Economic Growth

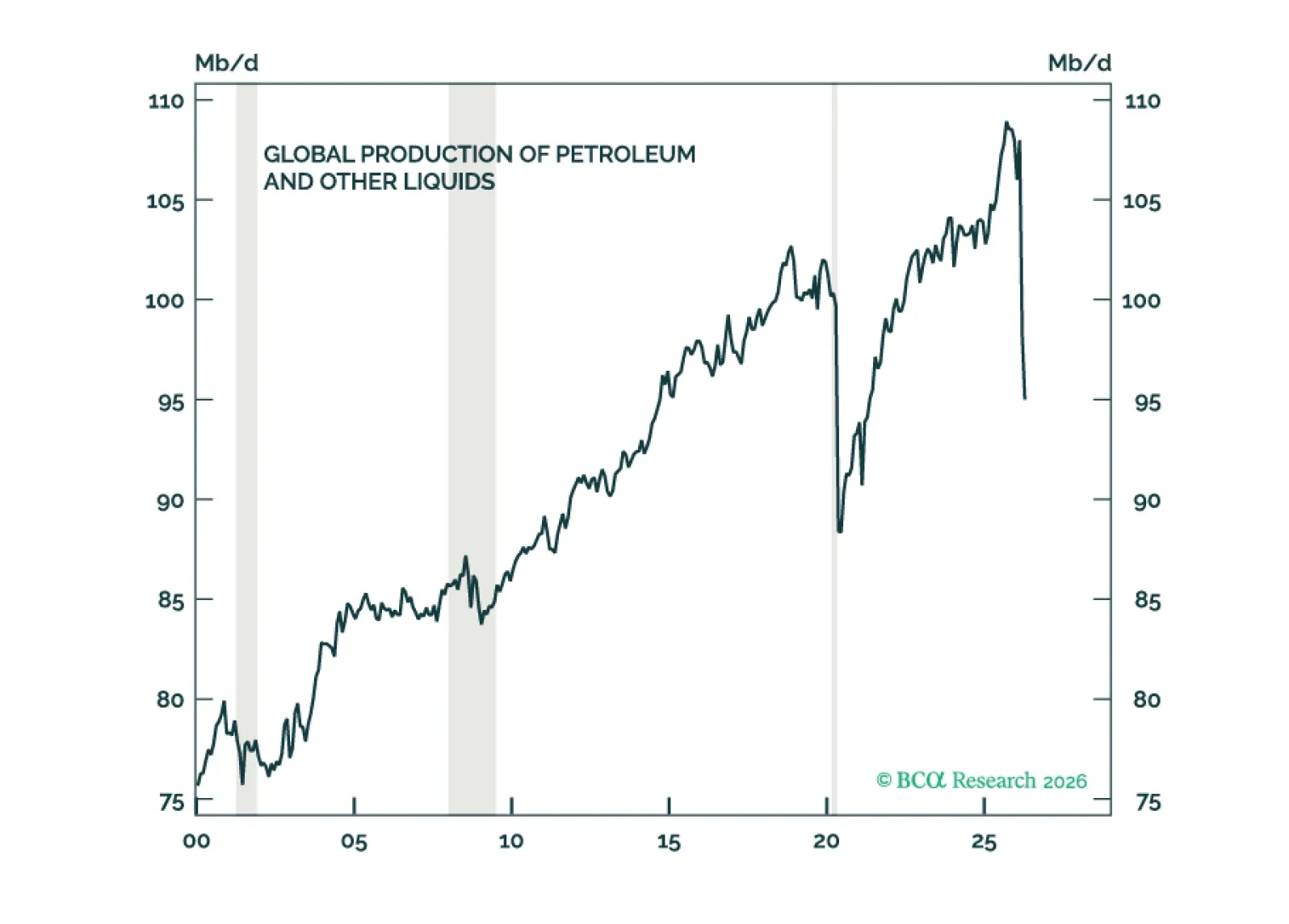

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

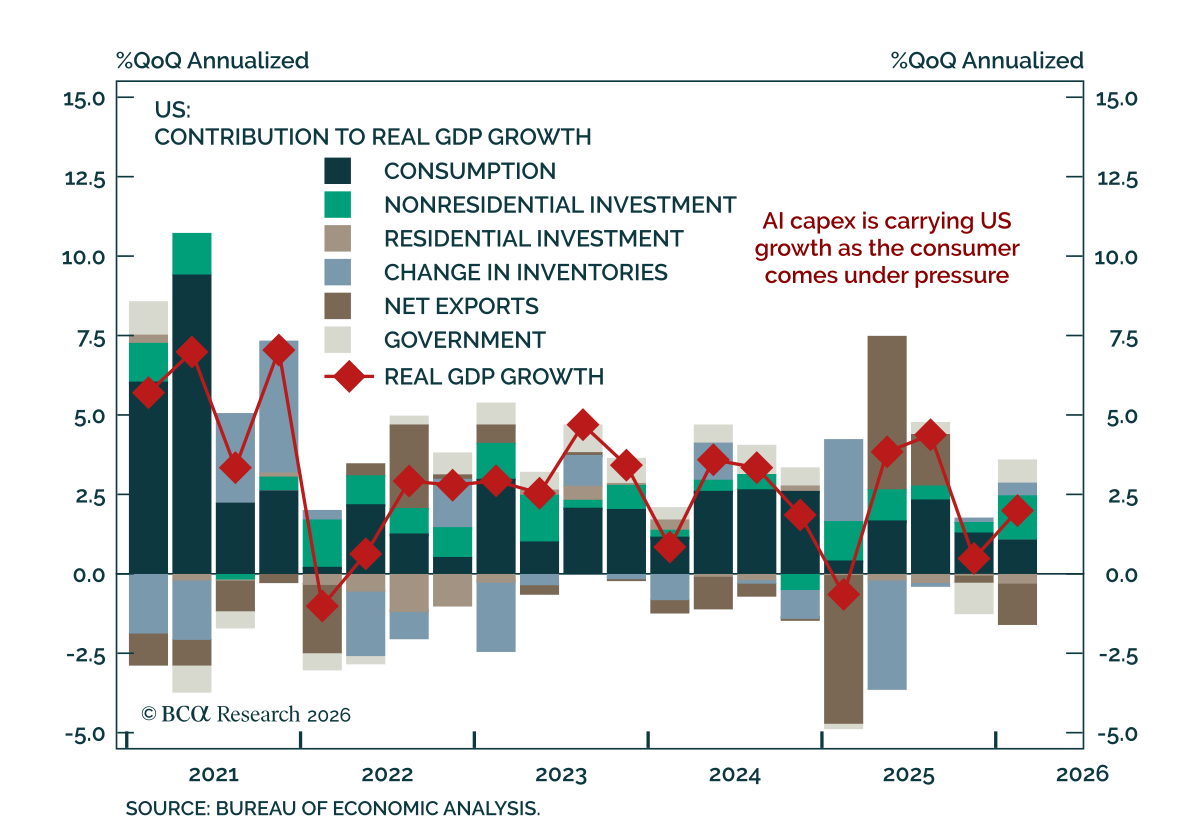

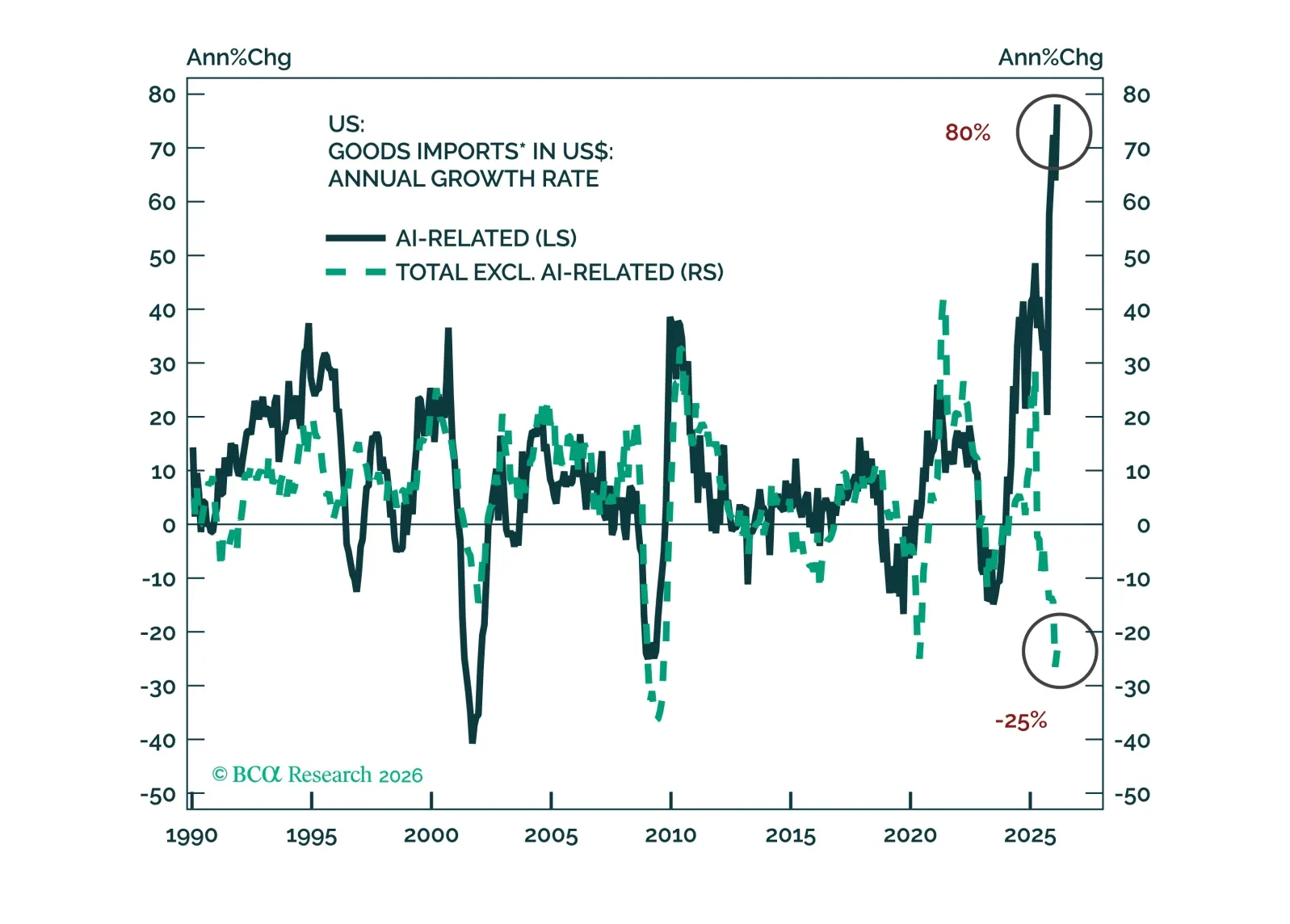

Global trade has held up despite US non-AI import volumes contracting by 25% over the past 12 months. The strength in global trade has concentrated in two areas: (1) imports of AI-related hardware and (2) developing countries’ imports, especially from China. Will these continue?

The relief rally in stocks can continue a while longer. However, much can still go wrong. As such, we are retaining a 12-month underweight to stocks but are moving to neutral on a short-term tactical horizon.

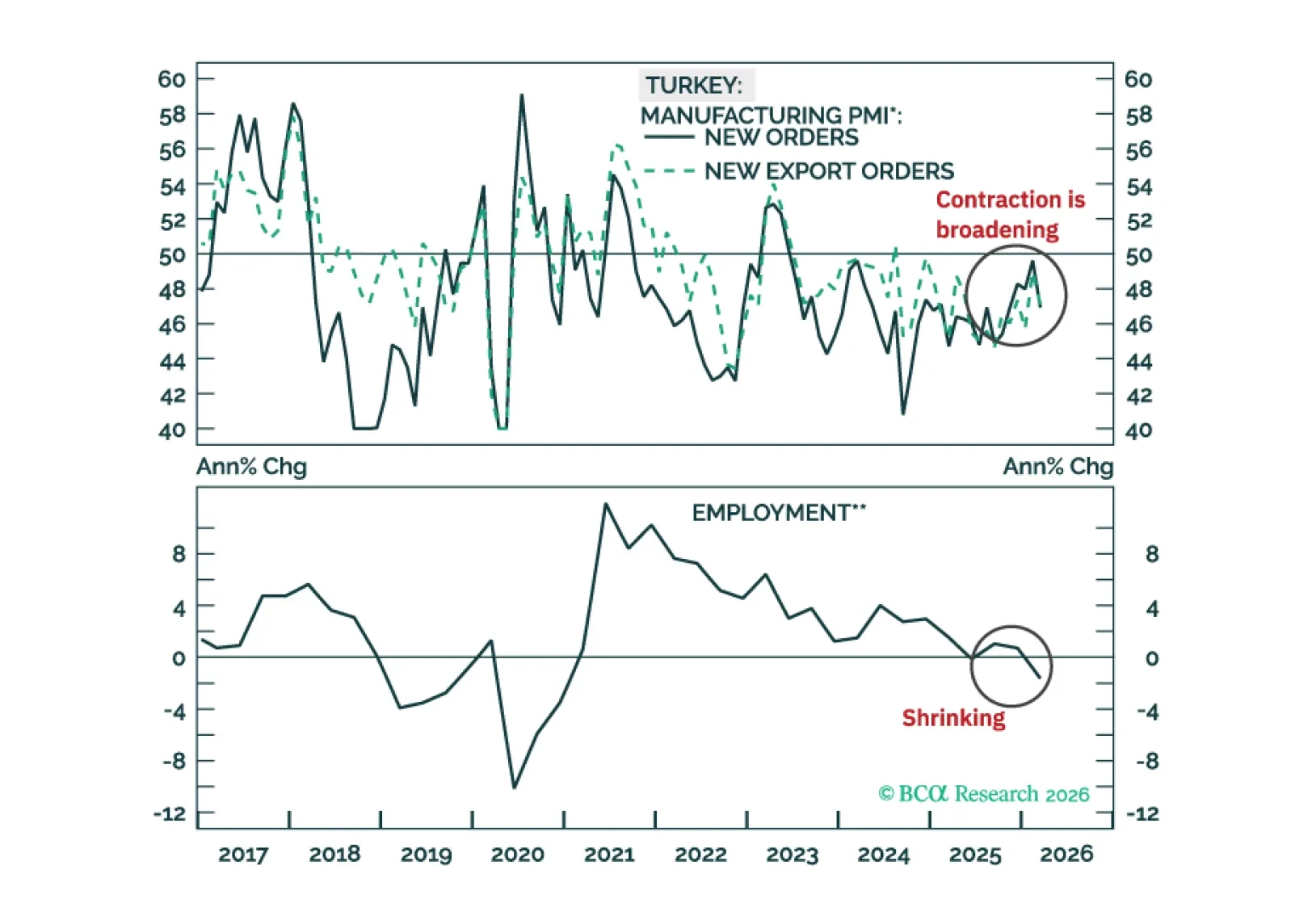

The Turkish financial markets will struggle in the very near term, but beyond that, the cyclical disinflation process will resume. Fixed-income investors should put Turkish 2-year local currencybonds on a ‘buy’ watch list.

We introduce our Macro Regime Indicators (MRI), a framework for forecasting growth and inflation surprises in the US. The MRI on the economy shows no substantial mispricing in either growth or inflation over the next 12 months.

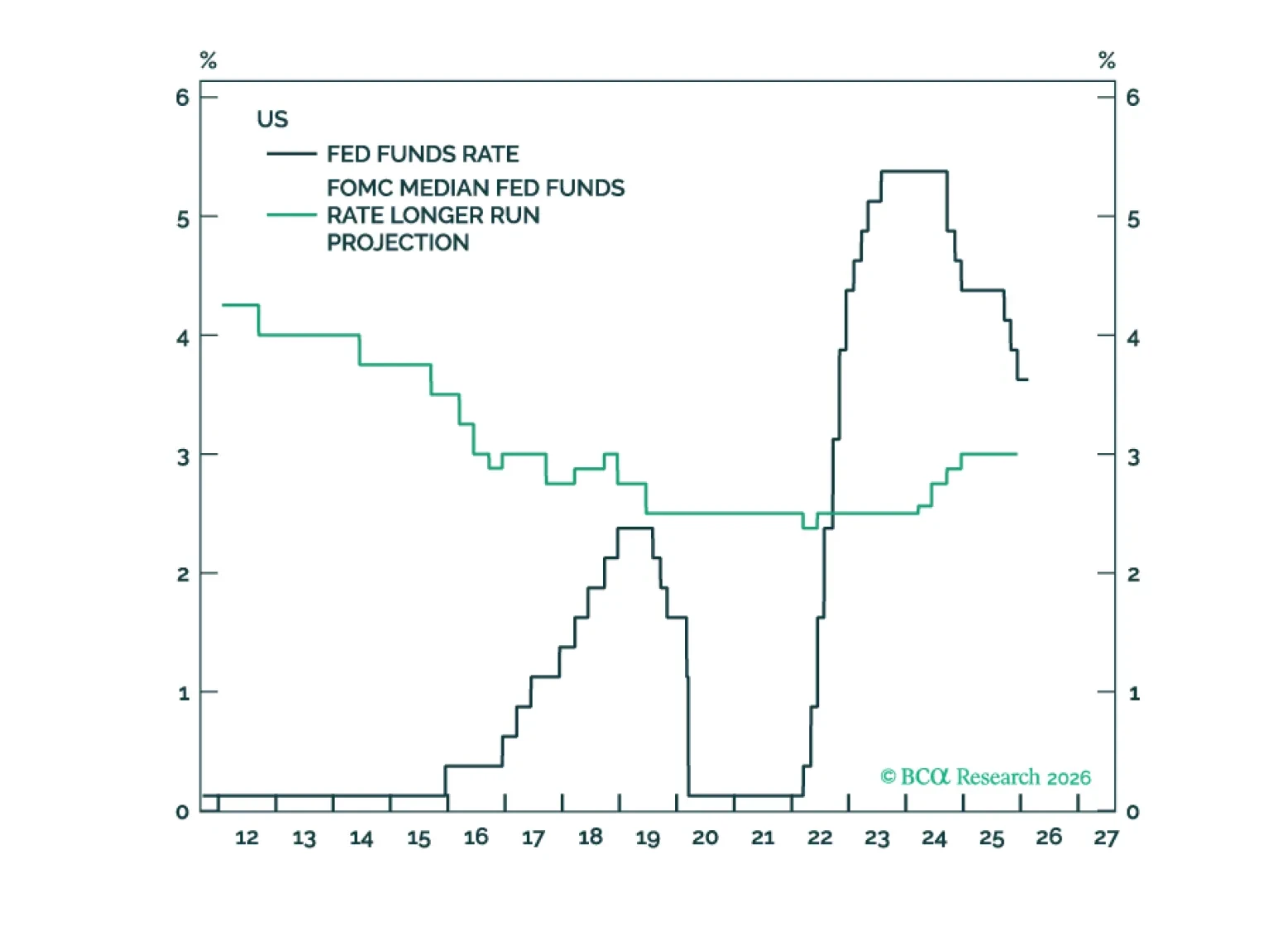

The neutral rate in the US is being propped up by a variety of forces that are at risk of reversing. These include the AI capex boom, large budget deficits, and the extraordinarily high level of household wealth. As such, interest rates are likely to surprise to the downside over the next few years.