Currencies

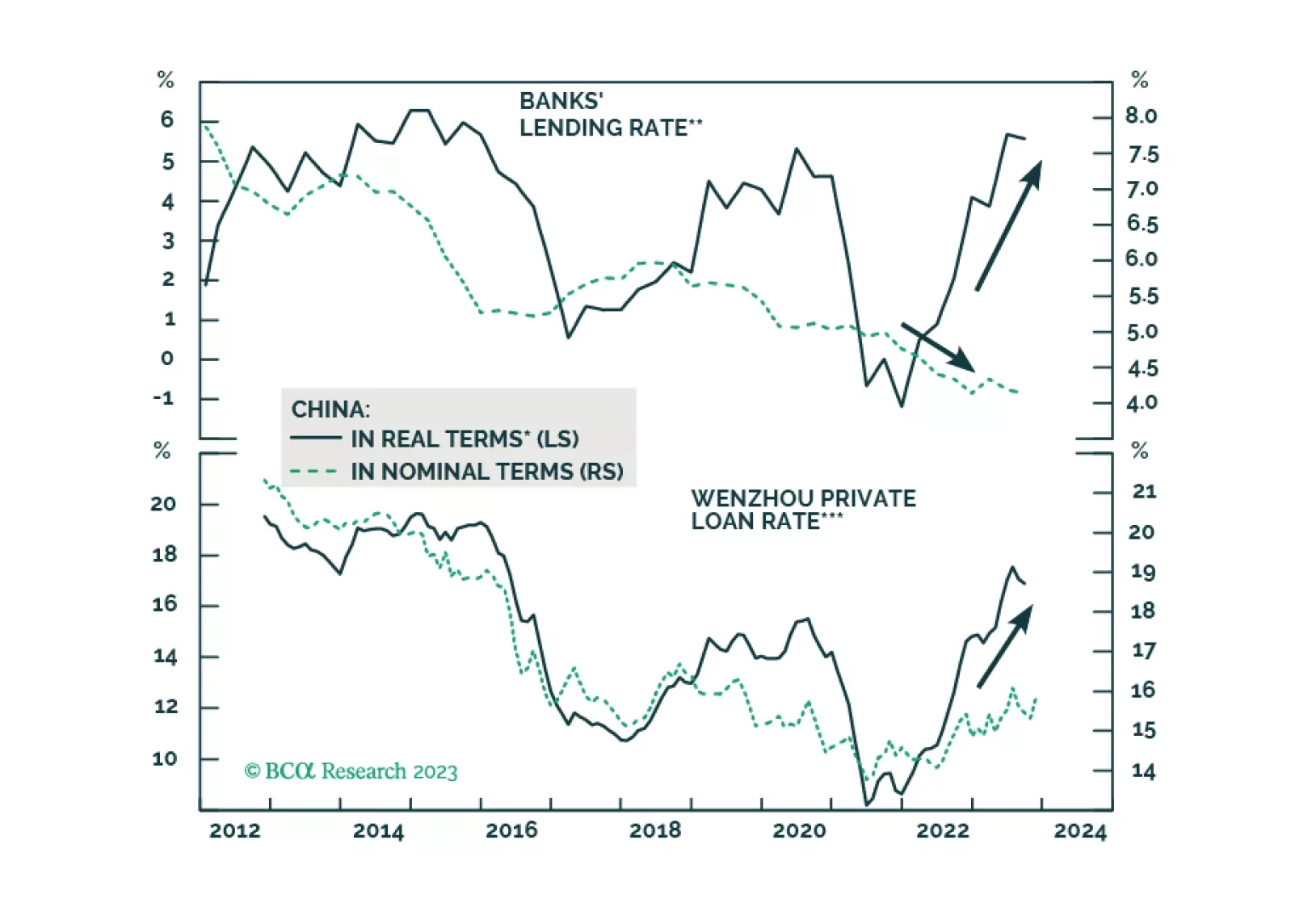

A low multiplier effect of stimulus will reduce the magnitude of the rebound in China's business activities in 2024. The housing market downturn will likely persist, and the ongoing household deleveraging also poses a significant challenge to China’s economic recovery.

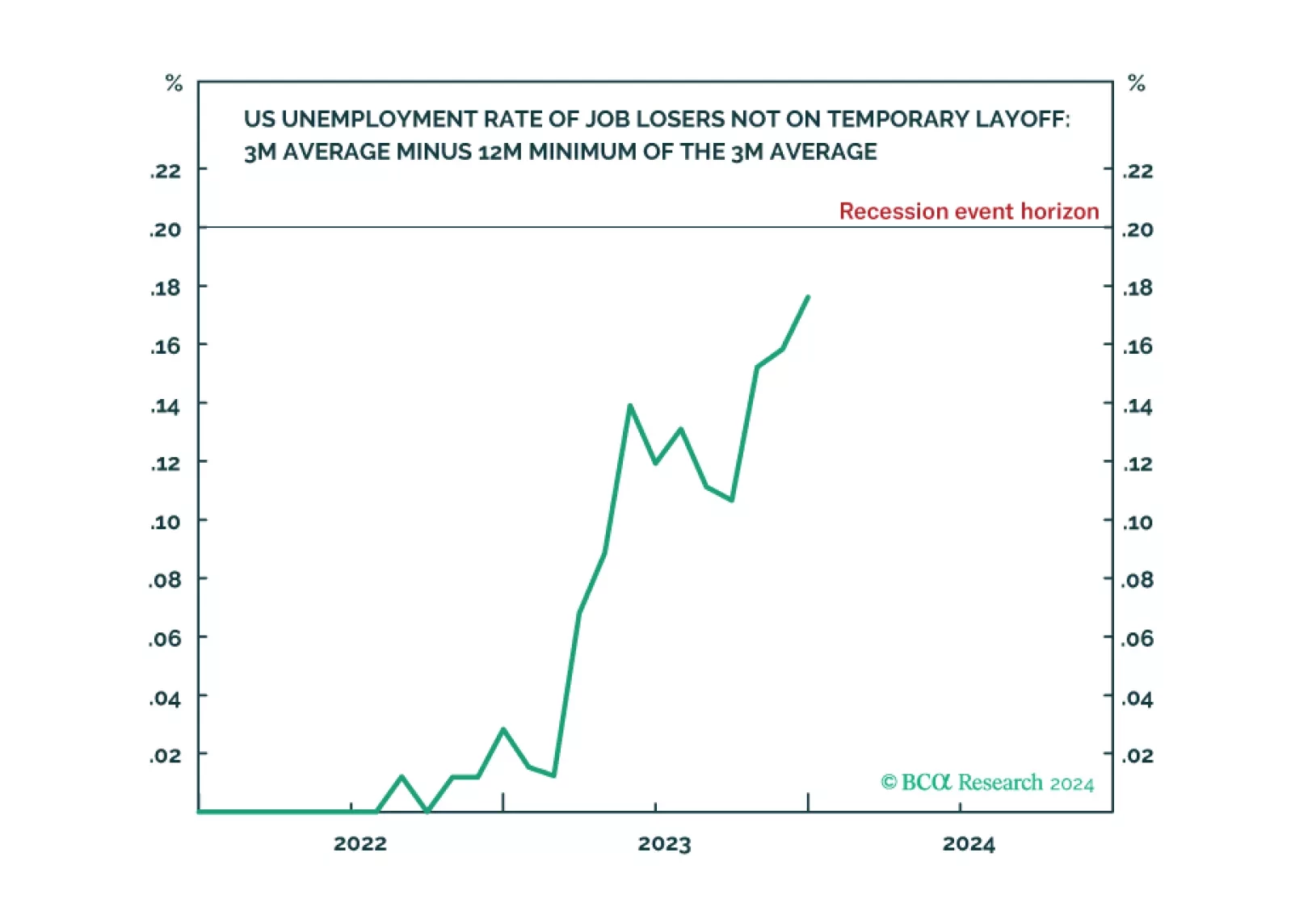

Following today’s US jobs data release, the Joshi rule real-time US recession indicator inched up to 0.18 and is now just a whisker from its recession event-horizon of 0.20.

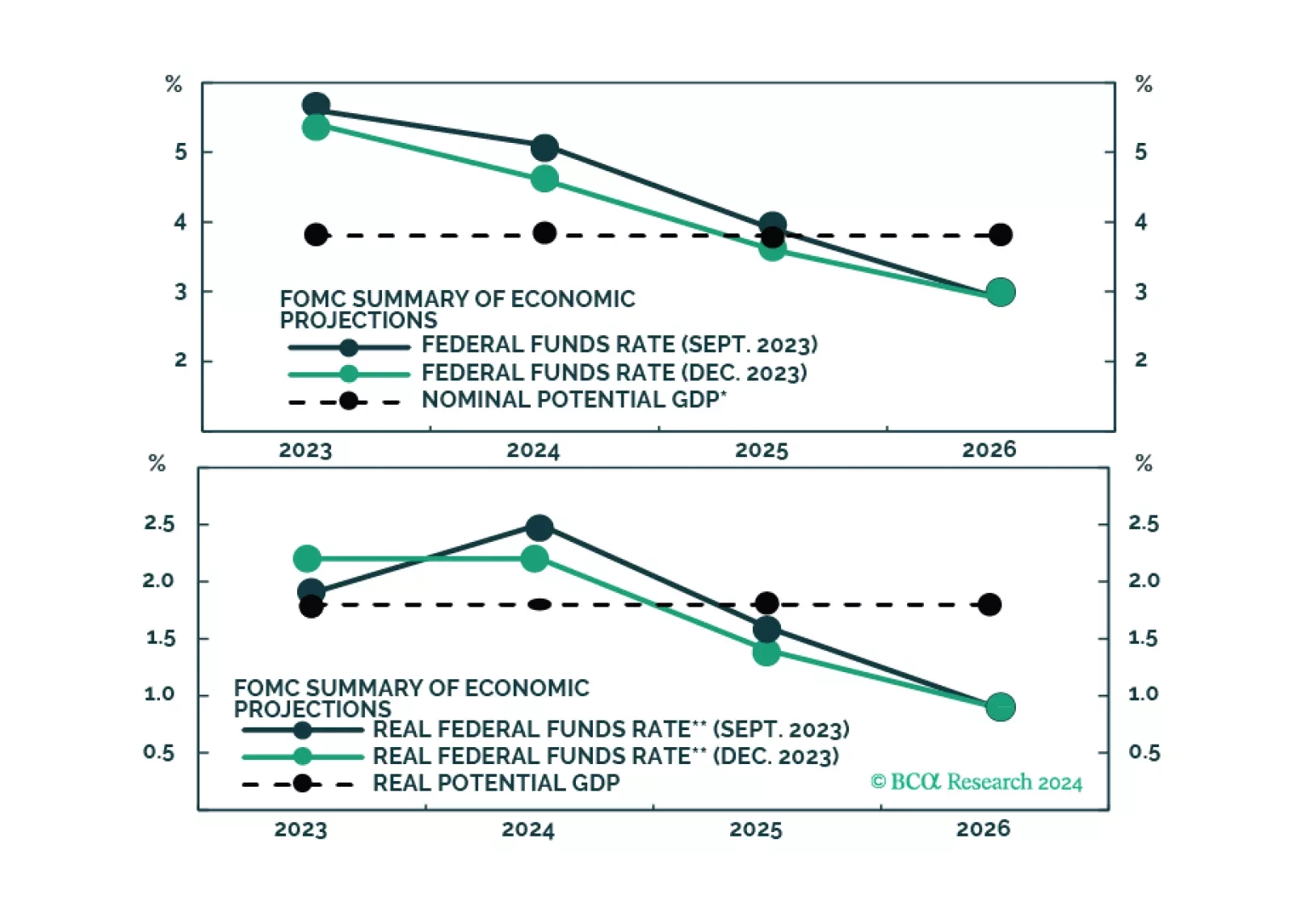

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

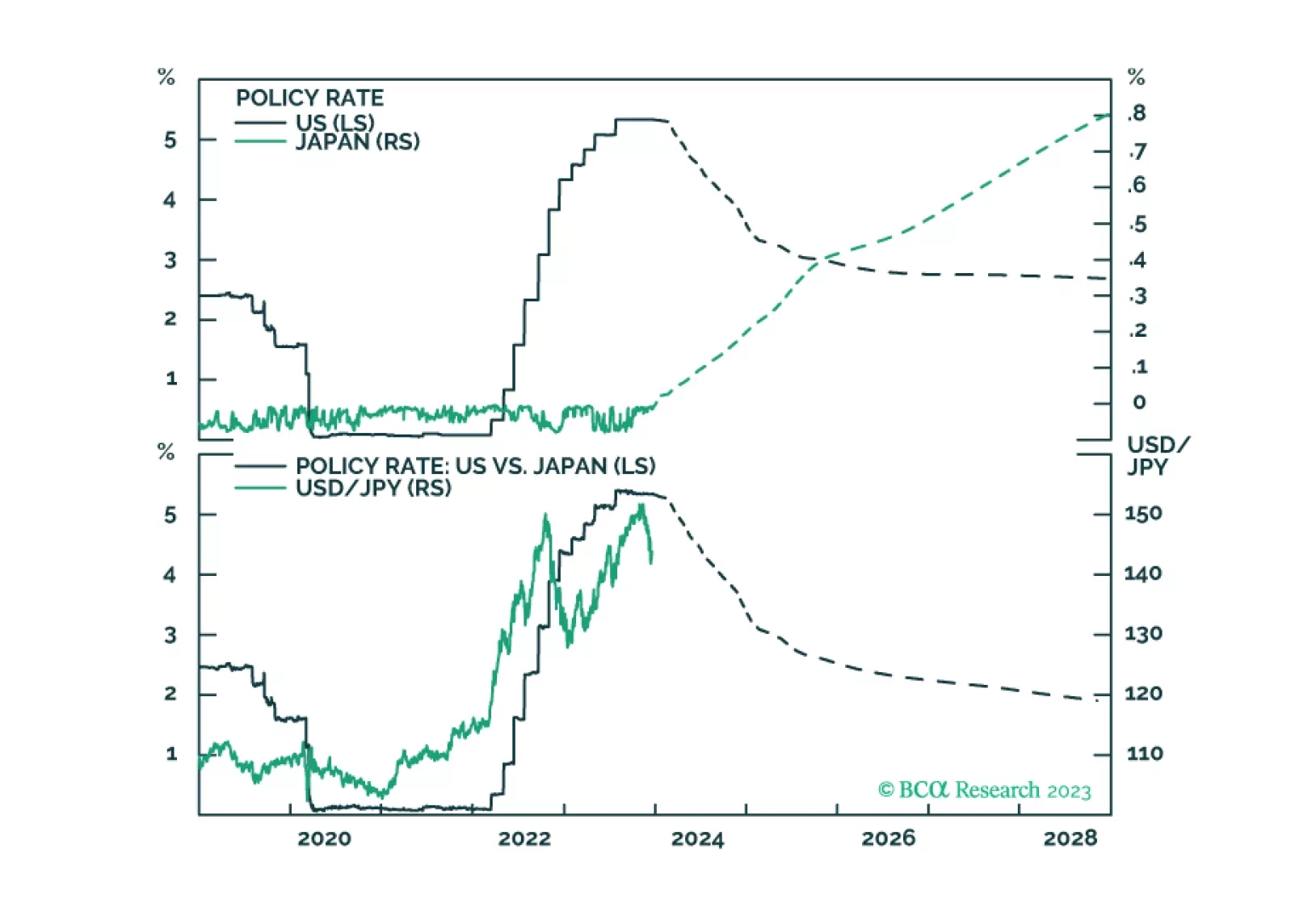

A post-mortem of our trades for the year, and also comments on future yen and sterling moves from the recent BoJ meeting, and the UK inflation report.

The statement from last week’s Central Economic Work Conference indicates that Chinese authorities are still not considering large-scale stimulus in 2024. Odds are that a full-fledged business cycle recovery in 2024 is unlikely. Chinese share prices remain vulnerable, and strengthening in the RMB will be short-lived.

Explore the eight main themes that will drive the returns of European assets in 2024.

Our recommendations for blogs and X’s (on the economy, financial markets, asset allocation, bonds, quants, energy, real estate, geopolitics, and specific countries and regions) to try over the holidays.