China Stimulus

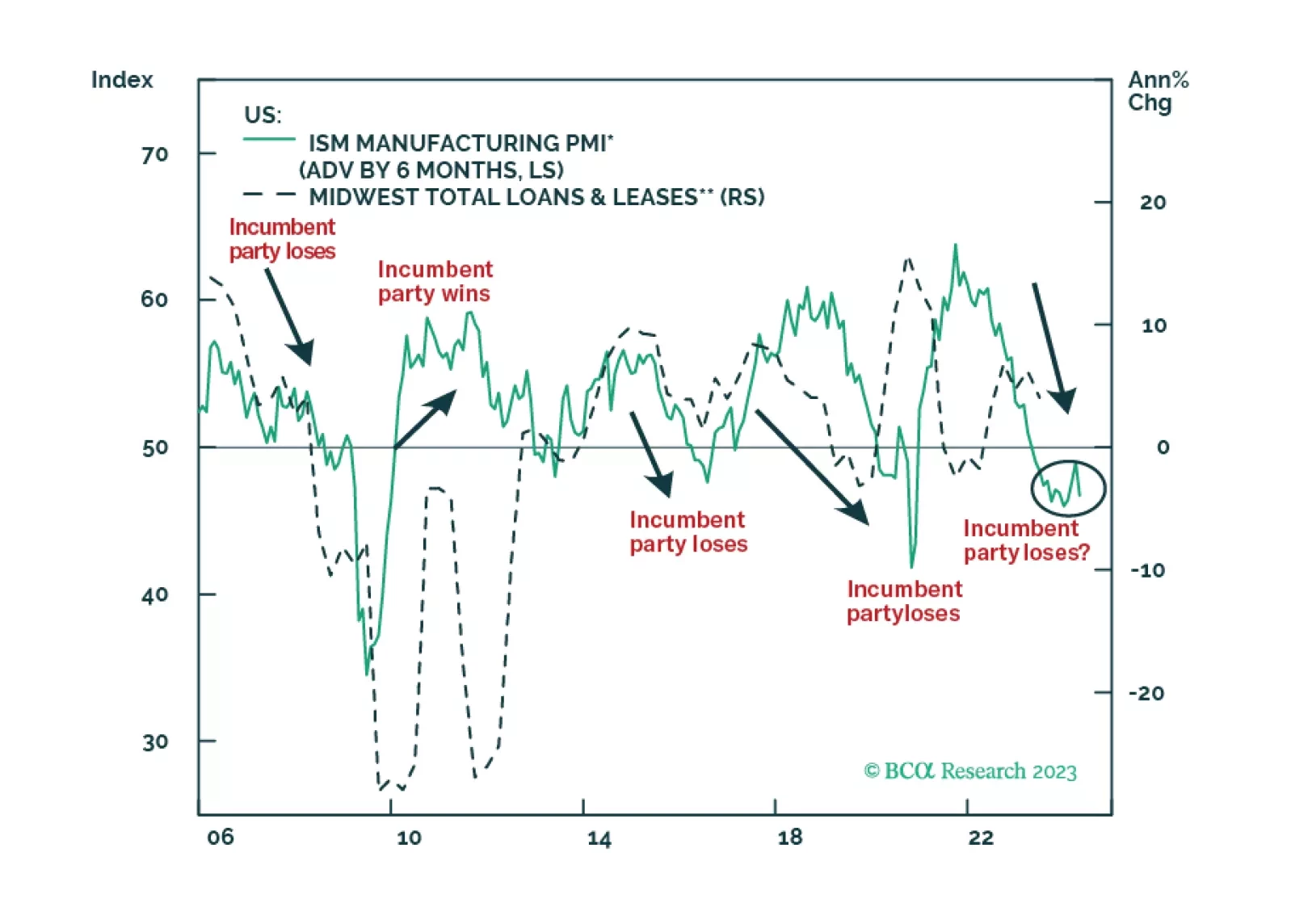

President Biden is facing foreign challenges on three fronts and these challenges are coalescing around the critical states of the Midwest. Take risks off the table and stay defensive in 2024.

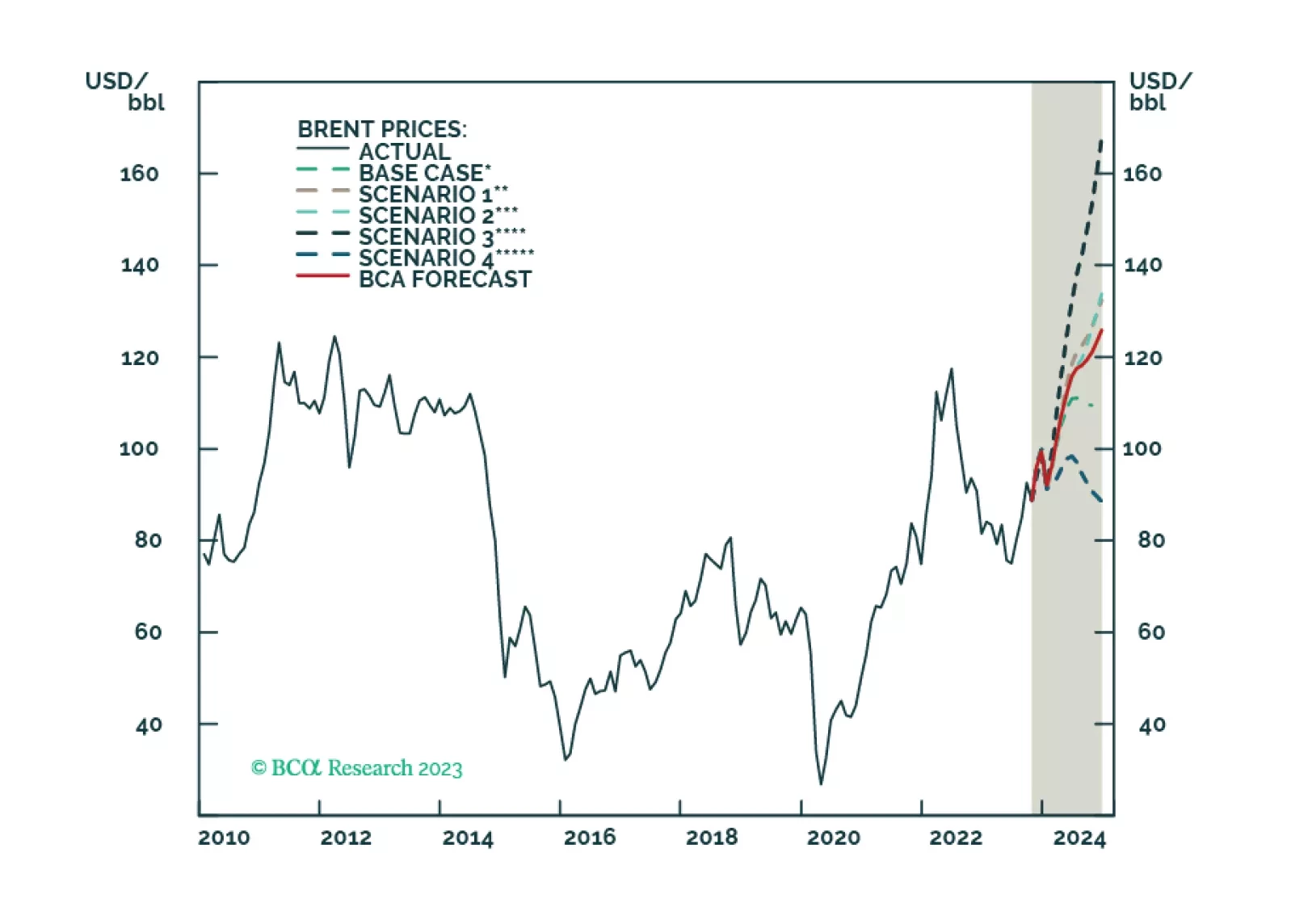

US and Chinese oil-demand strength will offset EU weakness next year. Incremental supply growth from non-OPEC 2.0 producers, coupled with a lower risk of the US enforcing its sanctions on Iranian oil exports, reduces our 2024 Brent price forecast by $6/bbl, and takes it to $112/bbl.

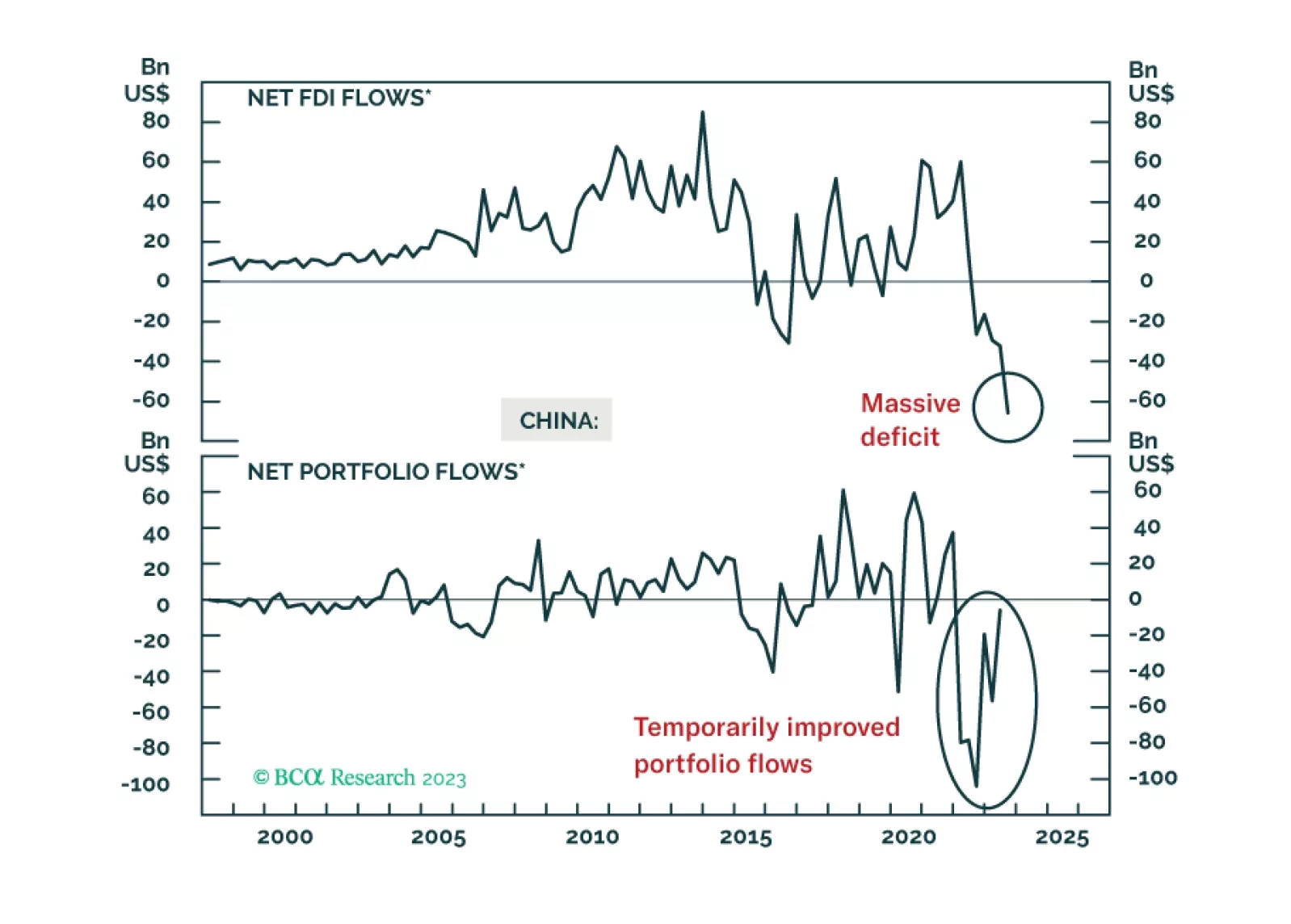

China’s capital outflows will likely remain substantial at least through the next few quarters. This wave of capital outflows will likely be more chronic, albeit less acute than the 2015-16 episode. Persistent capital outflows will exert downward pressure on the RMB.

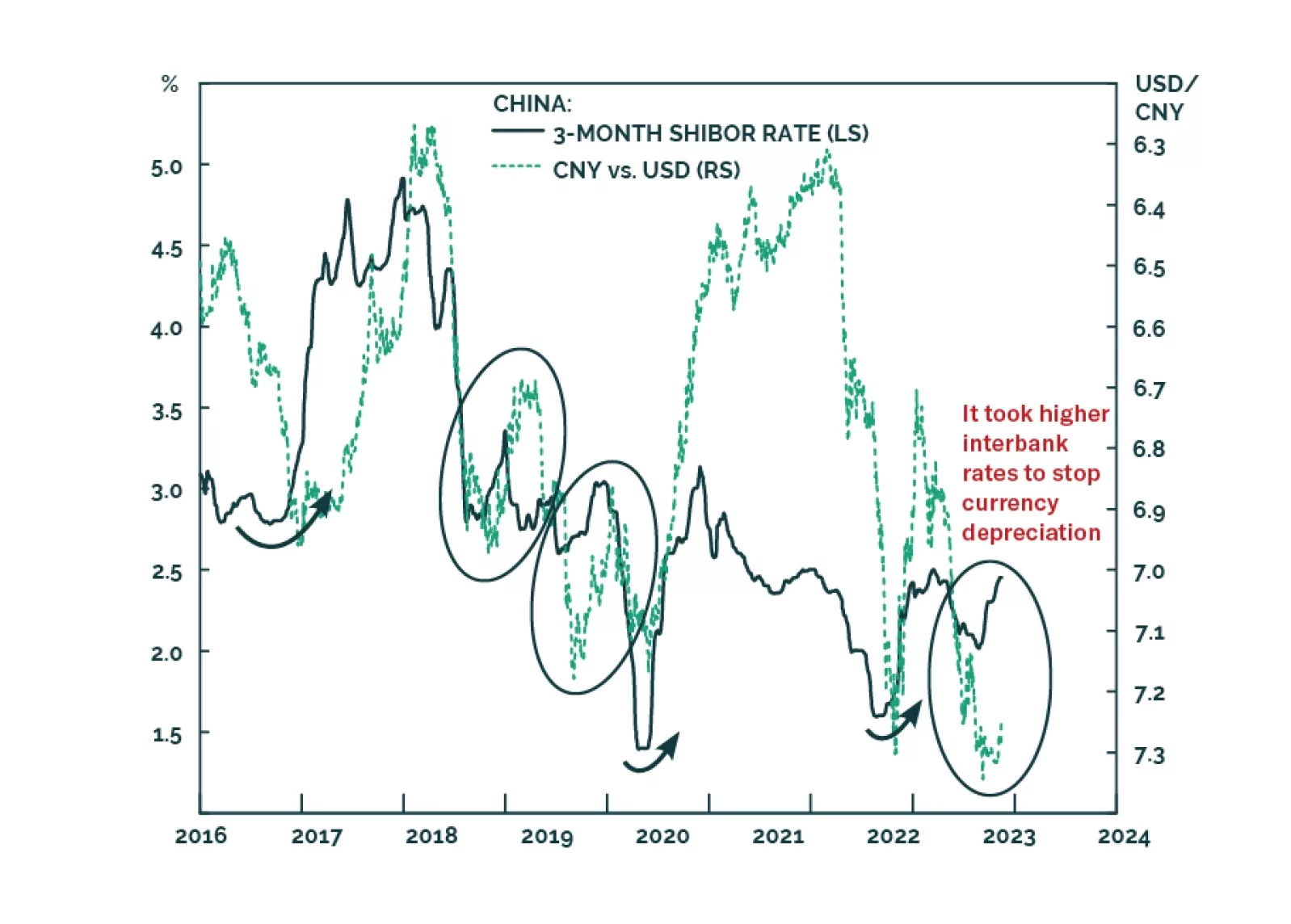

Many commentators have attributed the latest increase in Chinese interest rates to an improving economy, the large issuance of government bonds, the tax payments season, and other technical factors. Yet, these explanations are missing the key point: the PBoC has steered interbank rates higher to defend the currency. Higher borrowing costs are the last thing the mainland economy now needs.

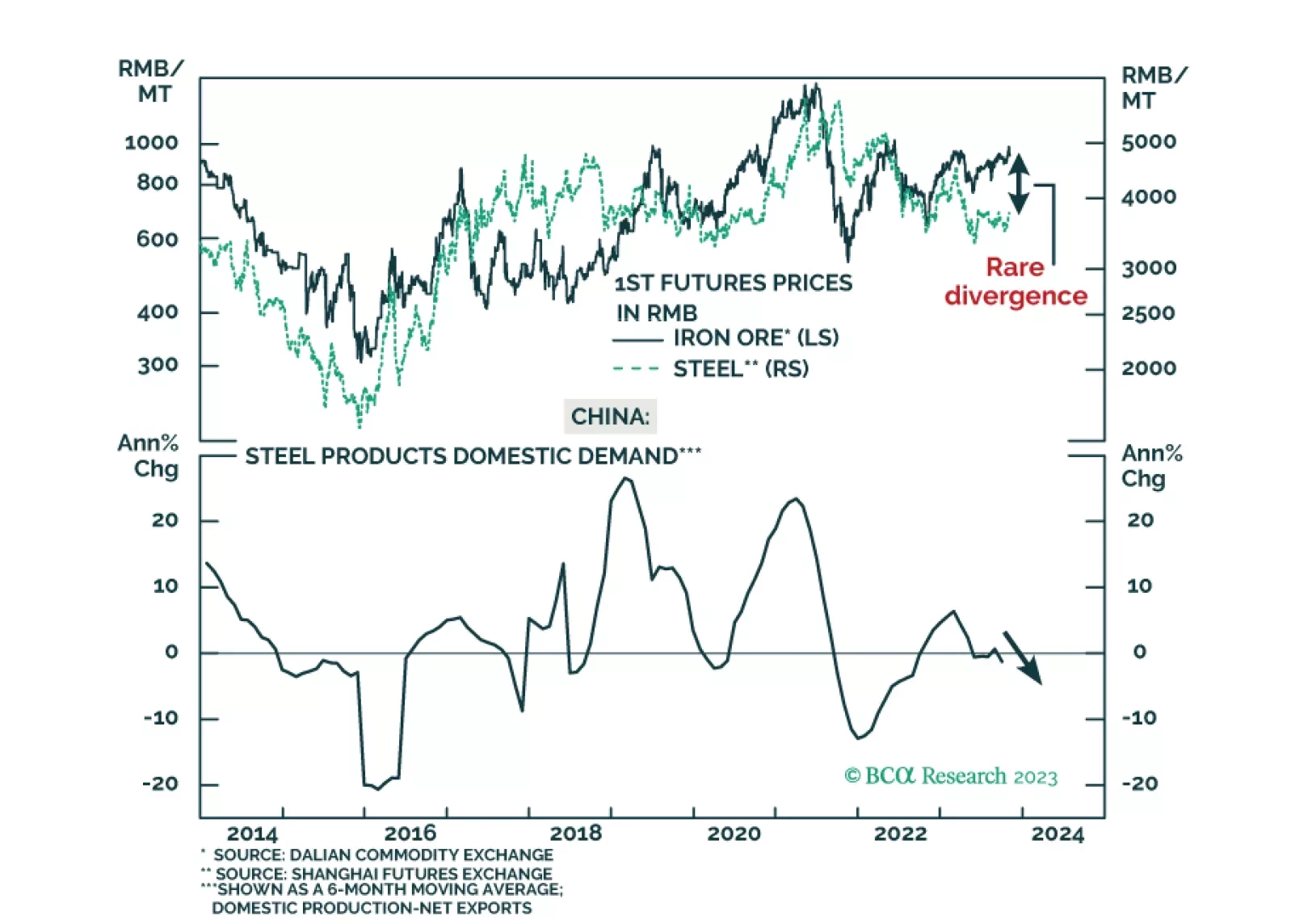

Increasing iron ore prices coupled with declining steel prices represent an unsustainable disparity. Iron ore prices will pivot downward in the next six months. A sizeable reduction in China’s steel production will likely occur, reducing global iron ore demand. Meanwhile, global iron ore supply will increase moderately.

In financial systems, cracks typically begin on the periphery and then expand to the center. Hence, the ruptures on the fringes often act as an early warning. These fissures tend to widen and spread to the core, causing a breakdown in the S&P 500. Investors should consider buying US Treasurys aggressively when the S&P 500 slips below 4,000.

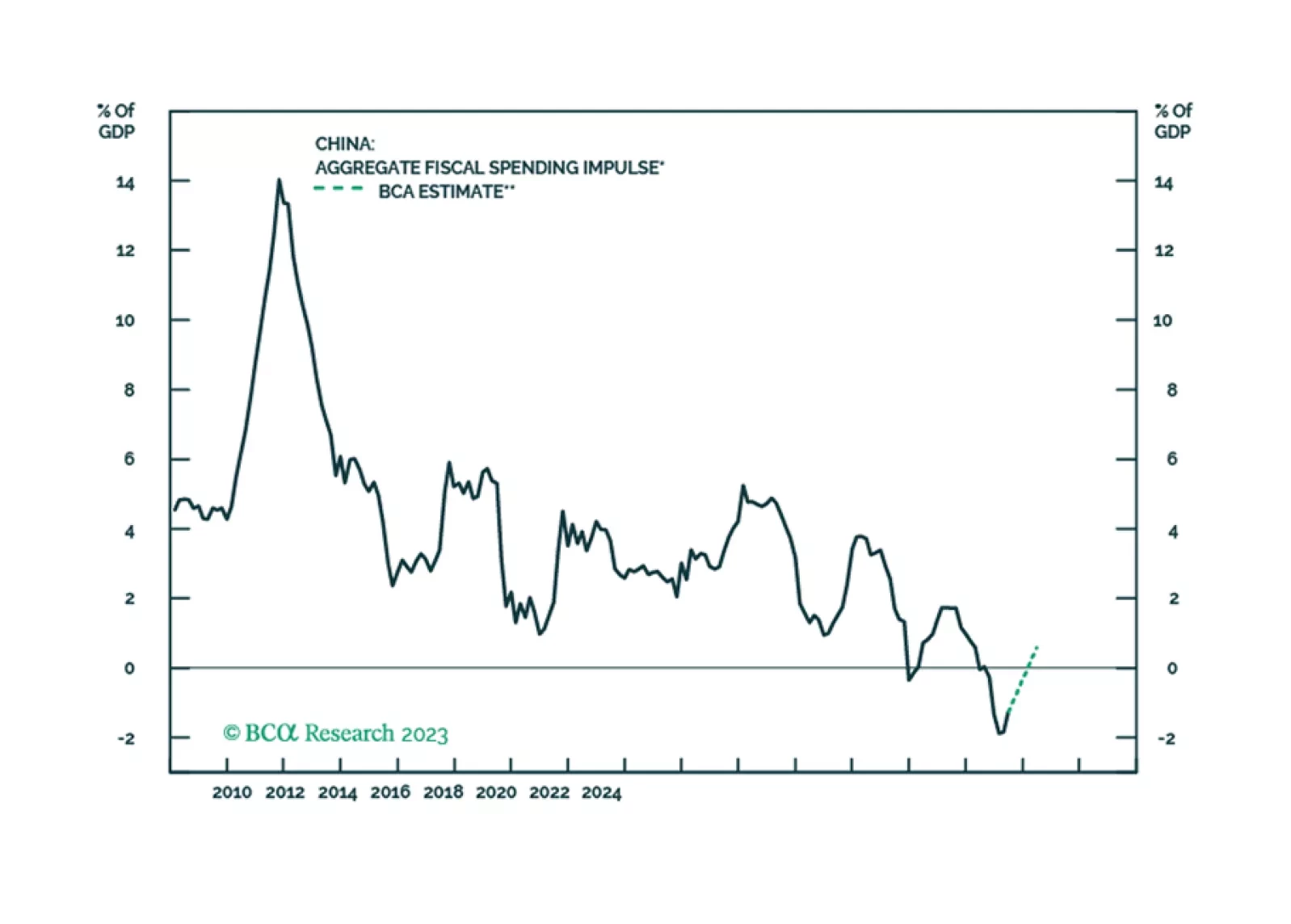

We maintain our view that China’s economic growth in the coming months will remain lackluster. Beijing's recent measures to provide additional financing may help to bridge the gap in government spending in the rest of 2023 and into 2024, but the impact on growth will be very limited.

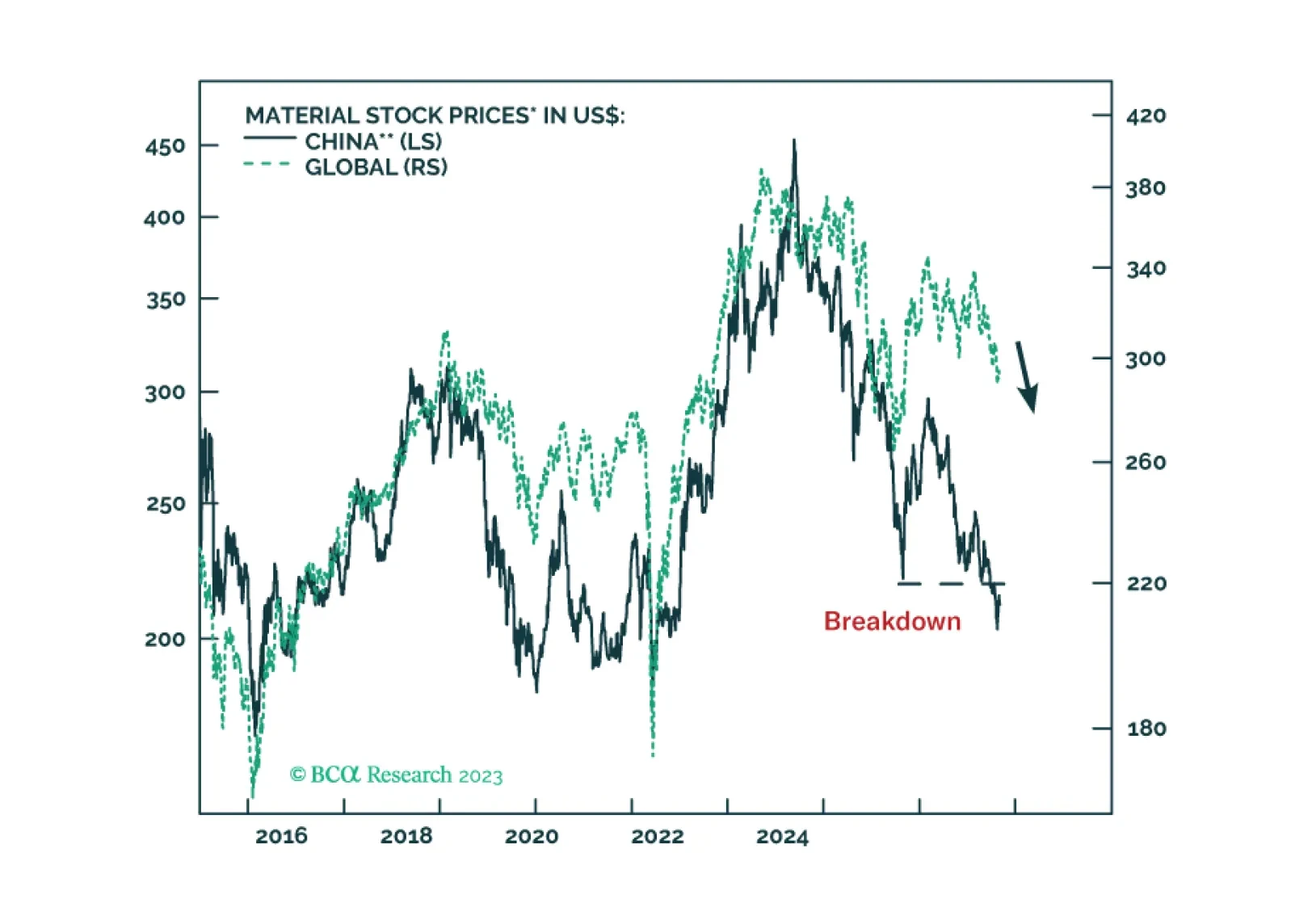

China’s economic growth will stagnate, at best, rather than revive. Lower valuations of Chinese equities are justified, and share prices have more downside. The RMB will continue to depreciate versus the US dollar.

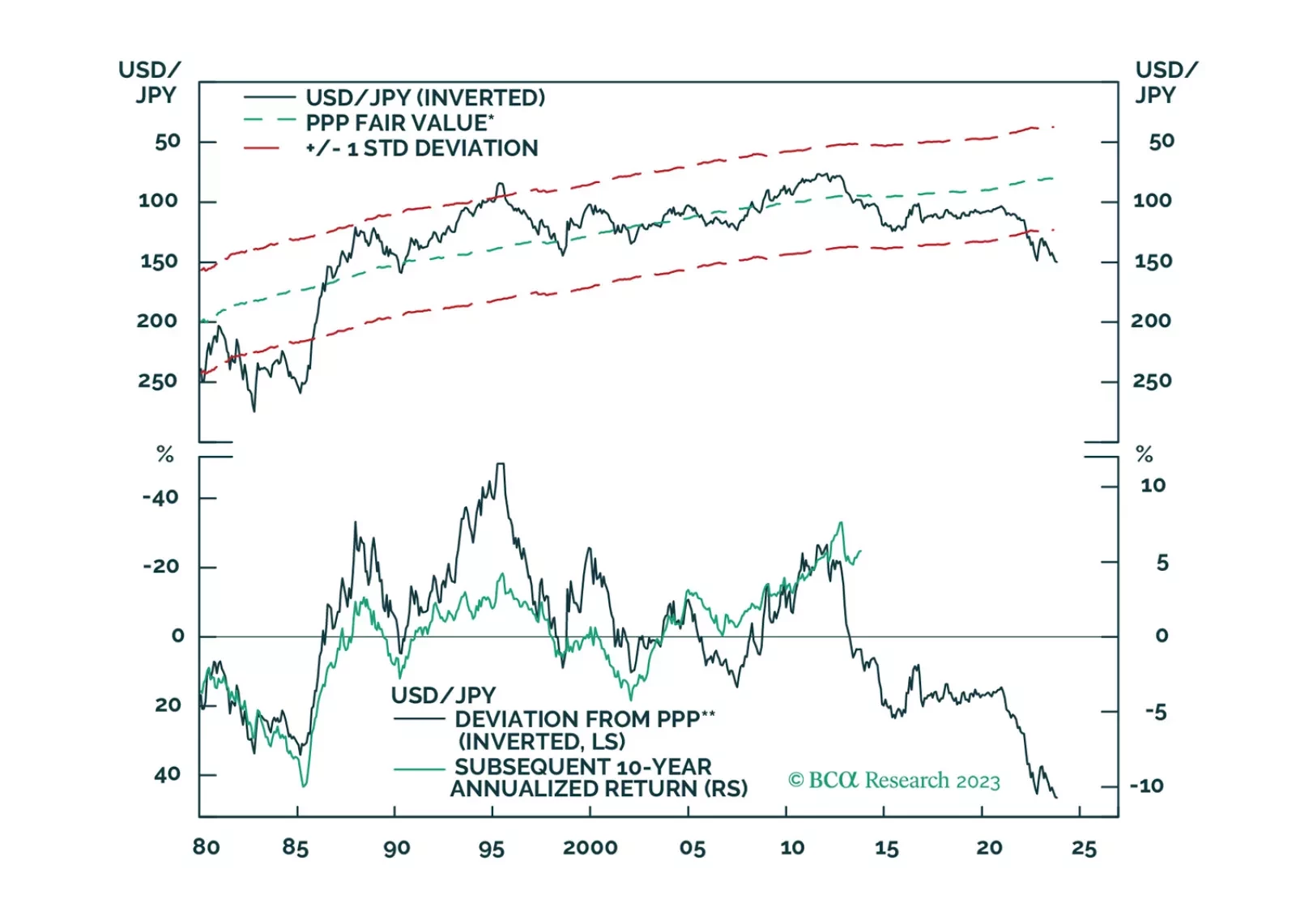

There is a high probability that the global economy will tip into recession in the second half of 2024. A long yen position is an excellent hedge against that risk.

As global financial institutions like the IMF draw attention to the real-estate crisis in China, the CCP will be forced to step up regulatory and restructuring efforts to contain its spread and limit further contagion domestically and globally. The Party also will be forced to deliver stronger fiscal- and monetary-policy support to beleaguered banks and developers. We expect it to do so, which keeps us bullish energy and metals. Failure raises the odds of a collapse in the property markets, which would be socially destabilizing, and lead to greater risk aversion and volatility globally.