Colombia

The rally in Colombia’s financial markets has a short shelf life. The election will bring a right-wing government, but it cannot fix inflation, fiscal arithmetic, or balance-of-payments vulnerabilities. Use the near-term rally to downgrade Colombian fixed income and equities.

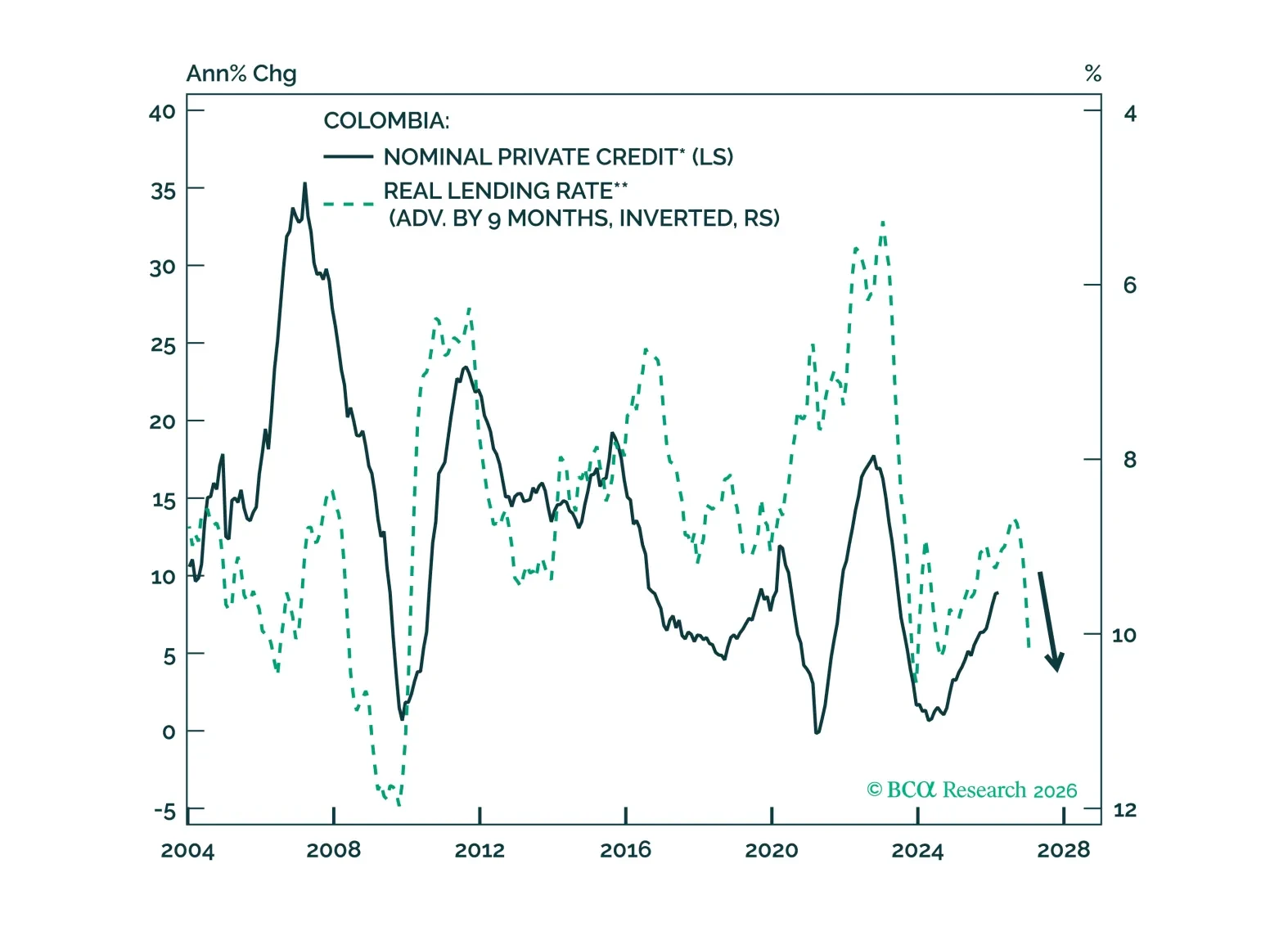

Go long LATAM ex. Brazil banks / short global bank stocks. Brazilian bank equities will underperform due to poor and worsening macro fundamentals.

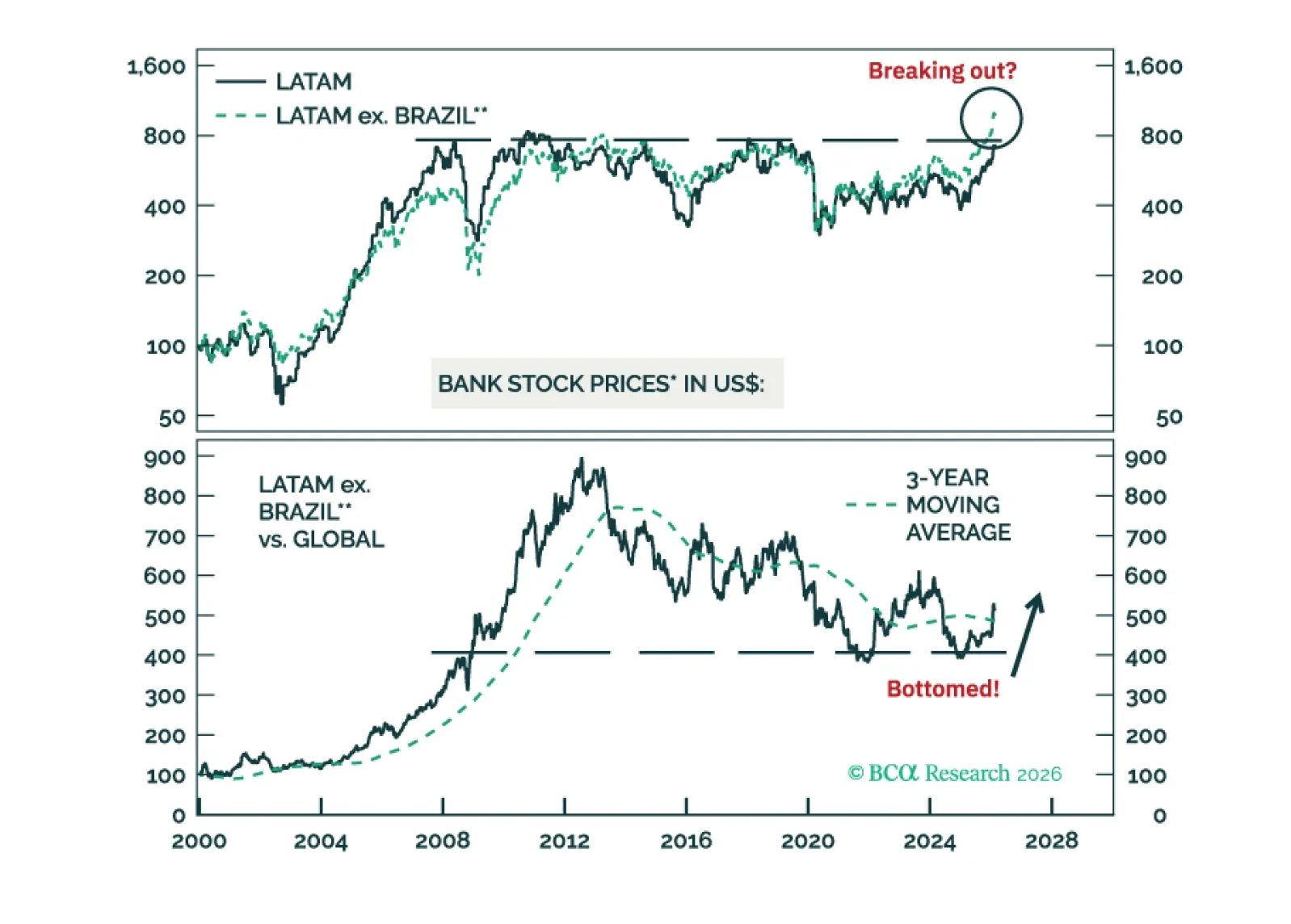

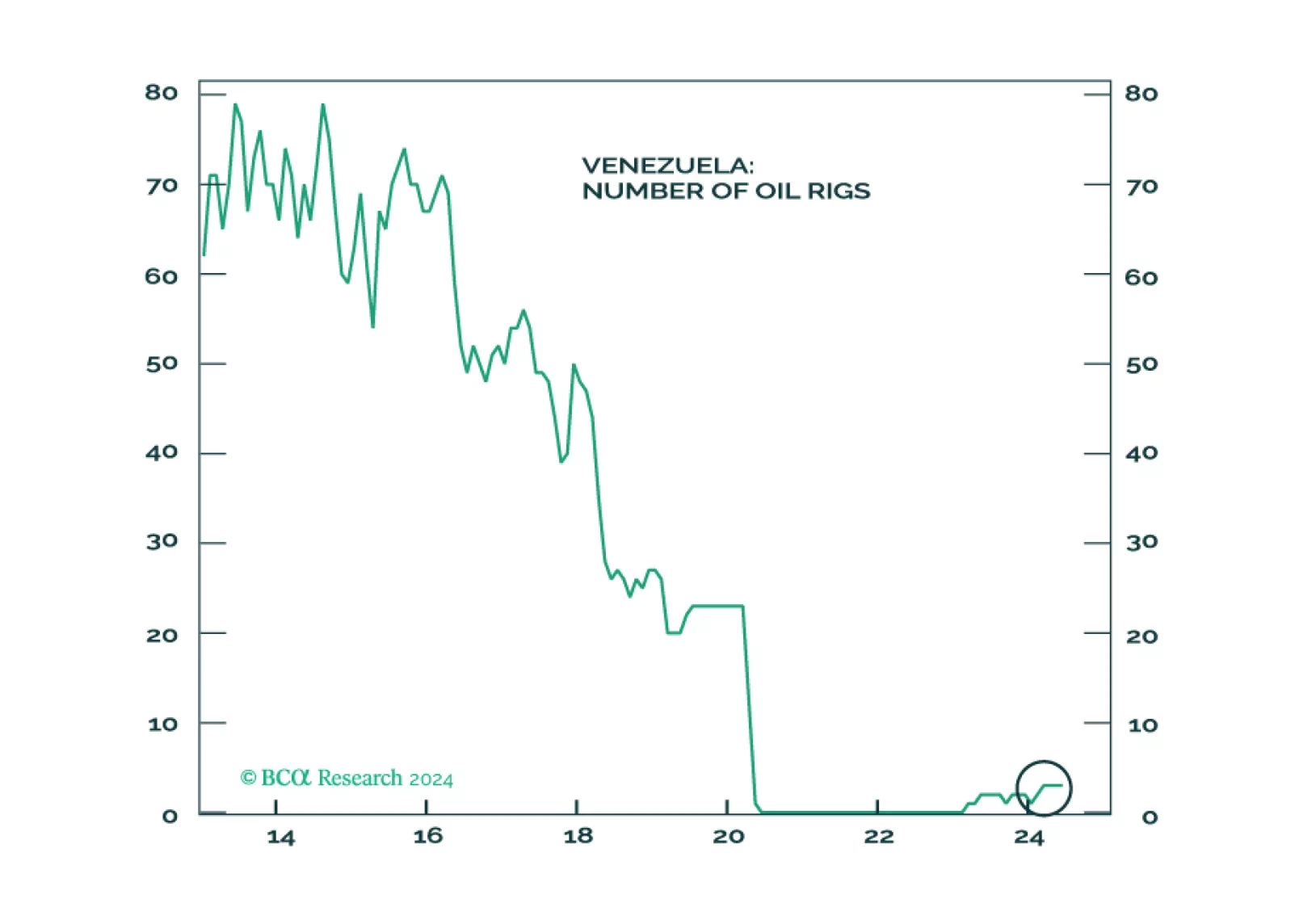

There will be little market and macro implications from the US intervention in Venezuela. Fade away any near-term moves in global oil markets. However, Colombian and Peruvian assets will benefit from lower political risk premiums. We are upgrading Colombian equities and fixed income to overweight versus EM.

Colombian markets will be torn between expectations of future orthodox policies and the reality of a worsening macro backdrop in the next 12 months. To balance risks, we are upgrading Colombian equities, local bonds, and sovereign credit from underweight to neutral versus their respective EM benchmarks.

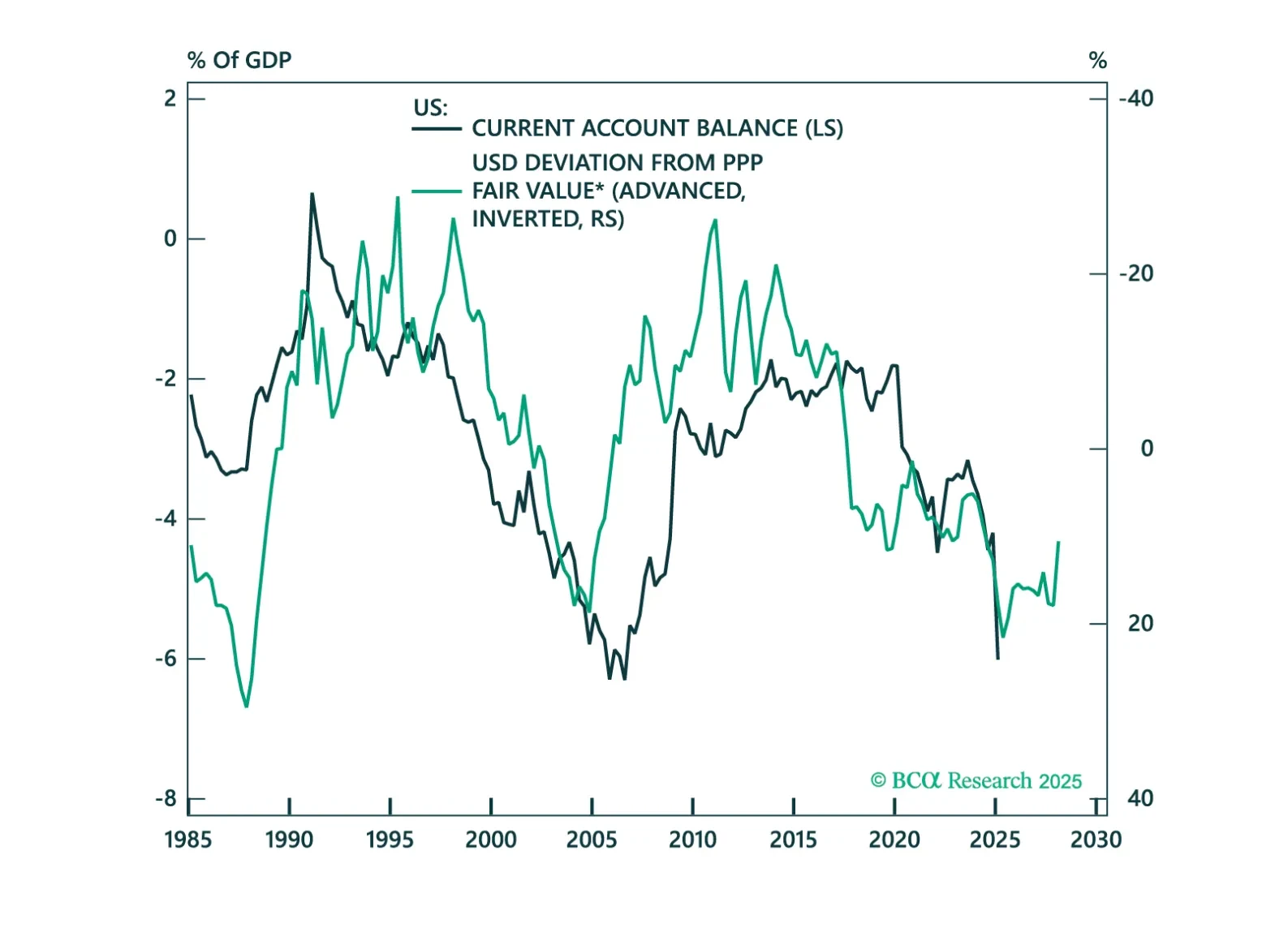

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.

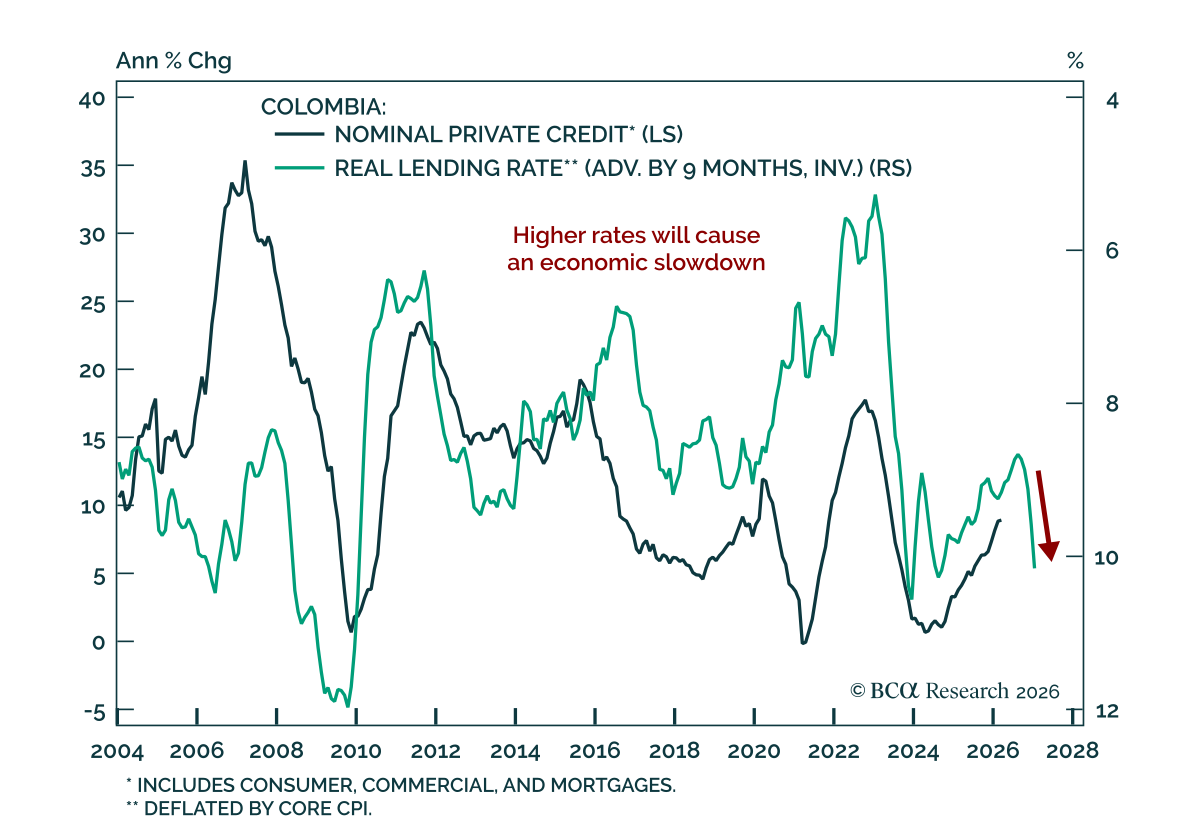

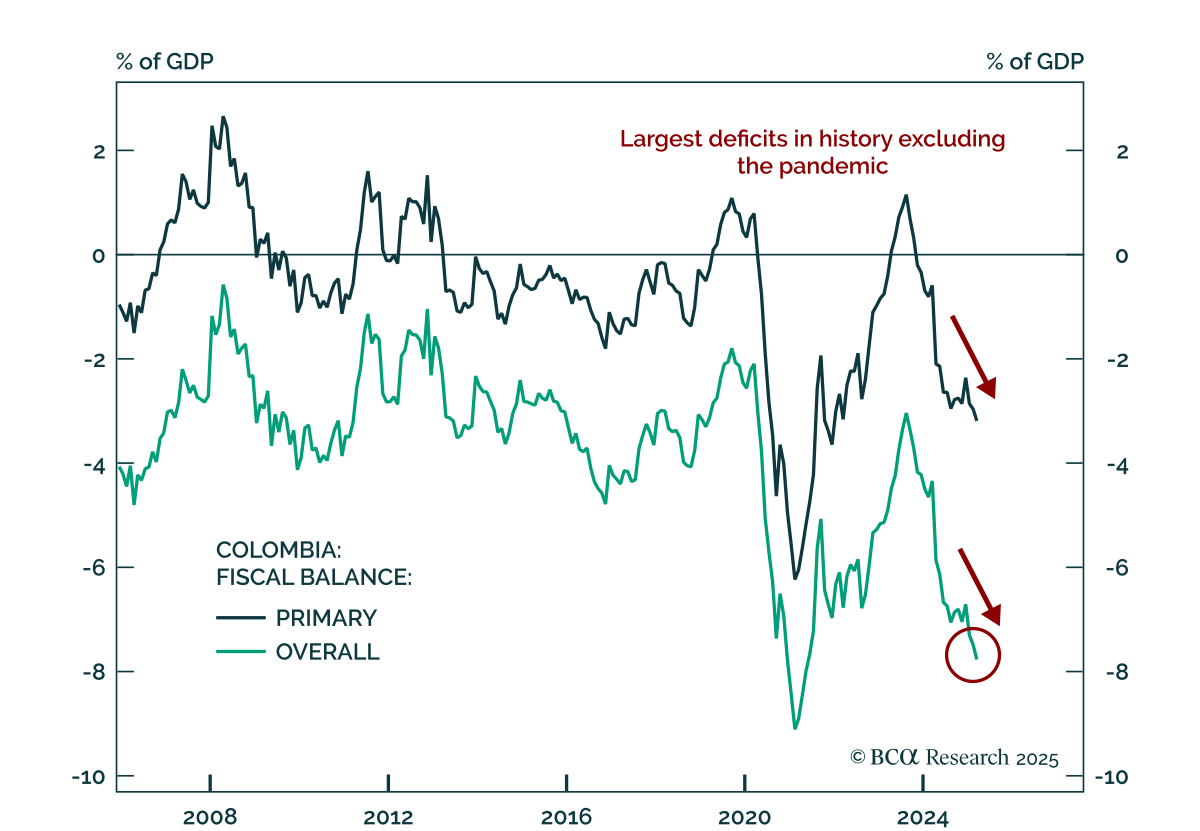

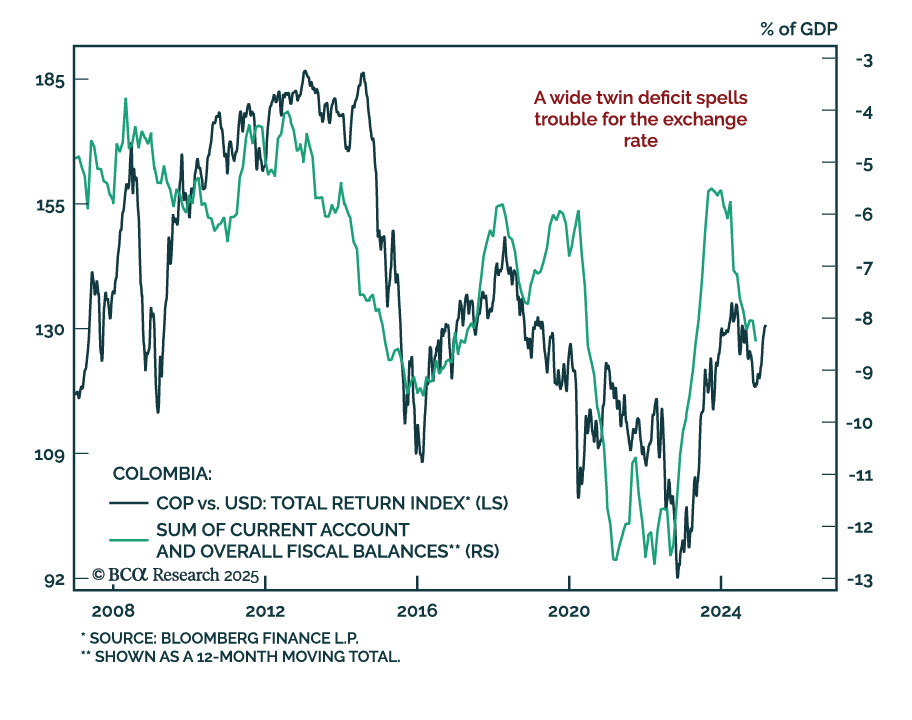

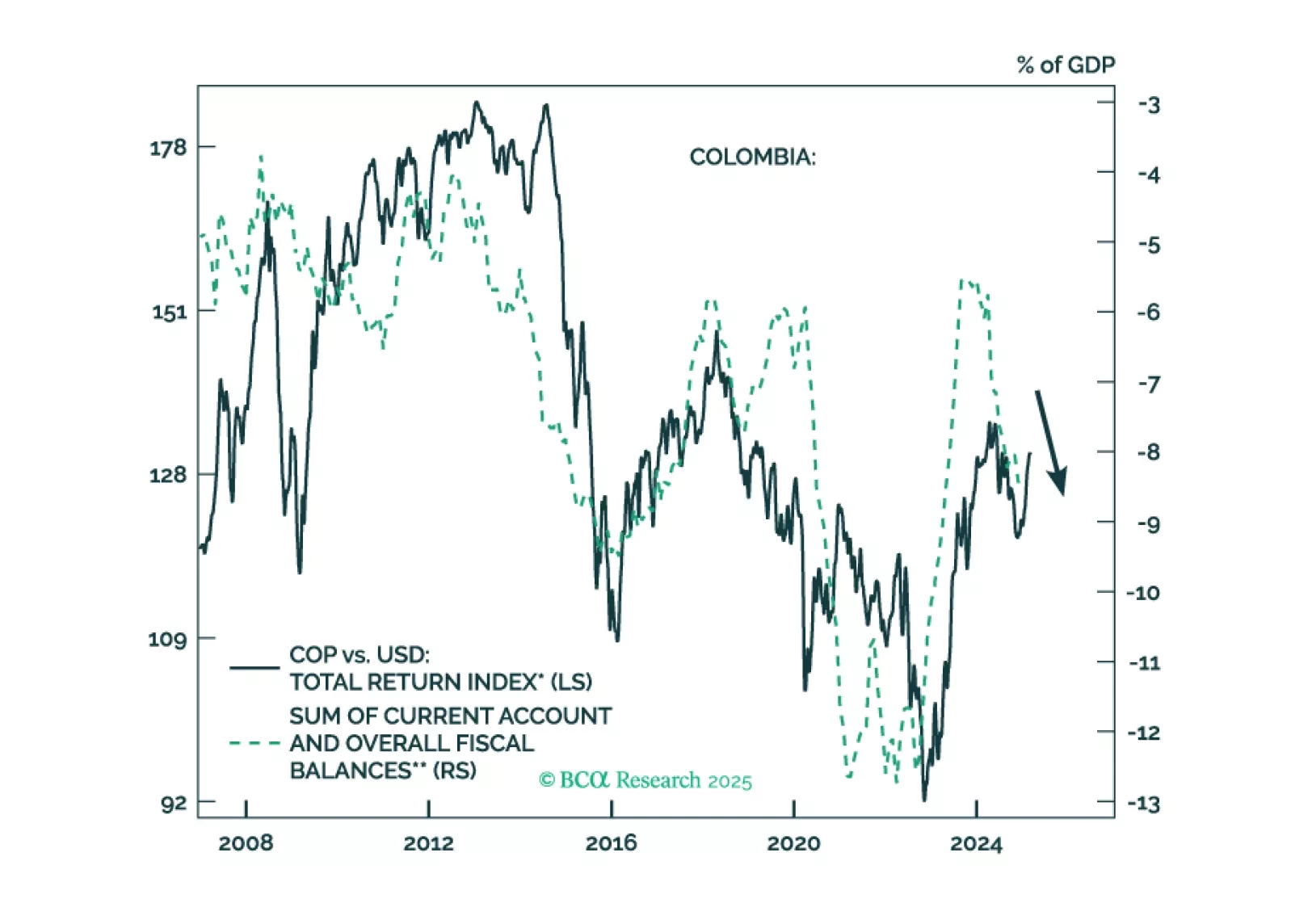

Colombian financial markets have rallied on the expectation that a right-wing government will be elected in 2026. We take a contrarian bearish stance on the nation's financial markets. Colombia is suffering from two structural macro issues – unsustainable public debt and plunging energy exports – that will not be easily solved by a conservative administration in 2026. Continue underweighting Colombia within EM equity and fixed-income portfolios, continue shorting the COP versus the USD and the CLP, and bet on yield curve steepening.

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.