Commodities & Energy Sector

High interest rates will eventually cause growth to slow. Signs of stress are already starting to show. Stay cautiously positioned.

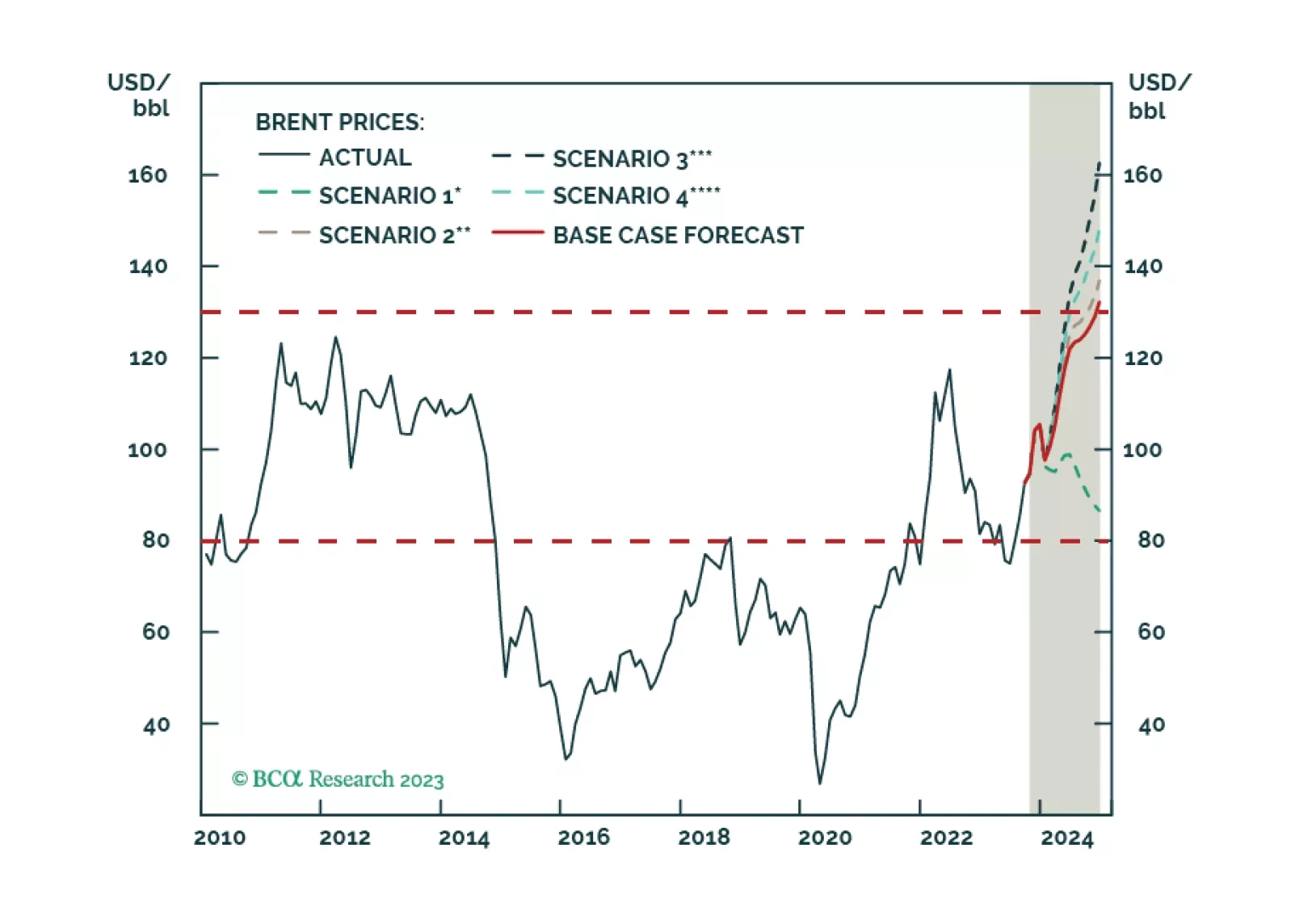

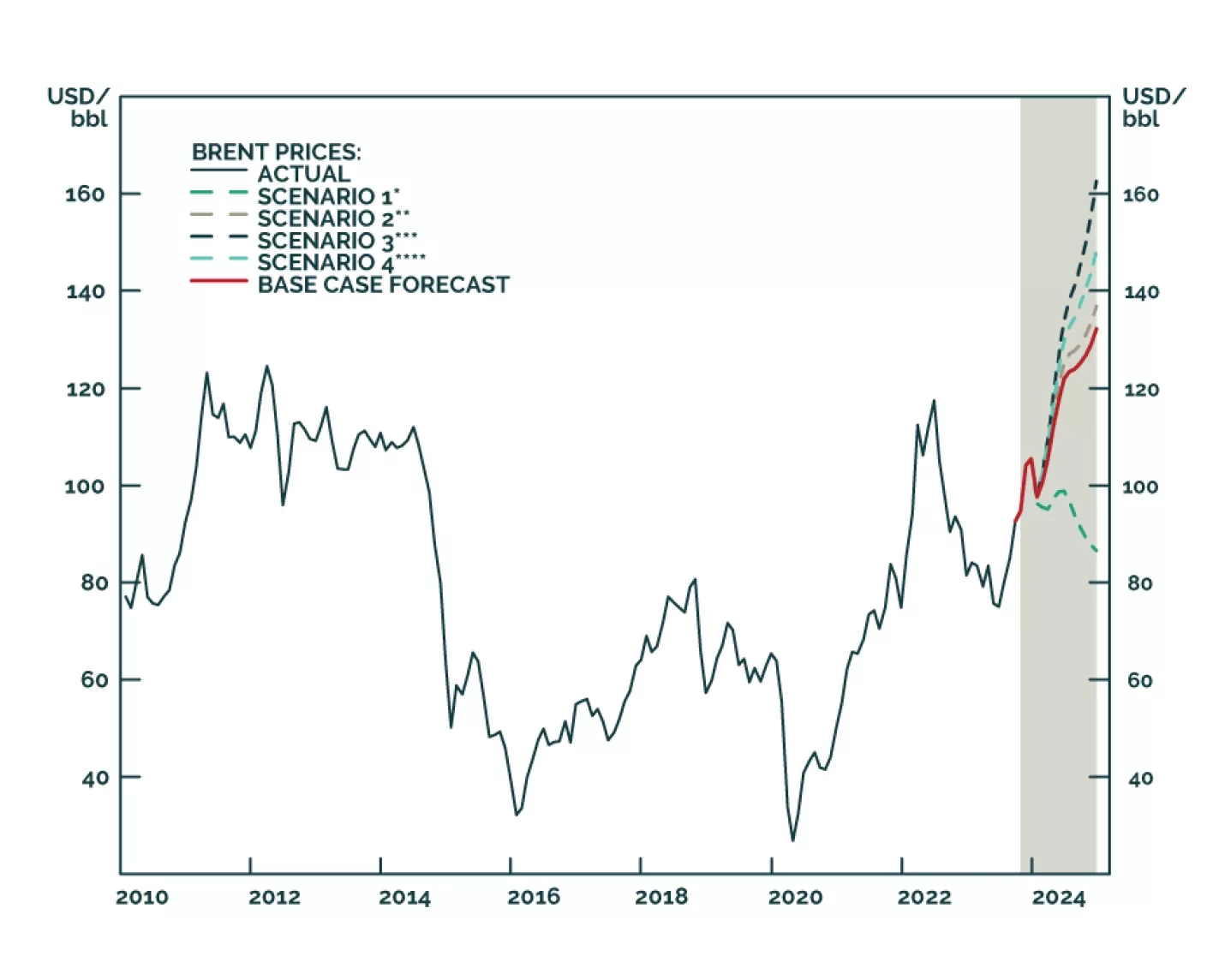

The US and core OPEC 2.0 are – wittingly or not – laying the groundwork for a price band with a floor and cap on oil prices – at $79/bbl and $130/bbl, respectively – “at least” to May 2024. This accommodates multiple goals for both. To meaningfully support policy, the US would need to scale up purchases to refill its SPR. We remain long the XOP and COMT ETFs for direct exposure to energy E+P equities and commodities.

Despite higher uncertainty, our Brent price forecasts remain unchanged at just over $101/bbl for 4Q23 and $118/bbl for next year. We remain long equity exposure to oil and gas producers via the XOP ETF, and commodity exposure via the COMT ETF. We also remain long $100 Dec24 Brent calls and long 1Q24 Brent futures vs. short 1Q25 Brent futures in anticipation of stronger backwardation.

The Hamas attack against Israel, timed almost 50 years to the day after a similar surprise attack on Yom Kippur of 1973, has evoked parallels with the 1970s. Parallels not only with Middle Eastern geopolitics then and now, but also with inflation, economics, and financial markets. In this report, we explain what went wrong in the 1970s and whether the mistakes will be repeated. Plus: the sharp sell-offs in some Latin American currencies are reaching a potential turning-point.

Investors underestimate the likelihood of the war in Israel spilling outside of Gaza, and engulfing wider swaths of the Middle East, endangering energy supplies. Stay overweight Energy and Aerospace & Defense.

The Israeli-Arab crisis is more likely to expand and cause oil disruptions than market consensus holds. Close long dollar trades and go long energy and defense stocks relative to cyclicals.