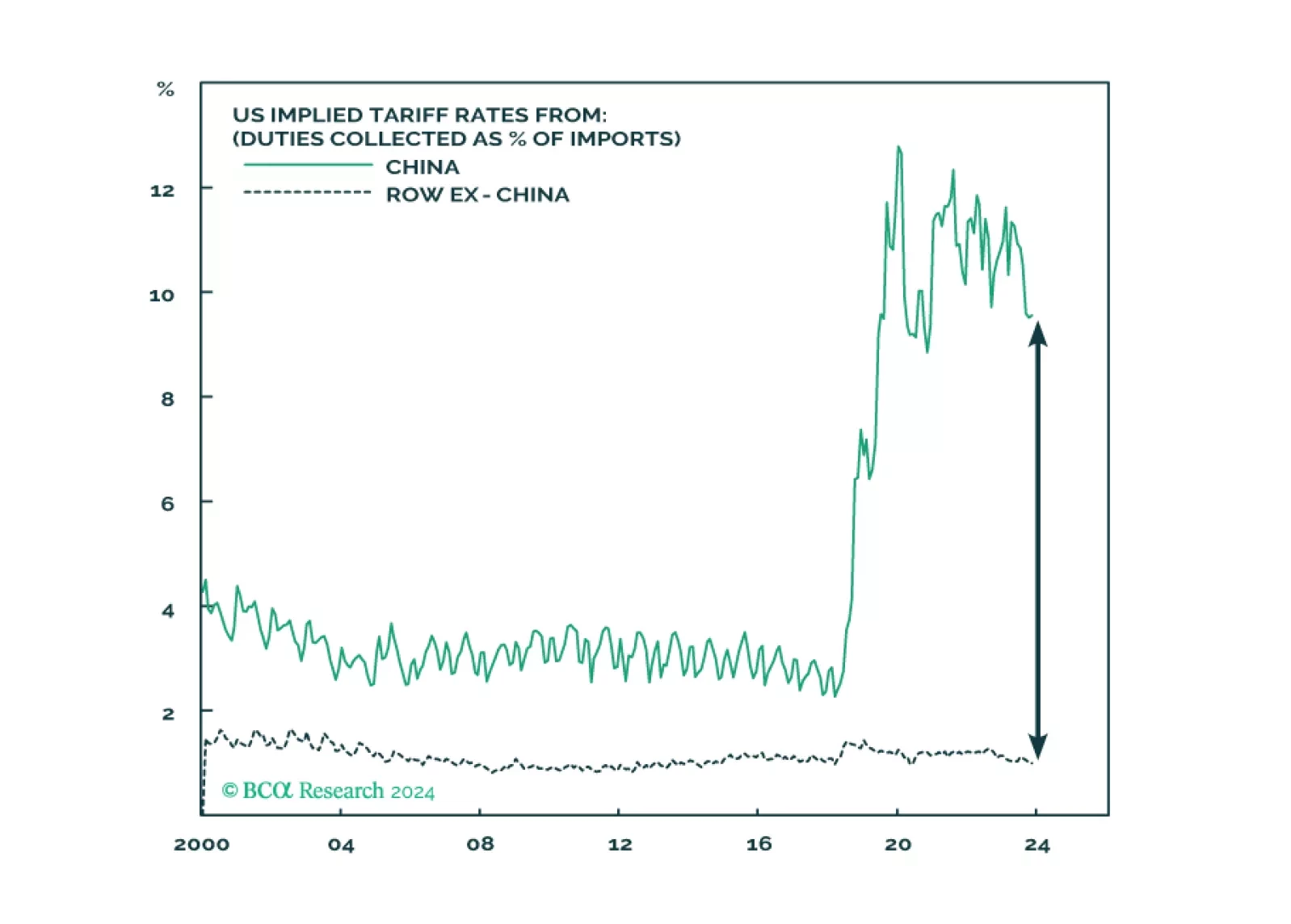

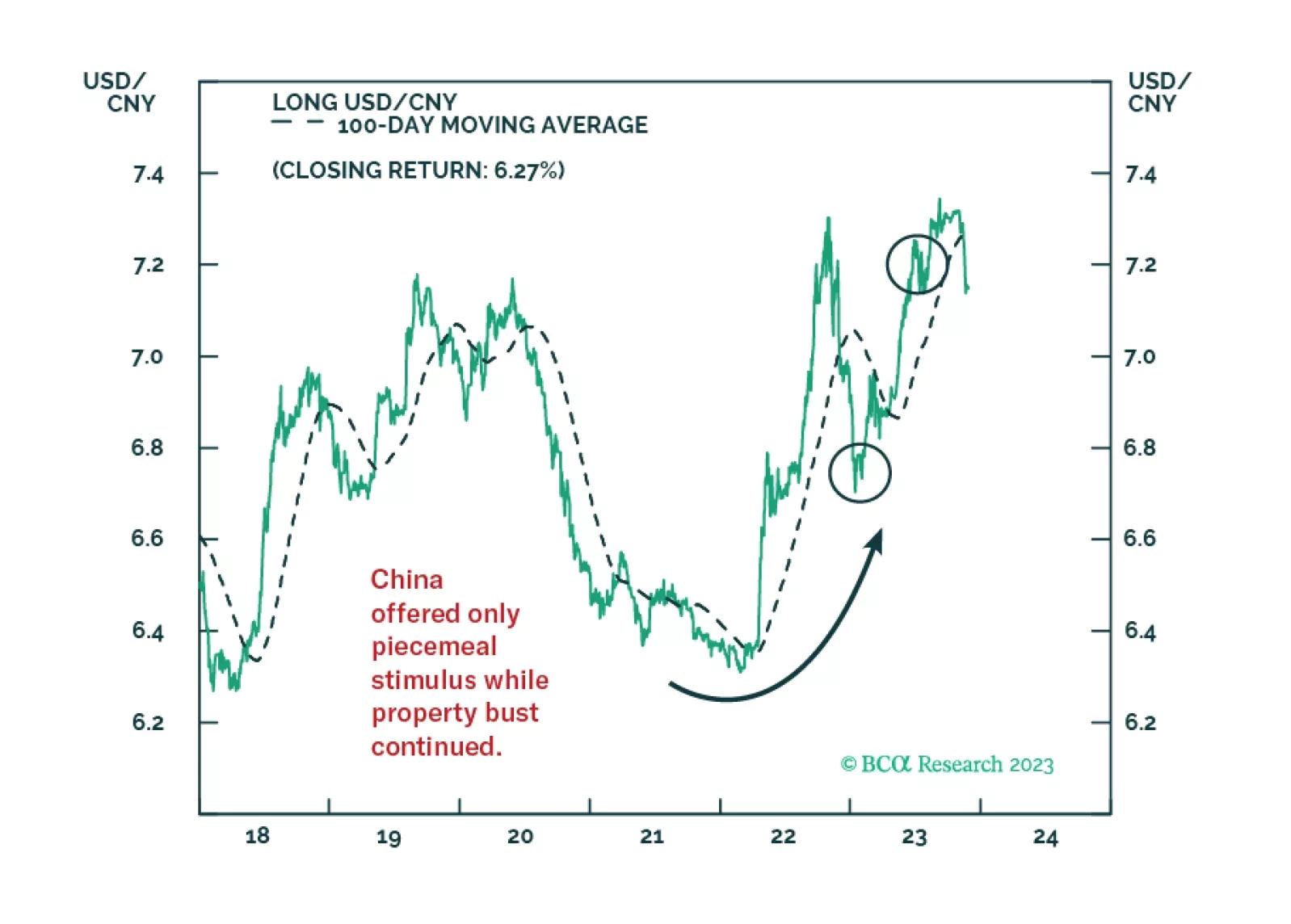

Chinese Yuan

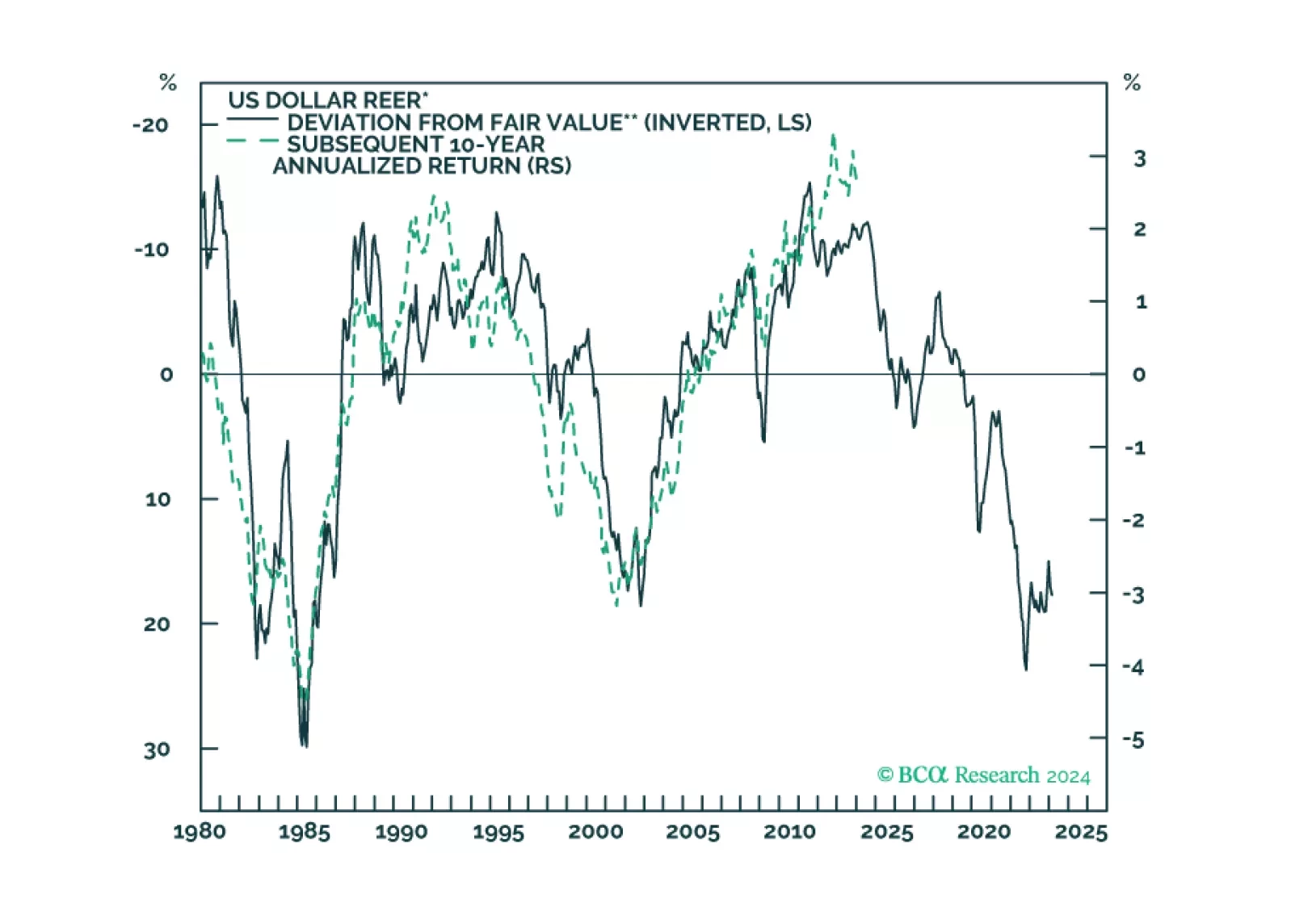

In this week’s report, we release an update to our long-term REER valuation model and expected future returns for major currencies.

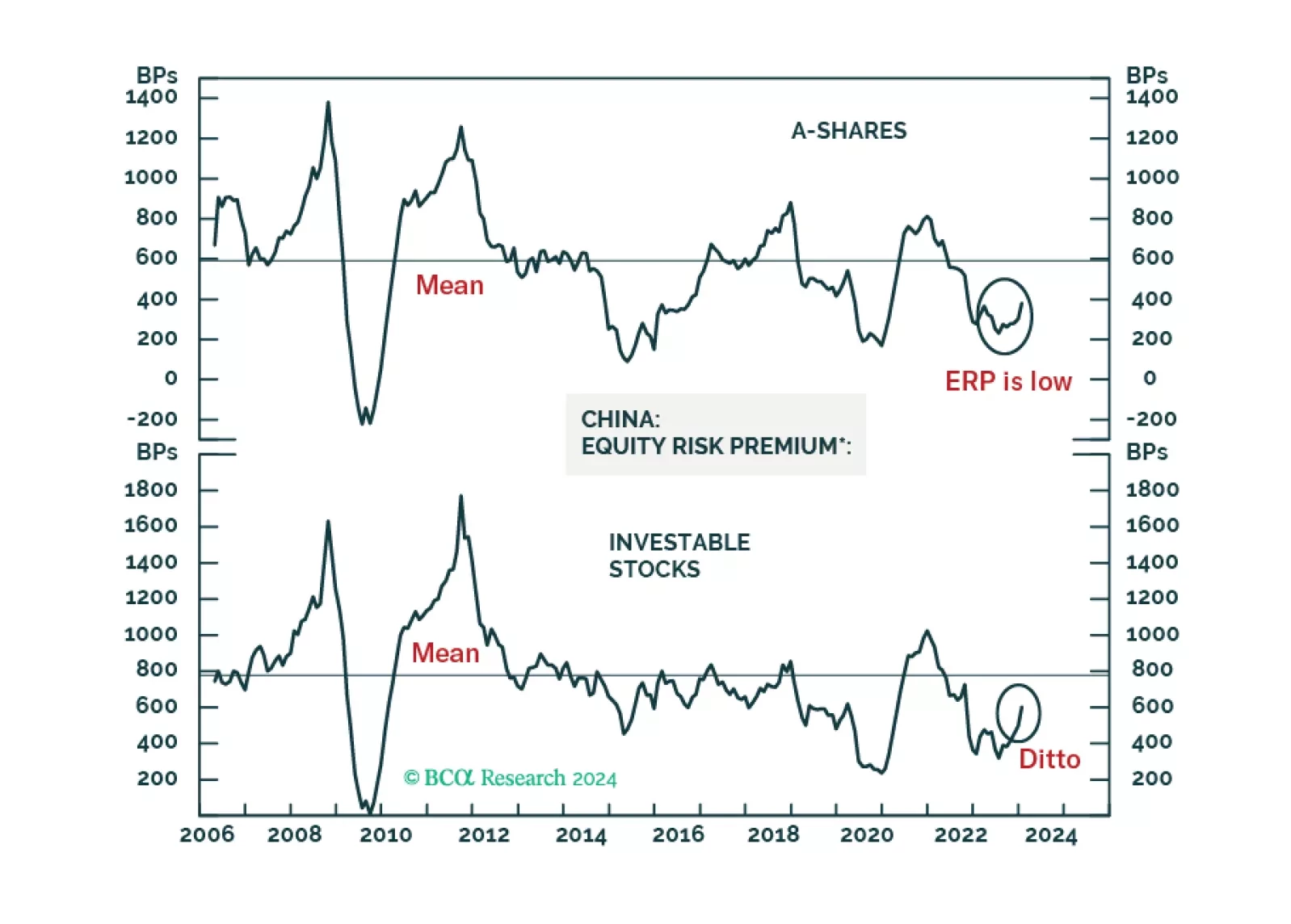

China will continue to suffer from a “triple crisis”. Though there could be a tactical bounce, cyclically we still recommend underweighting Chinese equities.

Chinese A-shares will probably begin forming a volatile bottom. The basis is that authorities will likely throw the kitchen sink at the onshore market in an attempt to stabilize share prices. The same is not true for offshore listed stocks. Hong Kong-traded Chinese share prices will likely continue to fall. Beijing is less concerned with offshore stocks as their holders are primarily foreign investors.

Our political forecasting scored wins in 2023 but we failed to capitalize on it adequately in our trade recommendations.

A global portfolio is likely to return only 5.3% a year over the next decade, compared to 6.7% in the past. Investors either need to lower their return expectations, or take more risk. Our total return methodology remains consistent with previous editions, with changes limited to the Alternatives section.

China removed checks and balances in its political system to deal with a very dangerous economic transition. The transition is going badly, yet investors cannot rely on checks and balances to correct or prevent policy mistakes. The Taiwanese election is a looming bellwether.