israel Strategic Partnership Joint Declaration,” July 14, 2022, whitehouse.gov. 2 Israel and the US will remove international peacekeepers from the formerly Egyptian Red Sea islands of Tiran and Sanafir, which clears the way for Saudi Arabia to turn them into tourist destinations. Saudi Arabia also removed its tight airspace restrictions on Israel, enabling civilian Israeli airlines to fly through Saudi airspace on normal basis. Of course, Saudi allowance for Israeli military flights to pass through Saudi airspace would be an important question in any future military operation against Iran. 3 The US has long wanted regional missile defense integration. The Biden administration is proposing “integrated air defense cooperation” that would include Israel as well as the Gulf Cooperation Council (GCC). A regional “air and missile defense architecture” would counter drones and missiles from rival states and non-state actors such as Iran and its militant proxies. Simultaneously the Israelis are putting forward the proposed Middle East Air Defense Alliance (MEAD) in meetings with the same GCC nations. Going forward, Iran’s nuclear ambitions will give more impetus to these attempts to cooperate on air defense. 4 This is apparent from the hard line on Iran and the relatively soft line on Russia in the document. Israel is wary of taking too hard of a line against Russia because of its security concerns in Syria where Russian forces are present. See footnote 1 above. 5 Khamenei called for long-term cooperation between Russia and Iran; he justified Russia’s invasion of Ukraine as a defense against NATO encroachment; he called for the removal of the US dollar as the global reserve currency. See “Khamenei: Tehran, Moscow must stay vigilant against Western deception,” Israel Hayom, July 20, 2022, israelhayom.com. 6 Russia’s natural gas champion Gazprom signed an ostensible $40 billion memorandum of understanding with Iran’s National Oil Company to develop gas fields and pipelines. See Nadeen Ebrahim, “Iran and Russia’s friendship is more complicated than it seems,” CNN, July 20, 2022, cnn.com. However, while there are longstanding obstacles to Russo-Iranian cooperation, the West’s tough new sanctions on Russia and EU diversification will make Moscow more willing to invest in Iran. Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Regional Geopolitical Risk Matrix

Executive Summary China's Unemployment

Questions From The Road

Questions From The Road

Over the past week we have been visiting clients along the US west coast. In this report we hit some of the highlights from the most important and frequently asked questions. Xi Jinping is seizing absolute power just as the country’s decades-long property boom turns to bust. He will stimulate the economy but Chinese stimulus is less effective than it used to be. The US and Israel are underscoring their red line against Iranian nuclear weaponization. If Iran does not freeze its nuclear program, the Middle East will begin to unravel again. The UK’s domestic instability is returning, with Scotland threatening to leave the union. Brexit, the pandemic, and inflation make a Scottish referendum a more serious risk than in the past. Shinzo Abe’s assassination makes him a martyr for a vision of Japan as a “normal country” – i.e. one that is not pacifist but capable of defending itself. Japan’s rearmament, like Germany’s, points to the decline of the WWII peace settlement and the return of great power competition. Bottom Line: Investors need a new global balance to be achieved through US diplomacy with Russia, China, and Iran. That is not forthcoming, as the chief nations face instability at home and a stagflationary global economy. Feature The world is becoming less stable as stagflation combines with great power competition. Global uncertainty is through the roof. From a macroeconomic perspective, investors need to know whether central banks can whip inflation without triggering a recession. From a geopolitical perspective, investors need to know whether Russia’s conflict with the West will expand, whether US-China and US-Iran tensions will escalate in a damaging way, and whether domestic political rotations in the US and China this fall will lead to more stable and productive economies. China: What Will Happen At The Communist Party Reshuffle? General Secretary Xi Jinping will cement another five-to-10 years in power while promoting members of his faction into key positions on the Politburo and Politburo Standing Committee. By December Xi will roll out a pro-growth strategy for 2023 and the government will signal that it will start relaxing Covid-19 restrictions. But China’s structural problems ensure that this good news for global growth will only have a fleeting effect. China’s governance is shifting from single-party rule to single-person rule. It is also shifting from commercially focused decentralization to national security focused centralization. Xi has concentrated power in himself, in the party, and in Beijing at the expense of political opponents, the private economy, and outlying regions like Hong Kong, the South China Sea, and Xinjiang. The subordination of Taiwan is the next major project, ensuring that China will ally with Russia and that the US and China cannot repair or deepen their economic partnership. Related Report Geopolitical StrategyWill China Let 100 Flowers Bloom? Only Briefly. Xi and the Communist Party began centralizing political power and economic control shortly after the Great Recession. At that time it became clear that a painful transition away from export manufacturing and close relations with the United States was necessary. The transition would jeopardize China’s long-term economic, social, political, and geopolitical stability. The Communist Party believed it needed to revive strongman leadership (autocracy) rather than pursuing greater liberalization that would ultimately increase the odds of political revolution (democratization). The Xi administration has struggled to manage the country’s vast debt bubble, given that total debt standing has surged to 287% of GDP. The global pandemic forced the government to launch another large stimulus package, which it then attempted to contain. Corporate and household deleveraging ensued. The property and infrastructure boom of the past three decades has stalled, as the regime has imposed liquidity and capital requirements on banks and property developers to try to avoid a financial crisis. Regulatory tightening occurred in other sectors to try to steer investment into government-approved sectors and reduce the odds of technological advancement fanning social dissent. China’s draconian “zero Covid” policy sought to limit the disease’s toll, improve China’s economic self-reliance, and eliminate the threat of social protest during the year of the twentieth party congress. But it also slammed the brakes on growth. China is highly vulnerable to social instability for both structural and cyclical reasons. Chinese social unrest was our number one “Black Swan” for this year and it is now starting to take shape in the form of angry mortgage owners across the country refusing to make mortgage payments on houses that were pre-purchased but not yet built and delivered (Chart 1). Chart 1China: Mortgage Payment Boycott

Questions From The Road

Questions From The Road

The mortgage payment boycott is important because it is stemming from the outstanding economic and financial imbalance – the property sector – and because it is a form of cross-regional social organization, which the Communist Party will disapprove. There are other social protests emerging, including low-level bank runs, which must be monitored very closely. Local authorities will act quickly to stop the spread of the mortgage boycott. But unhappy homeowners will be a persistent problem due to the decline of the property sector and industry. China’s property sector looks uncomfortably like the American property sector ahead of the 2006-08 bust. Prices for existing homes are falling while new house prices are on the verge of falling (Chart 2). While mortgages only make up 15% of bank assets, and household debt is only 62% of GDP, households are no longer taking on new debt (Chart 3). Chart 2China's Falling Property Prices

China's Falling Property Prices

China's Falling Property Prices

Chart 3China's Property Crisis

China's Property Crisis

China's Property Crisis

Chart 4China's Unemployment

China's Unemployment

China's Unemployment

Most likely China’s property sector is entering the bust phase that we have long expected – if not, then the reason will be a rapid and aggressive move by authorities to expand monetary and fiscal stimulus and loosen economic restrictions. That process of broad-based easing – “letting 100 flowers bloom” – will not fully get under way until after the party congress, say in December. Unemployment is rising across China as the economy slows, another point of comparison with the United States ahead of the 2008 property collapse (Chart 4). Unemployment is a manipulated statistic so real conditions are likely worse. There is no more important indicator. China’s government will be forced to ease policy, creating a positive impact on global growth in 2023, but the impact will be fleeting. Bottom Line: The underlying debt-deflationary context will prevail before long in China, weighing on global growth and inflation expectations on a cyclical basis. Middle East: Why Did Biden Go And What Will He Get? President Biden traveled to Israel and now Saudi Arabia because he wants Saudi Arabia and the Gulf Arab members of OPEC to increase oil production to reduce gasoline prices at the pump for Americans ahead of the midterm elections (Chart 5). Chart 5Biden Goes To Israel And Saudi Arabia

Biden Goes To Israel And Saudi Arabia

Biden Goes To Israel And Saudi Arabia

True, fears of recession are already weighing on prices, but Biden embarked on this mission before the growth slowdown was fully appreciated and he is not going to lightly abandon the anti-inflation fight before the midterm election. Biden also went because one of his top foreign policy priorities – the renegotiation of the 2015 nuclear deal with Iran – is falling apart. The Iranians do not want to freeze their nuclear program because they want regime survival and security. While Biden is offering a return to the 2015 deal, the conditions that produced the deal are no longer applicable: Russia and China are not cooperating with the US and EU to isolate Iran. Russia is courting Iran, oil prices are high and sanction enforcement is weak (unlike 2015). The Iranians now know, after the Trump administration, that they cannot trust the Americans to give credible security guarantees that will last across parties and administrations. The war in Ukraine also underscores the weakness of diplomatic security guarantees as opposed to a nuclear deterrent. Hence the joint US and Israeli declaration that Iran will never be allowed to obtain nuclear weapons. The good news is that this kind of joint statement is precisely what needed to occur – the underscoring of the red line – to try to change Ayatollah Ali Khamenei’s calculus regarding his drive to achieve nuclear breakout. In 2015 Khamenei gave diplomacy a chance to try to improve the economy, stave off social unrest, prepare the way for his eventual leadership succession process, and secure the Islamic Republic. The bad news is that Khamenei probably cannot make the same decision this time, as the hawkish faction now runs his government, the Americans are unreliable, and Russia and China are offering an alternative strategic orientation. The Saudis will pump more oil if necessary to save the global business cycle but not at the beck and call of a US president. The drop in oil prices reduces their urgency. The Americans can reassure the Saudis and Israel as long as the deal with Iran is not going forward. That looks to be the case. But then the US and Israel will have to undertake joint actions to underline their threat to Iran – and Iran will have to threaten to stage attacks across the region so as to deter any attack. Bottom Line: If a US-Iran deal does not materialize at the last minute, Middle Eastern instability will revive and a new source of oil supply constraint will plague the global economy. We continue to believe a US-Iran deal is unlikely, with only 40% odds of happening. Europe: Will Russia Turn Back On The Natural Gas? Russia’s objective in cutting off European natural gas is to inflict a recession on Europe. It wants a better bargaining position on strategic matters. Therefore we assume Russia will continue to squeeze supplies from now through the winter, when European demand rises and Russian leverage will peak. If Russia allows some flow to return, then it will be part of the negotiating process and will not preclude another cutoff before winter. It is possible that Russia is merely giving Europe a warning and will revert back to supplying natural gas. The problem is that Russia’s purpose is to achieve a strategic victory in Ukraine and in negotiations over NATO’s role in the Nordic countries. Russia has not achieved these goals, so natural gas cutoff will likely continue. Russia also hopes that by utilizing its energy leverage – while it still has it – it will bring forward the economic pain of Europe’s transition away from reliance on Russian energy. In that case European countries will experience recession and households will begin to change their view of the situation. European governments will be more likely to change their policies, to become more pragmatic and less confrontational toward Russia. Or European governments will be voted out of power and do the same thing. Other states could join Hungary in saying that Europe should never impose a full natural gas embargo on Russia. Russia would be able to salvage some of its energy trade with Europe over the long run, despite the war in Ukraine and the inevitable European energy diversification. In recent months we highlighted Italy as the weakest link in the European chain and the country most likely to see such a shift in policy occur. Italy’s national unity coalition had lost its reason for being, while the combination of rising bond yields and natural gas prices weighed on the economy. The Italian bond spread over German bunds has long served as our indicator of European political stress – and it is spiking now, forcing the European Central Bank to rush to plan an anti-fragmentation strategy that would theoretically enable it to tighten monetary policy while preventing an Italian debt crisis (Chart 6). The European Union remains unlikely to break up – Russian aggression was always one of our chief arguments for why the EU would stick together. But Italy will undergo a recession and an election (due by June 2023 but that could easily happen this fall), likely producing a new government that is more pragmatic with regard to Russia so as to reduce the energy strain. Chart 6Italy's Crisis Points To EU Divisions On Russia

Italy's Crisis Points To EU Divisions On Russia

Italy's Crisis Points To EU Divisions On Russia

Italy’s political turmoil shows that European states are feeling the energy crisis and will begin to shift policies to reduce the burden on households. Households will lose their appetite for conflict with Russia on behalf of Ukrainians, especially if Russia begins offering a ceasefire after completing its conquest of the Donetsk area. If Russia expands its invasion, then Europe will expand sanctions and the risk of further strategic instability will go up. But most likely Russia will seek to quit while it is ahead and twist Europe’s arm into foisting a ceasefire onto Ukraine. Bottom Line: A change of government in Italy will increase the odds that the EU will engage in diplomacy with Russia in the coming year, if Russia offers, so as to reach a new understanding, restore natural gas flows, and salvage the economy. This would leave NATO enlargement unresolved but a shift in favor of a ceasefire in Ukraine in 2023 would be less negative for European assets and the euro. UK: Who Will Replace Boris Johnson? Last week UK Prime Minister Boris Johnson fell from power and now the Conservative Party is engaging in a leadership competition to replace him. We gave up on Johnson after he survived his no-confidence vote and yet it became clear that he could not recover in popular opinion. The inflation outburst destroyed his premiership and wiped away whatever support he had gained from executing Brexit. In fact it reinforced the faction that believed Brexit was the wrong decision. Going forward the UK will be consumed with domestic political turmoil as the cost of stagflation mounts, and geopolitical turmoil as Scotland attempts to hold a second independence referendum, possibly by October 2023. Global investors should focus primarily on Scotland’s attempt to secede, since the breakup of the United Kingdom would be a momentous historical event and a huge negative shock for pound sterling. While only 44.7% of Scots voted for independence in 2014, now they have witnessed Brexit, Covid-19, and stagflation, producing tailwinds for the Scots nationalist vote (Chart 7). Chart 7Forget Bojo's Exit, Watch Scotland

Questions From The Road

Questions From The Road

There are still major limitations on Scotland exiting, since its national capabilities are limited, it would need to join the European Union, and Spain and possibly others will threaten to veto its membership in the European Union for fear of feeding their own secessionist movements. But any new referendum – including one done without the approval of Westminster – should be taken very seriously by investors. Bottom Line: Johnson’s removal will only marginally improve the Tories’ ability to manage the rebellion brewing in the north. A snap election that brings the Labour Party back into power would have a greater chance of keeping Scotland in the union, although it is not clear that such a snap election will happen in time to affect any Scottish decision. The UK faces economic and political turmoil between now and any referendum and investors should steer clear of the pound. (Though we still favor GBP over eastern European currencies). Britain will remain aggressive toward Russia but its ability to affect the Russian dynamic will fall, leaving the US and EU to decide the fate of Russian relations. Japan: What Is The Significance Of Shinzo Abe’s Assassination? Former Japanese Prime Minister Shinzo Abe was assassinated by a lone fanatic with a handmade gun. The significance of the incident is that Abe will become a martyr for a certain vision of Japan – his vision of Japan, which is that Japan can become a “normal country” that moves beyond the shackles of the guilt of its imperial aggression in World War II. A normal country is one that is economically stable and militarily capable of defending itself – not a pacifist country mired in debt-deflation. Abe stood for domestic reflation and a proactive foreign policy, along with the normalization of the Japanese Self-Defense Forces (JSDF). True, economic policy can become less dovish if necessary to deal with inflation. Some changes at the Bank of Japan may usher in a less dovish shift in monetary policy in particular. But monetary policy cannot become outright hawkish like it was before Abe. And Abe’s fiscal policy was never as loose as it was made out to be, given that he executed several hikes to the consumption tax. Japan’s structural demographic decline and large debt burden will continue to weigh on economic activity whenever real rates and the yen rise. The government will be forced to reflate using monetary and fiscal policy whenever deflation threatens to return. Debt monetization will remain an option for future Japanese governments, even if it is restrained during times of high inflation. Chart 8Shinzo Abe's Legacy

Questions From The Road

Questions From The Road

This is not only because Japanese households will become depressed if deflation is left unchecked but also because economic growth must be maintained in order to sustain the nation’s new and growing national defense budgets. Japan’s growing need for self defense stems from China’s strategic rise, Russia’s aggression, and North Korea’s nuclearization, plus uncertainty about the future of American foreign policy. These trends will not change anytime soon. Indeed the Liberal Democratic Party’s popularity has increased under Abe’s successor, Prime Minister Fumio Kishida, who will largely sustain Abe’s vision. The Diet still has a supermajority in favor of constitutional revision so as to enshrine the self-defense forces (Chart 8). And the de facto policy of rearmament continues even without formal revision. Bottom Line: Any Japanese leader who attempts to promote a hawkish BoJ, and a dovish JSDF, will fail sooner rather than later. The revolving door of prime ministers will accelerate. As Japan’s longest-serving prime minister, Shinzo Abe opened up the reliable pathway, which is that of a dovish BoJ and a hawkish foreign policy. This is important for the world, as well as Japan, because a more hawkish Japan will increase China’s fears of strategic containment. The frozen conflicts in Asia will continue to thaw, perpetuating the secular rise in geopolitical risk. We remain long JPY-KRW, since the BoJ may adjust in the short term and Chinese stimulus is still compromised, but that trade is on downgrade watch. Investment Takeaways Russia’s energy cutoff is aimed at pushing Europe into recession so as to force policy changes or government changes in Europe that will improve Russia’s position at the negotiating table over Ukraine, NATO, and other strategic disputes. Hence Russia is unlikely to increase the natural gas flow until it believes it has achieved its strategic aims and multiple veto players in the EU will prevent the EU from ever implementing a full-blown natural gas embargo. Chinese stimulus cannot be fully effective until it relaxes Covid-19 restrictions, likely beginning in December or next year when Xi Jinping uses his renewed political capital to try to stabilize the economy. However, China’s government powers alone are insufficient to prevent the debt-deflationary tendency of the property bust. The Middle East faces rising geopolitical tensions that will take markets by surprise with additional energy supply constraints. The implication is continued oil volatility given that global growth is faltering. Once global demand stabilizes, the Middle East’s turmoil will add to existing oil supply constraints to create new price pressures. The odds are not very high of the Federal Reserve achieving a “soft landing” in the context of a global energy shock and a stagflationary Europe and China. Matt Gertken Chief Geopolitical Strategist mattg@bcaresearch.com Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Regional Geopolitical Risk Matrix "Batting Average": Geopolitical Strategy Trades () Section II: Special (EDIT this Header) Section III: Geopolitical Calendar

Executive Summary Global risk assets are oversold, and investor sentiment is downbeat. In this context, a technical equity rebound cannot be ruled out. However, we do not think it will be the beginning of a major cyclical rally. The Fed and the stock market remain on a collision course. An equity rally and easing financial conditions would make the Fed even more resolute to continue hiking interest rates. There are many similarities between dynamics that prevailed in US tech stocks and in previous bubbles. While it is not our baseline view, the odds of a protracted bear market are nontrivial. Resource prices and commodity plays have more downside. The History Of Financial Bubbles: Is This Time Different?

On A Bull Case, Bubbles And Commodity Prices

On A Bull Case, Bubbles And Commodity Prices

Bottom Line: The decline in commodity prices and the relentless US dollar rally will ensure that EM currencies, bonds and stocks continue to sell off even if the US equity market rebounds in the near term. Feature Among the most frequently discussed topics in recent client calls are the upside and downside risks to our baseline view. We elaborate on these risks in this report. To recap, our baseline view is as follows: EM and DM stocks have another 15% downside in USD terms, the US dollar will continue overshooting and commodity prices will fall. Global yields are topping out, and the US yield curve will soon invert. Hence, defensive positioning for absolute-return investors is still warranted, and global equity and fixed-income portfolios should continue to underweight EM. The rationale is that US and EU demand for goods ex-autos, and hence global trade, is about to contract while the Fed is straightjacketed by high and broad-based inflation. China’s economy will be struggling to recover. In EM ex-China, domestic demand will relapse. Chart 1Will The S&P 500's Technical Support Hold?

Will The S&P 500's Technical Support Hold?

Will The S&P 500's Technical Support Hold?

If one believes that the US equity bull market that began in 2009 is still alive (i.e. the March 2020 selloff is a short-lived red herring), odds are that the S&P 500 drawdown is over. The reasoning is that the S&P 500 is already down 23% from its 2021 peak, on par with the selloffs that occurred in 2011, 2015-16 and 2018 (Chart 1). However, if one believes that the structural bull market is over, the magnitude of the current equity selloff is likely to exceed the ones in 2011, 2015-16 and 2018. Hence, a bearish stance is still warranted. As we argue below, after a 12-year bull run, the excesses in the US equity market in general, and US tech stocks in particular, have become extreme. There are many signs of a bubble, or at least of a major top. Even though we risk overstaying in our negative view, our bias is that the global equity market rout is not yet over. A Bullish Scenario A (hypothetical) bullish case would look something like this: Weakening global and US growth and falling commodity prices bring down US inflation and Treasury yields. As US bond yields drop further, the S&P 500 rallies given their negative correlation of the past 18 months or so. As US inflation declines rapidly, the Fed makes a dovish pivot, reinforcing the risk asset rally and reversing the US dollar’s uptrend. Finally, Chinese stimulus produces a robust business cycle recovery in China that propels commodity prices higher and lifts the rest of EM out of the abyss. Chart 2Keep An Eye On Rising US Trimmed-Mean Inflation

Keep An Eye On Rising US Trimmed-Mean Inflation

Keep An Eye On Rising US Trimmed-Mean Inflation

In our opinion, this scenario has no more than a 25% chance of playing out. Even if there are apparent signs of a US/global slowdown, elevated US core inflation and accelerating wages and unit labor costs would keep the Fed from dialing down its hawkishness Critically, even though US core PCE inflation has rolled over and will likely decline further, its trimmed-mean PCE inflation is rising (Chart 2). The latter means that inflation is broadening even as some volatile items like food, energy and used-auto prices deflate. As we have written extensively, wages and inflation are lagging variables. Despite the ongoing slowdown in the US economy, it will take many months before the underlying core inflation rate drops below 3%. We maintain that the Fed and the stock market remain on a collision course. An equity rally and easing financial conditions would make the Fed even more resolute to hike interest rates. The basis is that even if core inflation falls in the coming months, it would still be well above the Fed’s target of 2%. Notably, the Fed has recently communicated that its commitment to bring down inflation to 2% is unconditional. Chart 3The Anatomy Of The US Equity Bear Market In 2000-2002

The Anatomy Of The US Equity Bear Market In 2000-2002

The Anatomy Of The US Equity Bear Market In 2000-2002

This policy stance represents a major departure from the past several decades when the Fed was very sensitive to any tightening in financial conditions and often eased preemptively. In short, with inflation still well above its target, the Fed will, for now, err on the side of hawkishness if financial conditions ease. Importantly, US corporate profits will likely contract even if US real GDP does not shrink. As US corporate top-line growth slows and unit labor costs accelerate, profit margins will shrink. For example, the 2001-2002 recession was very mild – consumer spending did not contract at all, and housing boomed (Chart 3, top two panels). Yet, the S&P 500 operating earnings dropped by 30%, and the S&P 500 fell by 50% (Chart 3, bottom two panels). In brief, a devastating bear market does not necessarily require a hard landing. Concerning China, the recovery will likely be U-shaped rather than V-shaped with risks skewed to the downside. Finally, contracting global trade and falling commodity prices will continue, which are negative for EM currencies and assets. Notably, industry data from Taiwan’s manufacturing PMI suggest that the slowdown in the Asian and global economies is widespread. Taiwan’s substantial trade linkages with mainland China signify that the slowdown is not limited to the US and the EU but includes China too. Taiwanese PMI export orders of both semiconductor and basic material producers have plunged to 40 and 30, respectively (Chart 4). Barring a quick turnaround, global semiconductor and basic materials stocks have more downside. Even as US Treasury yields drop, the dollar will continue firming versus EM currencies, including those of Emerging Asian countries. In such a scenario, EM stocks and bonds will weaken further (Chart 5). Chart 4A Broad-Based Contraction In Global Trade Is In The Cards

A Broad-Based Contraction In Global Trade Is In The Cards

A Broad-Based Contraction In Global Trade Is In The Cards

Chart 5A Free Fall In EM Ex-China Stocks And Currencies

A Free Fall In EM Ex-China Stocks And Currencies

A Free Fall In EM Ex-China Stocks And Currencies

Bottom Line: The S&P 500 is oversold, and investor sentiment is downbeat. In this context, a technical equity rebound can occur at any moment. However, we do not think it will be the beginning of a major cyclical rally. A Bearish Case: Are US TMT Stocks A Bubble? What is a more bearish scenario than our baseline case? The bursting of bubbles or the unwinding of excesses would entail a more protracted and devastating bear market than the 15% drop in global share prices we currently expect. We can identify two major excesses in the global economy and financial system: In US TMT (Technology, Media & Entertainment and Internet & Catalog Retail) stocks and private equity In Chinese real estate. We have written extensively about property market excesses in China. Below we discuss the recent sharp selloff in commodities, which is partially linked to Chinese property construction. We also present the case for major excesses in US stocks. Chart 6 illustrates the history of bubbles of the past several decades: The Nifty-fifty (involving the 50 US large-cap stocks) bubble occurred in the 1960s and burst in the 1970s (not shown in the chart). The commodity bubble took place in the 1970s and burst in the 1980s. Japanese equity and property prices rose exponentially in the 1980s and deflated in the 1990s. The Nasdaq bubble occurred in the 1990s and was shattered in the early 2000s. Commodities/EM/China were the leaders of the 2000s, and they were devastated in the 2010s. We use iron ore in this chart because its price surged the most in the 2000s. FAANGM stocks, the Nasdaq 100 index and private equity were by far the biggest beneficiaries of the 2010s. No one can be certain about bubbles in real time because there are always superior fundamentals or persuasive stories that justify exponential price appreciation. That said, there are a lot of similarities between dynamics prevailing in US tech and private equity and in previous bubbles: In the past decade, FAANGM stocks, the Nasdaq 100 index and private equity companies registered gains comparable to the bubbles of the previous 60 years. Furthermore, as Chart 6 illustrates, the equal-weighted FAANGM index in inflation-adjusted terms rose 30-fold, much more than the bubbles of the previous decades. The Nasdaq 100 index and share prices of Blackstone, the largest private equity company, have risen by nearly 10-fold in real (inflation-adjusted terms) between 2010 and the end of 2021. Chart 6The History Of Financial Bubbles: Is This Time Different?

On A Bull Case, Bubbles And Commodity Prices

On A Bull Case, Bubbles And Commodity Prices

The final phase of bubbles is often characterized by growing retail investor participation. This is exactly what happened with US tech/new economy stocks. Chart 7US TMT Stocks: Exponential Growth Rarely Ends Well

US TMT Stocks: Exponential Growth Rarely Ends Well

US TMT Stocks: Exponential Growth Rarely Ends Well

Toward the end of the decade, not only retail but also institutional capital stampedes into the winners of the decade. This played out with US large-cap tech stocks as well as in private equity and private debt spaces. Inflows into private equity and private debt have been enormous. As a result of these inflows into US large-cap stocks, the market cap share of US TMT stocks as a percentage of total US market cap has surpassed 40%, its peak in 2000 (Chart 7). Bubbles often thrive during periods of low interest rates and crash when the cost of capital rises. This is exactly what has been happening in global financial markets since early 2019. The parameters of the overall US equity market were also excessive prior to this bear market. As of last year, the S&P 500 stock prices in real (inflation-adjusted) terms became as elevated relative to their long-term time trend as they were in the late 1960s and the late 1990s − the peaks of previous secular bull markets (Chart 8, top panel). Chart 8The S&P 500 and Operating Profits: A Long-Term Perspective

The S&P 500 and Operating Profits: A Long-Term Perspective

The S&P 500 and Operating Profits: A Long-Term Perspective

Chart 9Equity Issuance Marks Market Tops

Equity Issuance Marks Market Tops

Equity Issuance Marks Market Tops

The S&P 500’s operating earnings in real terms have surpassed two standard deviations above its time trend (Chart 8, bottom panel). Some sort of mean reversion to its long-term trend is in the cards. US corporate profits have benefited from fiscal/monetary stimulus, low labor costs and pricing power. All of these are now working against profits. Finally, new share issuance in the US mushroomed in 2021, another sign of a major top (Chart 9). Bottom Line: We are not entirely convinced that US TMT stocks are a bubble waiting to burst. Yet, the odds of this happening are nontrivial. This time might not be different. A Word On Commodities The selloff in the commodity space has been broad-based. Odds are that it will continue for the following reasons: A global business cycle downtrend is always bearish for commodity prices. In fact, oil prices are often lagging and are typically the last shoe to drop during global slowdowns. US sales of gasoline have started to contract. Besides, Saudi Arabia will likely increase its oil output and shipments following President Biden’s visit to the Kingdom next week. Chart 10Investors Have Been Long Commodity Futures

Investors Have Been Long Commodity Futures

Investors Have Been Long Commodity Futures

As we have argued in recent months, China’s demand for commodities was contracting and, in our opinion, the rally in resource prices over the past 12 months was supported by investment demand for commodities, i.e., financial inflows into the commodity space. Many portfolios have bought commodities as an inflation hedge. When a hedge becomes a consensus trade and crowded, it stops being a hedge. Chart 10 demonstrates that net long positions in 17 commodities have been very elevated. The speed at which liquidation is taking place corroborates our thesis that it is investors not producers or consumers who have been caught being long commodities. China’s business cycle recovery will be U-shaped at best. Domestic orders point to weaker import volumes in the months ahead (Chart 11, top panel). Corporate loan demand has plunged suggesting that liquidity provisions by the PBoC might fail to produce a meaningful recovery in credit growth (Chart 11, bottom panel). Finally, technicals bode ill for commodity prices. As Chart 12 illustrates, copper prices and global material stocks have probably formed medium-term tops, and risks are skewed to the downside. Chart 11China: The Economy Is Struggling To Gain Traction

China: The Economy Is Struggling To Gain Traction

China: The Economy Is Struggling To Gain Traction

Chart 12A Major Top In Commodity Prices?

A Major Top In Commodity Prices?

A Major Top In Commodity Prices?

Bottom Line: Commodity prices and their plays have more downside. Investment Strategy The decline in commodity prices and the relentless US dollar rally will ensure that EM currencies, bonds and stocks continue to sell off even if the US equity market rebounds in the near term driven by lower Treasury yields. Global equity and fixed-income portfolios should continue underweighting EM. We also continue to short the following currencies versus the USD: ZAR, COP, PEN, PLN, PHP and IDR; as well as HUF vs. CZK, and KRW vs. JPY. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Strategic Themes (18 Months And Beyond) Equities Cyclical Recommendations (6-18 Months) Cyclical Recommendations (6-18 Months)

Executive Summary Caught In Risk-Off Selling

Copper Testing Support

Copper Testing Support