China & EM Asia

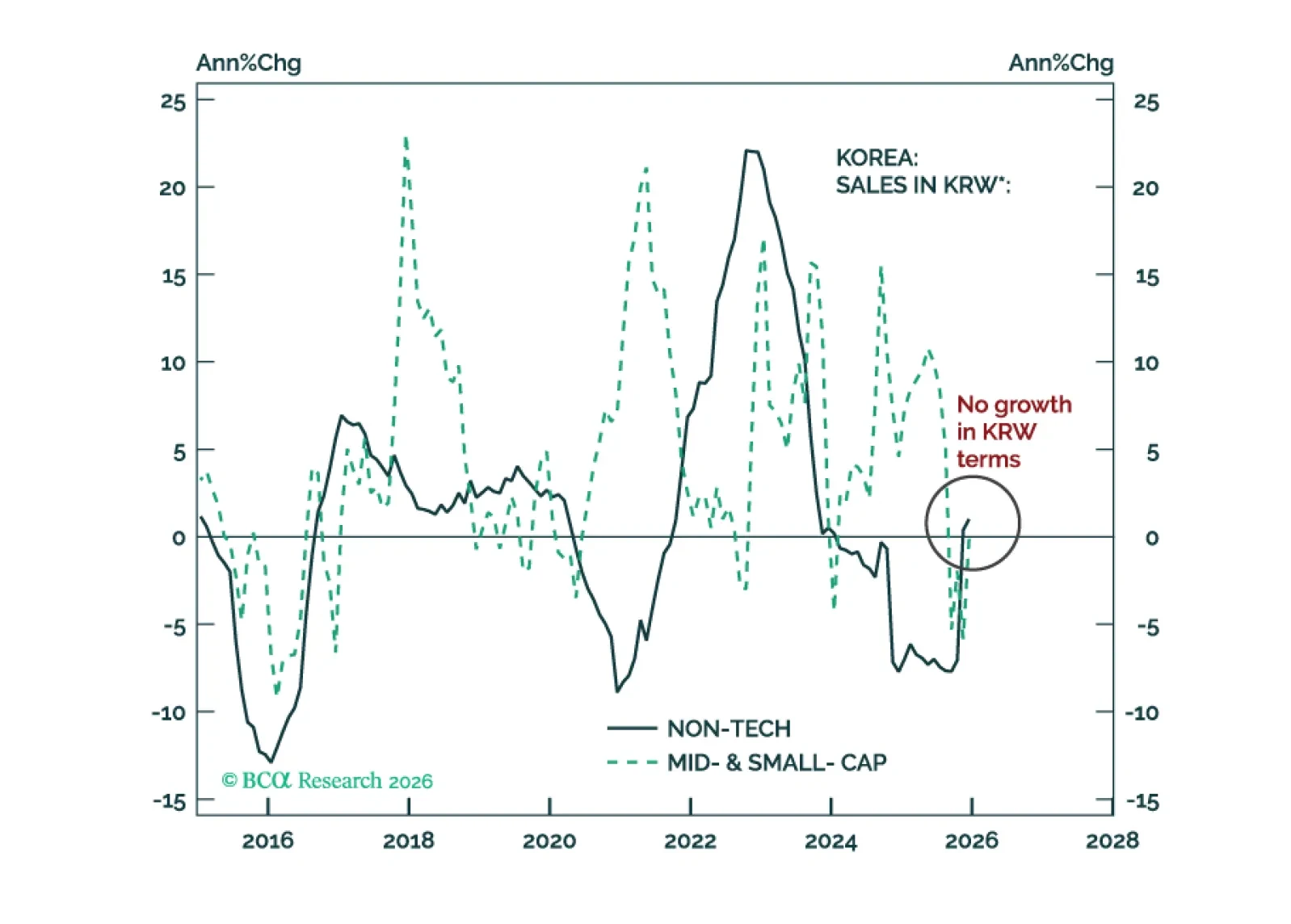

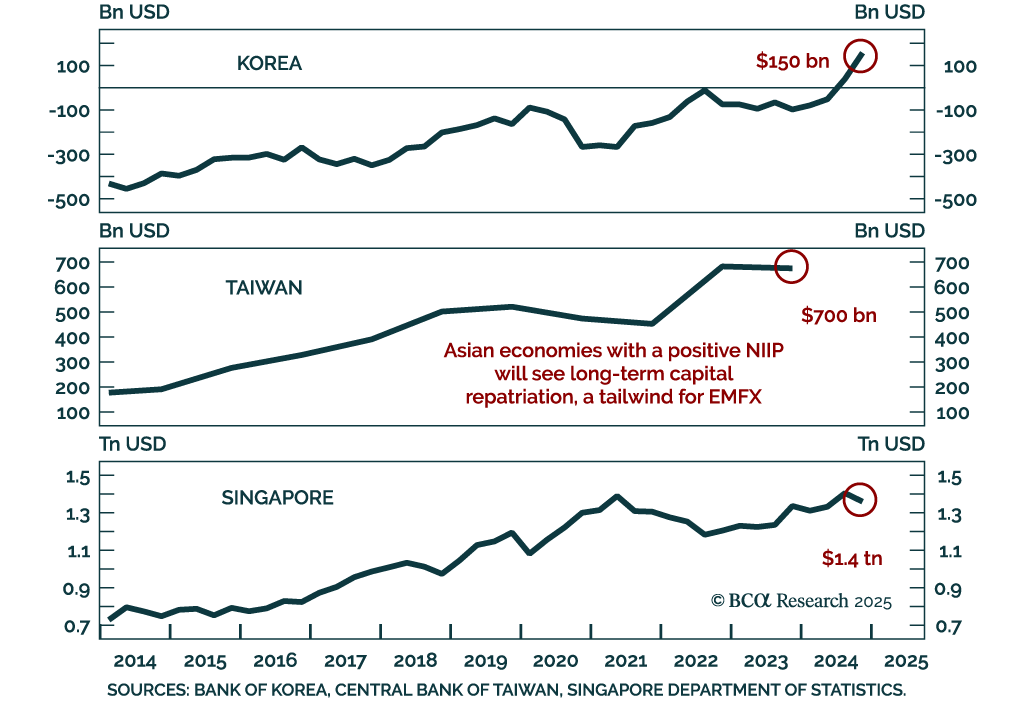

Go long KRW versus USD. Within an EM equity portfolio, overweight Korean tech and stay neutral on Korean non-tech. However, we are not bullish on the Korean bourse's absolute performance.

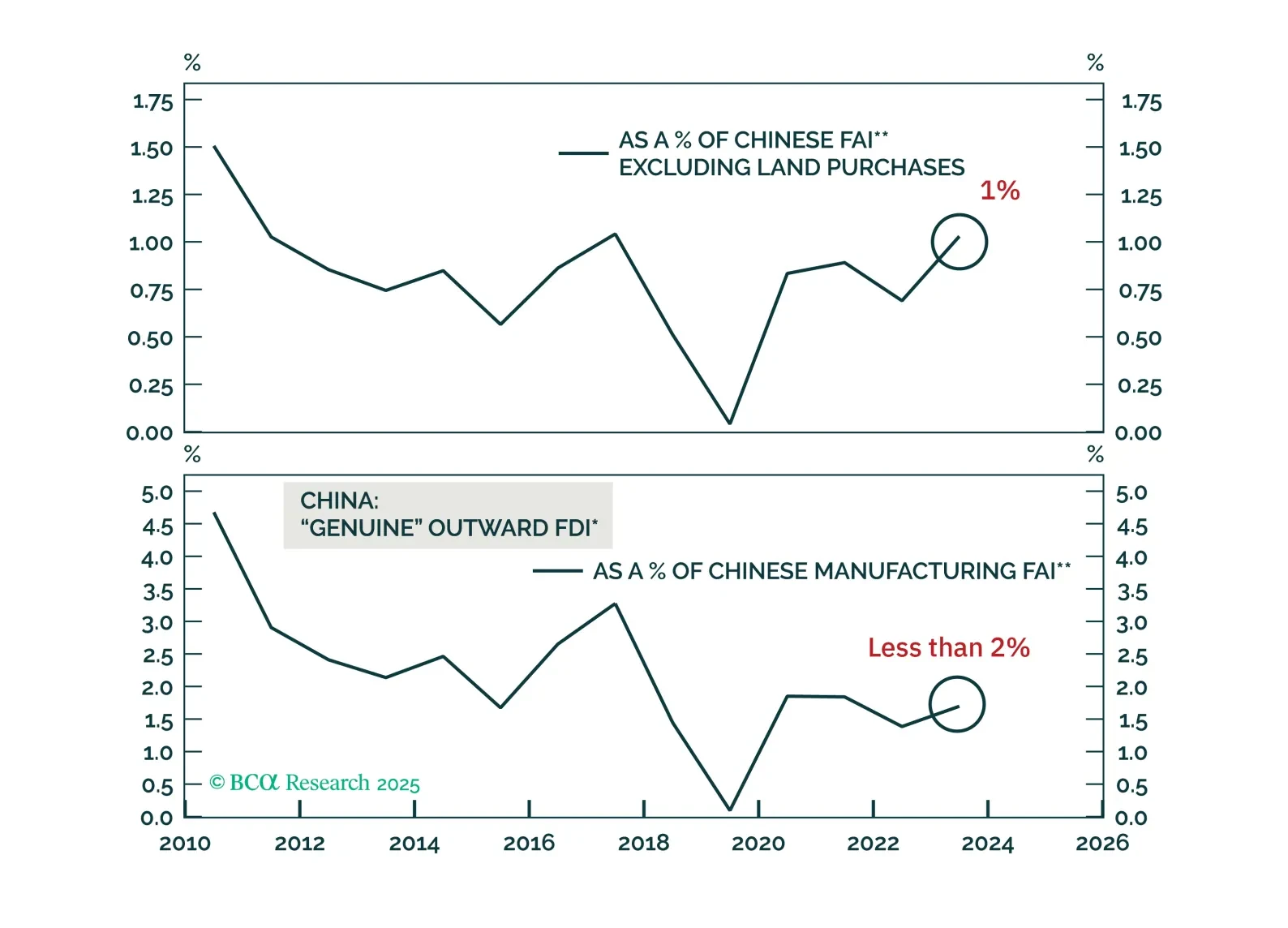

With Sino-US tensions flaring up again, will Chinese manufacturers accelerate their overseas capacity shift? In this Special Report we examine China’s manufacturing offshoring through multiple lenses and tackle the key questions shaping its next phase.

A world of political churn favors safe havens — buy yen, stay overweight US stocks, and avoid chasing the fragile rally in China.

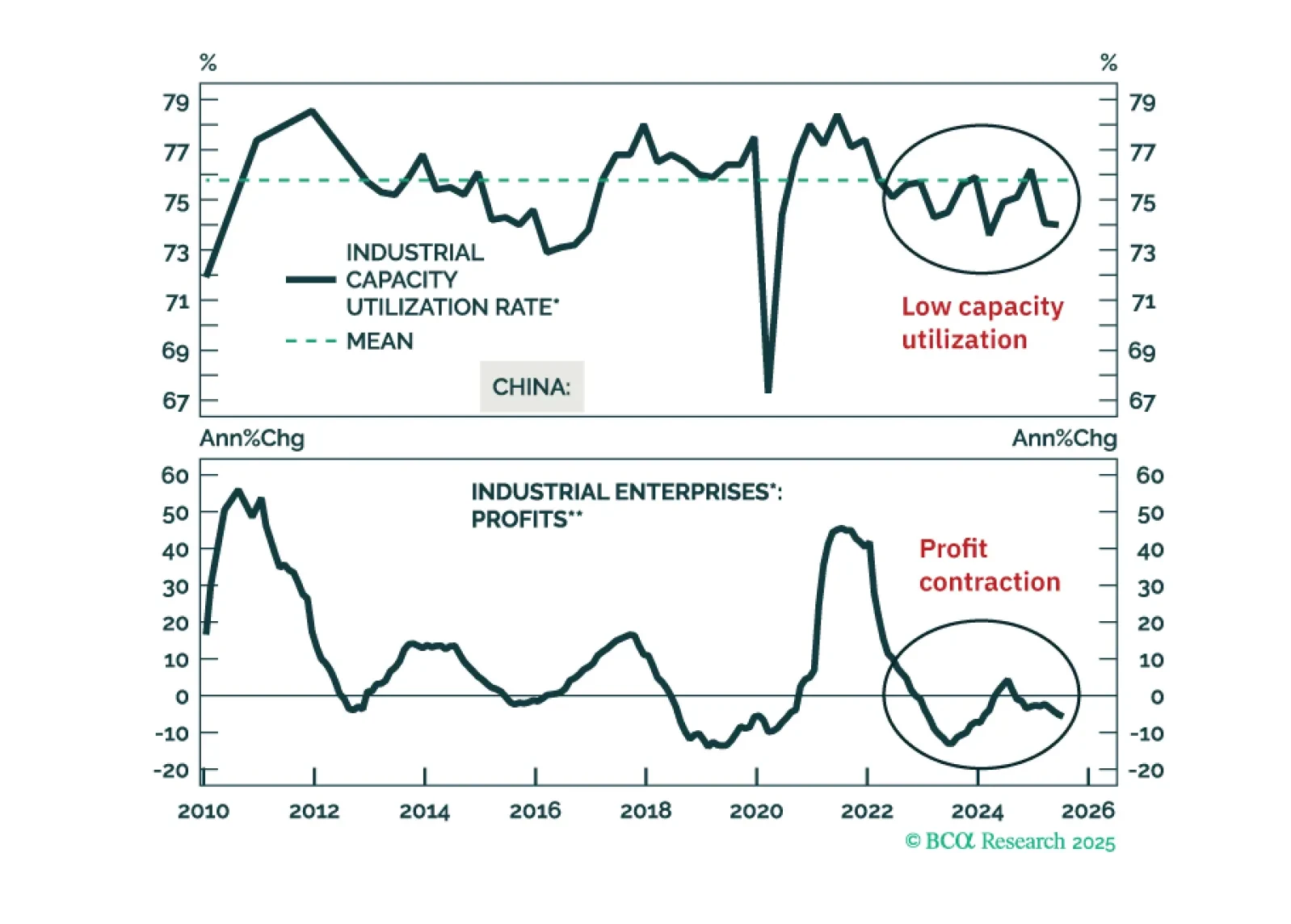

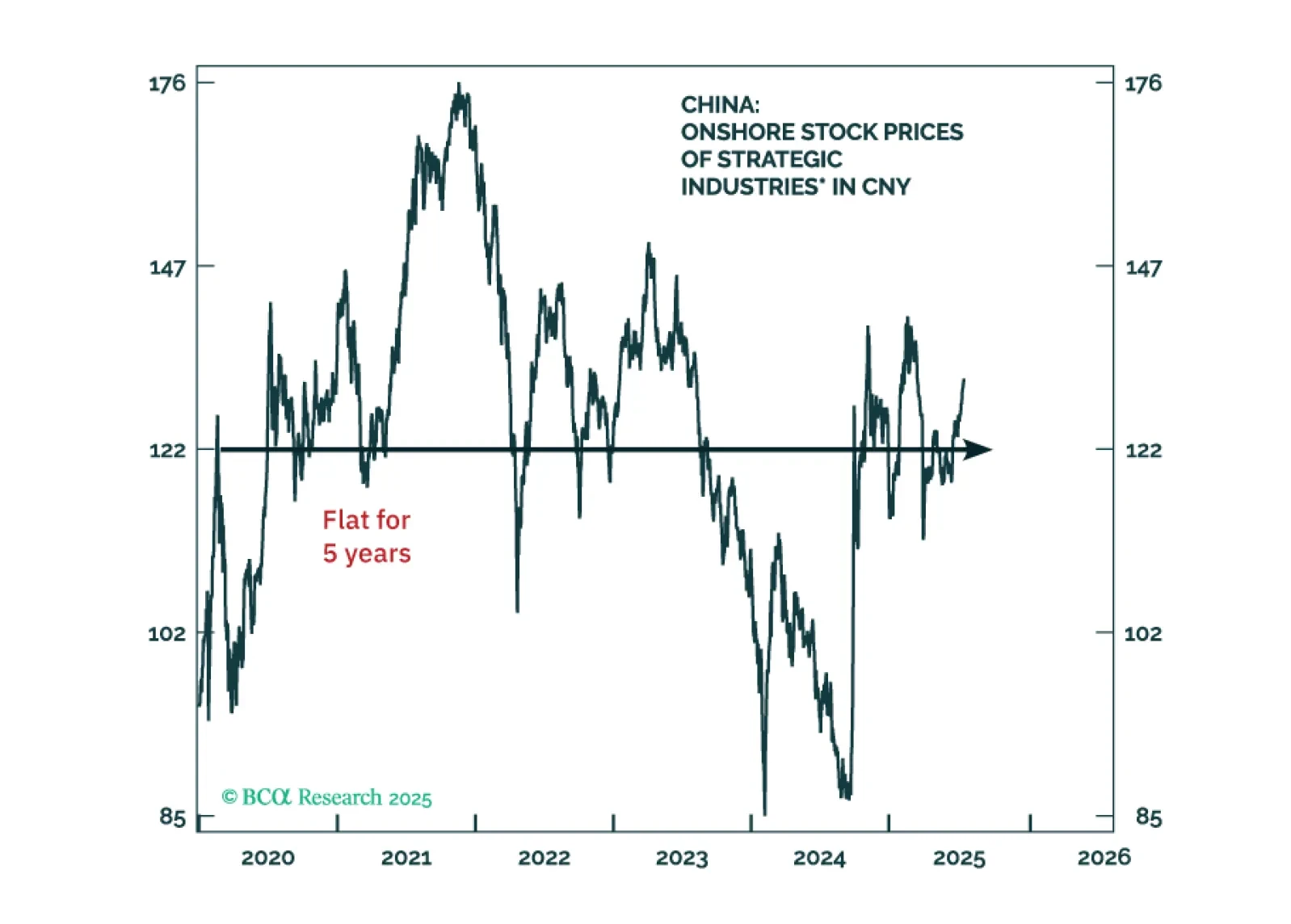

China’s policy-driven constraints prevent the “destruction” part of the creative destruction process. Instead, they entrench overcapacity, deflation, and poor profitability. We are reluctant to chase the rally in Chinese stocks in absolute terms.

Investors often ask us which industries the Chinese government is prioritizing for expansion. The assumption is that investing in sectors hand-picked authorities will produce solid investment returns. Yet, this assumption has not held over the past decade.

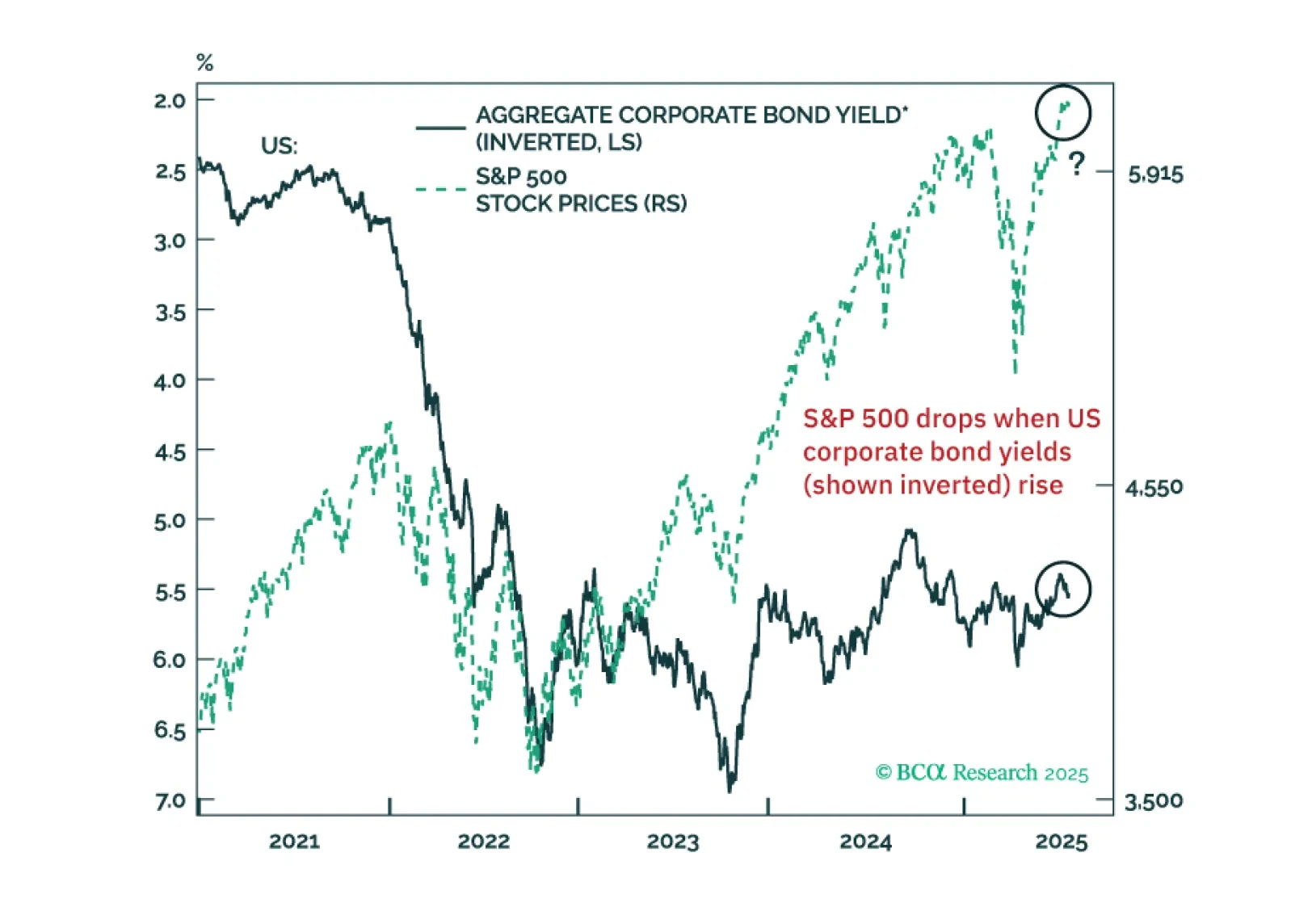

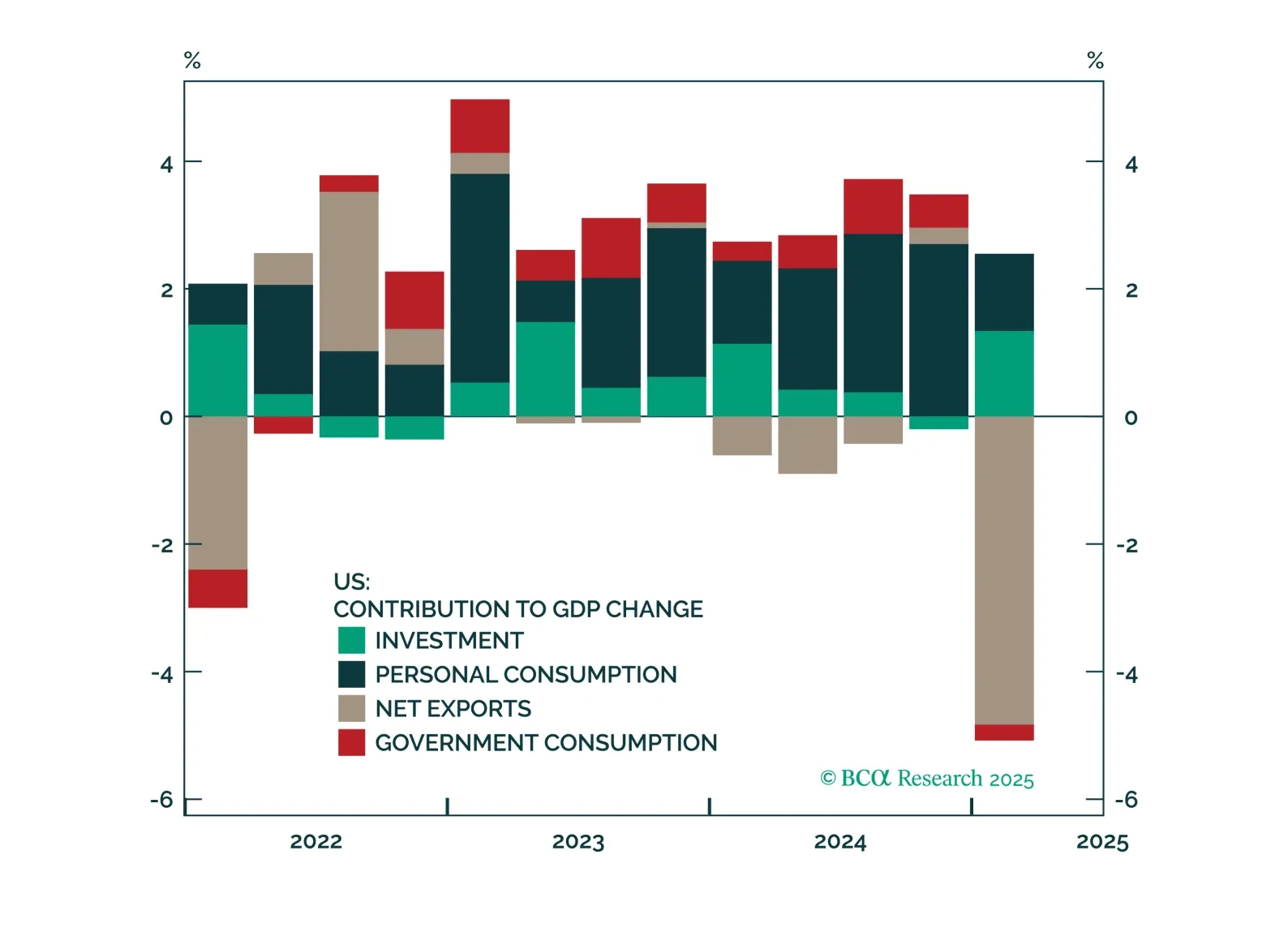

US equity investors should heed warning signals from US corporate bond yields. There are early red flags for EM share prices. Global trade will shrink in H2 2025. China’s economic tailwinds from H1 2025 – fiscal and export frontloading – are coming to an end.

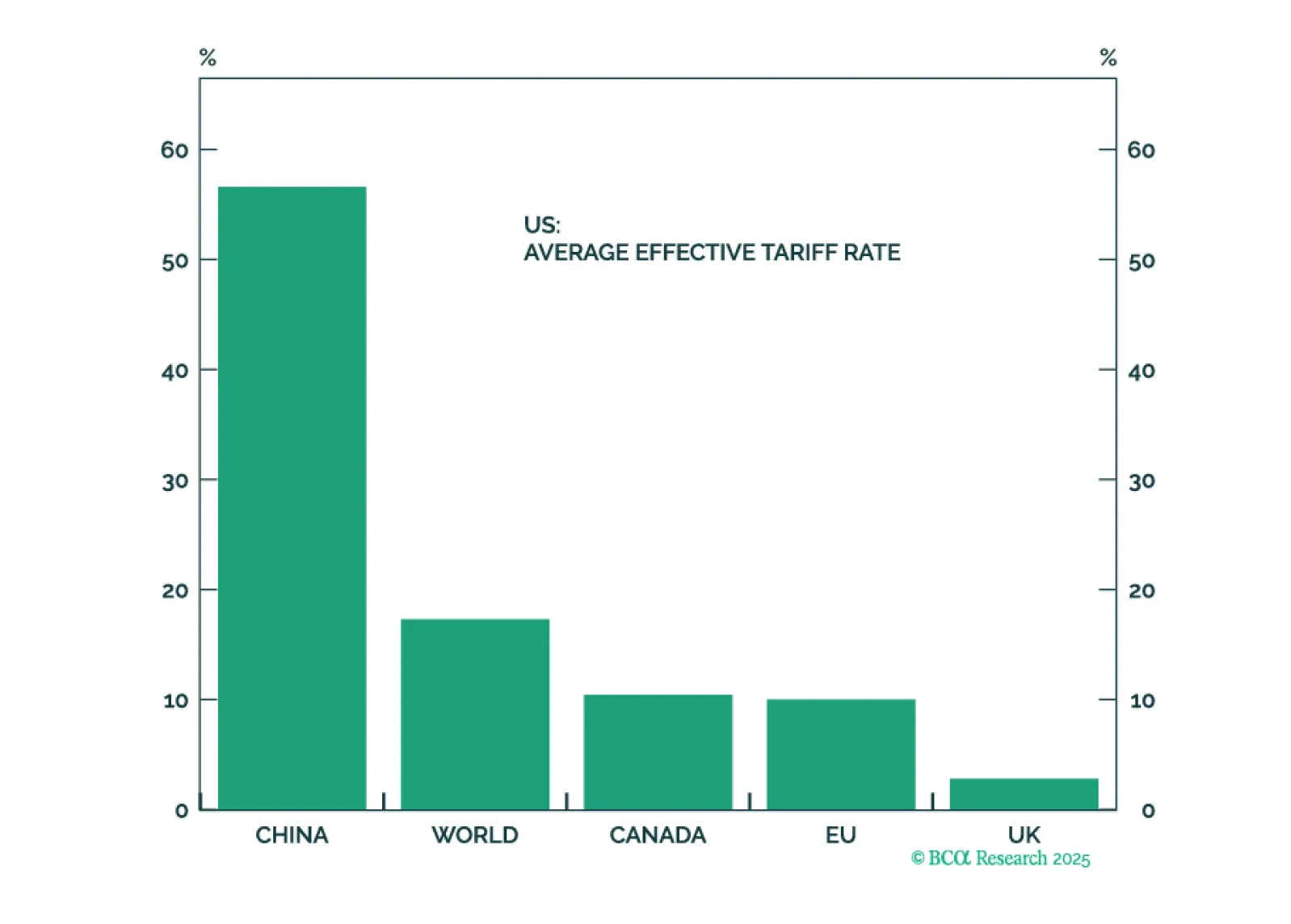

Acute geopolitical risks, like a massive oil shock, may be abating. But structural geopolitical risk remains high and could upset a blithe market. Cyclical economic risks are underrated as the US slows down and China continues to stumble. Investors should book some profits in anticipation of tariff implementation and a downturn in hard economic data.

Negotiations on trade, Iran, and Ukraine will prove critical this month. Markets will remain volatile because positive data surprises enable the White House to press its hawkish tariff hikes, while negative surprises force the White House to backpedal.

Do not play the bounce in US and global cyclical assets as Trump backpedals from the trade war. China will talk, but the pace will be slow and the outcome disappointing. Fiscal stimulus will surprise marginally in the EU, China, and even the US, but still may not rescue the business cycle.