China

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

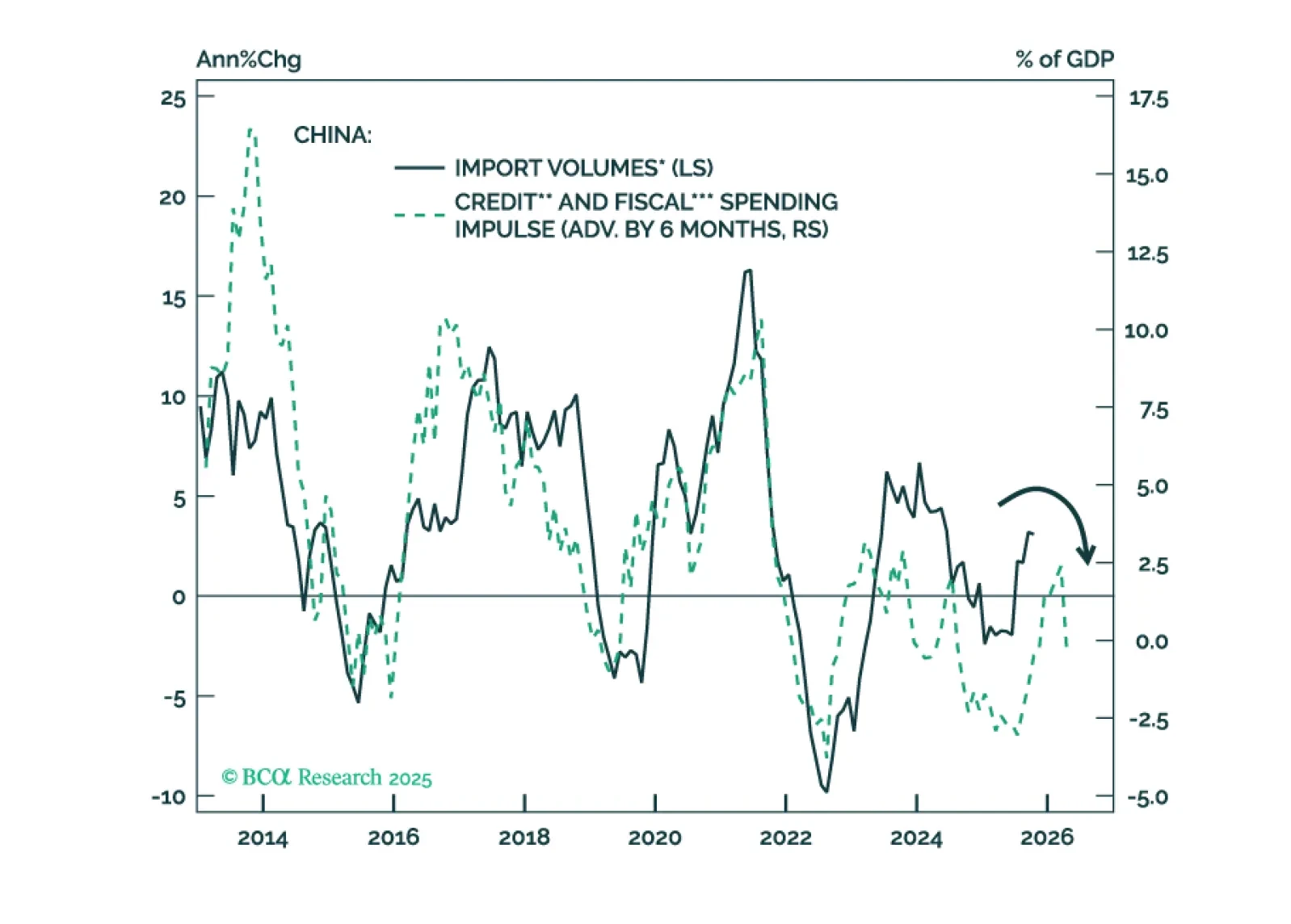

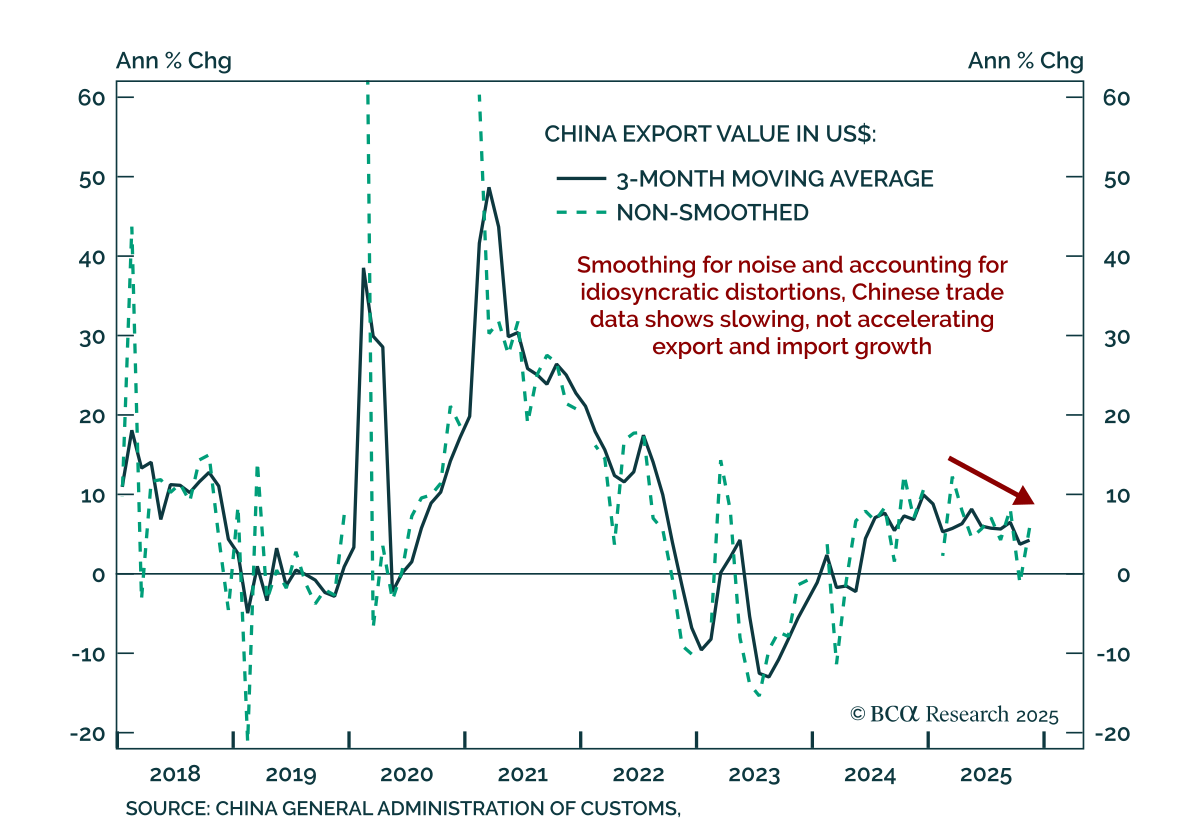

Risk assets in EM/China and cyclical commodities will sell off in H1 2026. A shift toward aggressive policy stimulus in China and a clear improvement in global manufacturing are needed to produce durable rallies in EM/China risk assets and the prices of energy and industrial metals.

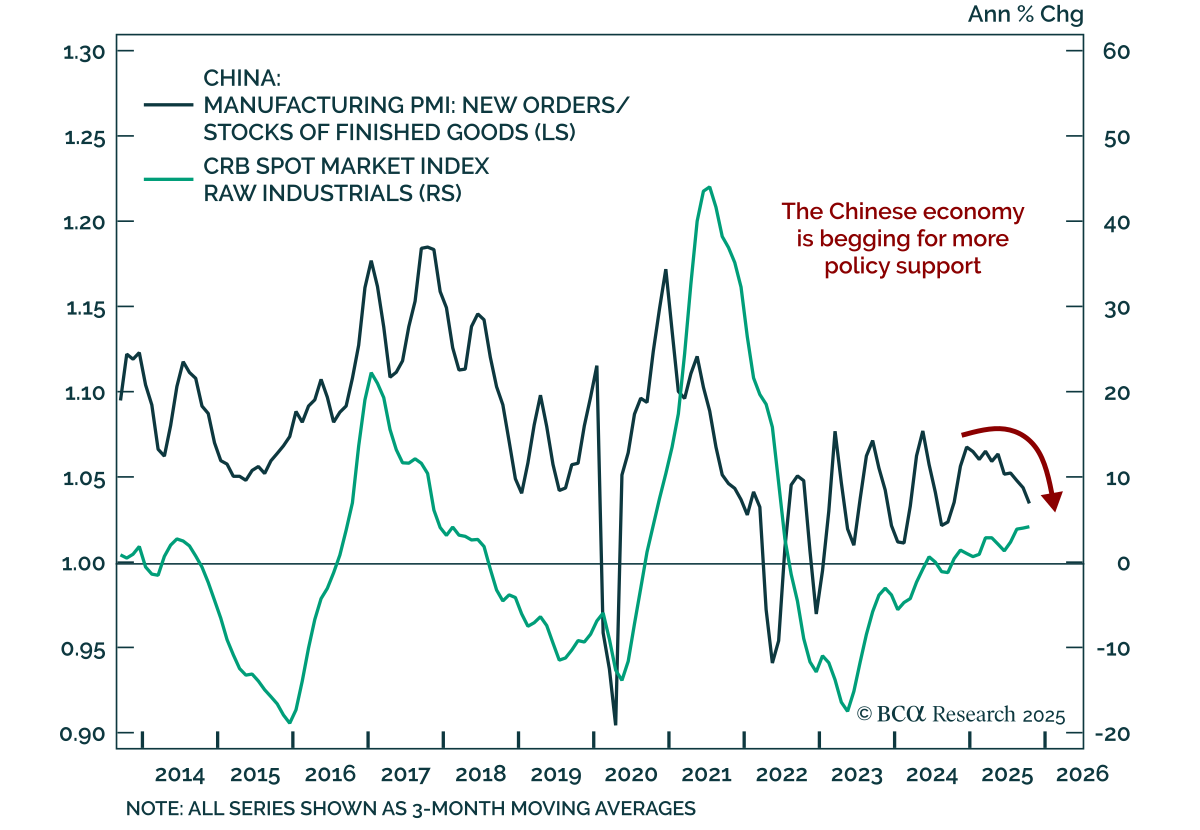

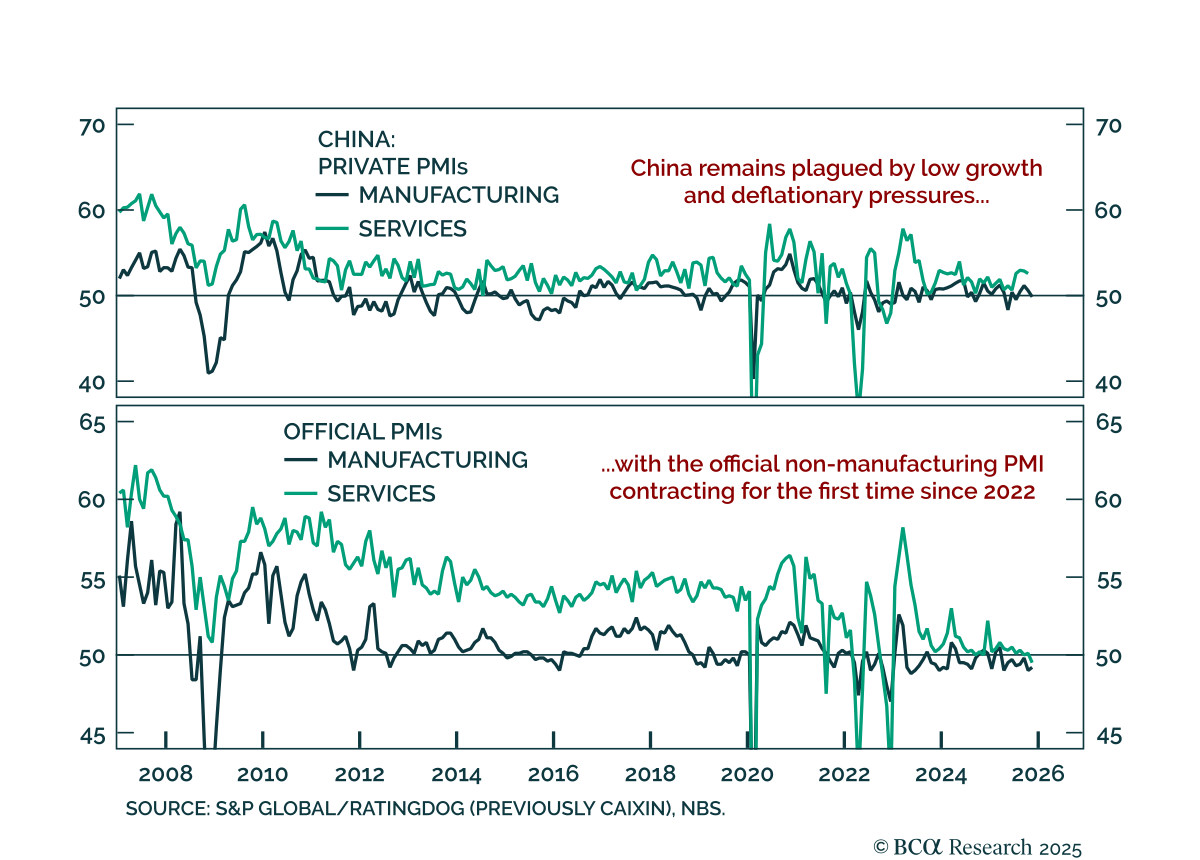

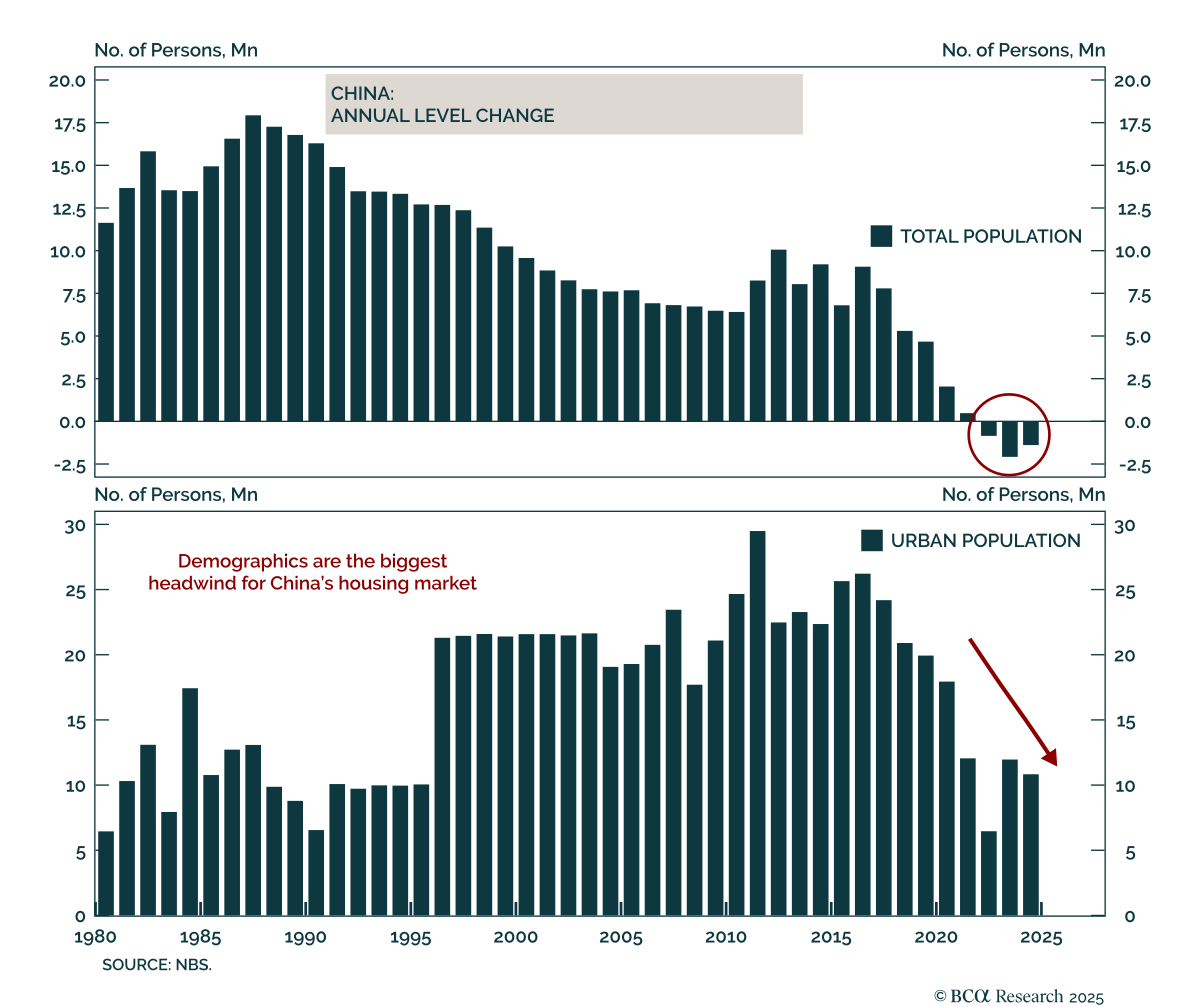

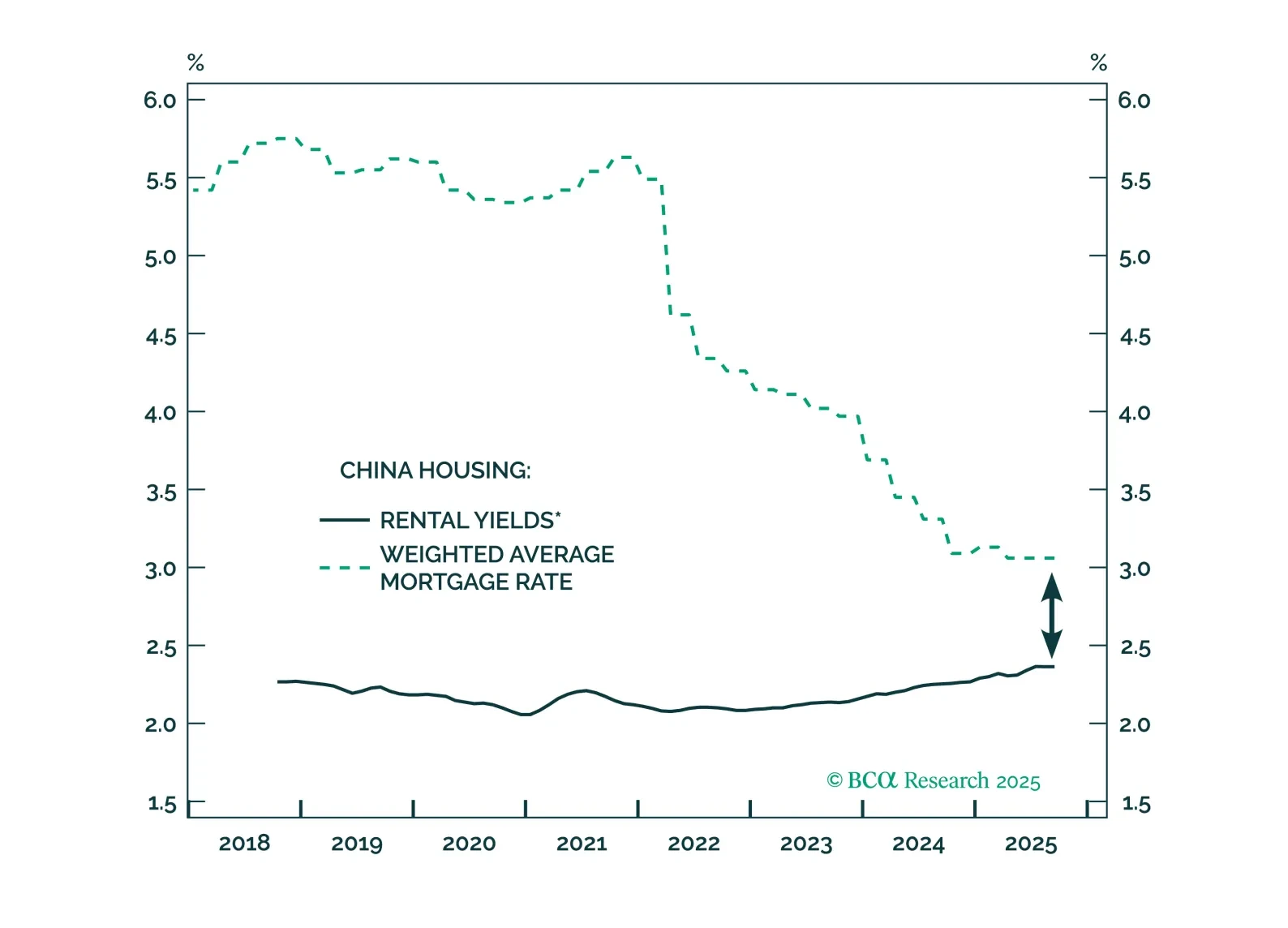

China’s economy is weakening across the board as global risk-off hits equities. With housing conditions worsening and exports contracting—a perfect storm—Beijing faces mounting pressure to deliver stronger, housing-focused stimulus.

This report revisits China’s property market through both cyclical and structural lenses, assesses the likely policy responses, and evaluates their investment implications.