Domestic Politics

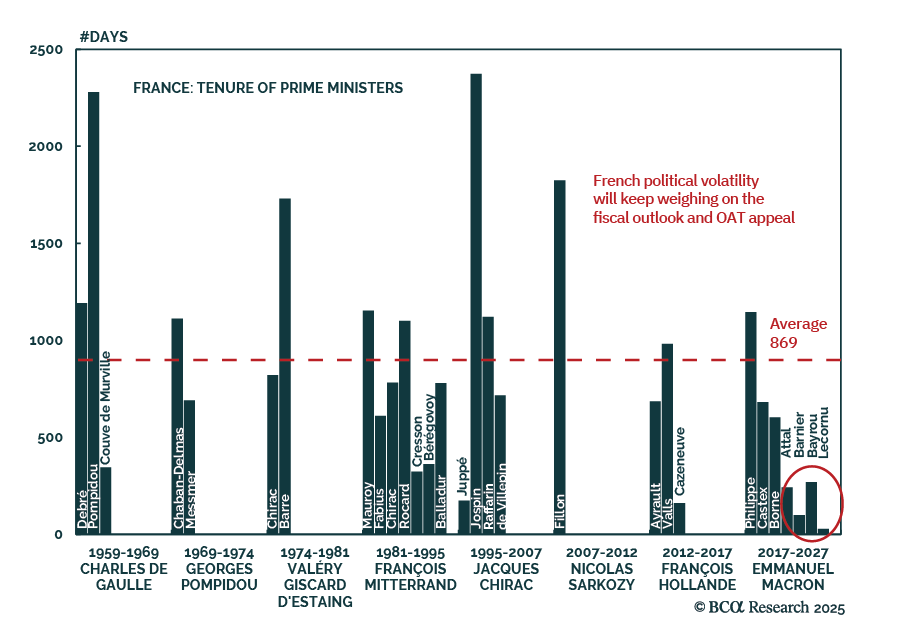

French markets woke up Monday to fresh political turmoil, with Prime Minister Sébastien Lecornu resigning just 27 days into office, marking the shortest tenure in modern French history. The CAC 40 dropped over 2%, the euro slid 0.7% against the dollar, and…

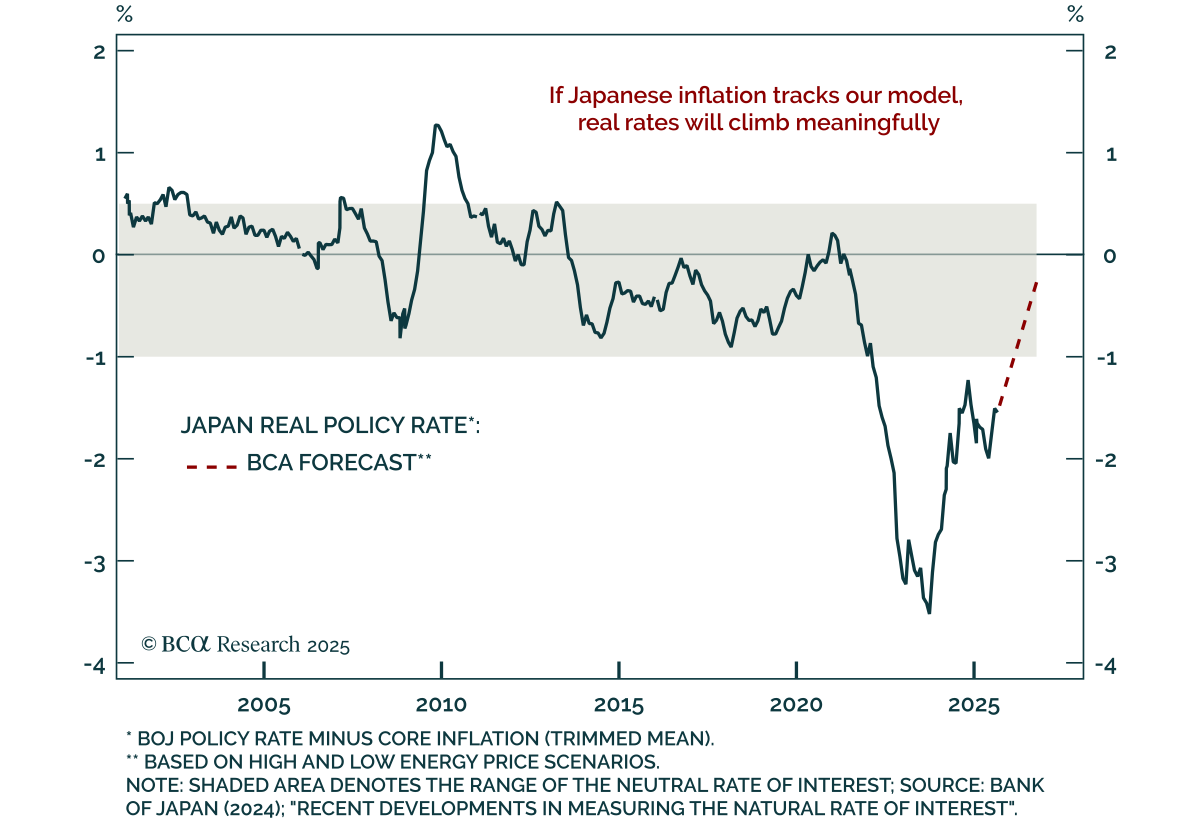

Japanese markets reacted sharply to Sanae Takaichi’s election as the leader of the ruling Liberal Democratic Party and the frontrunner to become Japan’s next Prime Minister. The Nikkei surged 4.8% and the yen plunged nearly 2% across major pairs. Seen as a…

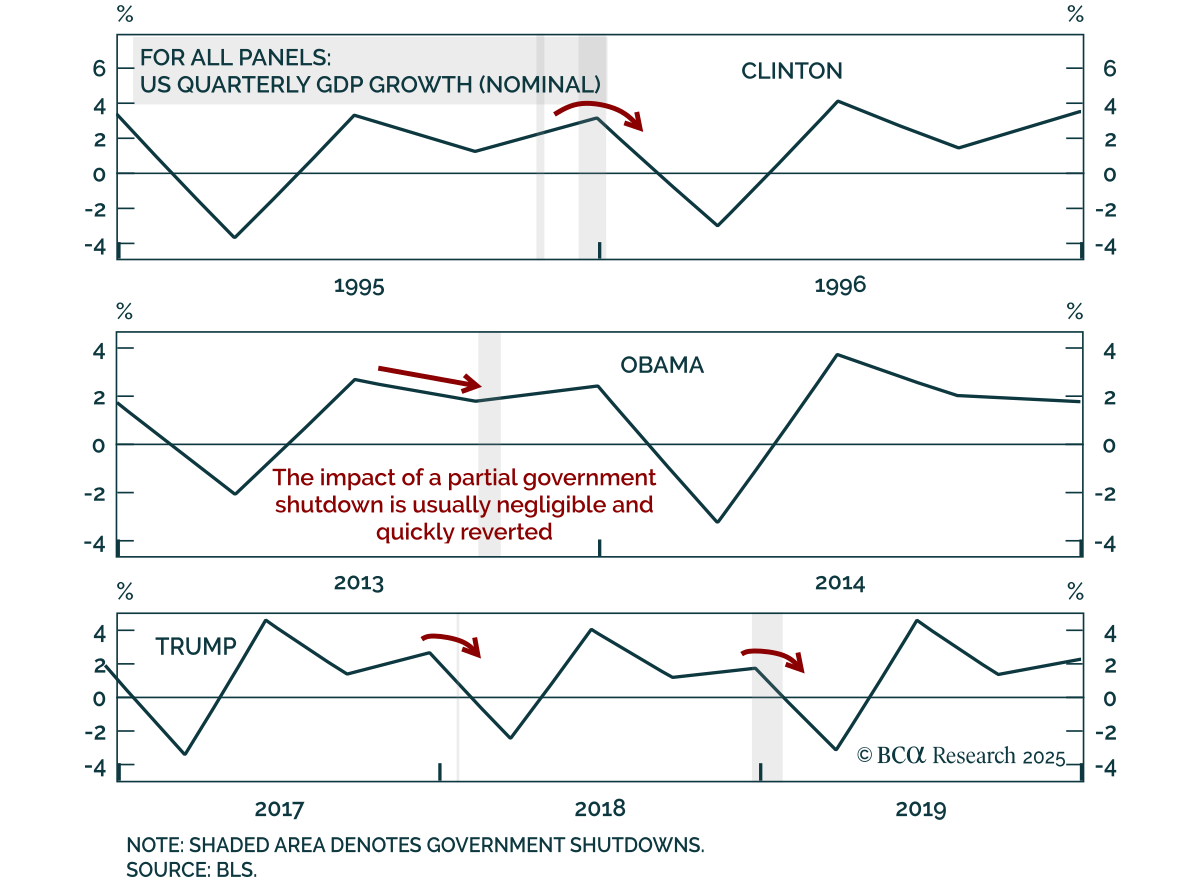

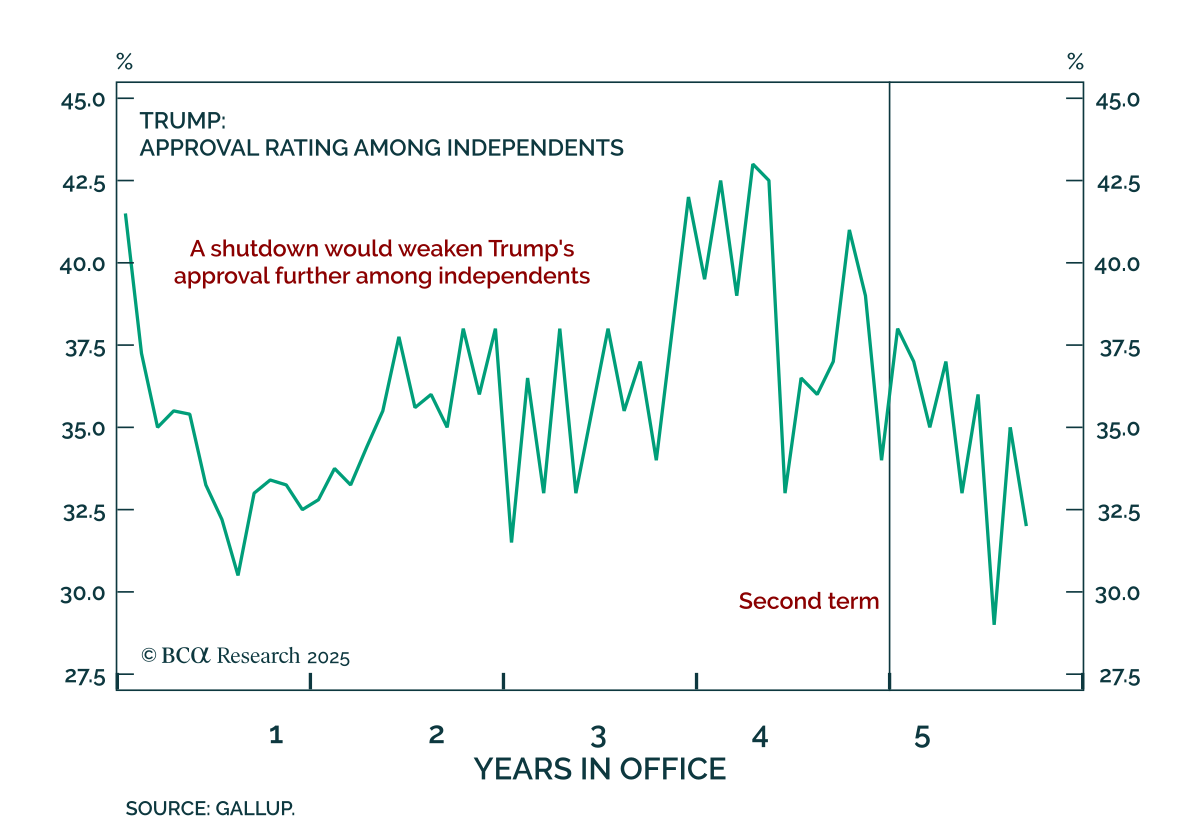

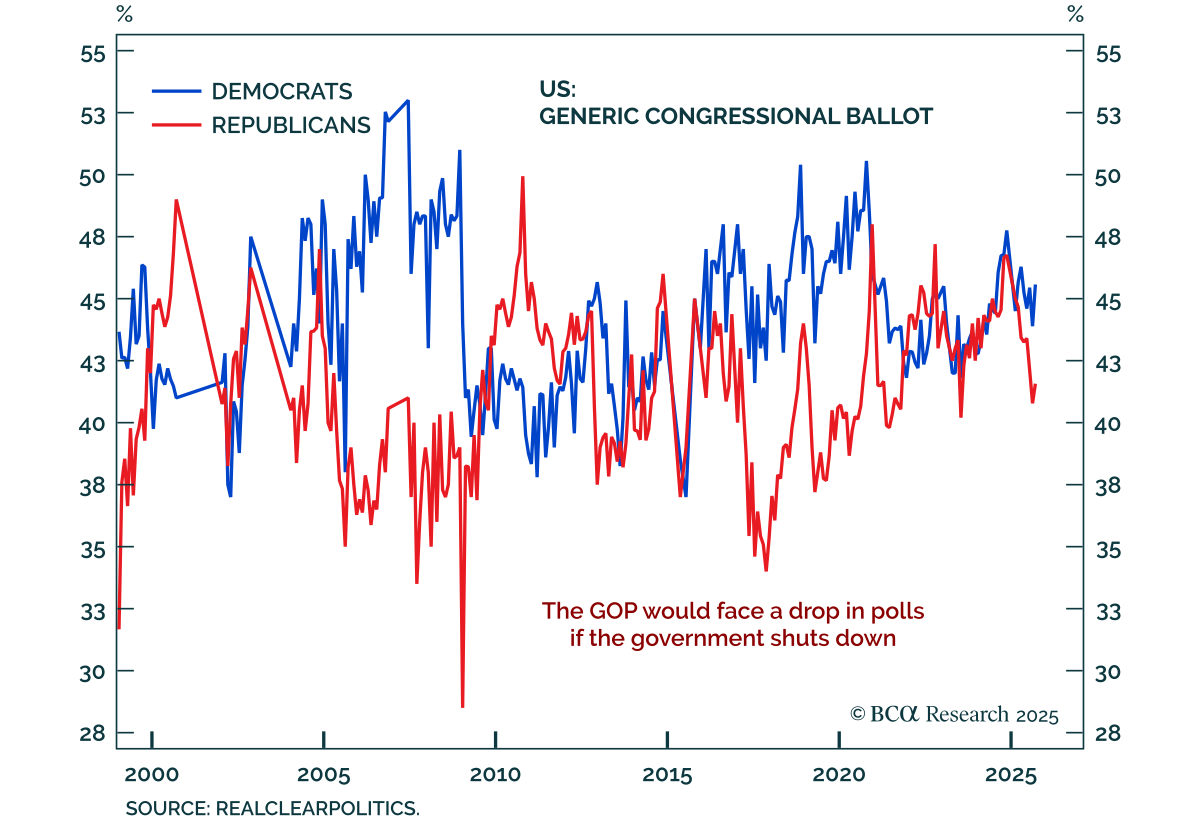

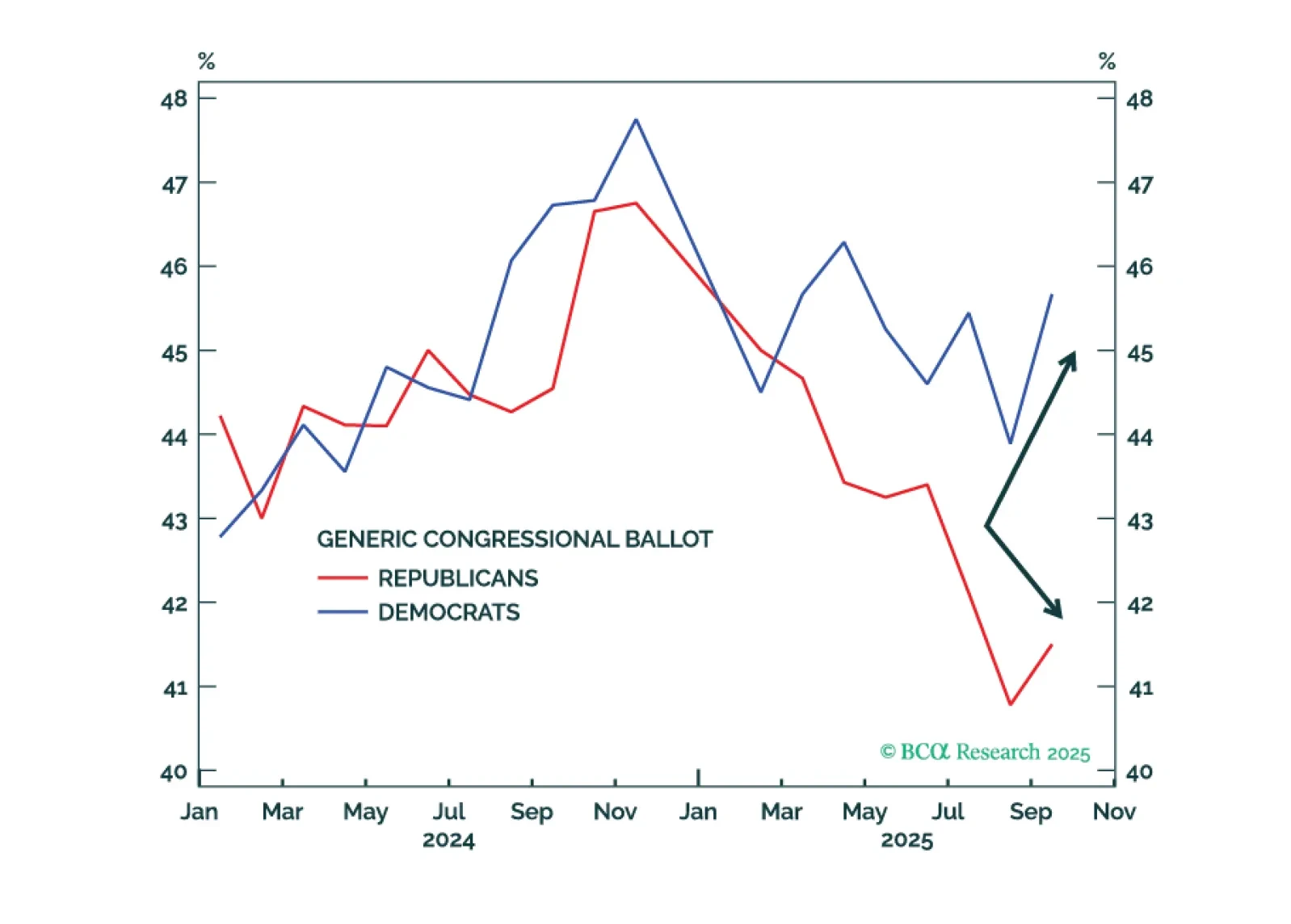

Our US and Geopolitical strategists see 50% odds of a shutdown that lasts beyond three weeks. Investors continue to wonder whether the US federal government shutdown will last long enough, or involve large enough layoffs, to affect the underlying…

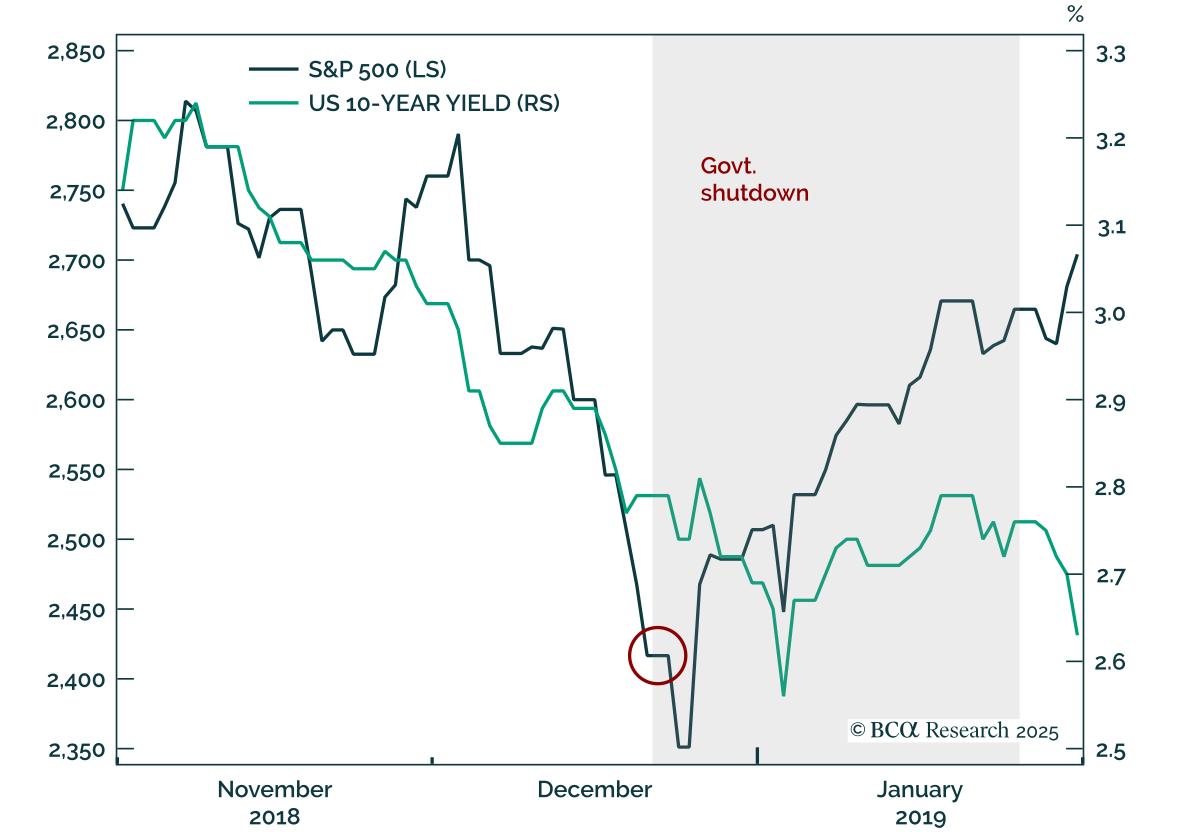

The October 1 partial US government shutdown risks denting near-term GDP and sentiment but should present a buying opportunity if it triggers equity weakness. The US federal government partly shutdown on October 1 after the Republican-held Senate failed to…

President Trump said a partial federal government shutdown is "probably likely" late in the afternoon on September 30. Senators have until midnight to pass a continuing resolution already passed by the House that would keep the government operating until…

Will the US federal government shutdown on October 1? Congressional leaders are meeting with President Trump in the White House as we go to press. If eight Democratic senators do not vote with Republicans to pass a no-frills "continuing resolution" by…

We give a one-third probability of a federal government shutdown. It probably will not happen before November. At worst, government shutdowns only cause temporary market volatility.

Our US Political Strategists give a one-third probability of a federal government shutdown before November. The odds could increase after that. But the market impacts are limited. The source of the disagreement is the enhanced subsidy for health care under…

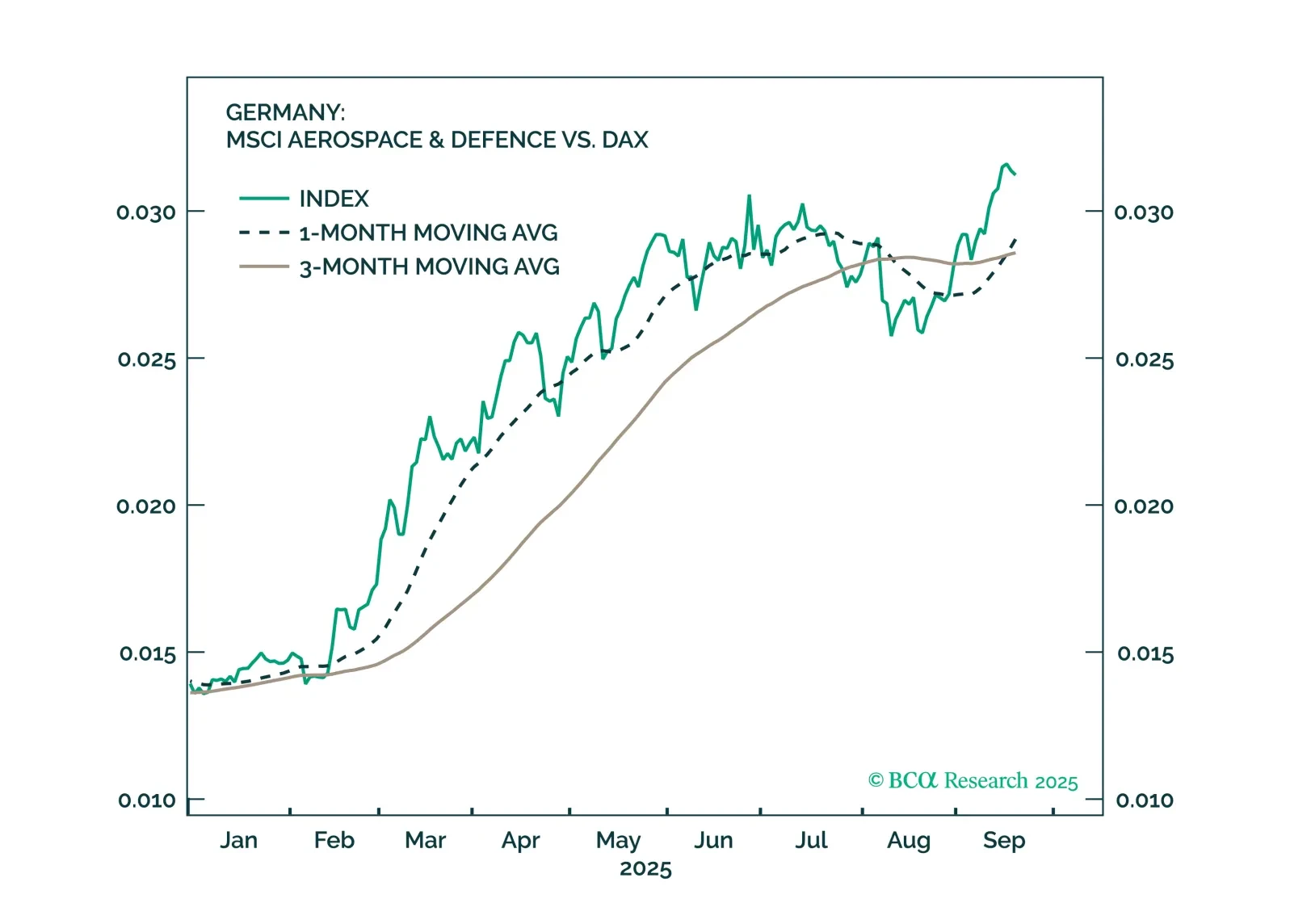

Germany is moving forward with implementing the large fiscal and defence spending announced earlier this year. Fiscal reforms are also positive, though they will fall short of expectations.

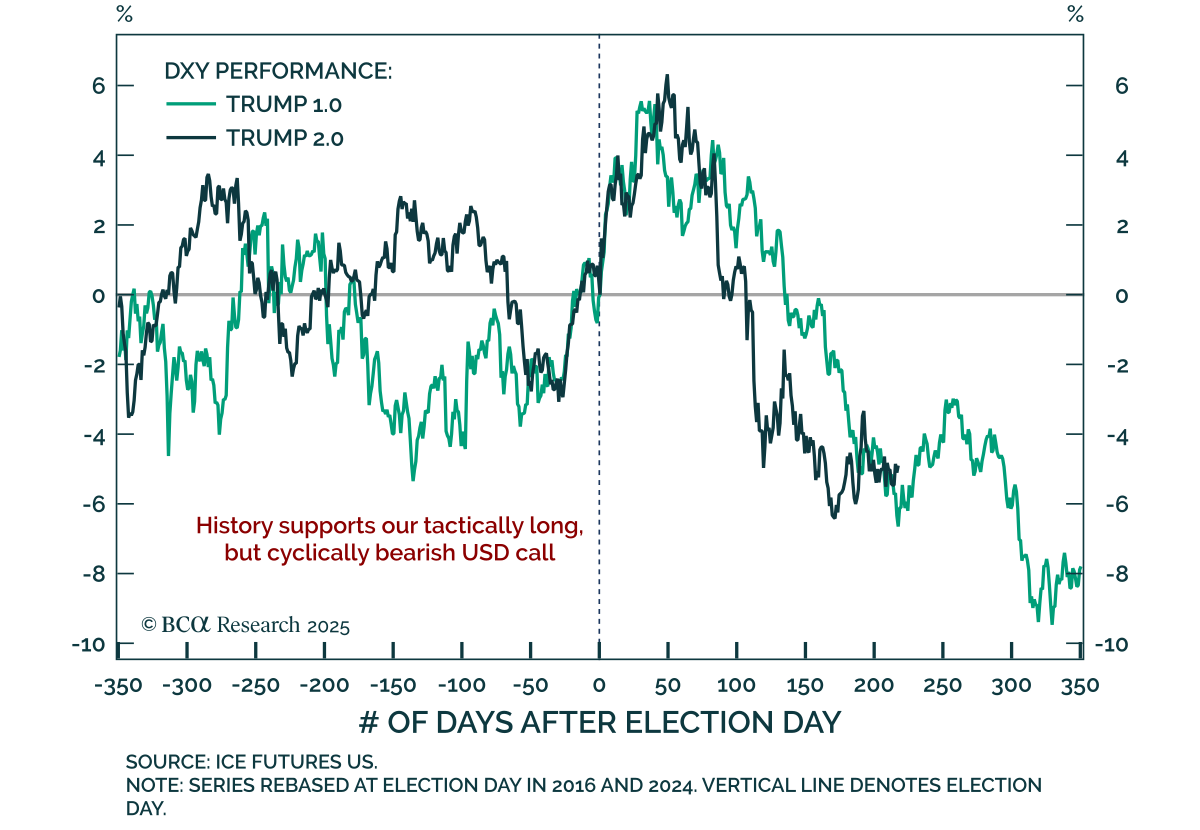

Trump-era policy patterns are reappearing in FX, supporting a temporary bounce in the dollar. Our Chart Of The Week comes from Chester Ntonifor, FX Solutions and Special Reports strategist.Chester updated his “KISS” (Keep It Simple & Stupid) chart, which…