China Stimulus

We spent last week visiting our clients in China. In this report, we share some of the key questions from the client meetings as well as our responses.

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.

In this report, we discuss why we are lifting our US recession probability from 60% to 65% and explain why China’s latest stimulus announcements are welcome, but probably are “too little, too late.”

To produce a moderate economic recovery, at least RMB 3 trillion in additional government expenditures is needed in H1 2025. Our bias is that Beijing is not yet ready to launch such a massive fiscal support measure. Hence, volatility-adjusted equity returns in China will be poor.

The adrenaline from the recent policy stimulus might be sufficient to produce a window of outperformance for Chinese equities and China-plays in financial markets. However, this adrenaline will not extend to China's real economy. Net-net, we are upgrading the allocation to EM in a global equity portfolio from underweight to neutral.

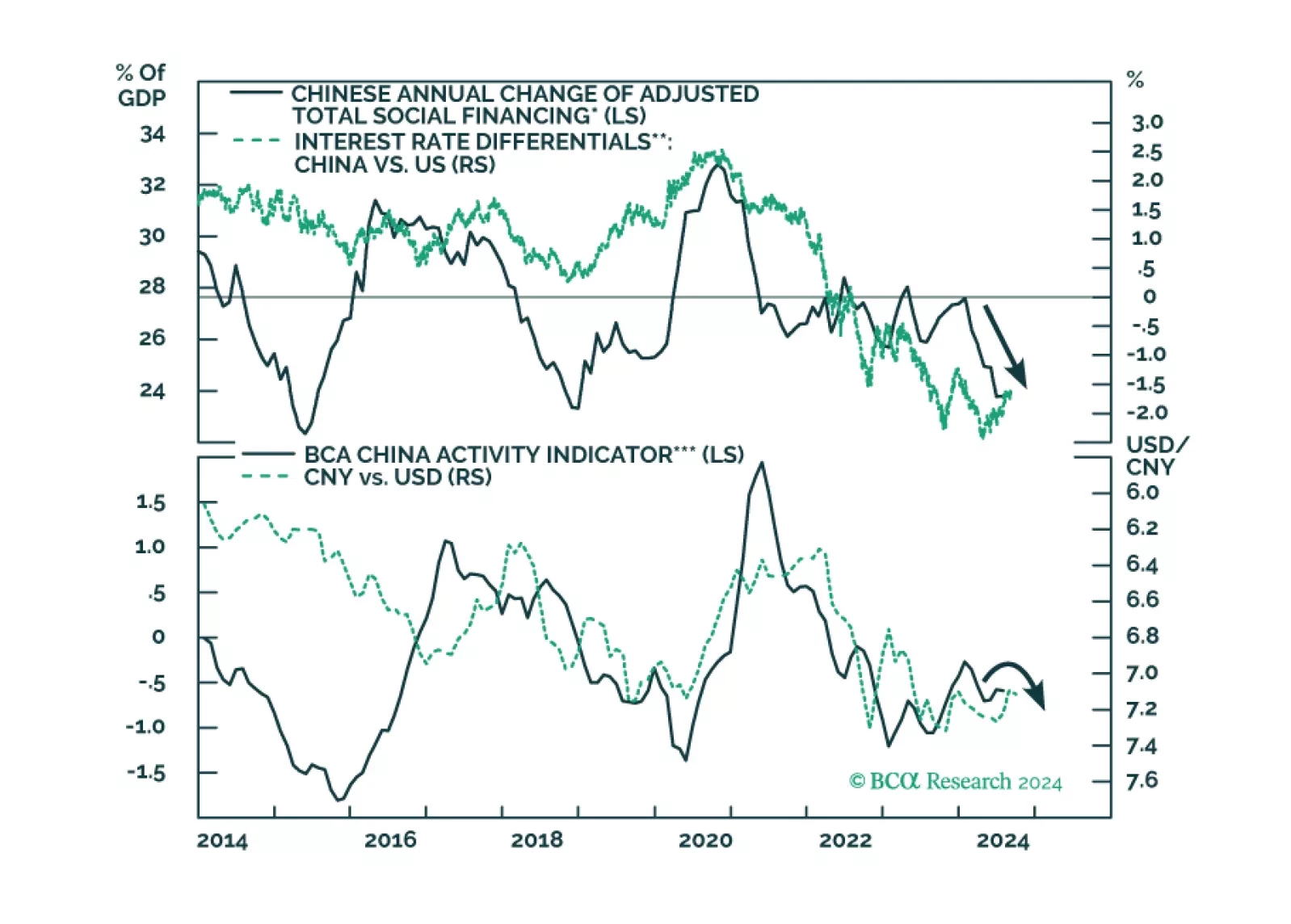

Both the Chinese and US central banks will likely take policy actions in the coming weeks. What is the potential impact of a mortgage rate cut on China’s household consumption and the broader economy? Will the anticipated Fed easing cycle further lift the RMB exchange rate versus the US dollar?

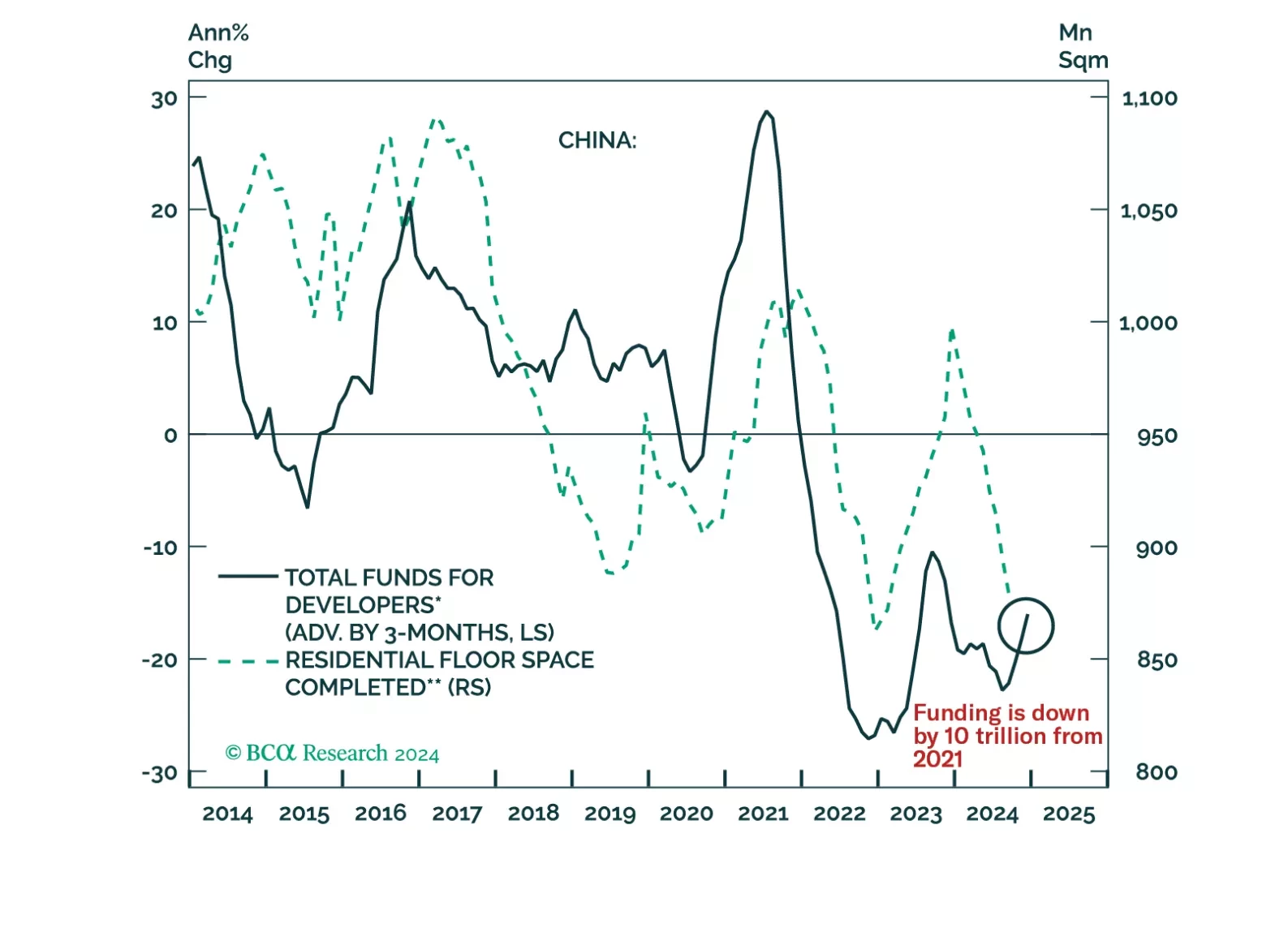

Chinese property developers will require at least RMB 500 billion in additional government funding to prevent further declines in housing completions for the rest of 2024. However, without addressing the underlying challenges, any new rescue measures similar to those announced in May are unlikely to effectively support the real estate market.

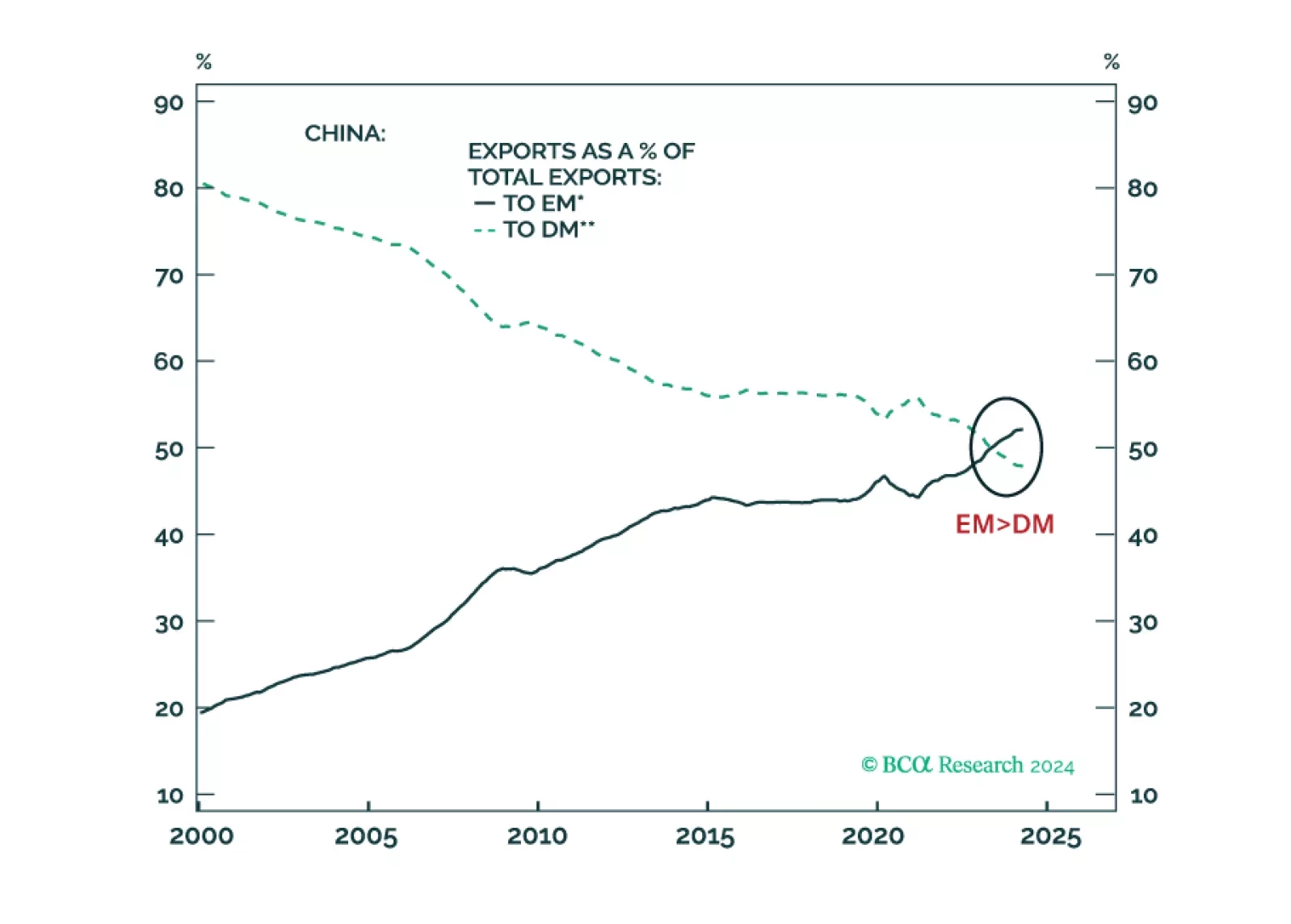

China has become less reliant on exports to advanced economies, and its products have successfully penetrated developing economies. Exports to the US make up 3% of Chinese GDP, while exports to all developing economies account for 10% of its GDP. China’s trade pivot from advanced to developing economies has economic, political, and geopolitical ramifications.

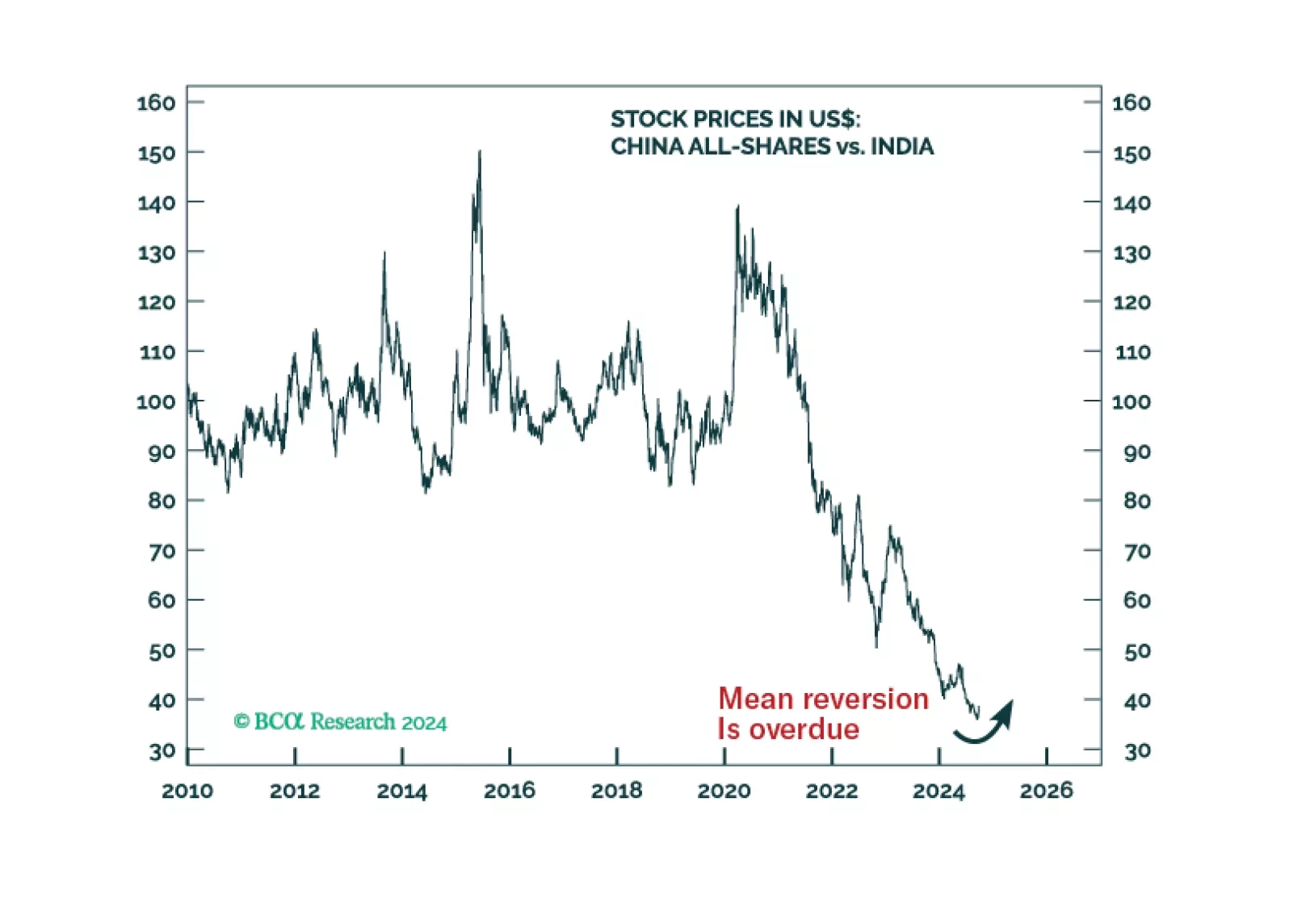

The prices of multiple financial assets have failed to break above their technical resistances. When this occurs, a breakdown ensues. In brief, global risk assets remain vulnerable. We are upgrading Chinese onshore stocks from neutral to overweight and offshore ones from underweight to neutral within EM and global equity portfolios.