Diplomacy/Foreign Relations

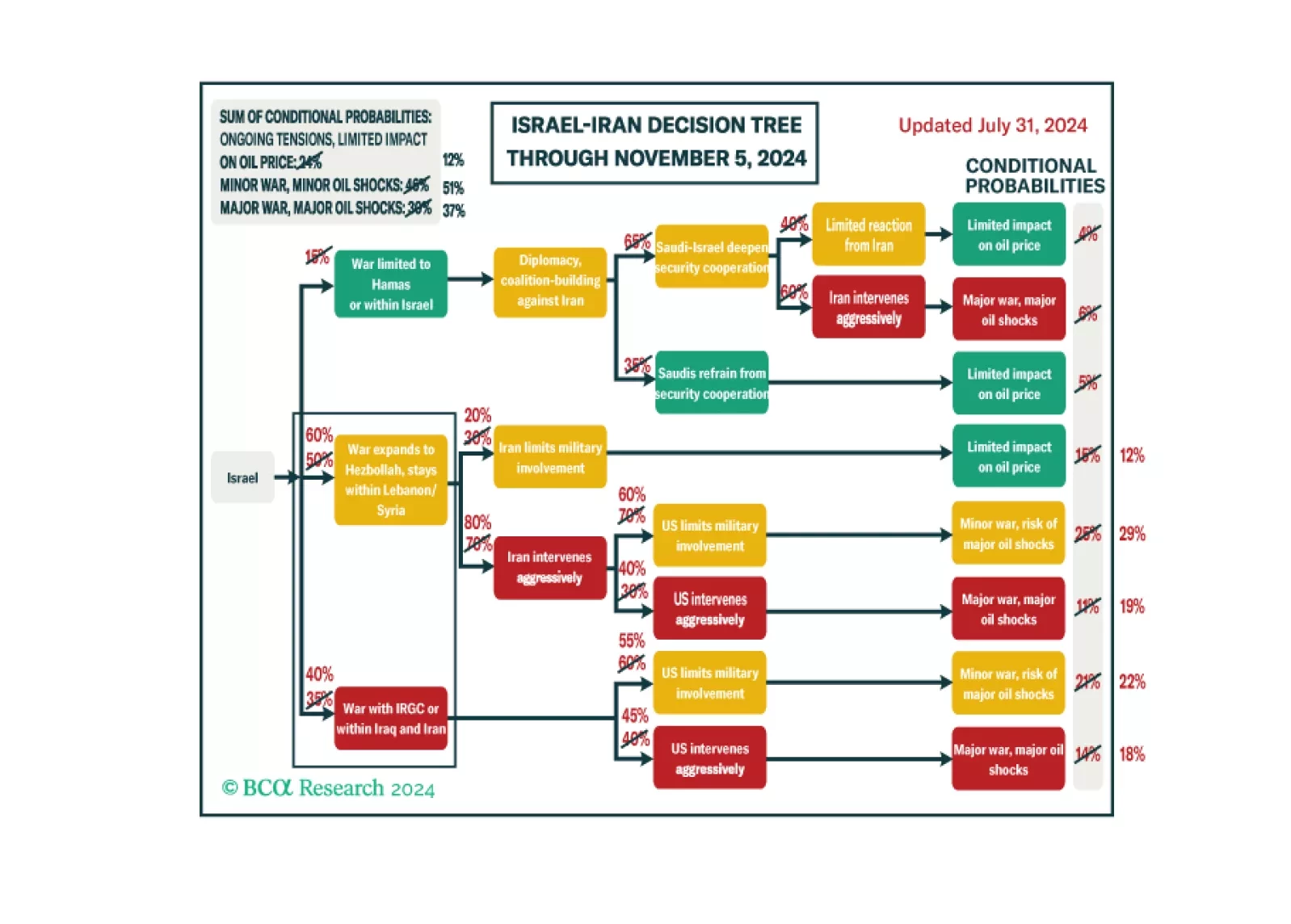

The war in the Middle East is expanding, upgrading our subjective odds of a major oil supply shock to 37% and underscoring our 60% odds of Republican victory in November. Volatility should spike again as investors contemplate the prospect of rising oil prices amid slowing US and global growth. Tactically investors should stay overweight energy stocks relative to other cyclicals and favor oil producers in the Americas rather than Middle East.

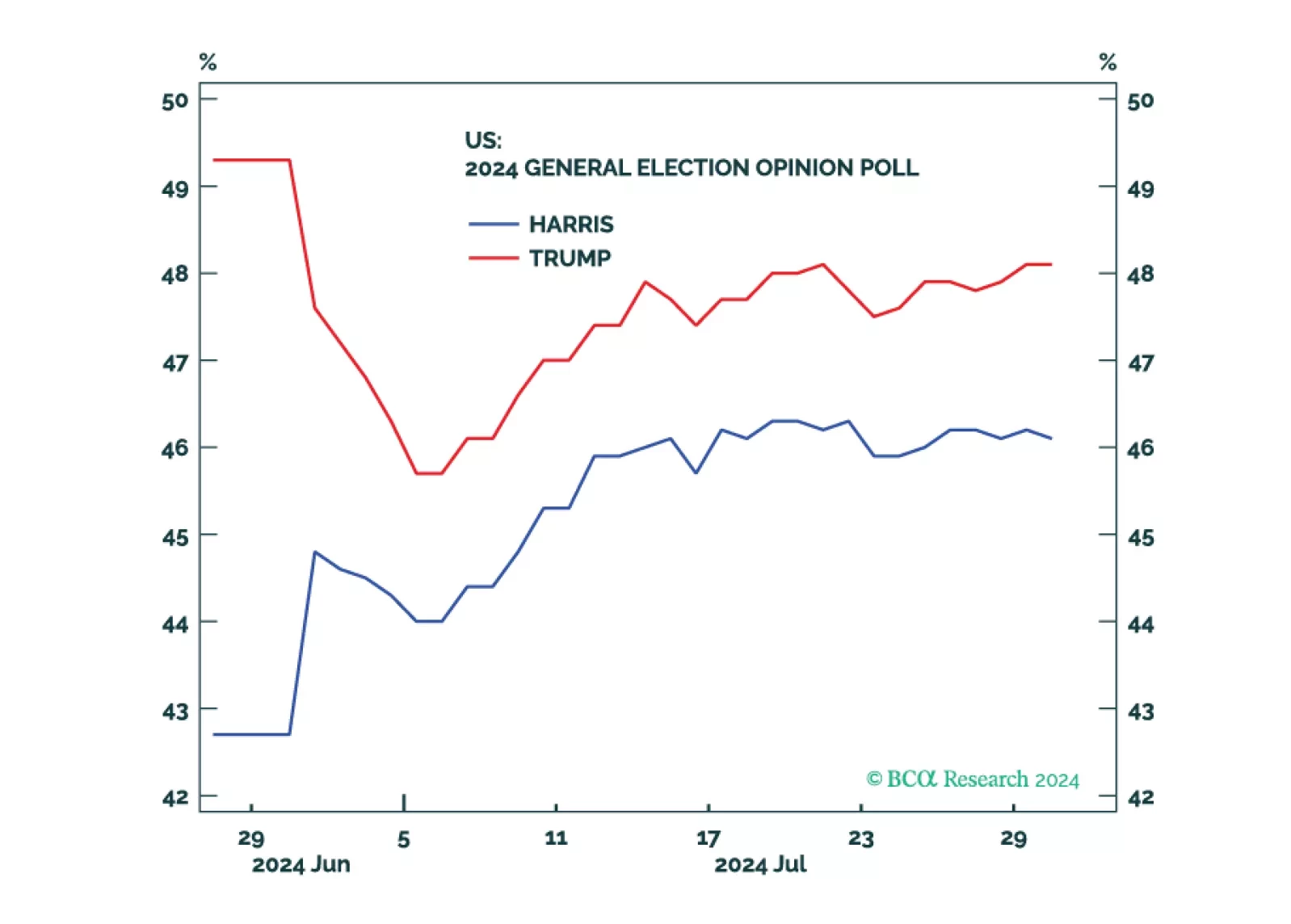

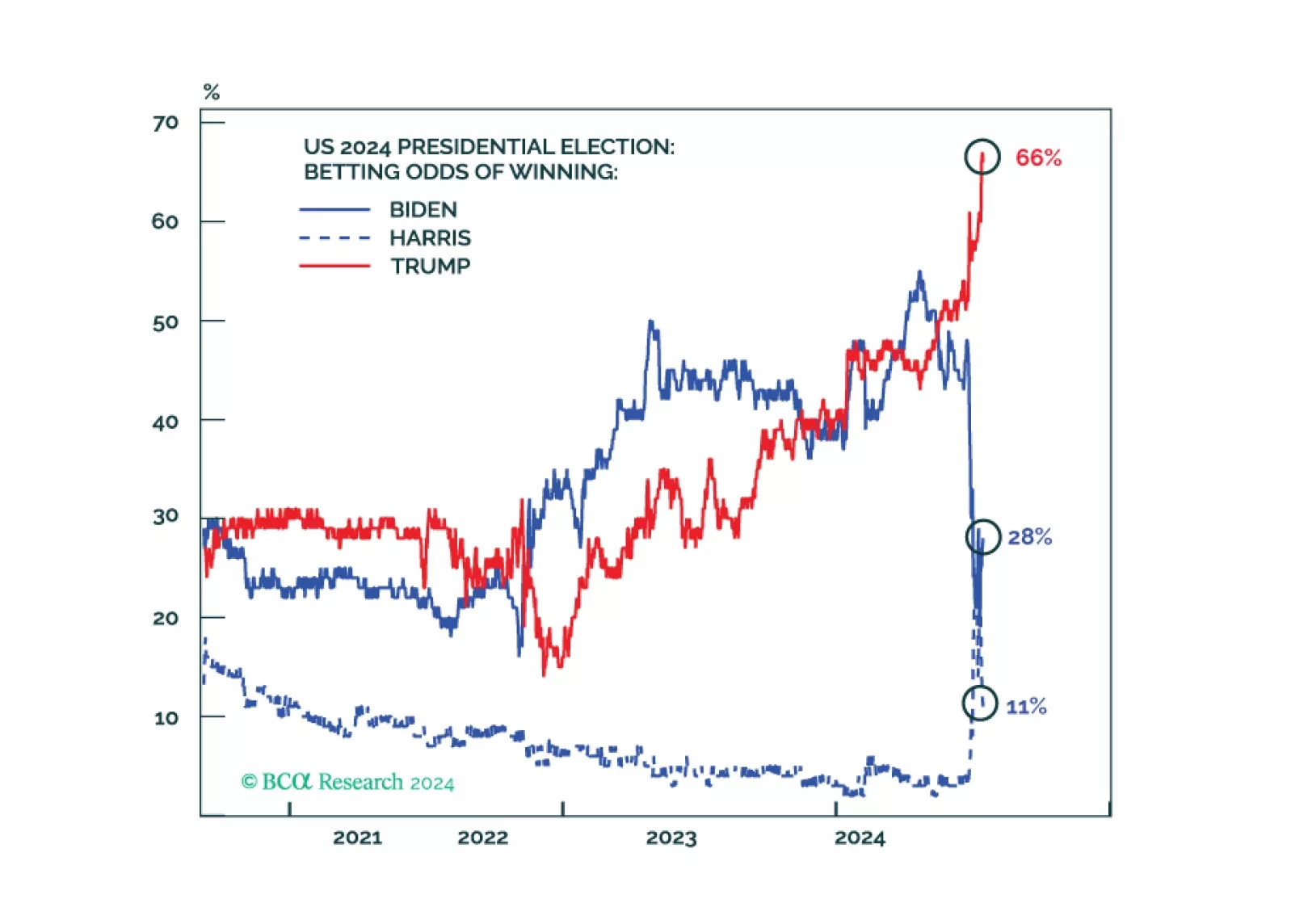

Republicans are favored but the election is still competitive. Equities, corporate credit, and cyclical sectors will fall until policy uncertainty is reduced.

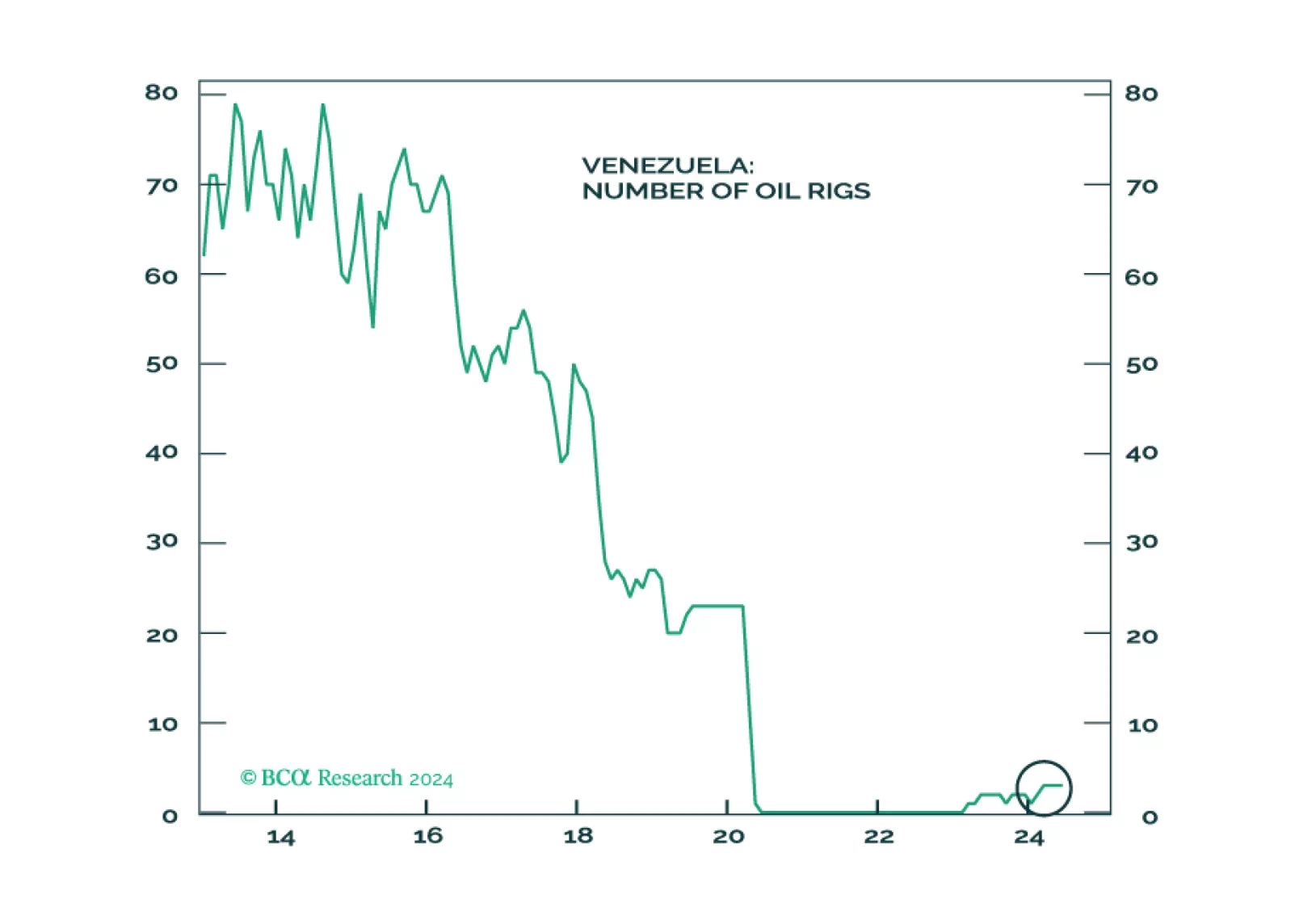

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.

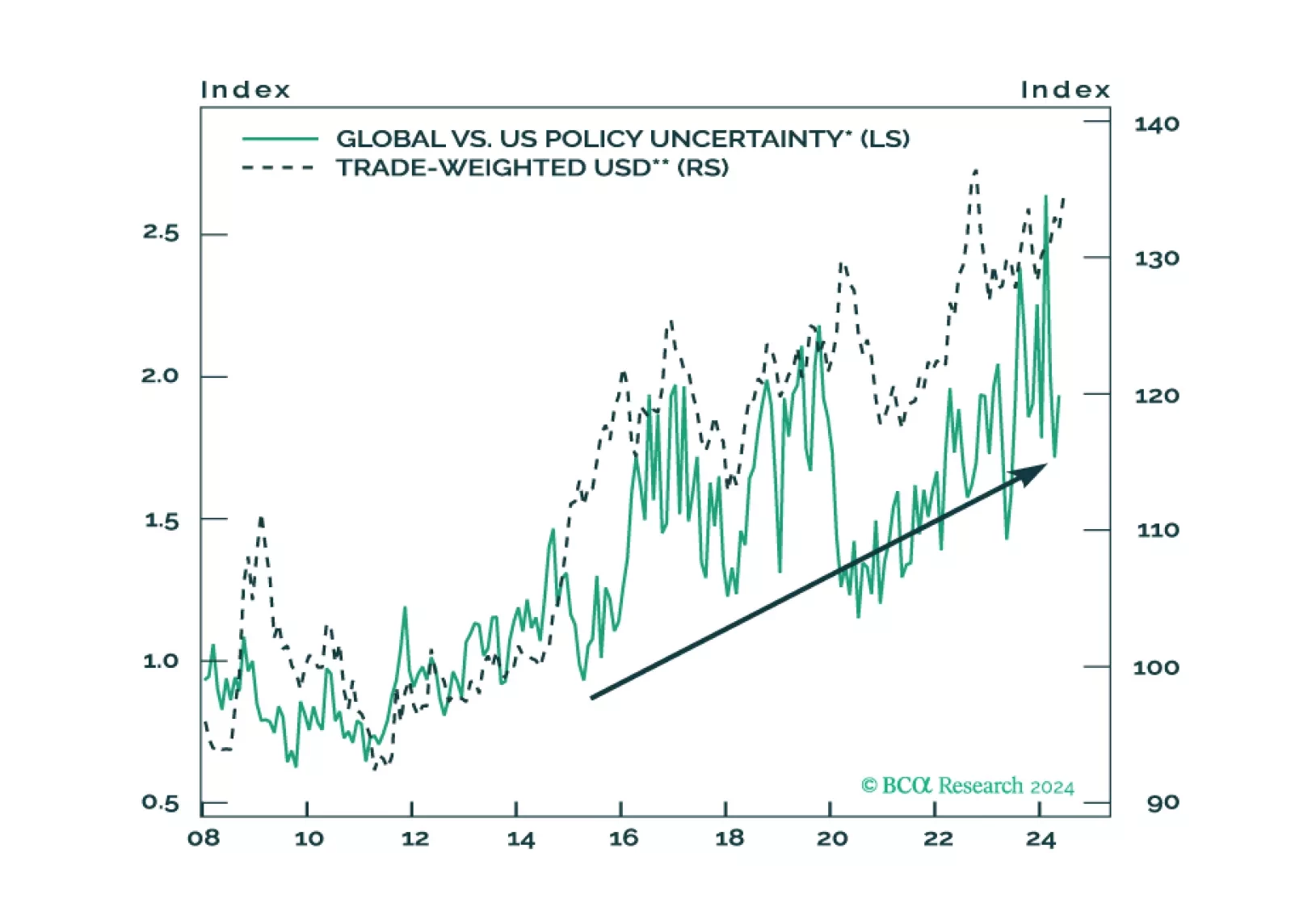

Investors should overweight US assets and de-risk their portfolios in anticipation of a major increase in policy uncertainty and geopolitical risk surrounding the US election and its global ramifications.

The cyclical economy is slowing today. Republicans are now more likely to win a full sweep, crack down on immigration and trade, and at least modestly stimulate the economy. Uncertainty and volatility will rise.

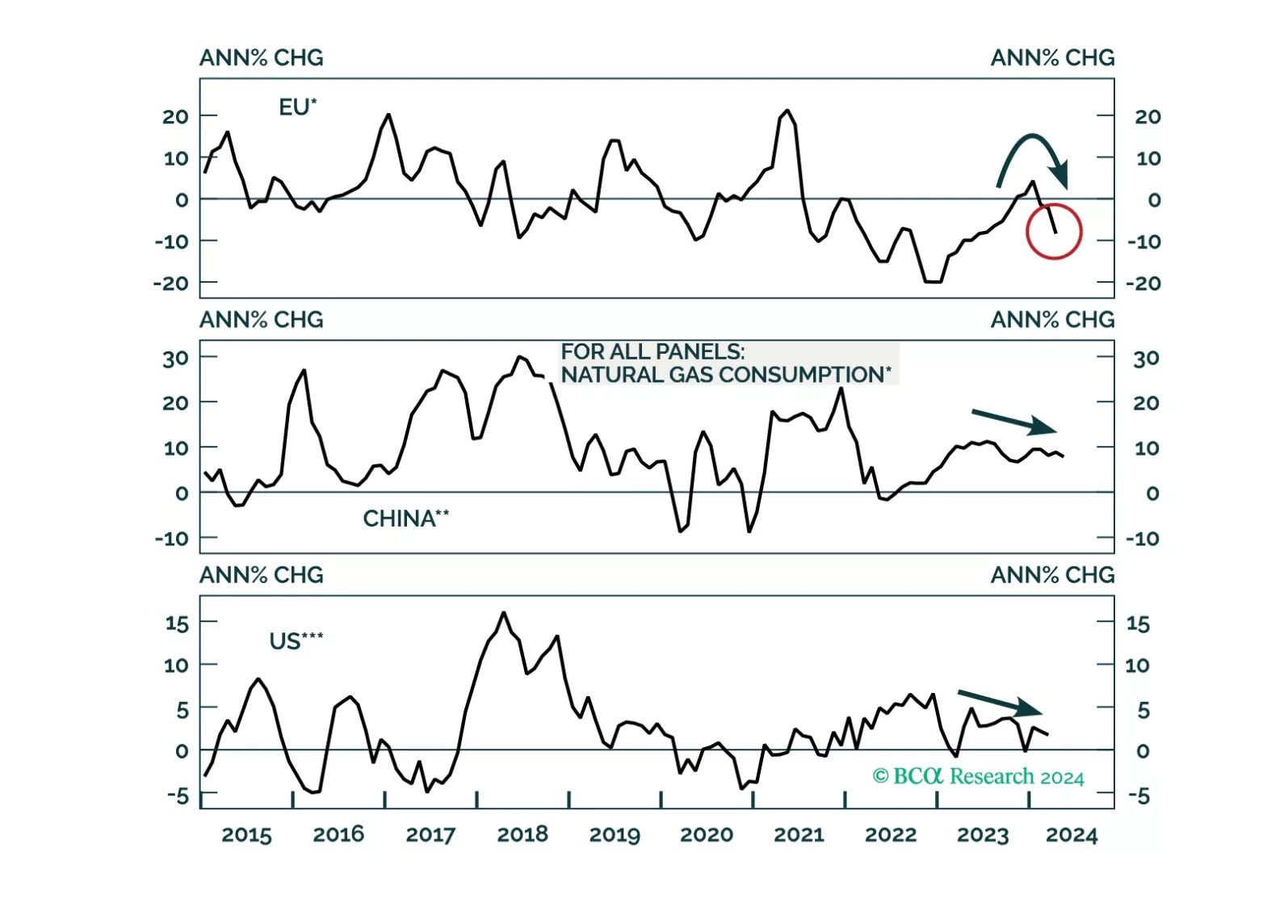

A global economic downturn will be a headwind for natgas prices over the cyclical horizon. Thereafter, LNG capacity additions will help keep the market in balance into the end of the decade. That said, Europe’s increased dependence on global LNG flows raises its exposure to market dynamics in the rest of the world. This will keep volatility elevated versus pre-Ukraine war.