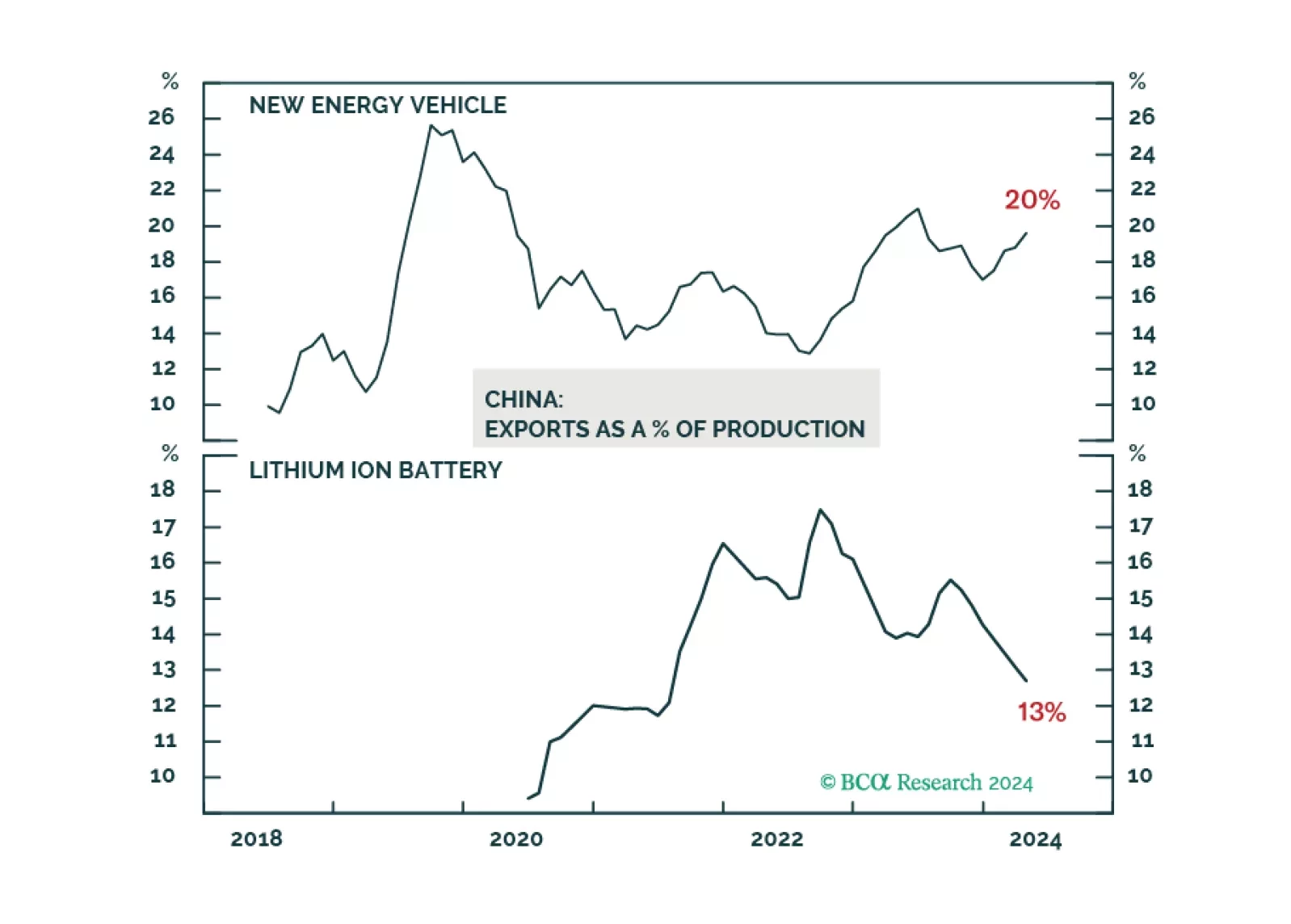

China

The EU's import tariff increases on Chinese EVs are expected to have a minimal impact on China's overall exports. We anticipate that most Western-brand EV shipments from China will be less affected by the EU import tax hike. Beijing will likely pursue continued negotiations with the EU rather than resort to harsh retaliatory measures.

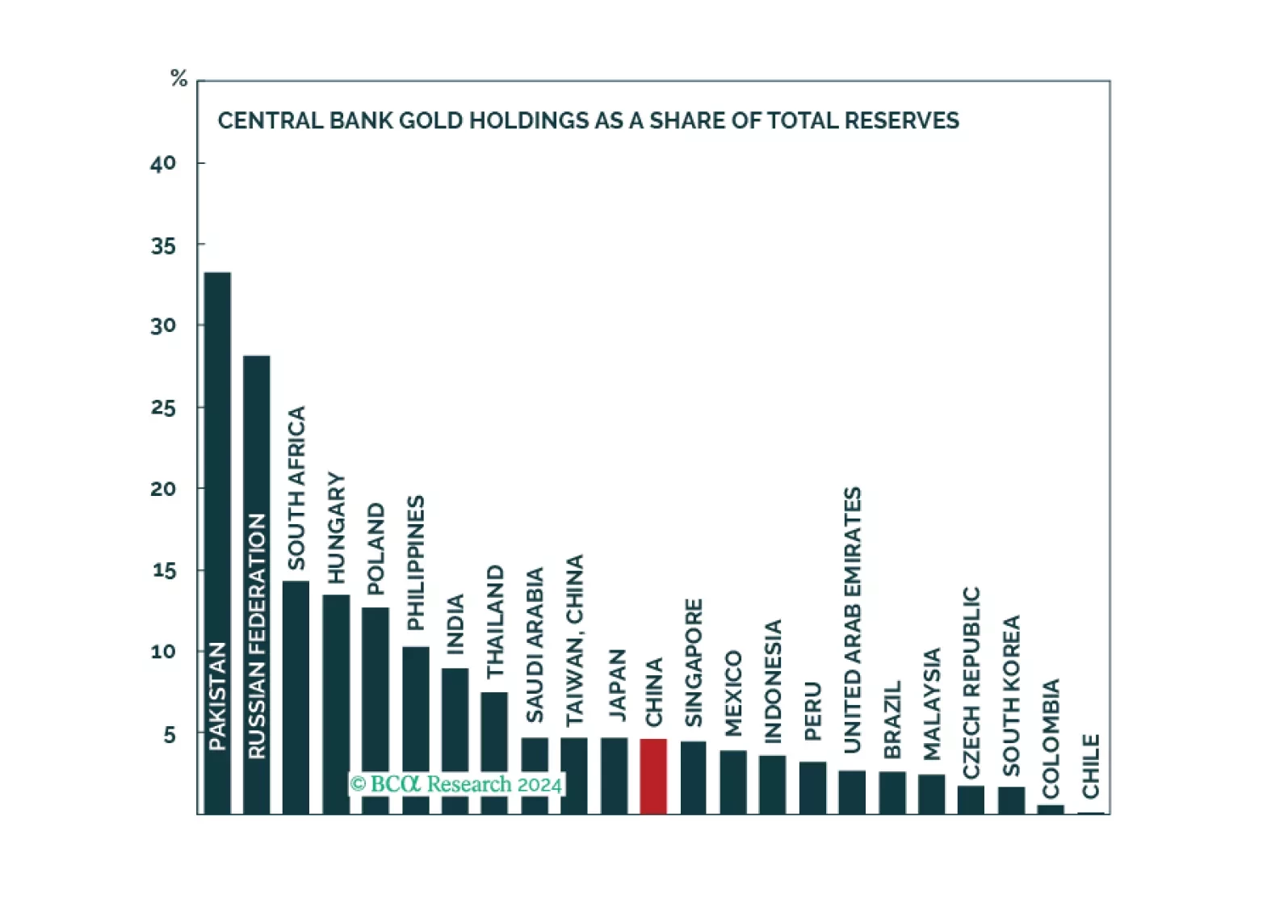

Gold prices might experience a correction or consolidation over the near term. However, cyclical and structural forces will ultimately cause the yellow metal to trend upwards.

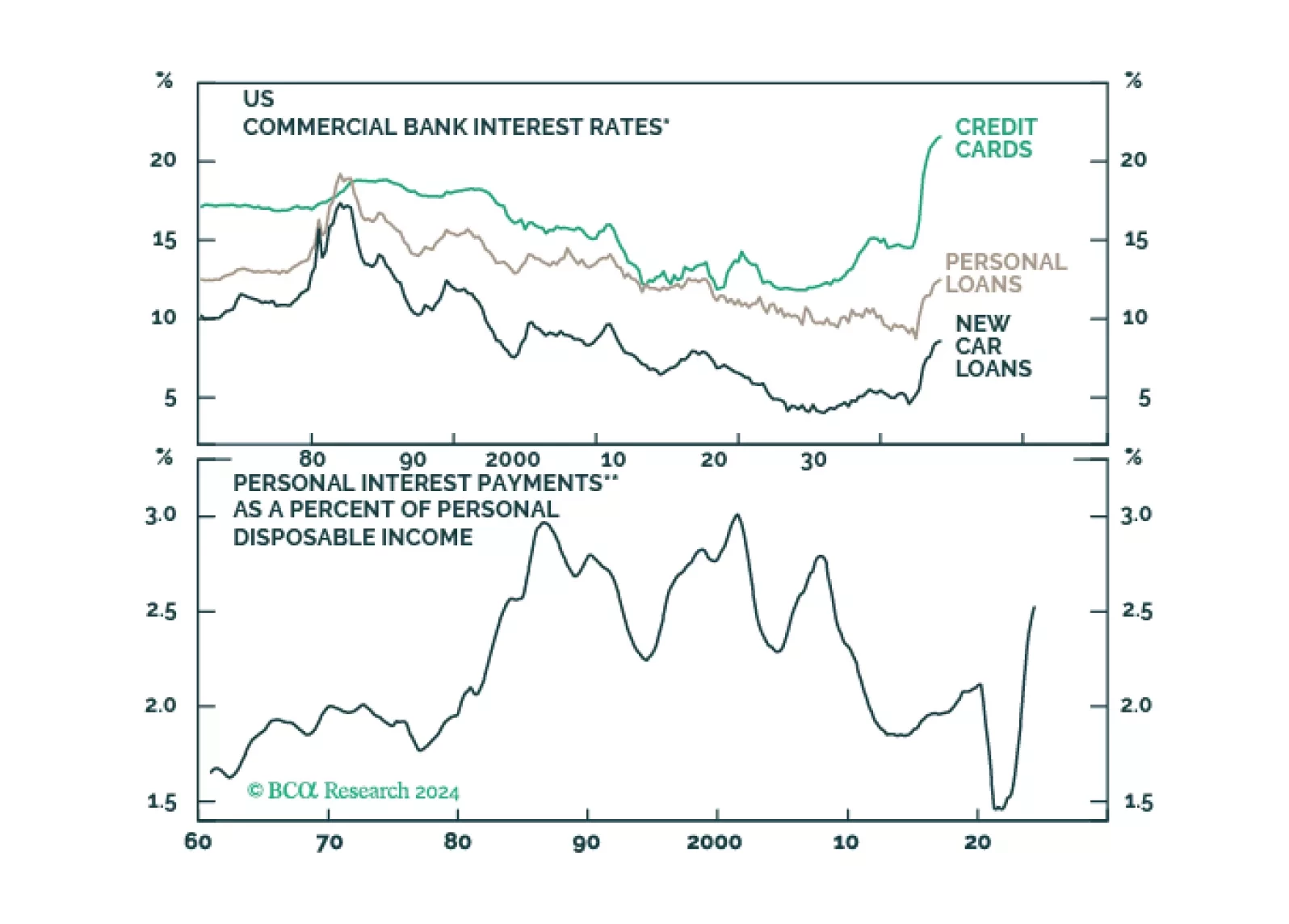

Global consumer spending is likely to slow over the coming quarters, culminating in a major economic downturn in late 2024 or early 2025. Investors should maintain benchmark exposure to equities for now but look to turn more defensive by the end of this summer.

The issue of "industrial overcapacity" in China may be a misconception. Overcapacity in the old-economy sectors has largely diminished, while China's dominance in the global green-energy market reflects its technological advancements and innovations.