Disasters/Disease

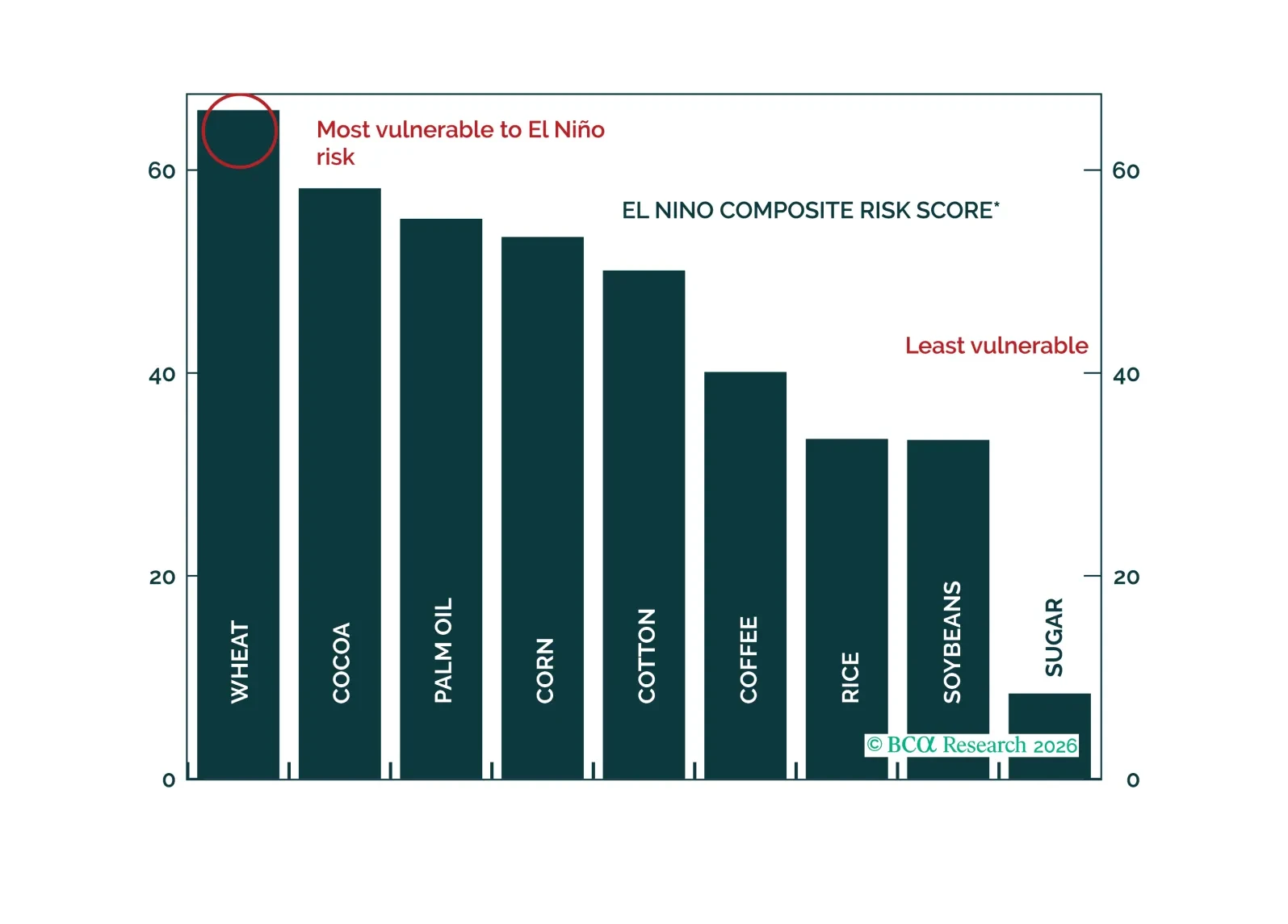

The risk of a “super El Niño” represents a meaningful threat to agricultural markets. Wheat, cocoa, and palm oil appear particularly vulnerable to El Niño-related supply disruptions.

A rise in food prices could also generate political — and potentially geopolitical — reverberations across frontier and emerging markets, where food prices are far more relevant than in developed economies.

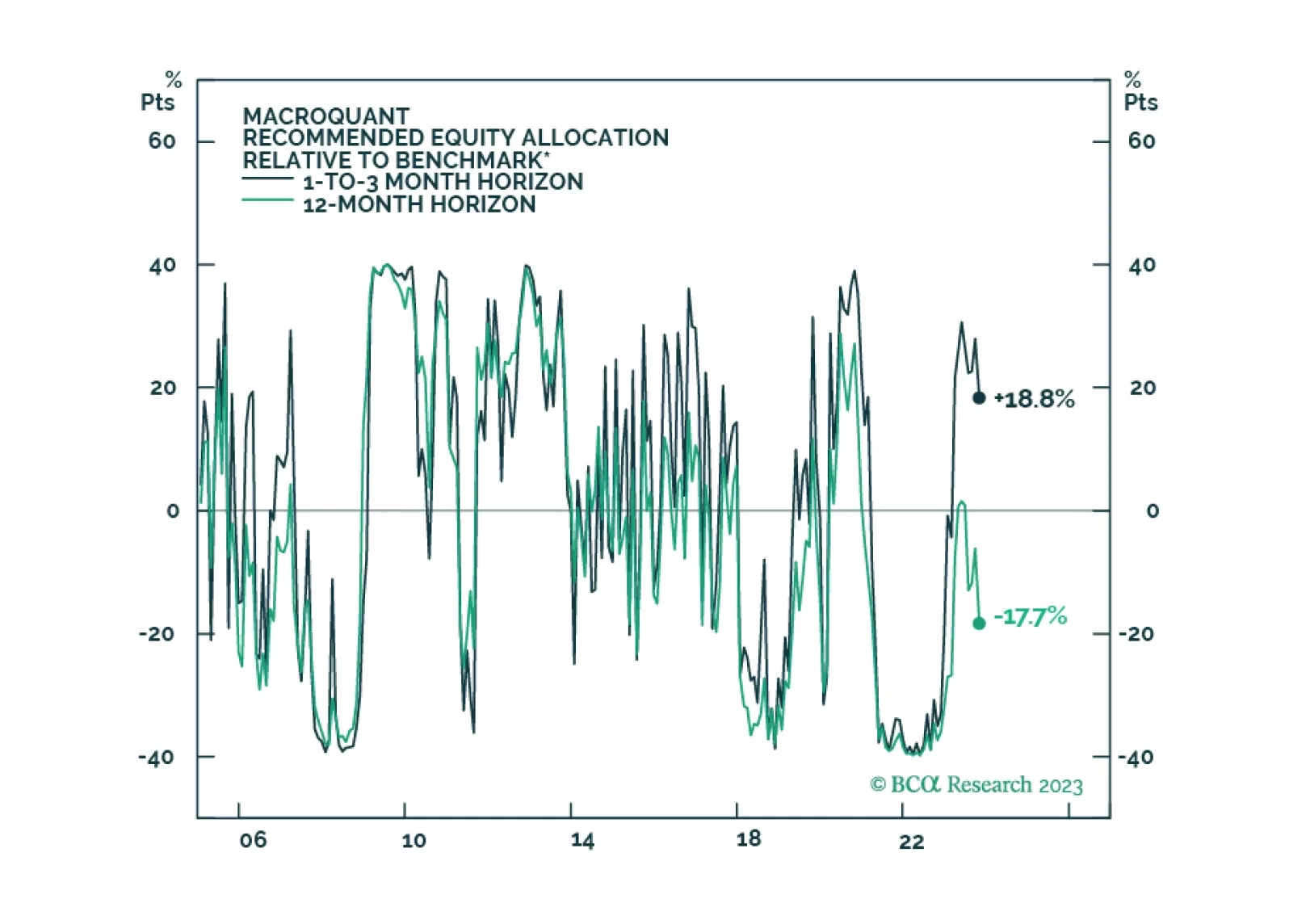

We are approaching another phase transition from boom to bust. Stocks should rally into year-end, but investors should look to reduce equity exposure early next year while increasing bond exposure.

President Erdogan and the Justice and Development Party emerged as the winner of the Turkish general election which was concluded yesterday. This victory means that their expansive policies of the past decade will continue, and Turkish assets will suffer. Across the Aegean, the Greeks voted to reelect the New Democrats under the leadership of Prime Minister Mitsotakis. Their fiscal prudence and structural reforms will be continued as voters had rewarded them with another term in office. Go long Greek versus Turkish equities.

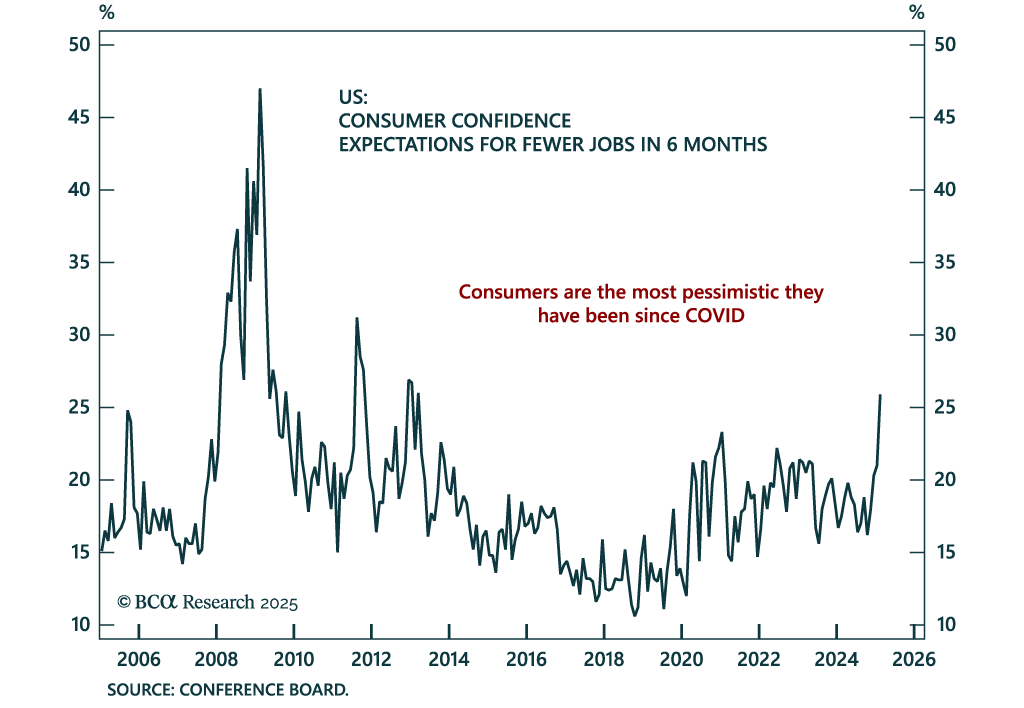

This week’s <i>Special Report</i>, written by Miroslav Aradski, highlights the worrisome deterioration in health trends in the US, which began before the pandemic. Over the long haul, this could weigh on labor supply and productivity, put upward pressure on bond yields, and hurt equity multiples.