Commodities & Energy Sector

Back in May, our Commodity and Energy strategists argued that OPEC, EIA, and IEA oil demand forecasts were likely too optimistic. Indeed, while all three major oil price forecasters projected a moderation in demand this year, none of them anticipated weak…

According to BCA Research’s Commodity and Energy Strategy service, soft oil demand growth raises the likelihood that OPEC+ will back down from its plan to begin unwinding some of its production cuts later this year. However, investors should not read this as…

US industrial production fell by a larger-than-expected 0.6% m/m in July, the largest monthly decline so far this year. Capacity utilization also decreased a full percentage point to 77.8% Although Hurricane Beryl distorted these nationwide July numbers,…

Regular readers are familiar with our expectation that the stabilization in global growth this year will be fleeting. The US has been the main source of demand in this cycle. We view the latest string of US employment data as further evidence the US…

The RBA kept its cash rate unchanged at 4.35% in August, in line with expectations. However, it lifted its trimmed-mean inflation forecast to 3.5% y/y in Q4 2024 and to 2.9% by Q4 2025 (up from 3.4% and 2.8% in its May forecast, respectively). Inflation…

Chinese exports in USD terms missed expectations in July, growing by 7.0% y/y, down from 8.6% in June. Conversely, imports rebounded smartly from a 2.3% contraction, rising by 7.2% in July and upending expectations of 3.2%. Slower export growth is…

Industrial metals were one of the worst performing asset classes last month. Have prices declined enough to make them an attractive investment? The outlook for industrial commodity prices is bearish over a 12-month horizon given we expect the US economy to…

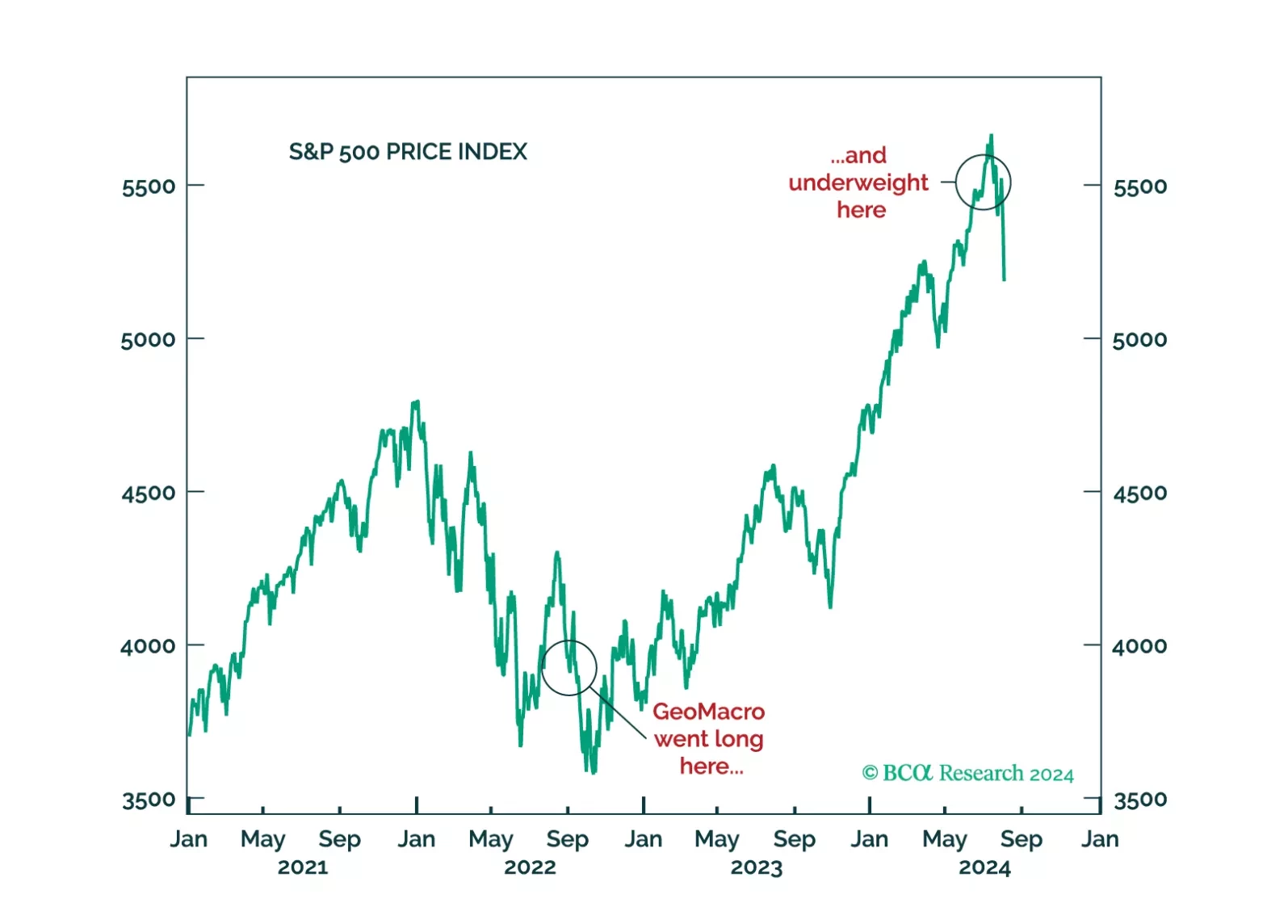

The decision by GeoMacro team on July 2 to short USDJPY and underweight equities has proven to be prescient. We still do not like the market setup from here on out. A recession would, obviously, be negative for risk assets. But even if investors avoid that scenario, the transition from cash- to leverage-driven growth is unlikely without a significant Fed rate-cutting cycle.

According to BCA Research’s Commodity & Energy Strategy service, robust iron ore imports are sending a false signal about steel demand. Instead, these supplies are being used to restock inventories. By the end of last year, iron ore stocks at Chinese…

The market is pricing in a soft landing, but we see growing signs that the global economy is faltering. Investors should be defensively positioned.