Commodities & Energy Sector

Seasonal weather and price variability in the first quarter will dissipate, which will reduce the agita caused by the recent inflation scare. This will increase the Fed’s comfort level in initiating a rate-cutting cycle in June with a 25 bp cut. With inflation well-behaved, real interest rates will move lower and gold prices will move higher. The rate-cutting cycle also will allow the USD to weaken as assets ex-US become more attractive; this will be bullish for gold. Physical demand for gold is expected to remain robust, along with safe-haven and central-bank diversification demand, due to heightened geopolitical uncertainty. We continue to expect gold to trade above $2,200/oz this year.

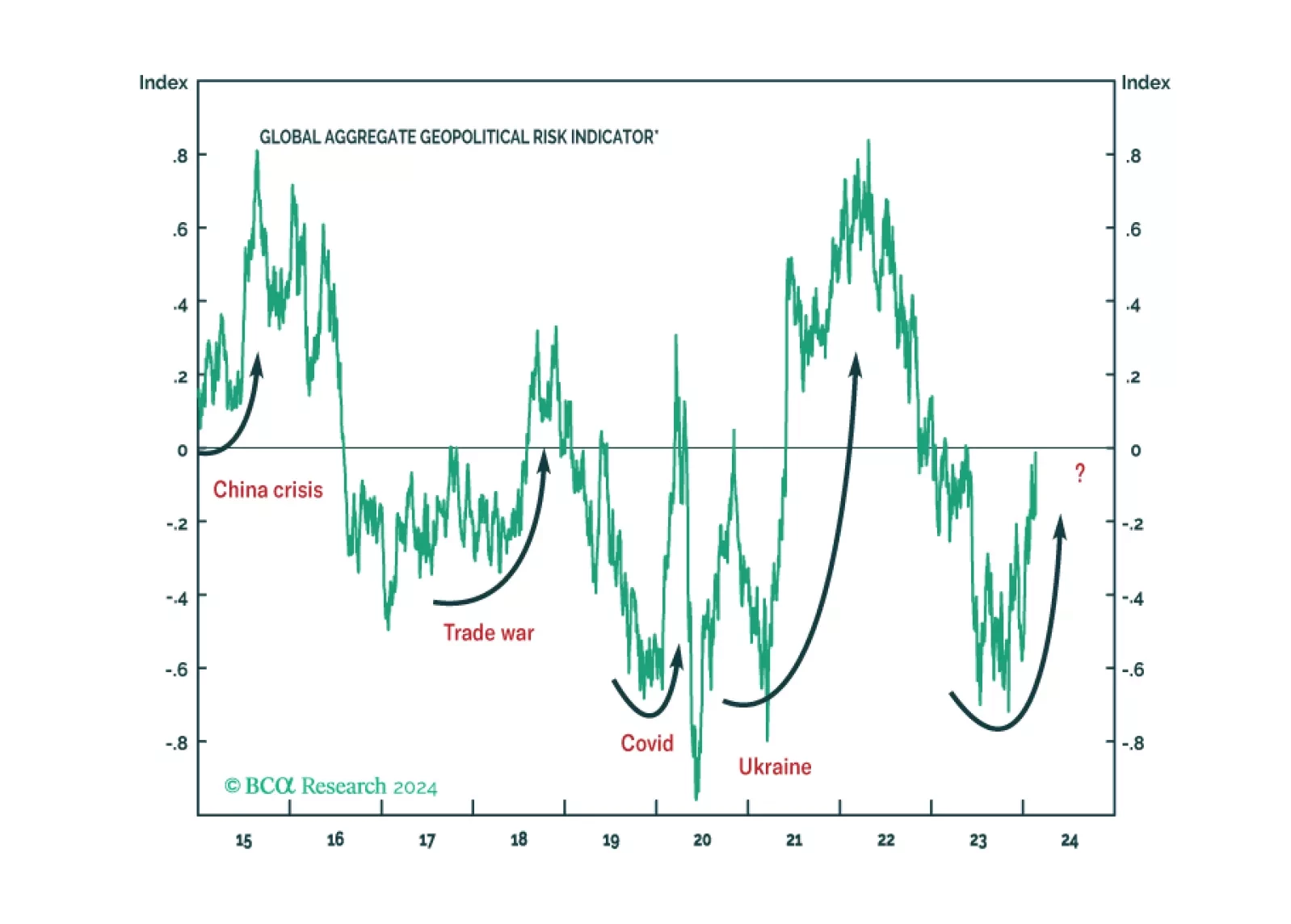

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

Reported earnings for Q4-2023 were rather underwhelming and prone to issues that we have identified over the past few months: Growth is concentrated in just a few sectors and companies, while the profitability of a broad swath of the equity market is under pressure from disinflation and sticky wages. Consumers are still spending, but less enthusiastically than before, while a switch from spending on services to spending on goods is in its very early innings. Downgrade Consumer Staples to neutral.

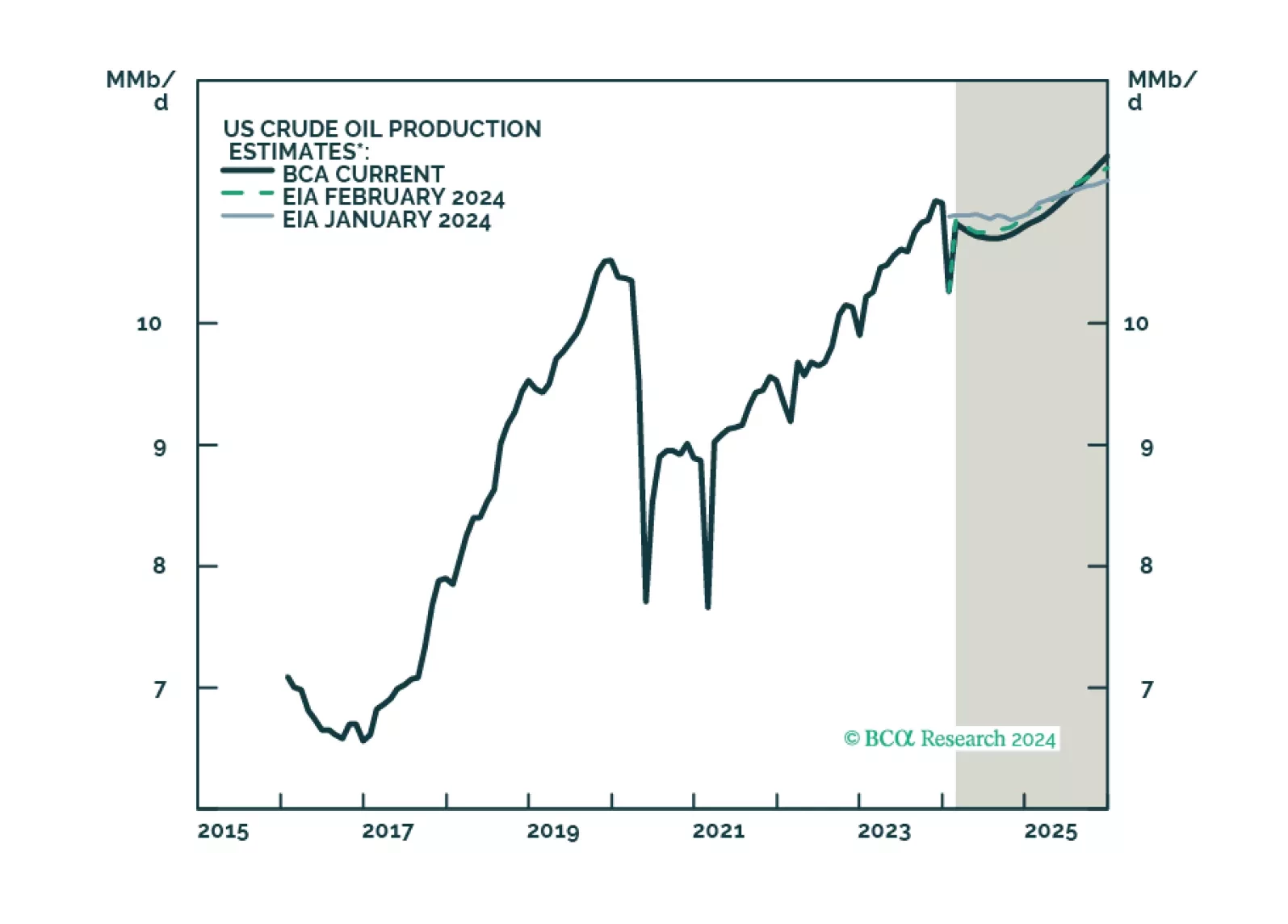

Energy markets are balanced in the short run, which keeps our Brent price forecasts at $95/bbl and $105/bbl in 2024 and 2025. Structurally, we see an upward bias to inflation, as geoeconomic fragmentation fundamentally alters supply chains; higher costs follow. Military access to oil will be prioritized. Renewables are the future, but war will be fought with hydrocarbons. We remain long the COMT, XOP and PPA ETFs.