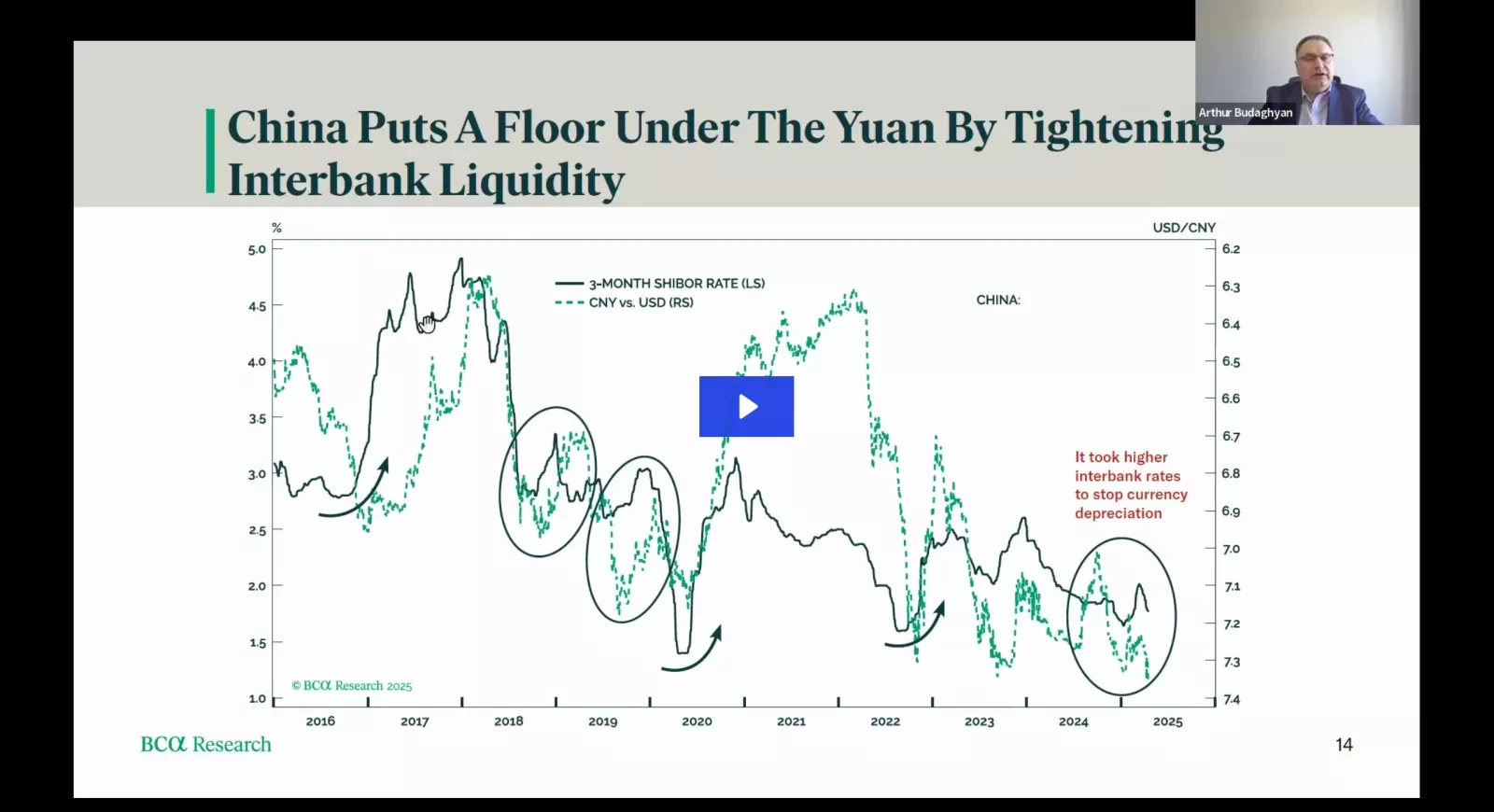

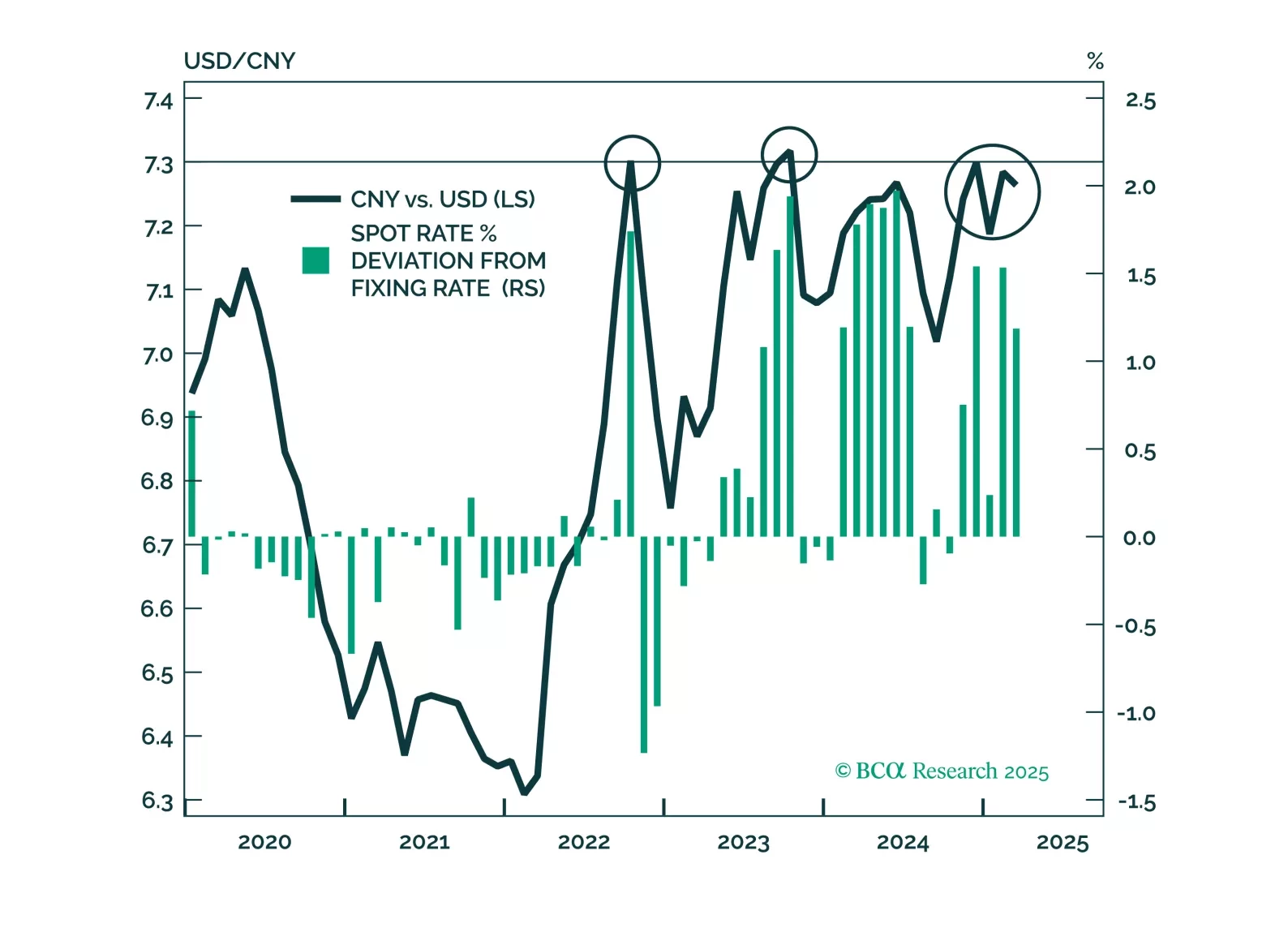

China

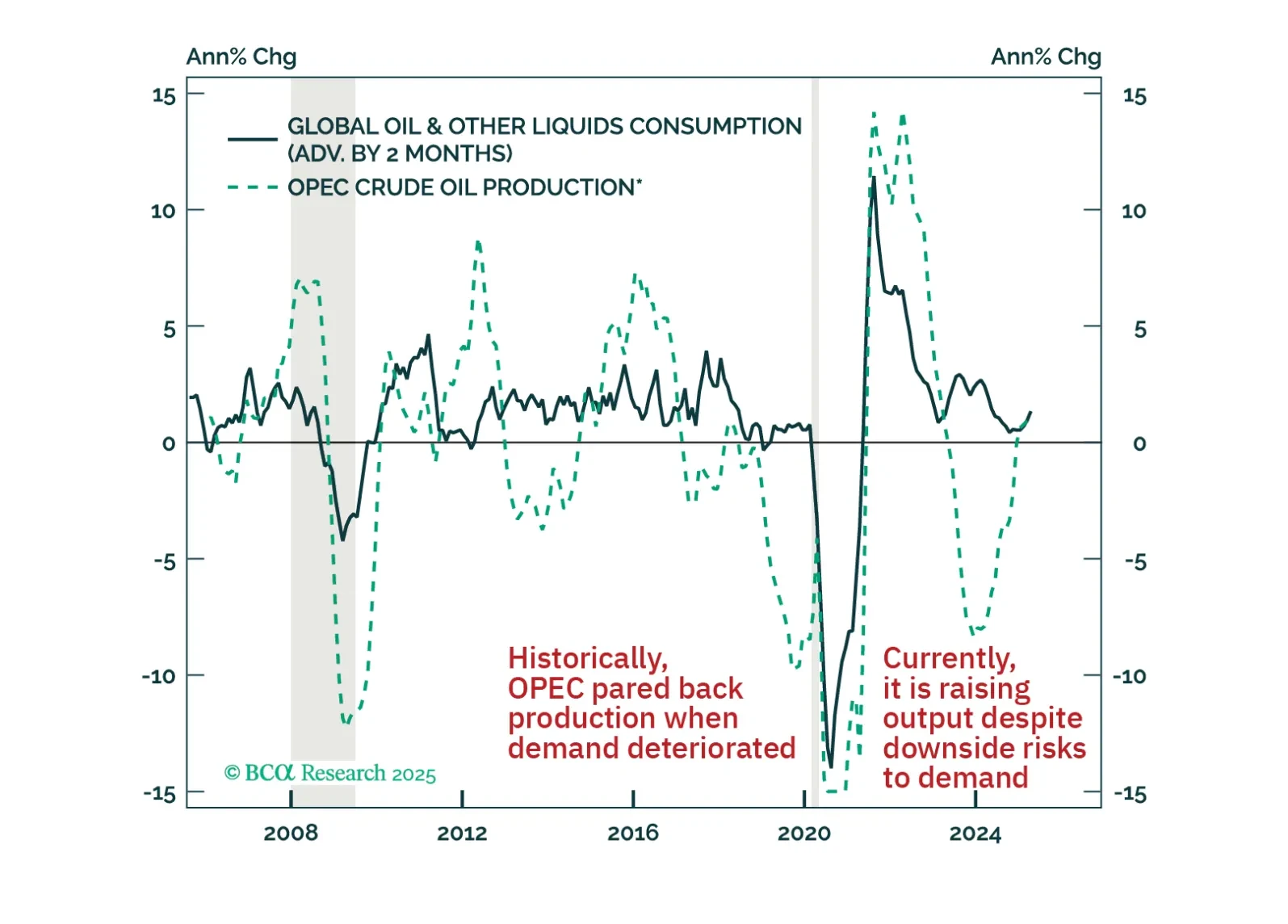

Oil has borne the brunt of the year-to-date deterioration in cyclically sensitive financial assets. It is a key underperformer both within the commodity space and among global risk assets. This underperformance underscores that in addition to the trade war-induced headwind to demand, bearish supply-side developments are also weighing down on crude prices. As we discuss in this report, these dynamics will likely continue exerting downside pressure on oil prices over the coming weeks and months.

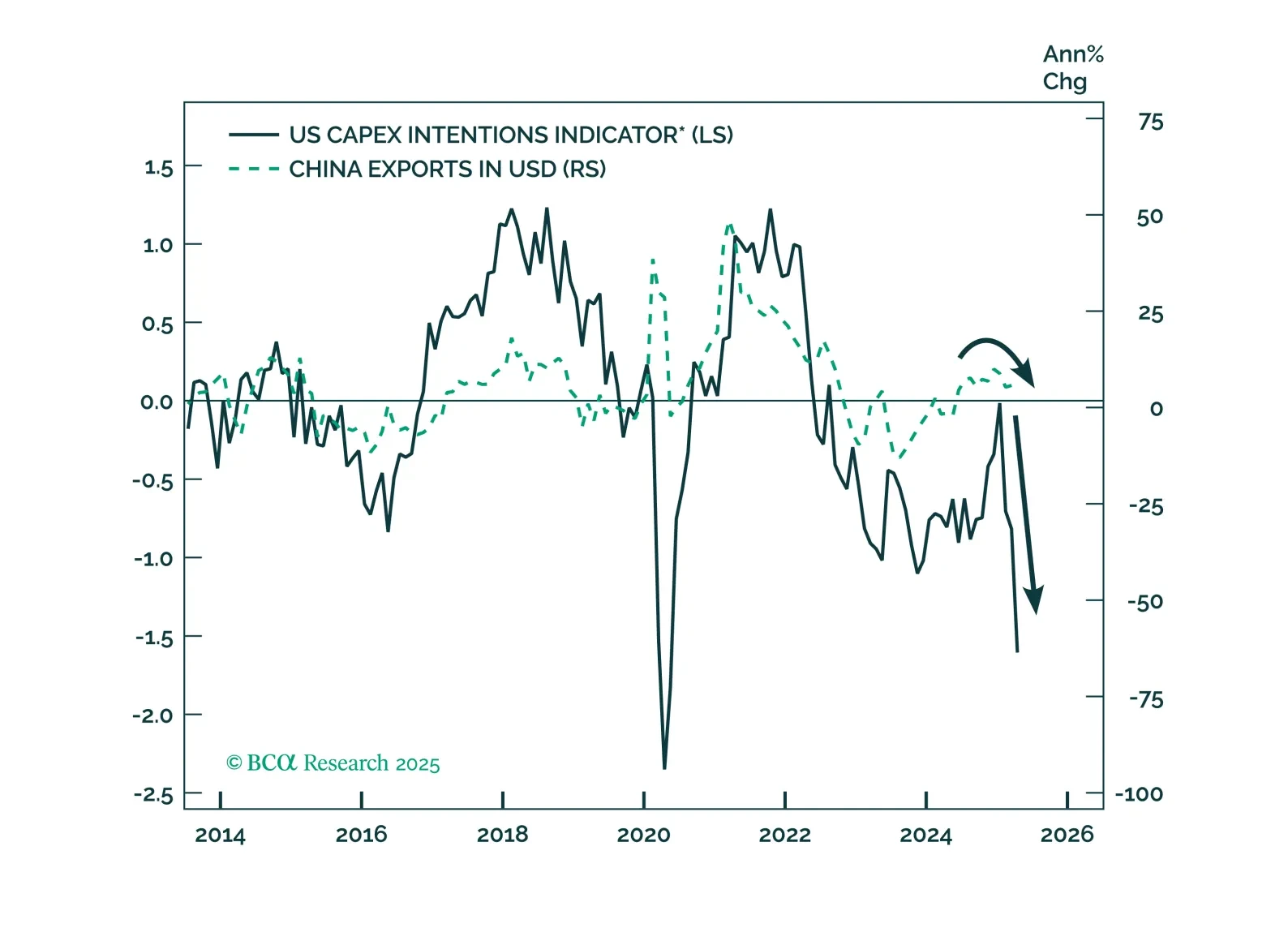

Despite marginal de-escalation in tariffs between the US and China, a sustainable trade agreement remains elusive. In the meantime, economic damage continues to mount, and Chinese equities have yet to fully price in the tariff-induced growth deterioration.

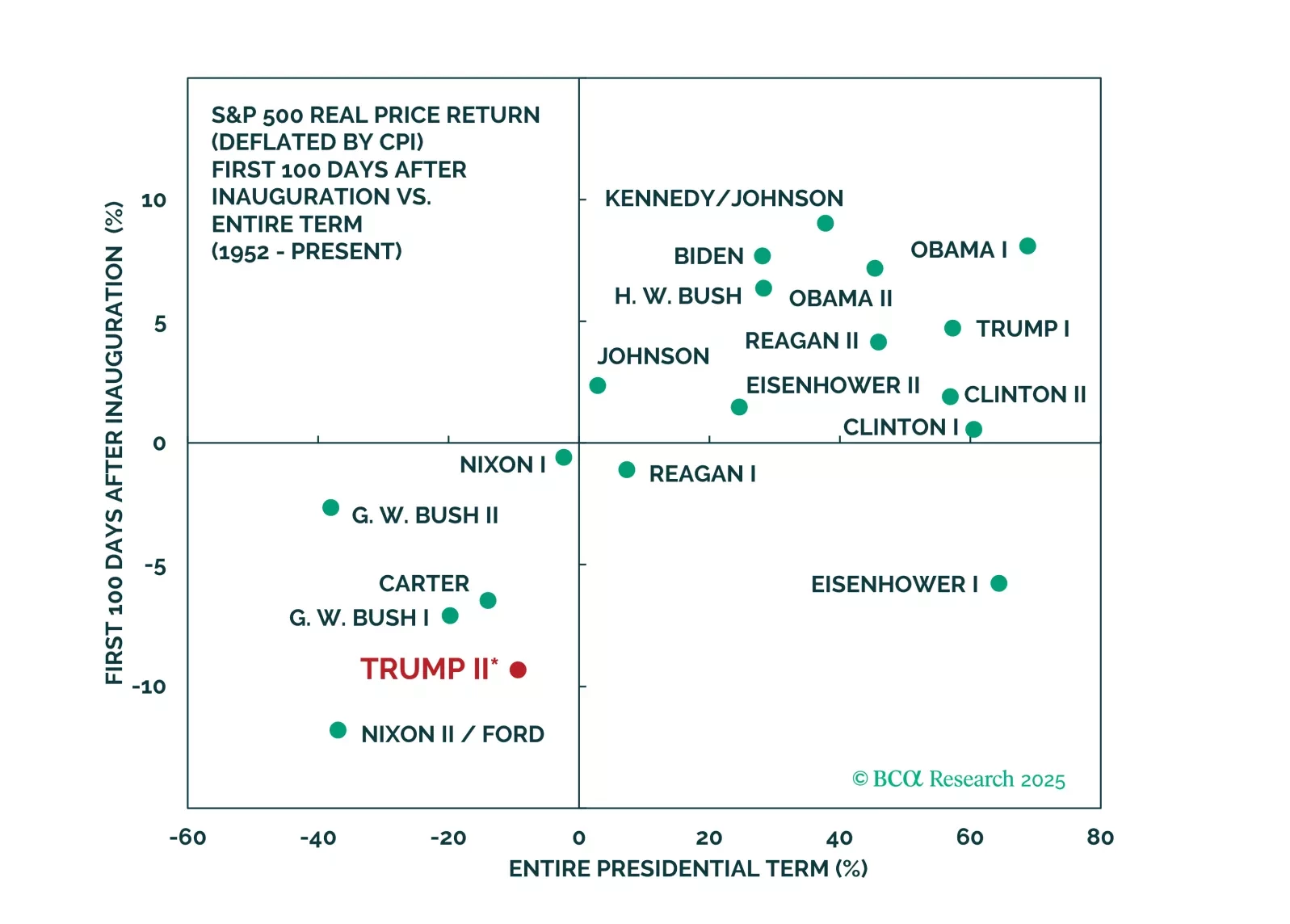

Do not play the bounce in US and global cyclical assets as Trump backpedals from the trade war. China will talk, but the pace will be slow and the outcome disappointing. Fiscal stimulus will surprise marginally in the EU, China, and even the US, but still may not rescue the business cycle.

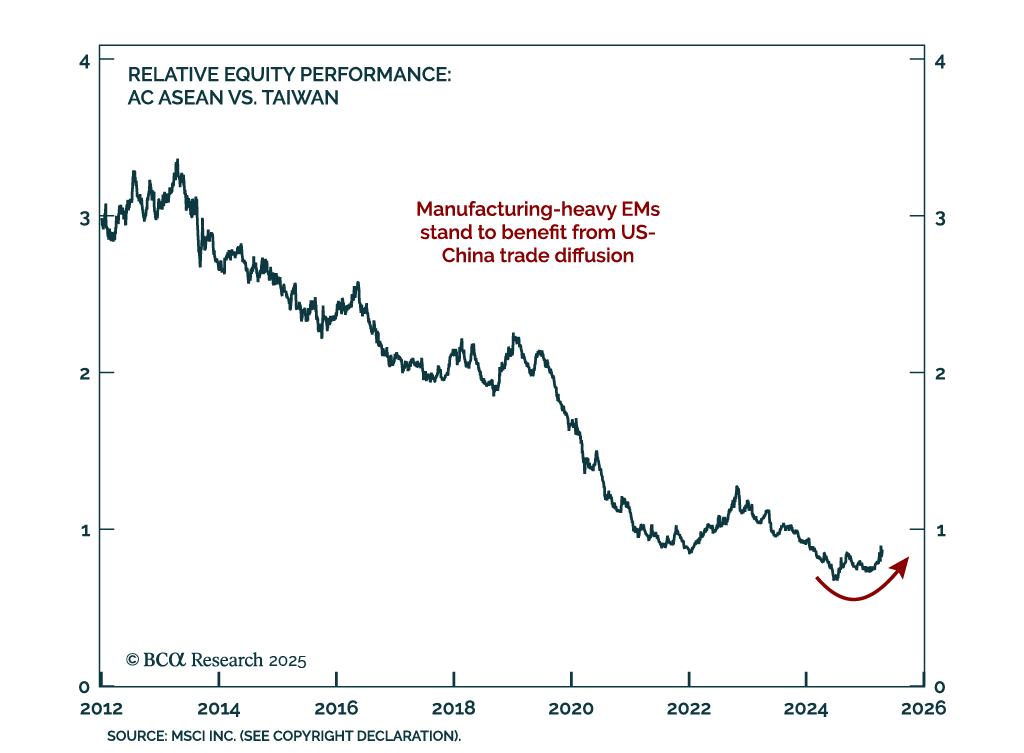

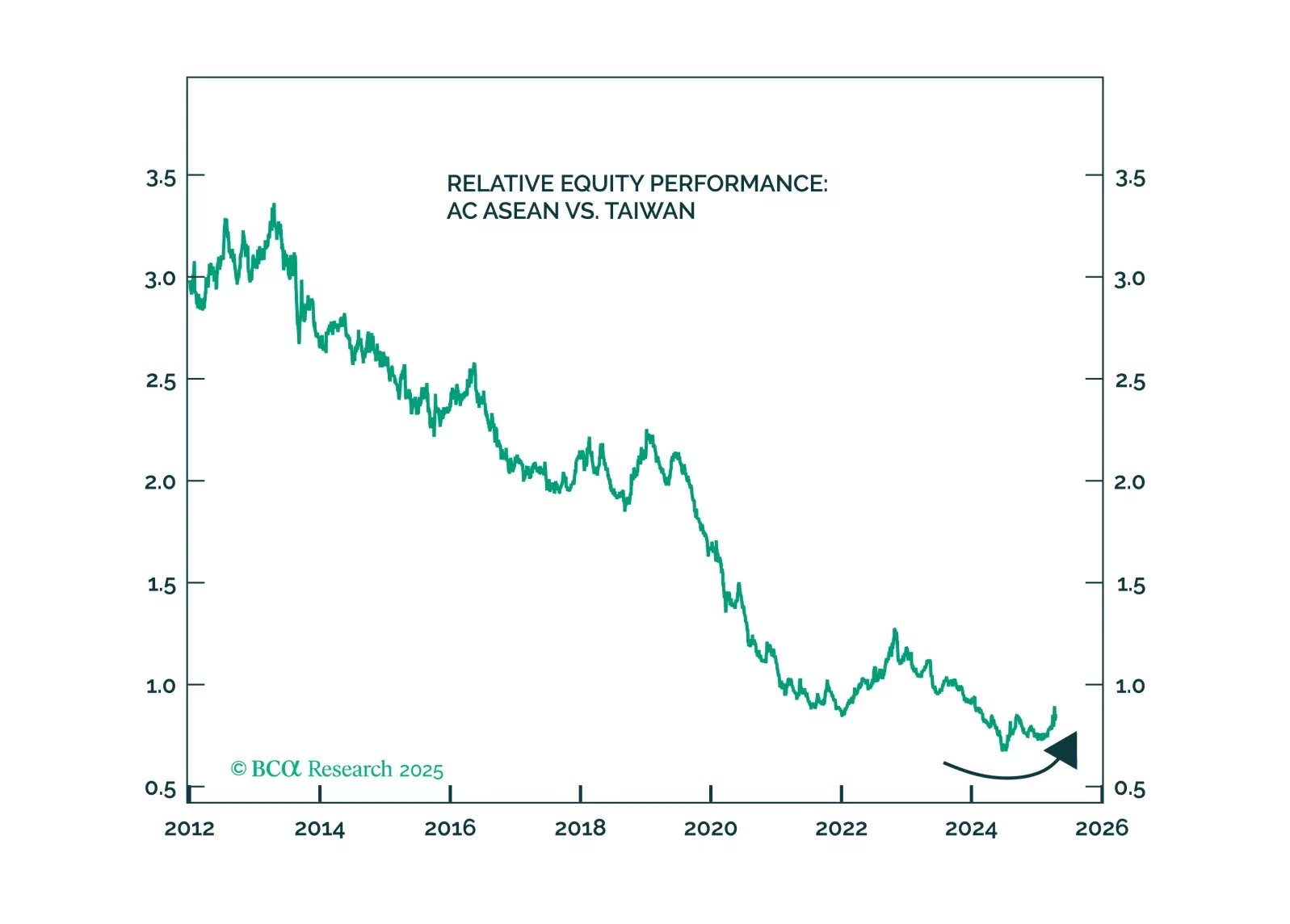

Upgrade the odds of a full-scale war in the Taiwan Strait from 5% to 10%. Rapid escalation of US-China economic war raises the probability of tensions spilling into the military-strategic domain. Investors should buy insurance against this tail risk while it is cheap. Meanwhile, use this year’s trade shock and equity volatility to increase allocation to EM manufacturing states.

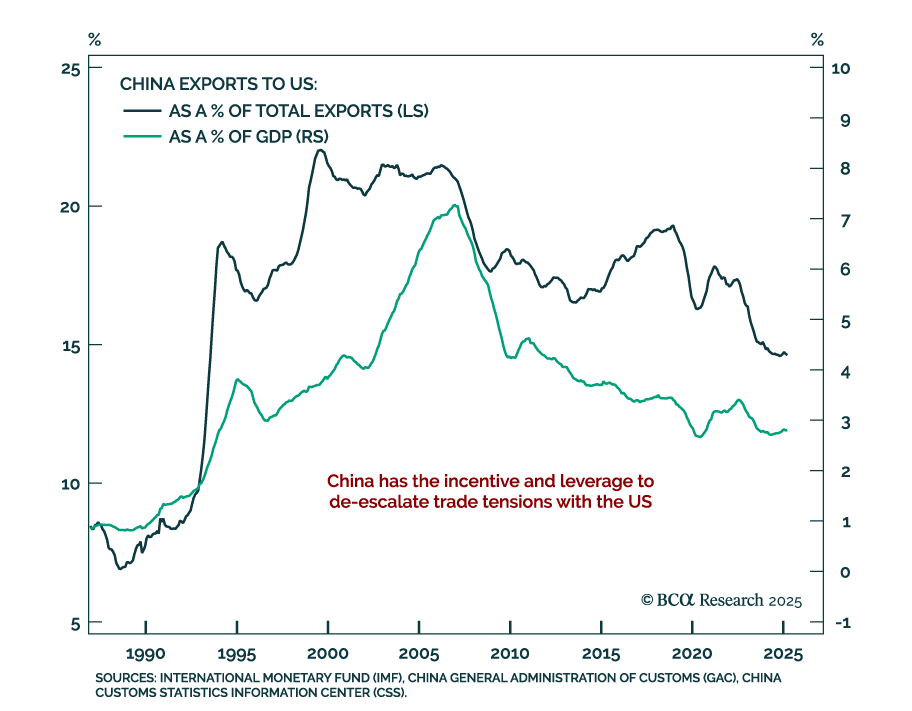

While the United States and China may aim for full decoupling, all they can afford now is some form of trade skirmishes. Increasing economic pressure will eventually force both Washington and Beijing to pursue more proactive negotiations. Until then, internal economic and financial strains are likely necessary to break the stalemate and resume dialogue between the two nations.