China Stimulus

China's cyclical and structural headwinds will likely undermine Beijing’s initiative to accelerate urban migration over the next five years.

This report provides our framework for interpreting the messages from last week’s Third Plenum, and the potential implications for the economy and investors.

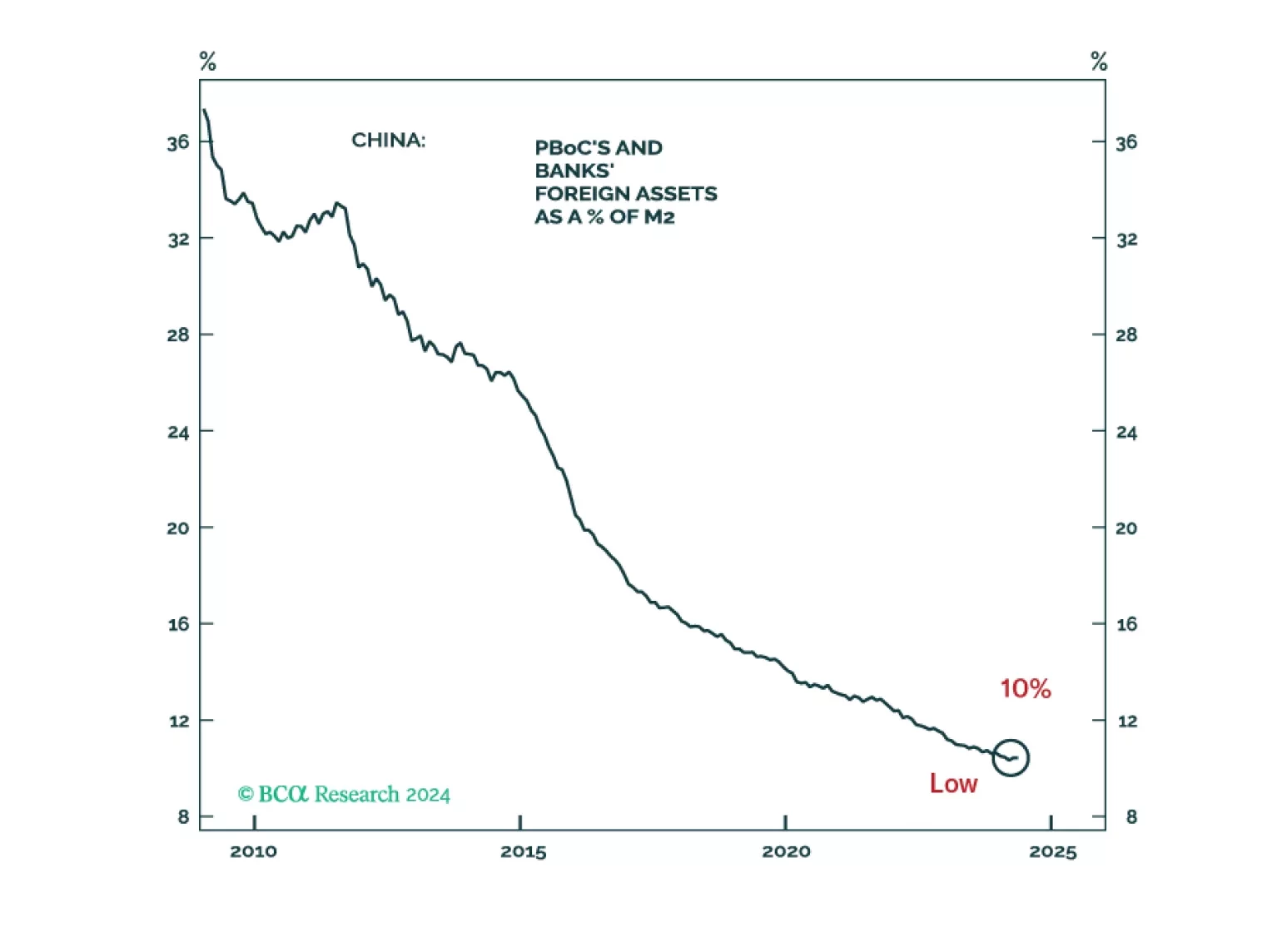

Is the RMB cheap or expensive? Based on trade accounts, the yuan is inexpensive, but the RMB is vulnerable due to capital outflows. Yet, Beijing will not resort to a rapid devaluation for now, and the option of floating the currency is improbable. The PBoC will allow a gradual depreciation of the yuan versus the dollar, say around 5%, in the next six months.

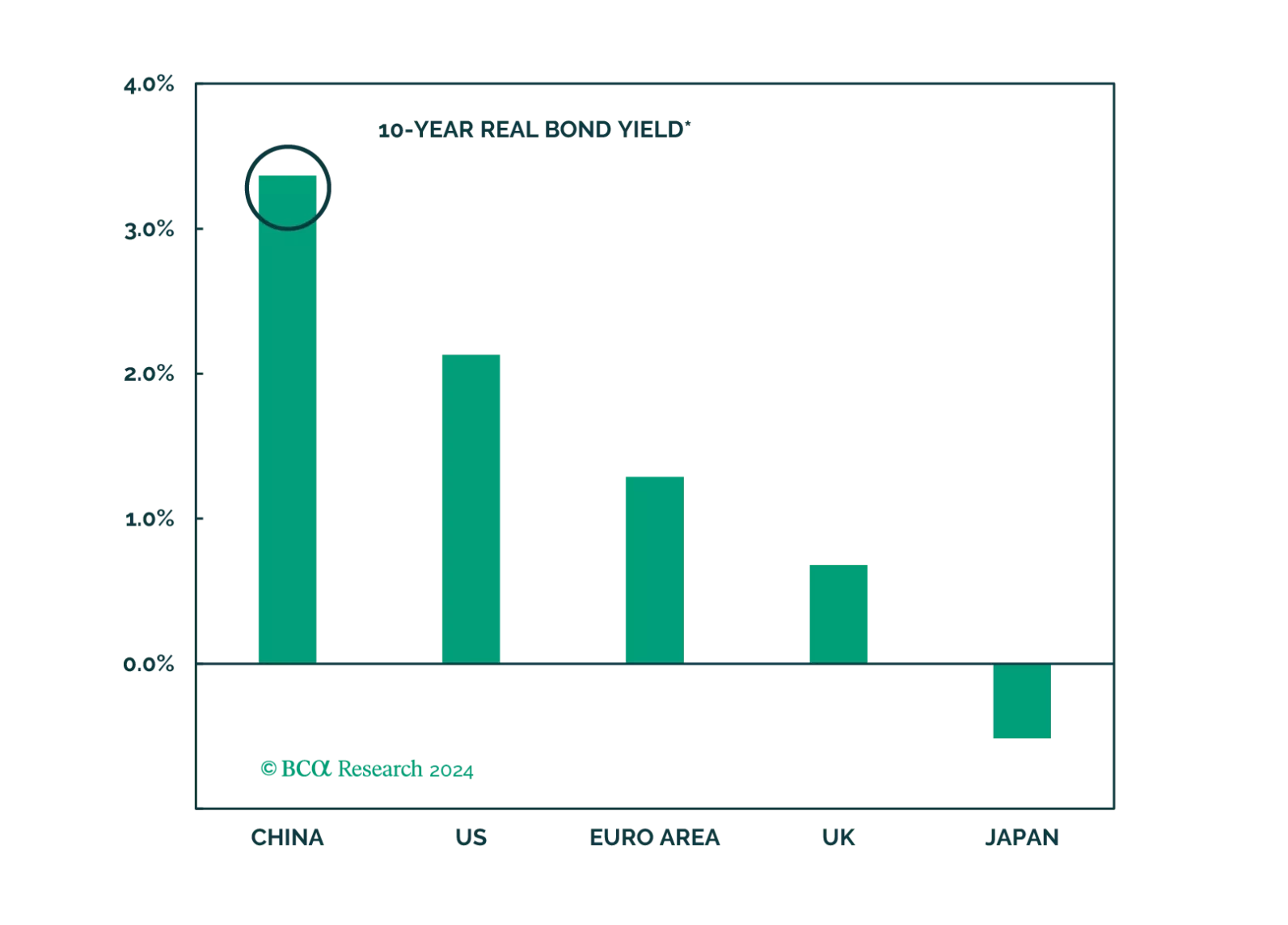

The PBoC appears increasingly uncomfortable with the rapid decline in the Chinese government bond yields. While the PBoC will succeed in temporarily curbing investors’ enthusiasm for bonds, the central bank will be unwilling to raise interest rates and unable to intervene in the bond market in any meaningful and lasting way.

The green energy transition will drive a surge in copper demand over a long-term horizon. However, a better entry point to get long will emerge after the next economic downturn begins.

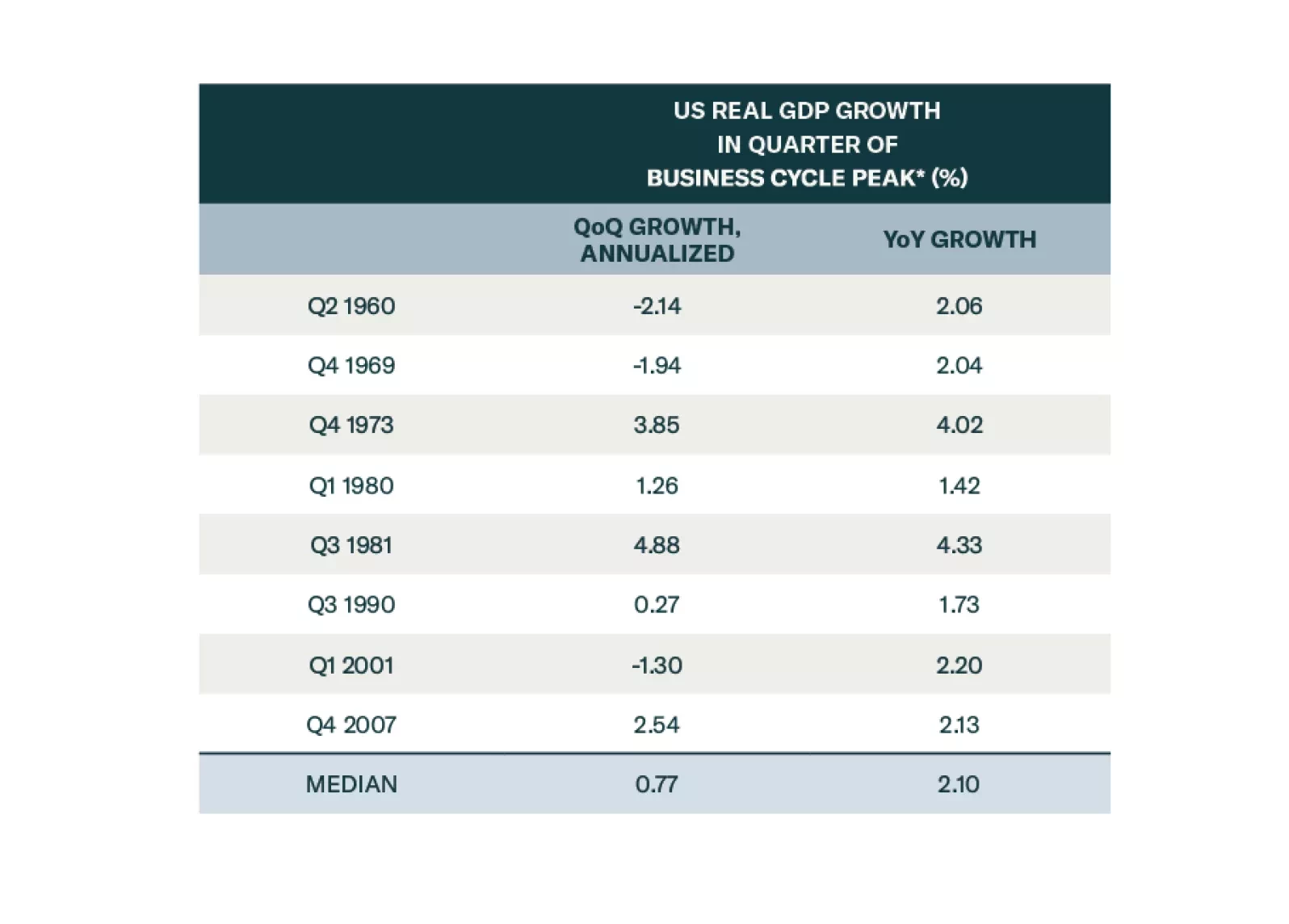

The consensus soft-landing narrative is wrong. The US will fall into a recession in late 2024 or early 2025. We were tactically bullish on stocks most of last year, turned neutral earlier this year, and are going underweight today. We conservatively expect the S&P 500 to drop to 3750 during the coming recession.

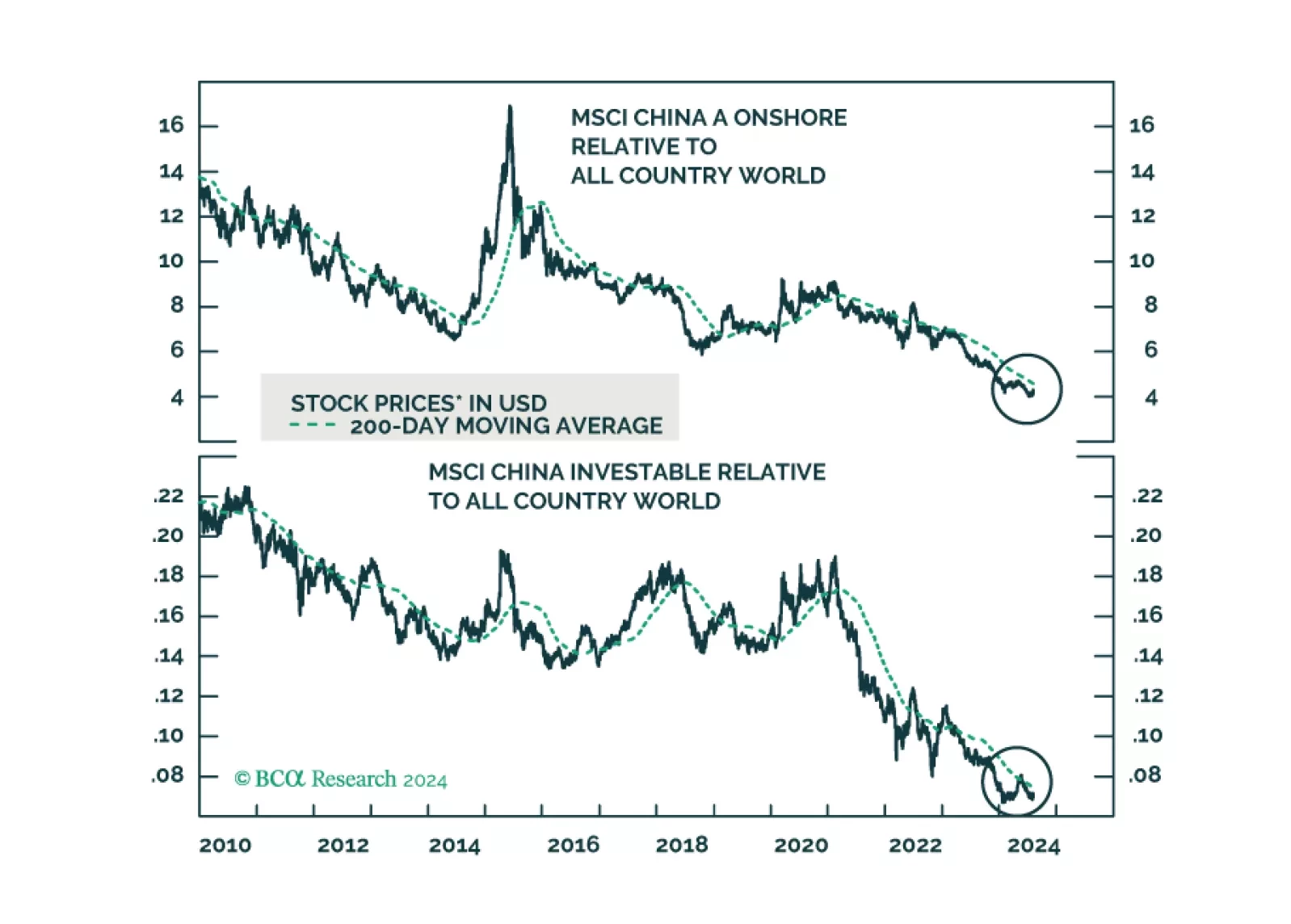

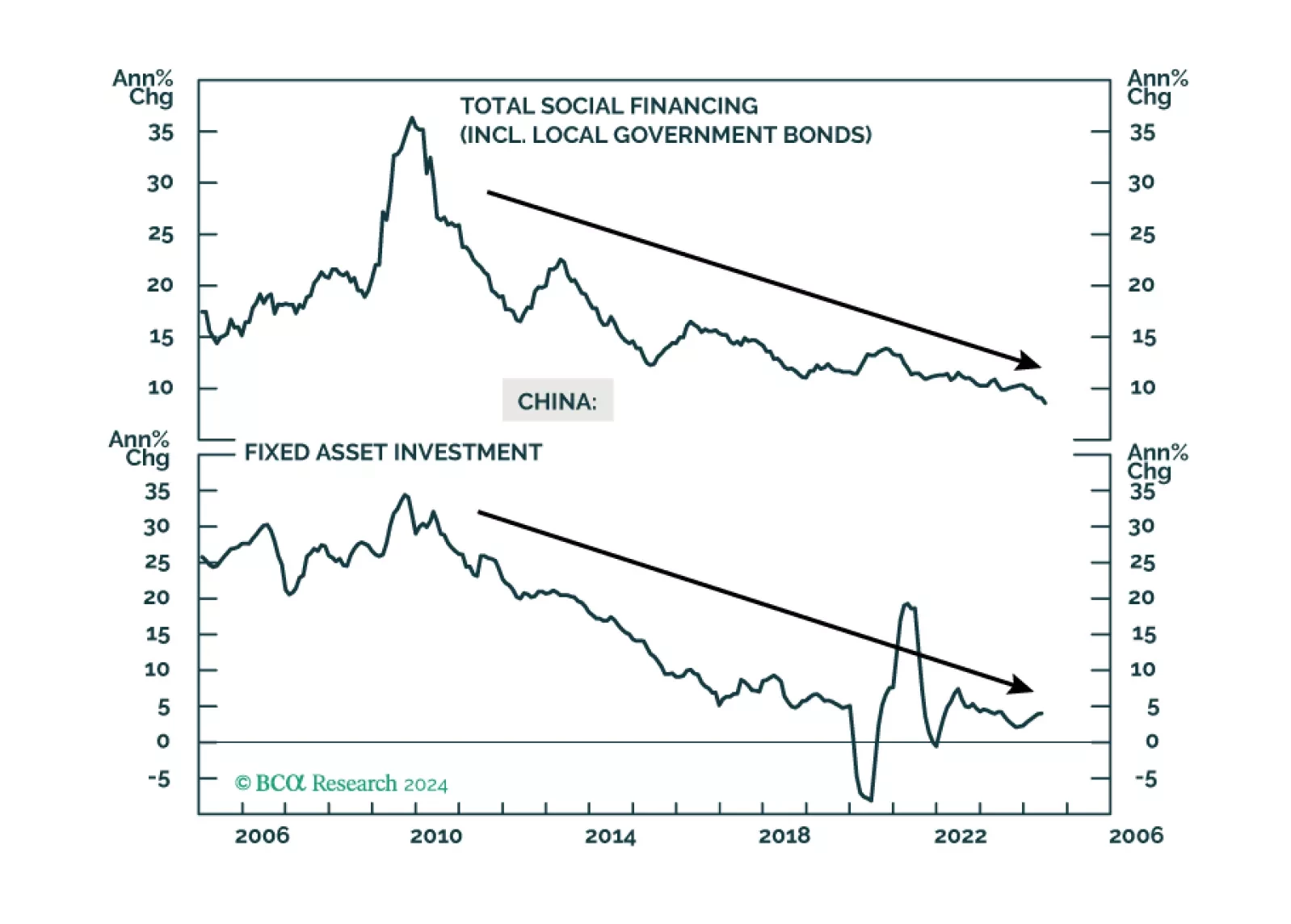

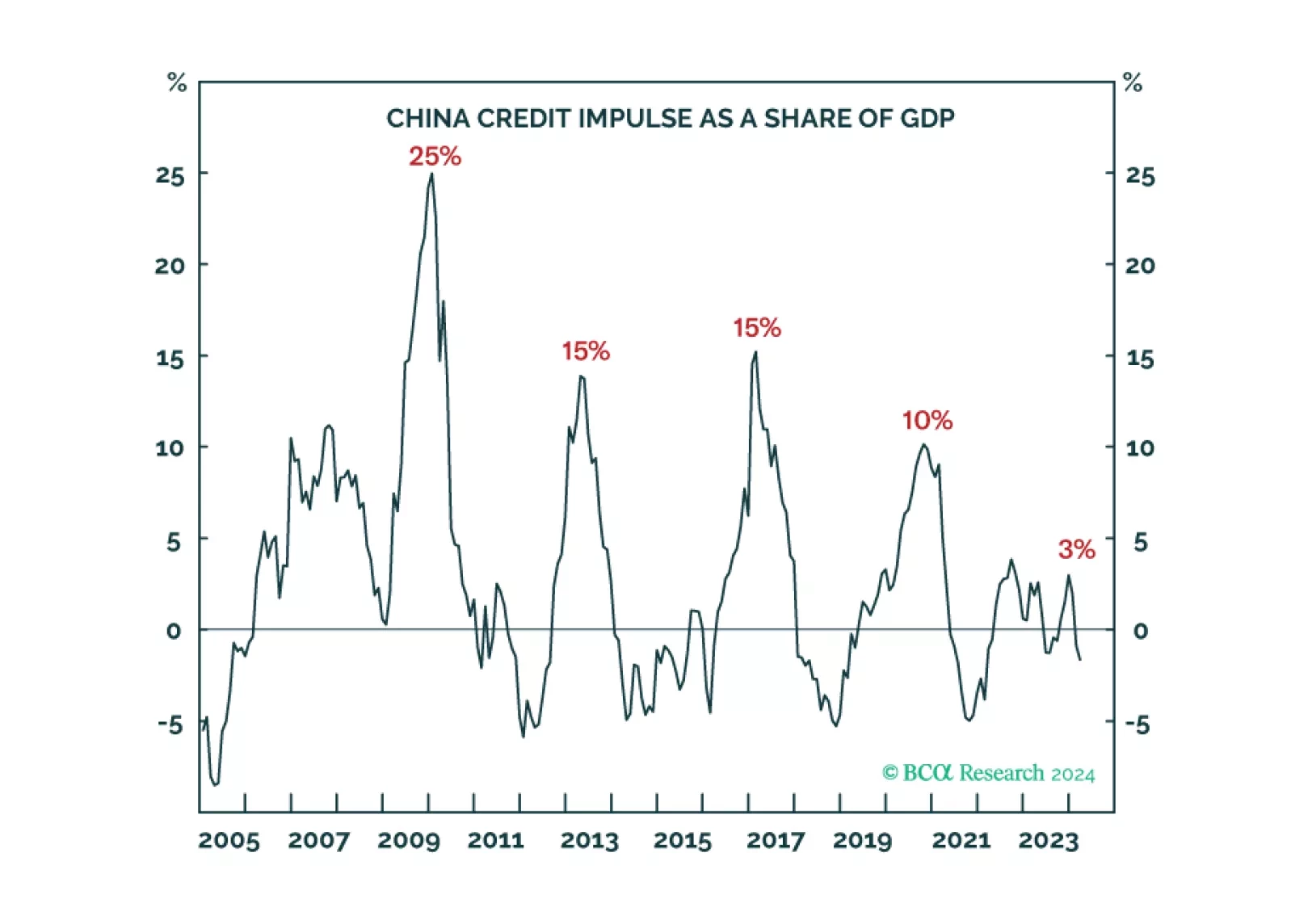

The end of China’s exponential credit growth will impede structural rallies in Chinese stocks and commodities, but US superstar stocks’ bubble-like valuations will impede them too. Leaving European stocks as the likely structural outperformer. Plus: copper is correcting, NVDA is consolidating.

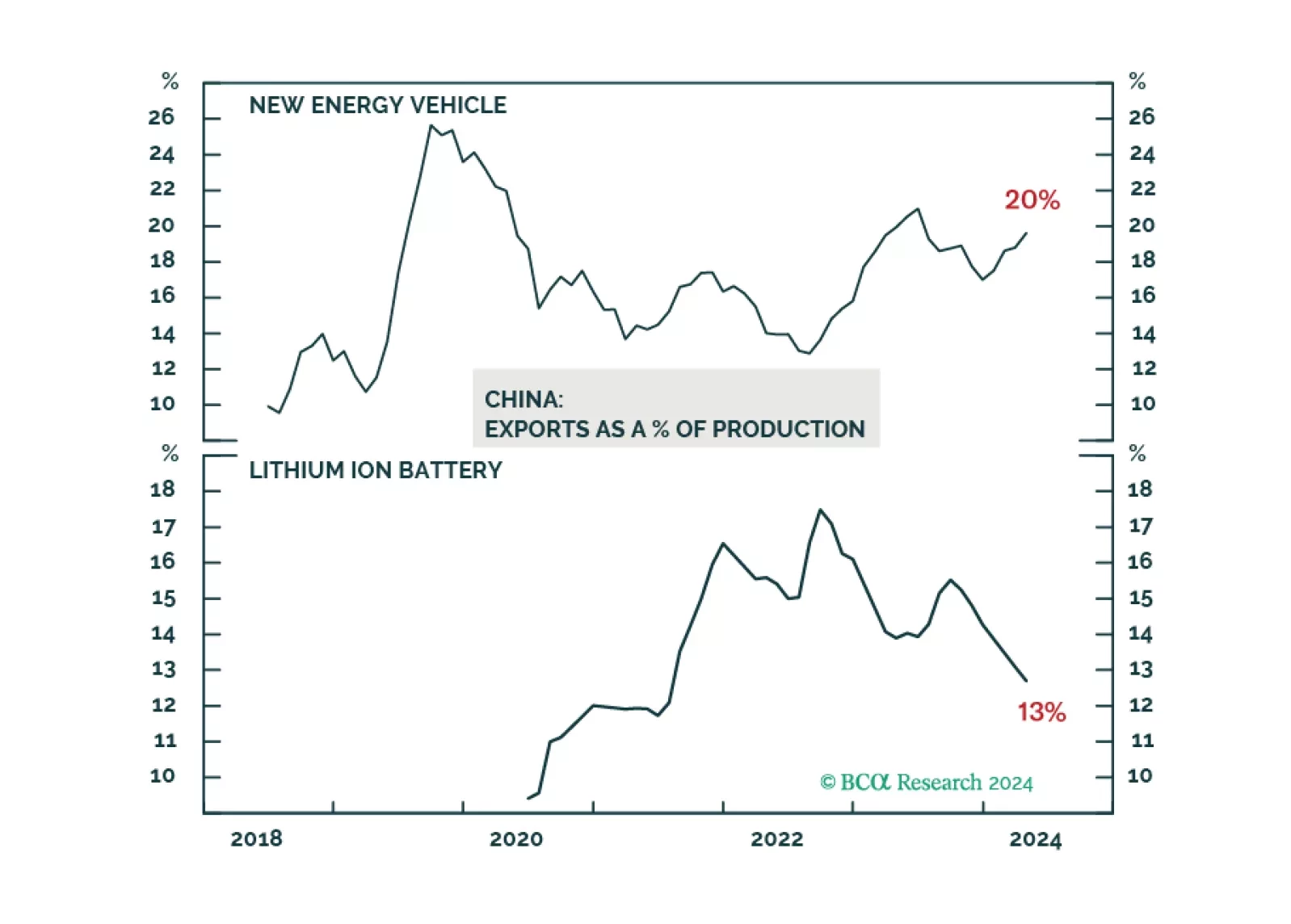

The EU's import tariff increases on Chinese EVs are expected to have a minimal impact on China's overall exports. We anticipate that most Western-brand EV shipments from China will be less affected by the EU import tax hike. Beijing will likely pursue continued negotiations with the EU rather than resort to harsh retaliatory measures.

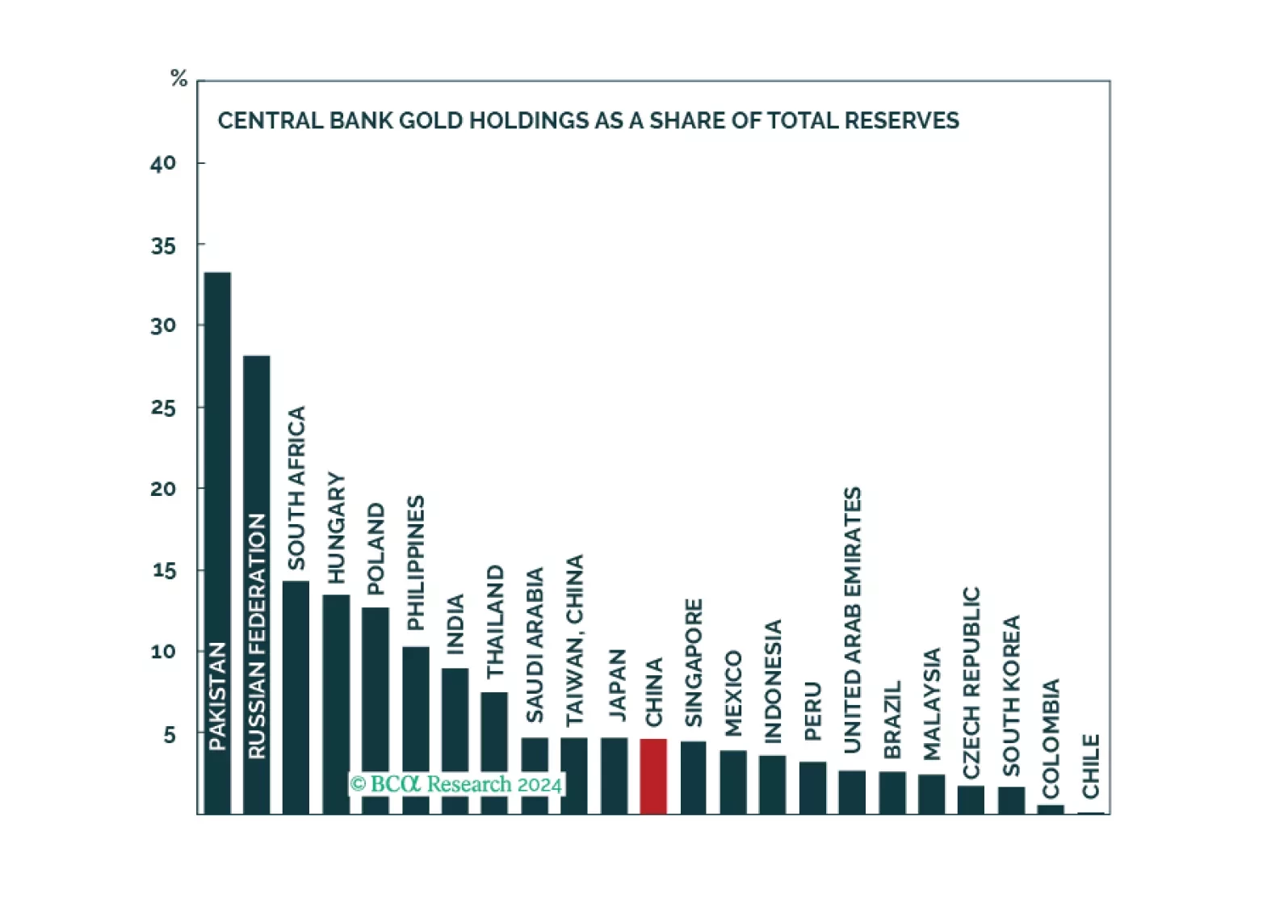

Gold prices might experience a correction or consolidation over the near term. However, cyclical and structural forces will ultimately cause the yellow metal to trend upwards.

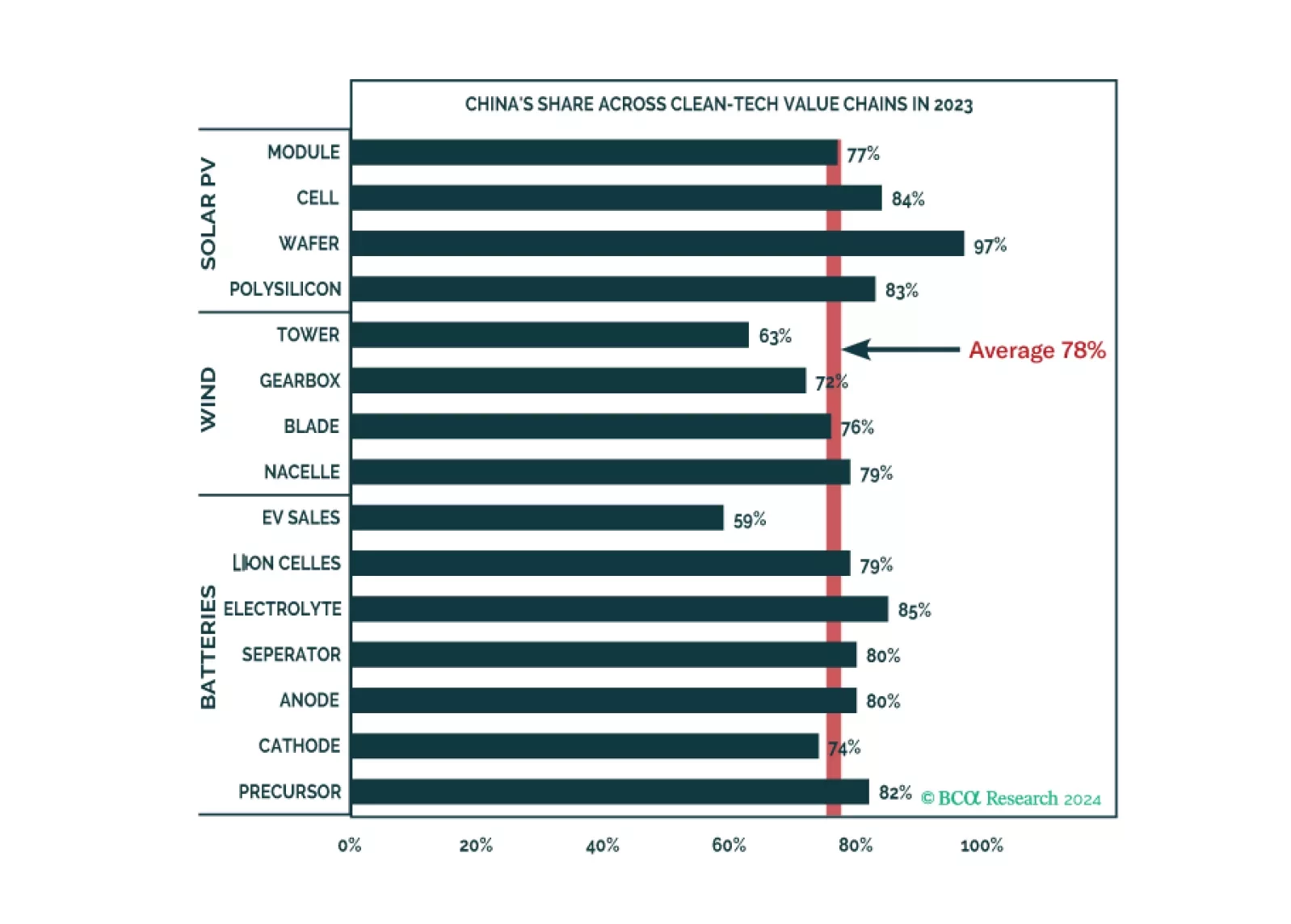

The issue of "industrial overcapacity" in China may be a misconception. Overcapacity in the old-economy sectors has largely diminished, while China's dominance in the global green-energy market reflects its technological advancements and innovations.