China Stimulus

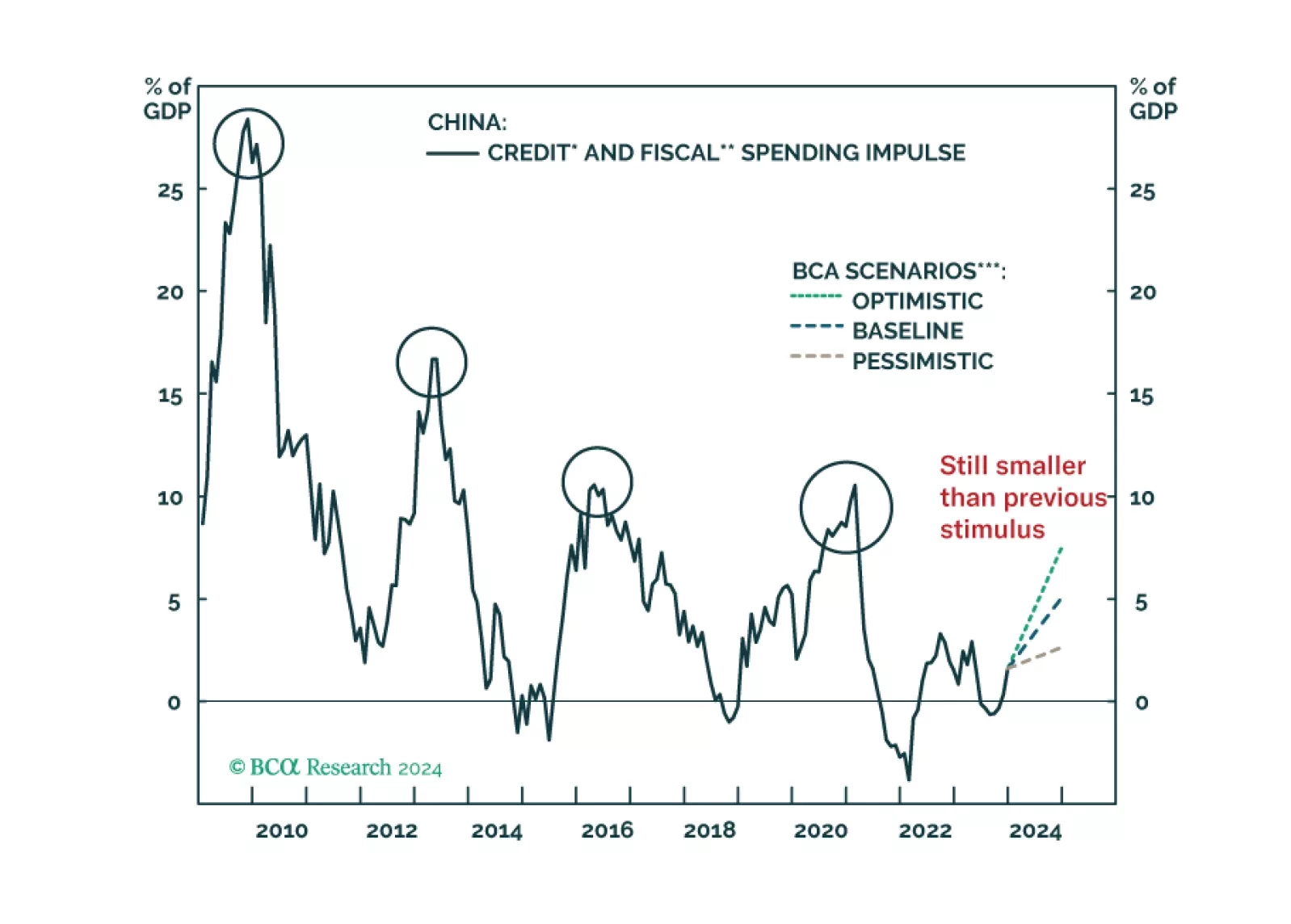

The stimulus measures announced at last week's NPC were not a game changer. As in 2023, we expect aggregate government spending will fall short of the budgeted amount again this year.

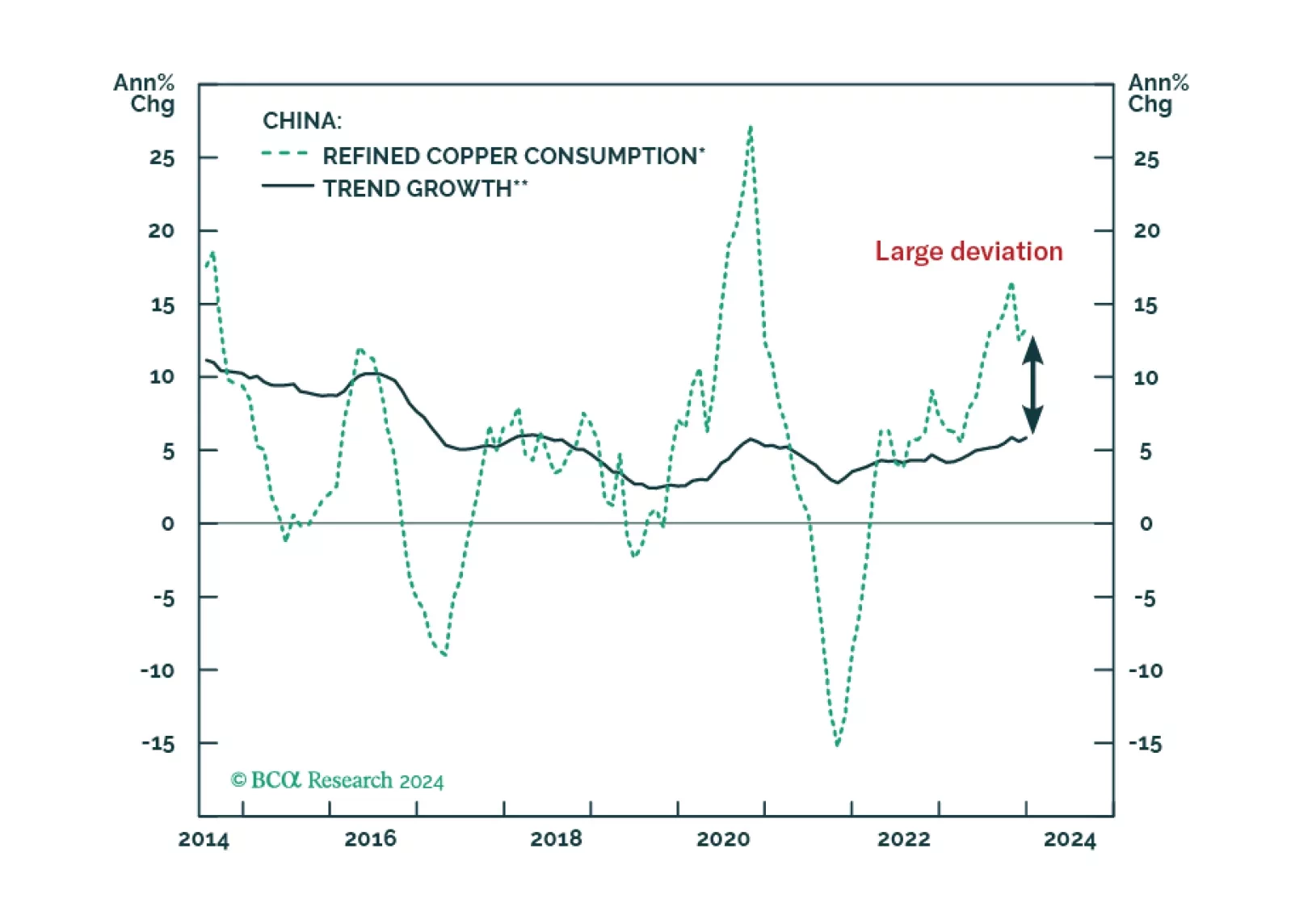

On the one hand, China’s copper intake boomed last year despite the travails of the mainland economy and shrinking property construction. On the other hand, global copper supply mushroomed despite persistent worries about supply shortages. This report uncovers this puzzle and elaborates on the outlook for copper prices. The conclusion is that red metal prices are still vulnerable.

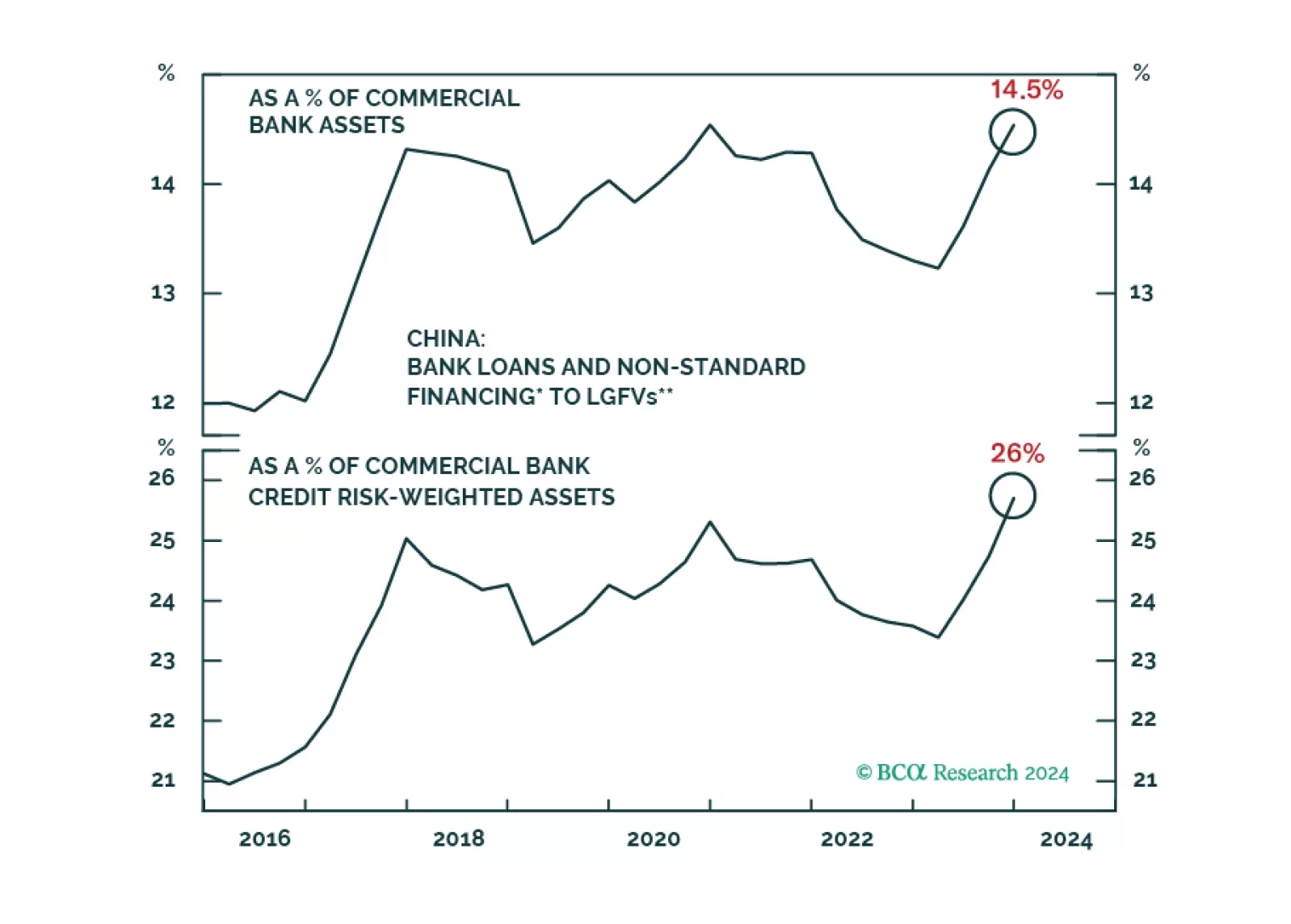

The odds of a “Minsky Moment” for the Chinese banking sector are low. They, however, will continue facing cyclical and structural headwinds, including a dismal asset quality and profit outlook. Bank stocks remain a value trap. Absolute-return investors should sell rebounds in Chinese bank stocks.

China will continue to suffer from a “triple crisis”. Though there could be a tactical bounce, cyclically we still recommend underweighting Chinese equities.

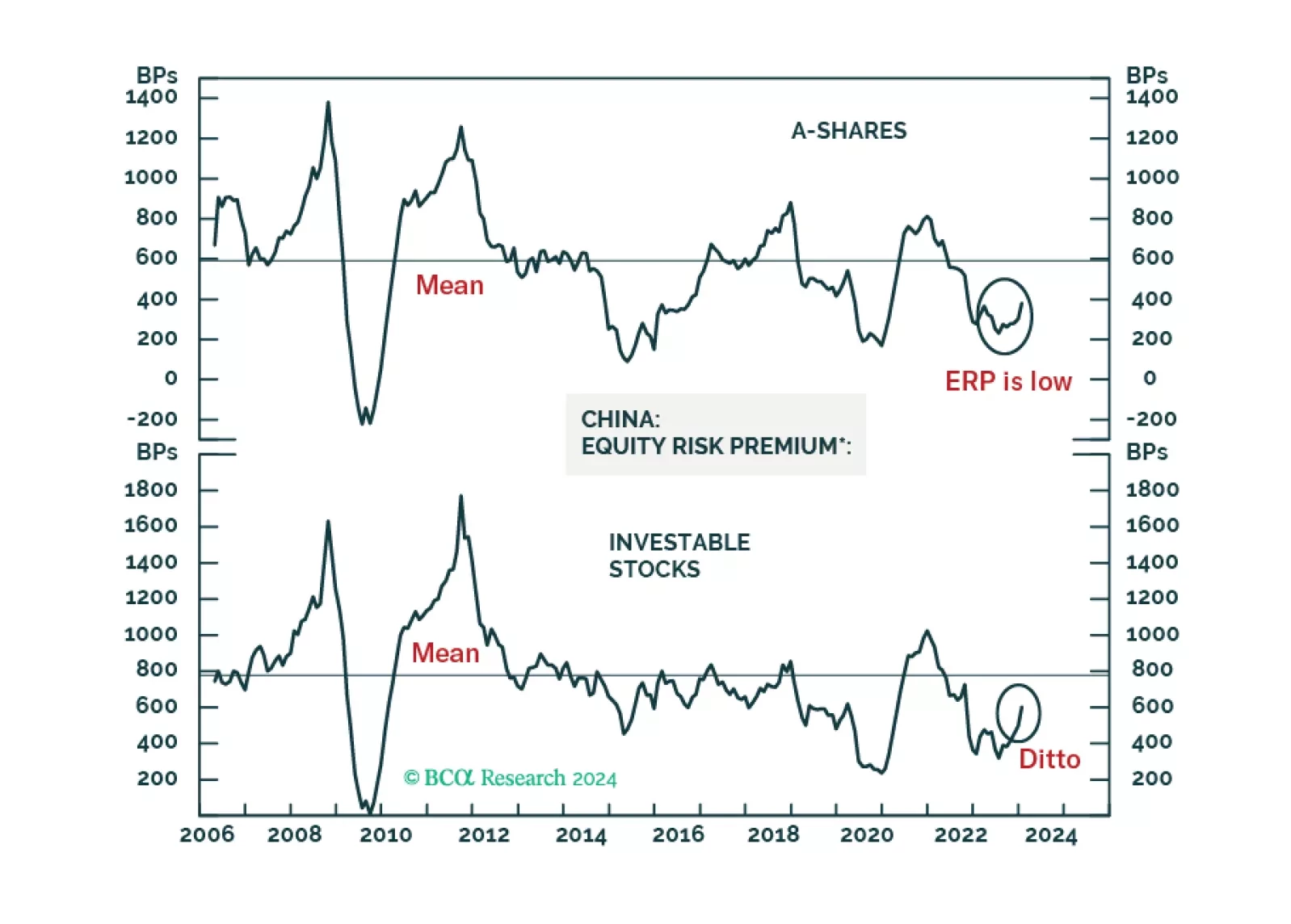

Chinese A-shares will probably begin forming a volatile bottom. The basis is that authorities will likely throw the kitchen sink at the onshore market in an attempt to stabilize share prices. The same is not true for offshore listed stocks. Hong Kong-traded Chinese share prices will likely continue to fall. Beijing is less concerned with offshore stocks as their holders are primarily foreign investors.

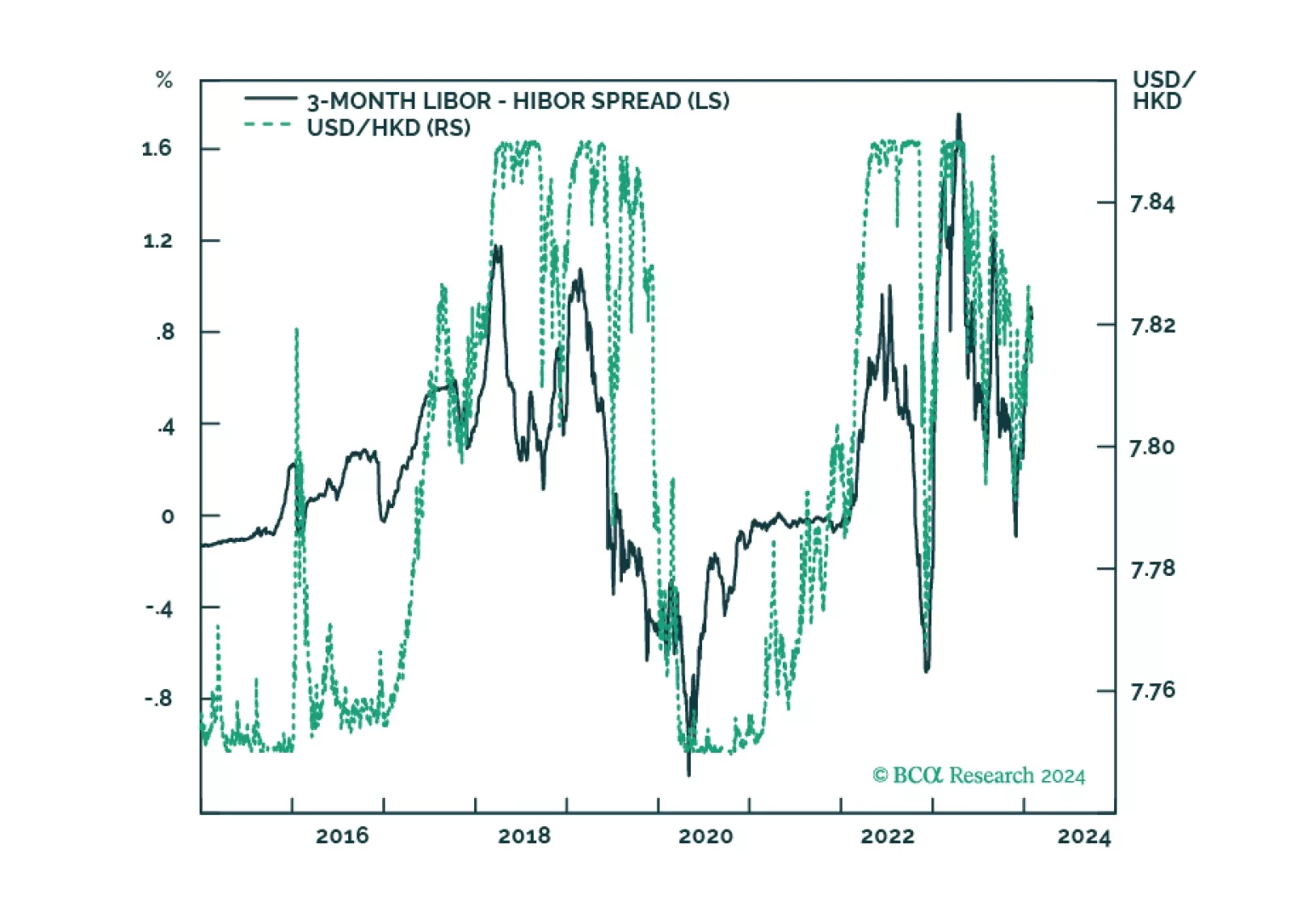

In this Special Report, we update our thinking on the Hong Kong SAR dollar peg, with implications for domestic asset markets.

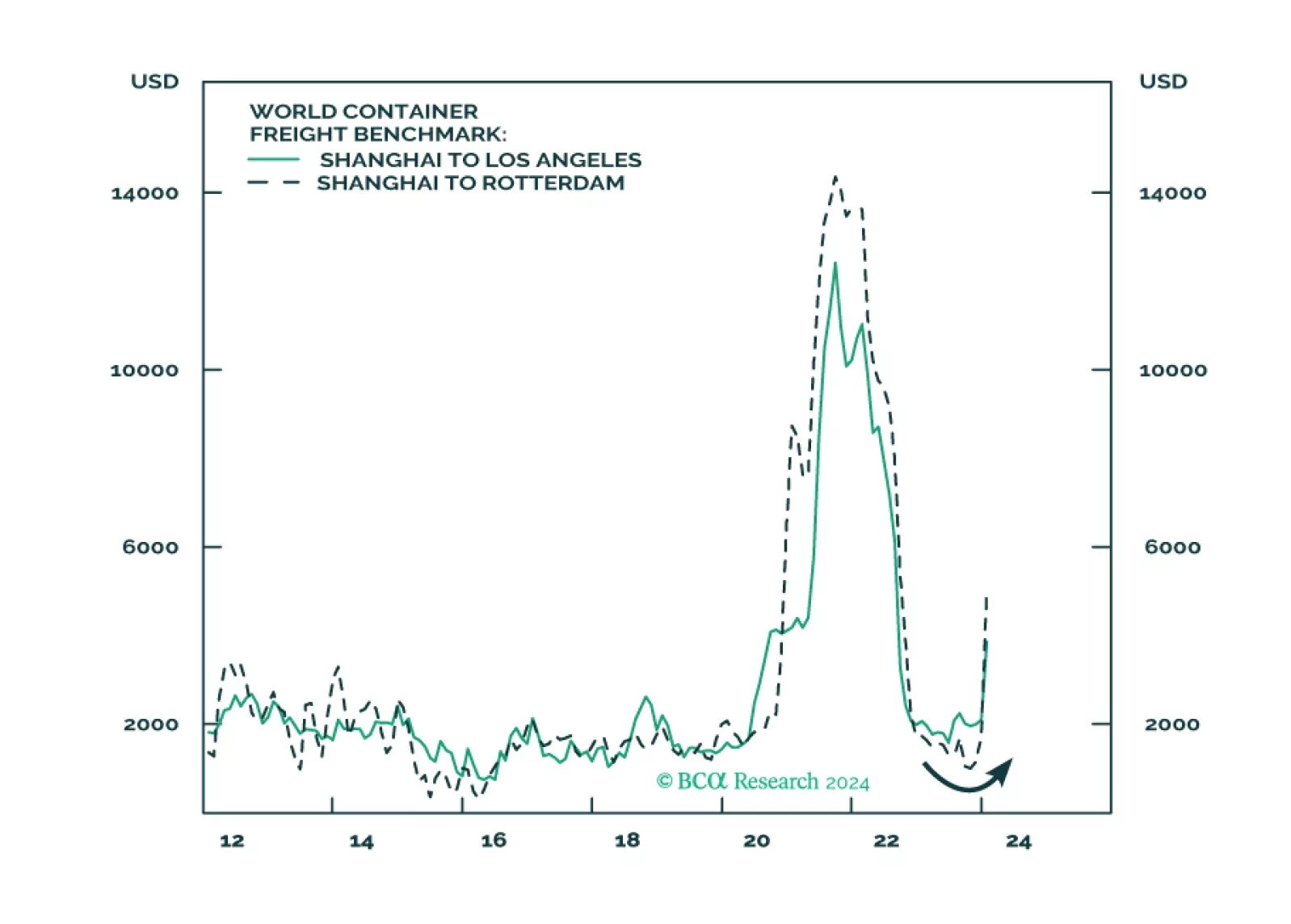

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.

Middle East conflict, extreme US policy uncertainty, Chinese economic slowdown, US-Russian proxy war, and Asian military conflicts do not create a stable investment backdrop for 2024. Our top five “black swan” risks may be highly improbable, but they stem from these underlying trends.

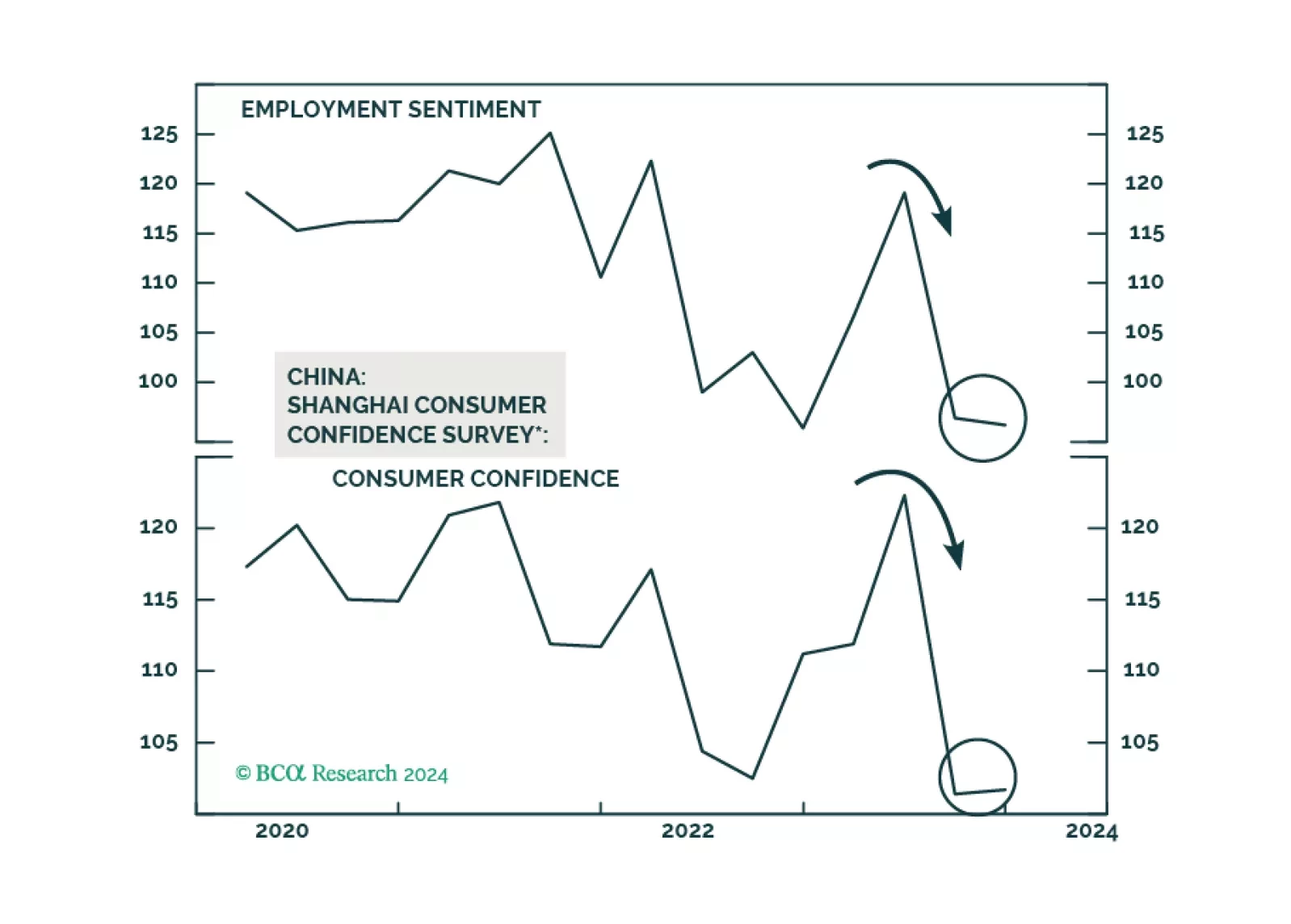

There is no easy way for China to forestall deflation. Provided policymakers are still reluctant to unleash large-size stimulus, more economic disappointments are likely in the coming months, and Chinese stocks will continue to sell off. The yuan is at risk of further depreciation versus the US dollar.

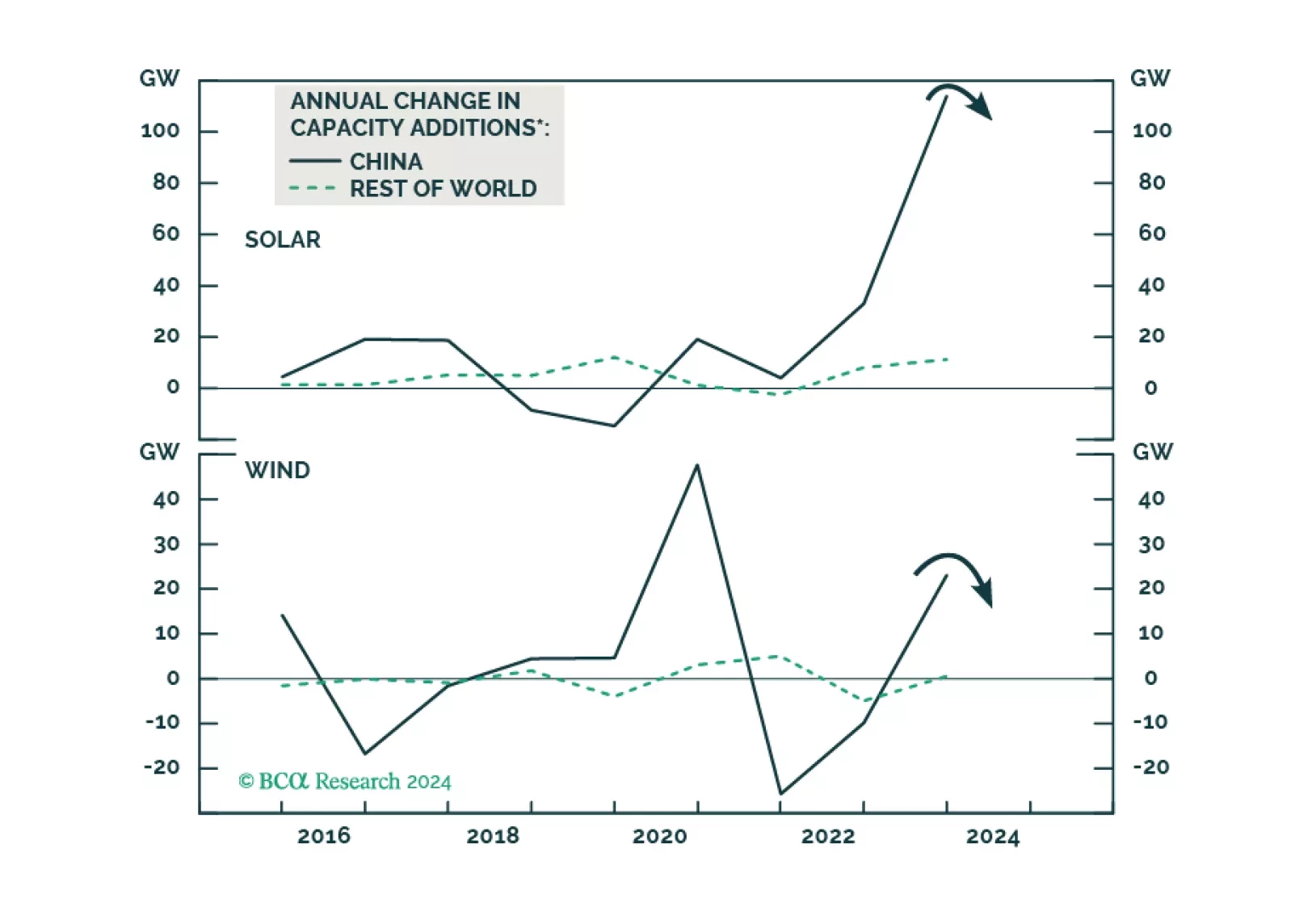

The global green energy rush faces mounting headwinds. Additional global solar and wind capacity installations will have considerable growth reduction this year. Copper prices did not drop much in 2023 due to surging demand from green power build-up. Green power will be less positive for copper demand in 2024 than in 2023. We expect more downside in global renewable energy stocks.