China

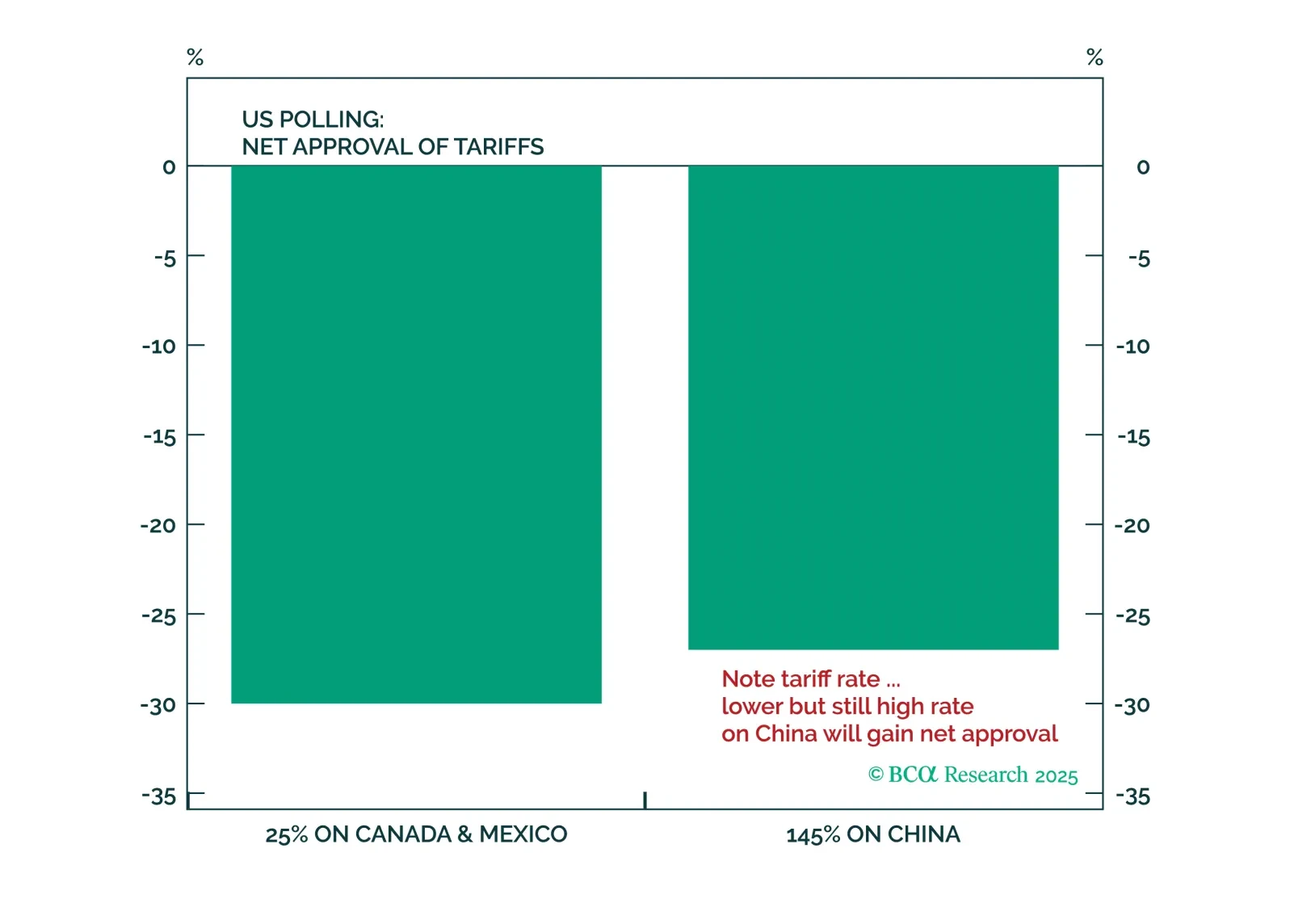

President Trump faces new restrictions on his trade powers coming from the US judicial branch, but they will not prevent him from continuing to restrict trade and investment with China. Rather, they will establish some curbs against entirely arbitrary executive tariffs, especially when wielded against US allies and partners.

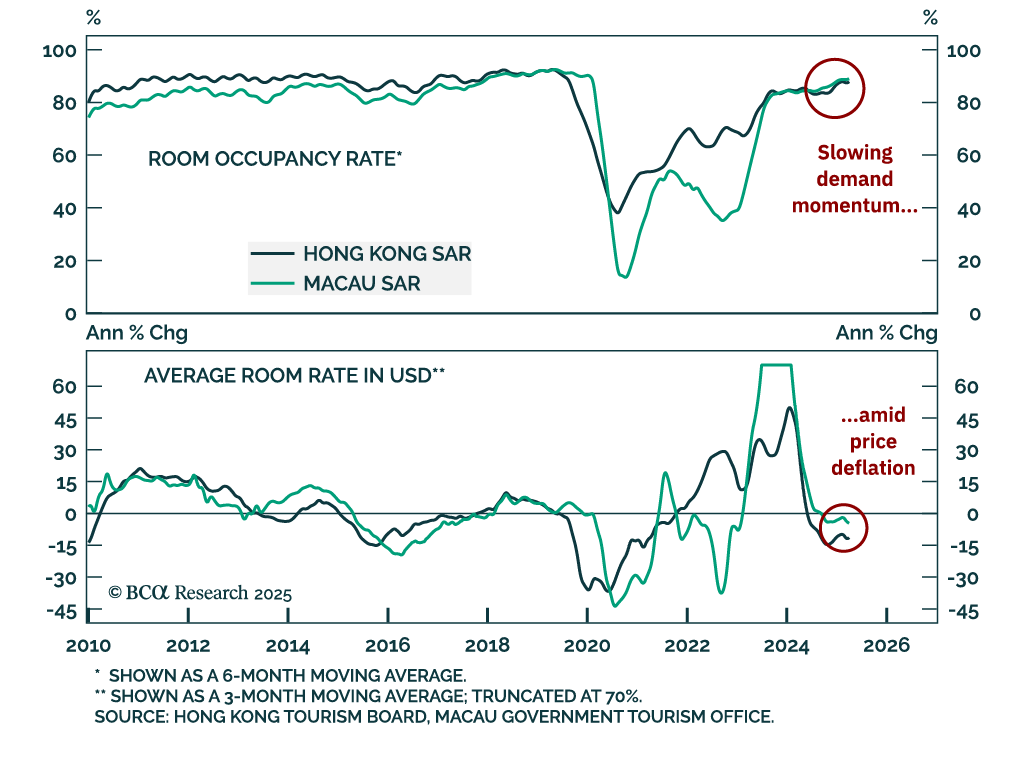

Chinese tourism will continue growing, but investors should be mindful not to overpay for Chinese tourism stocks by extrapolating their past double-digit revenue growth into the future.

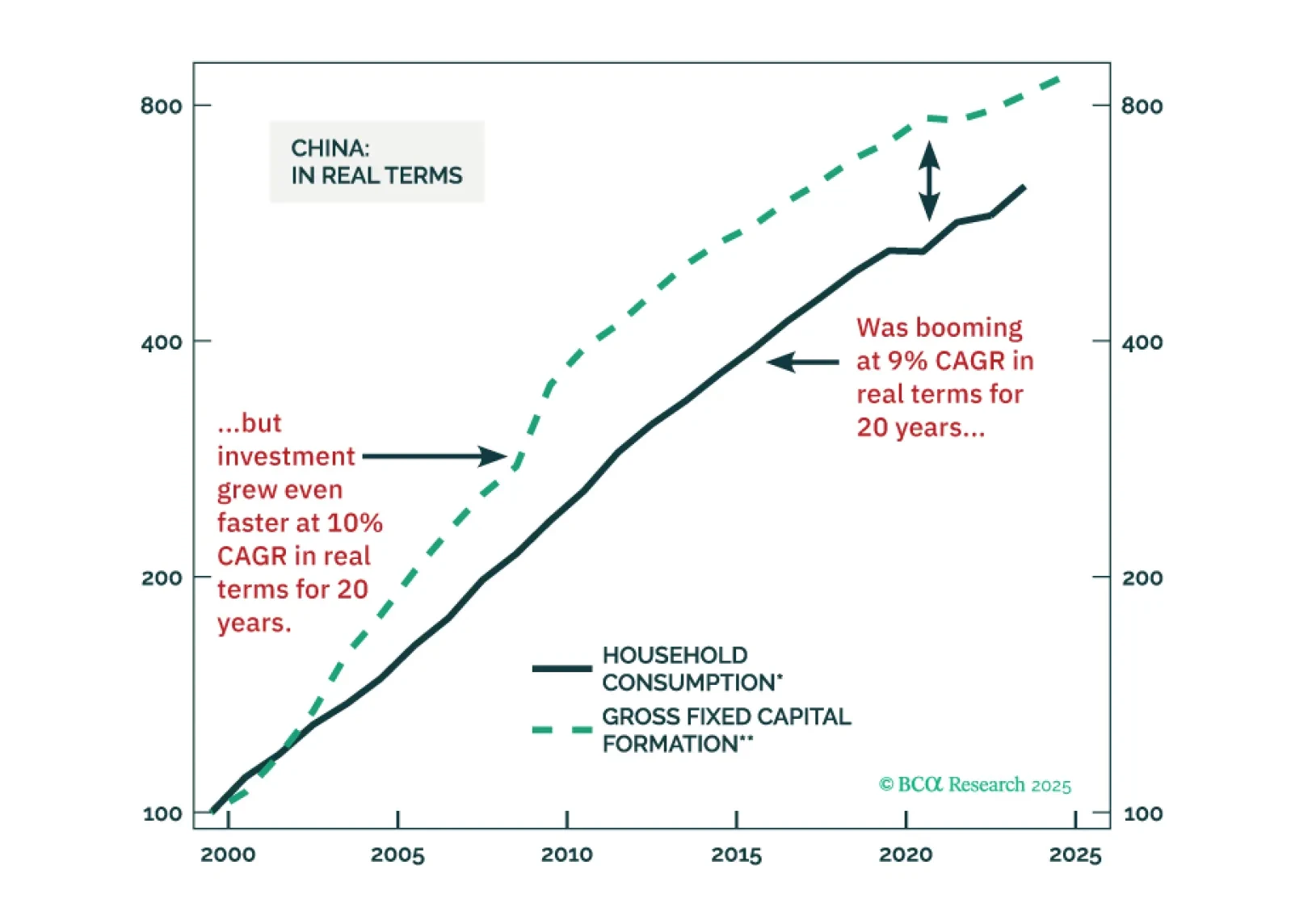

The prevailing narrative around the world is that Chinese households are not spending enough and that China has overly relied on exports for economic growth. Some parts of this conjecture are incorrect. The primary economic imbalance in China is neither inadequate consumption nor outsized exports. The main economic excess is overinvestment.

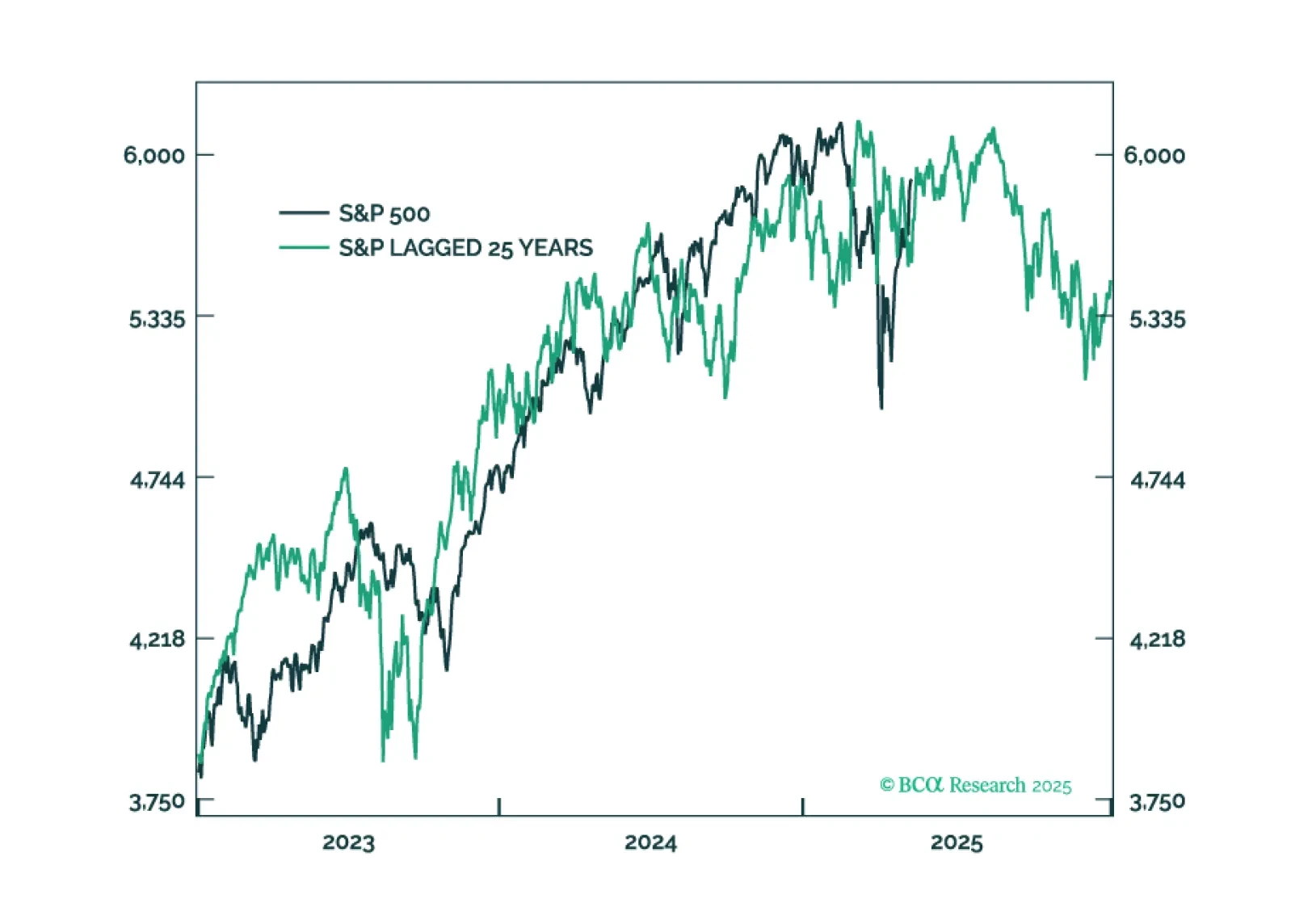

This year’s plunge in tech stocks followed by the recent strong countertrend rally is eerily reminiscent of 2000. But the market and economic parallels between 2025 and in 2000 run much deeper. This report lists 10 striking parallels between 2025 and 2020, then highlights some important differences, and ends by describing how the rest of 2025 might unfold based on a playbook that is: 2025 = ‘2000 with some tweaks.’

Negotiations on trade, Iran, and Ukraine will prove critical this month. Markets will remain volatile because positive data surprises enable the White House to press its hawkish tariff hikes, while negative surprises force the White House to backpedal.