Domestic Politics

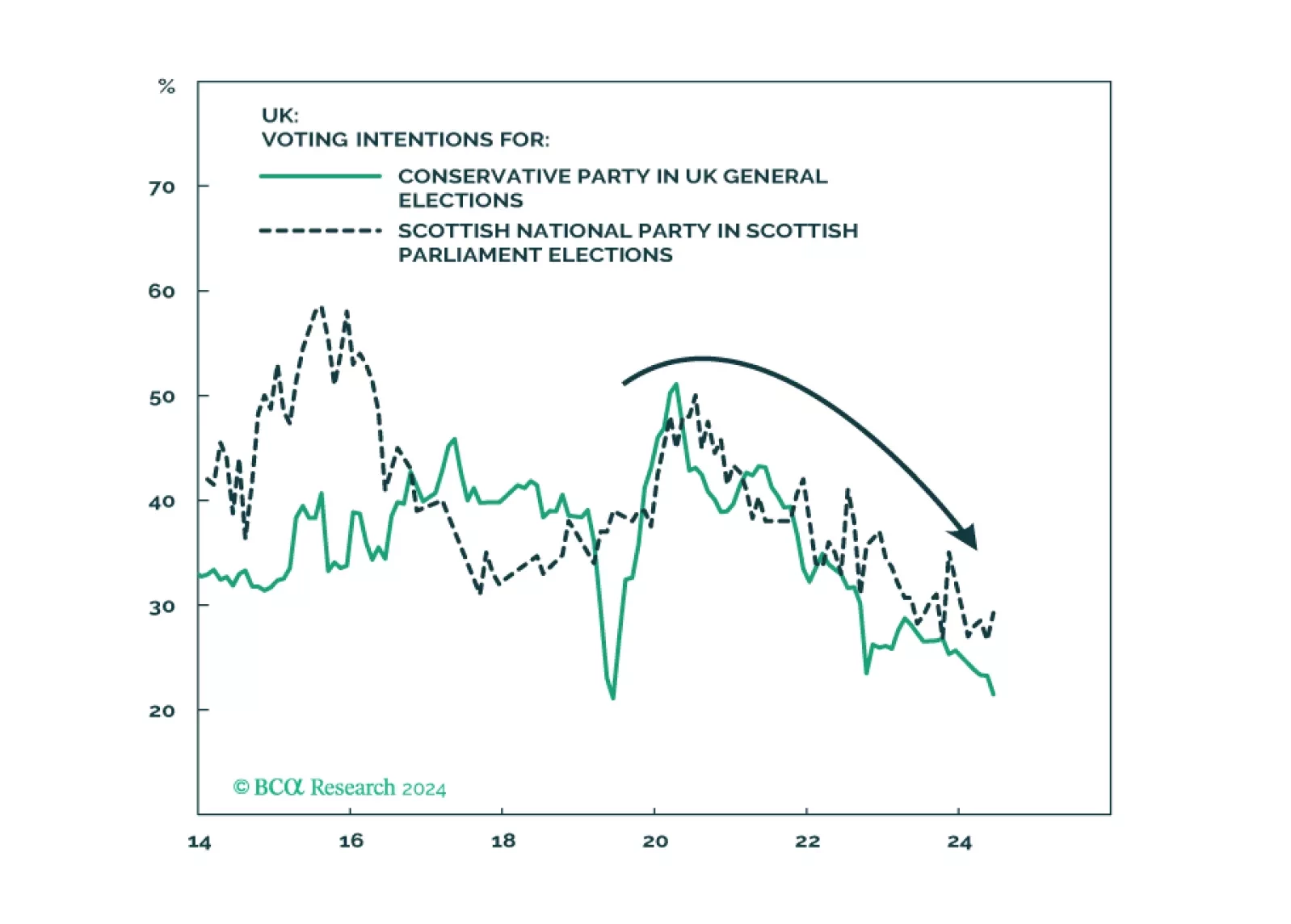

The Labour Party’s comeback in the UK is widely expected and will lead to fiscal stimulus consisting of increased public spending with minimal tax hikes. But a sweeping single-party majority will reduce social unrest only at the cost of higher taxes over the medium term. The paradigm has shifted away from the Thatcherite low-tax regime of the now-discredited Tories. v

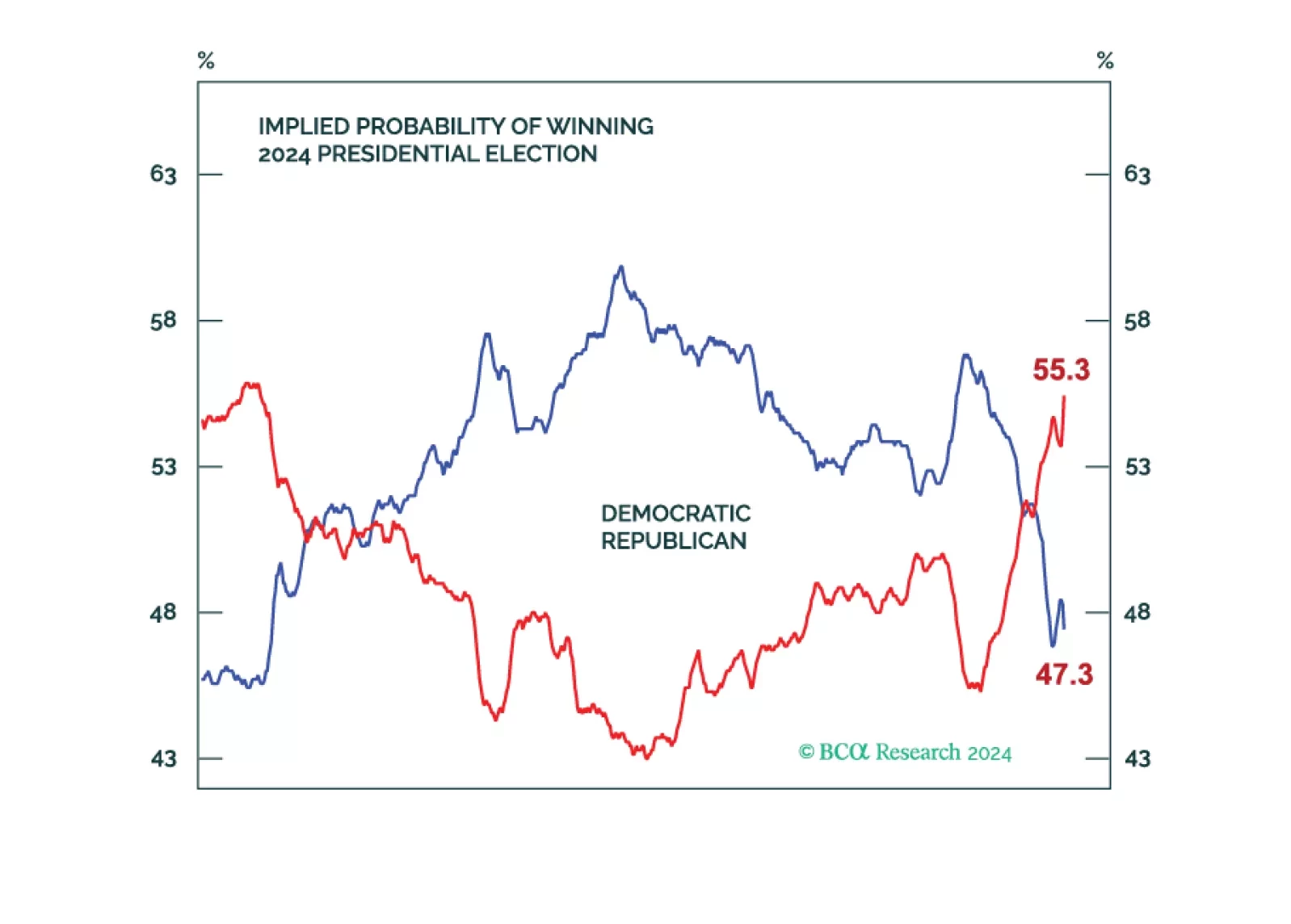

The bond market should sell off and drag stocks down on higher odds of a single-party sweep, policy uncertainty, unorthodox Trump presidency, aggressive tariffs, large tax cuts, large budget deficits, labor shortages, a fired Fed chair, and higher inflation.

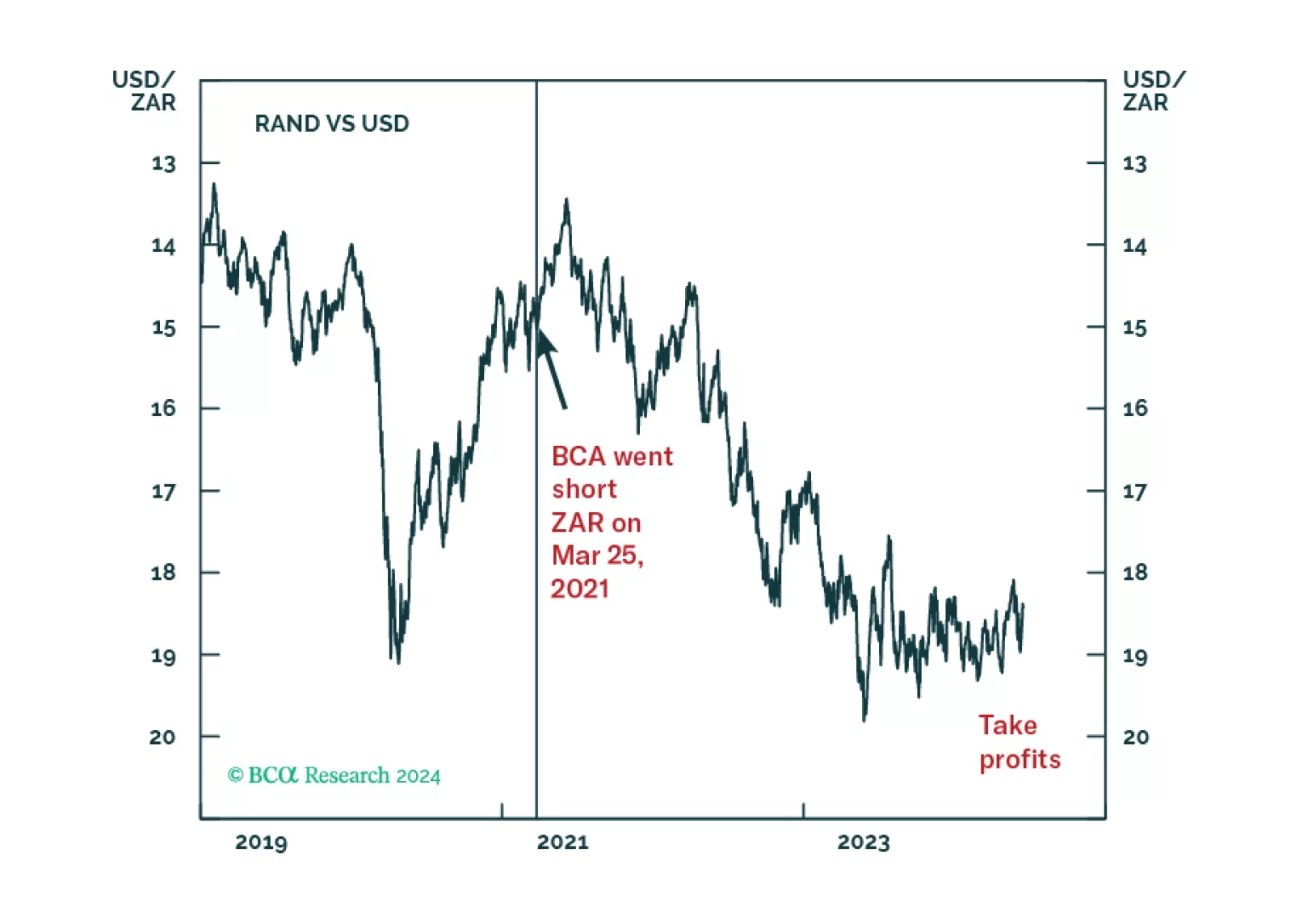

The new national unity government in South Africa creates a geopolitical opportunity that investors should not bet against in the short term. A broad-based rally is likely to unfold relative to other emerging markets. However, structural problems and distrust within the new coalition hold out significant risks over the long run.

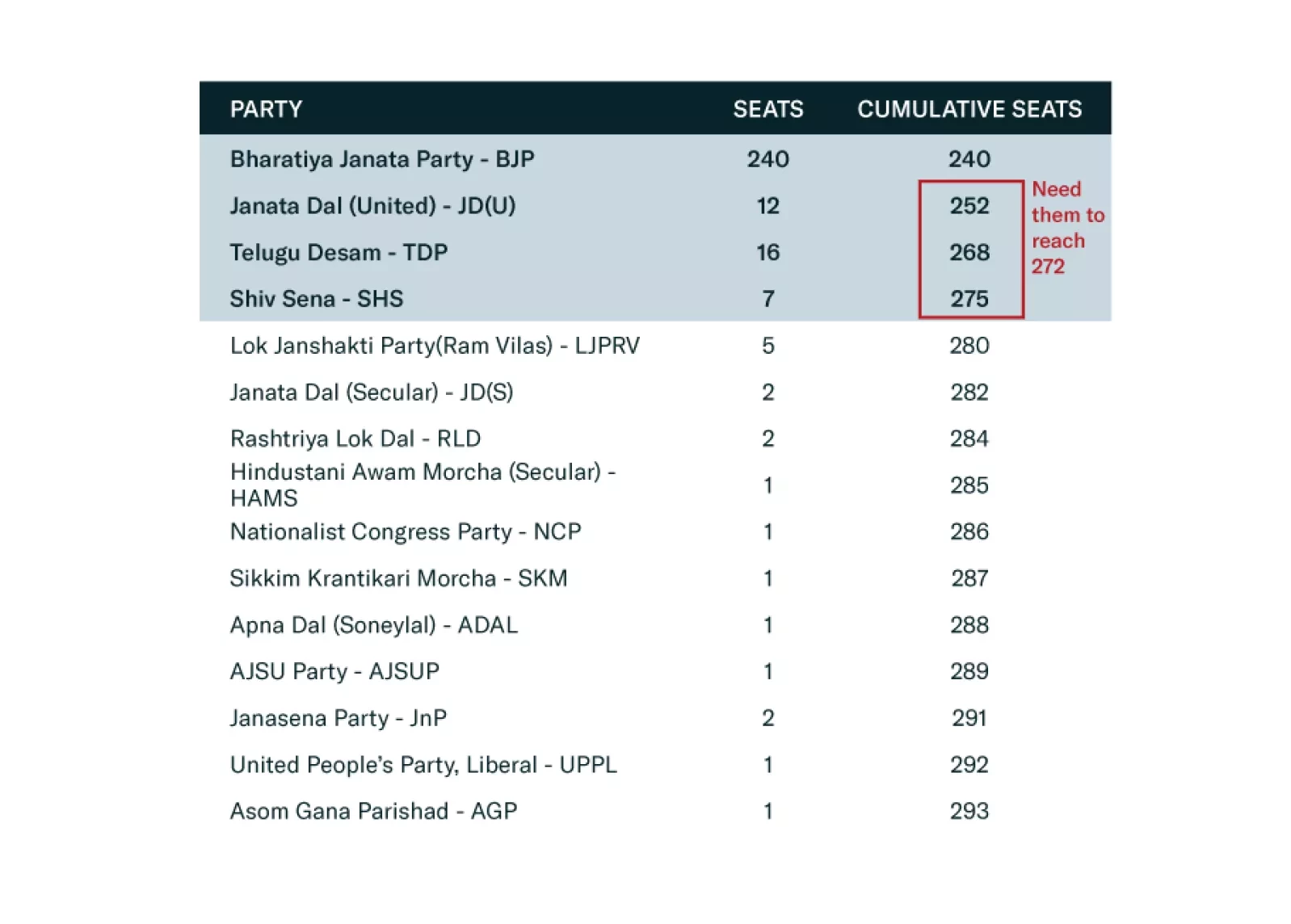

Prime Minister Narendra Modi won a third term and will become the third longest-serving prime minister of India. While investors responded negatively to the BJP’s loss of an outright majority, Modi and the NDA will continue to perpetuate the reforms they have already put into motion. The result also affirms that Indian democracy continues to thrive, contrary to the narrative that Modi had formed an authoritarian grip on the country, a view we always rejected.