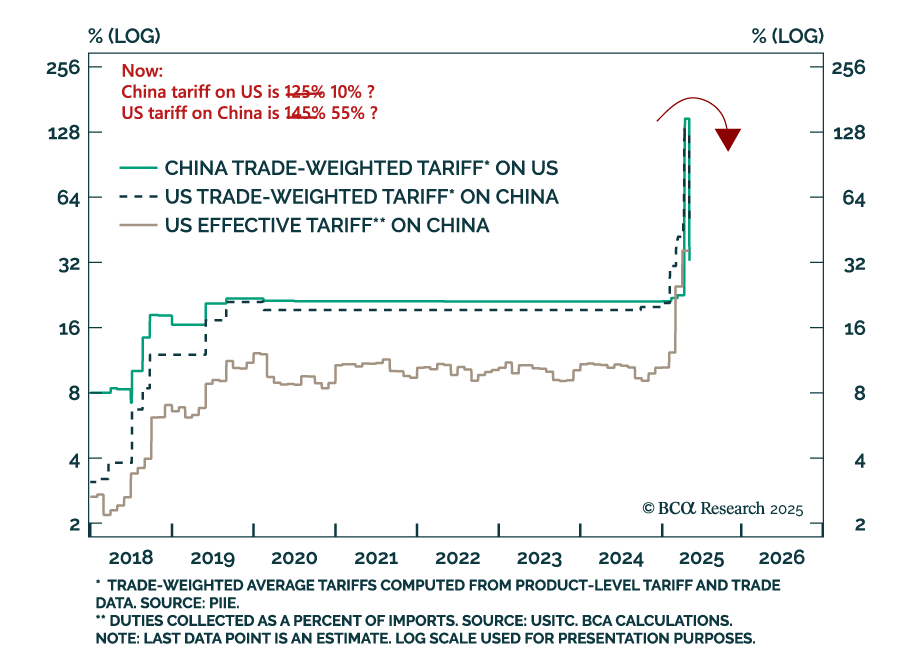

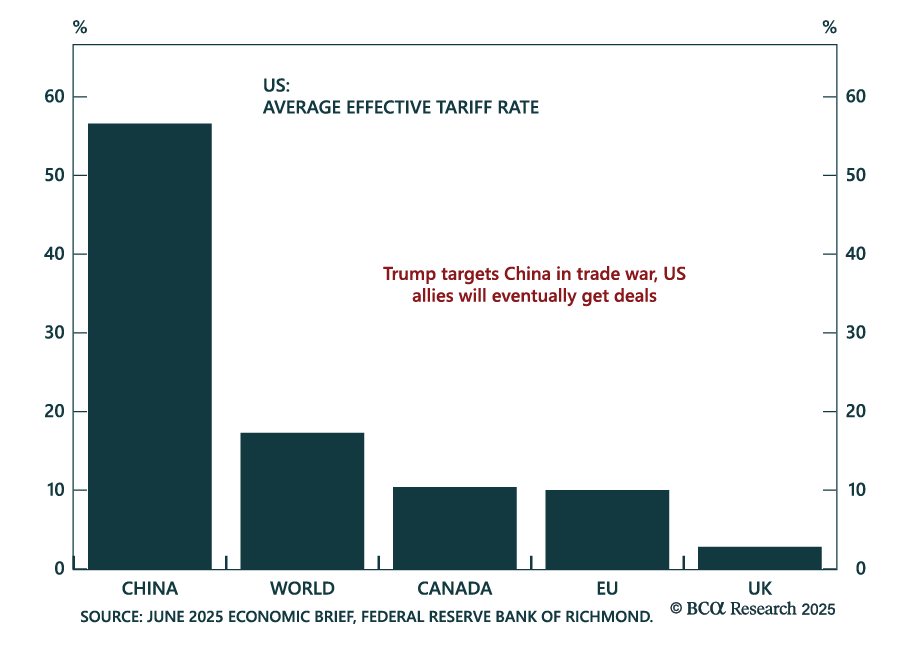

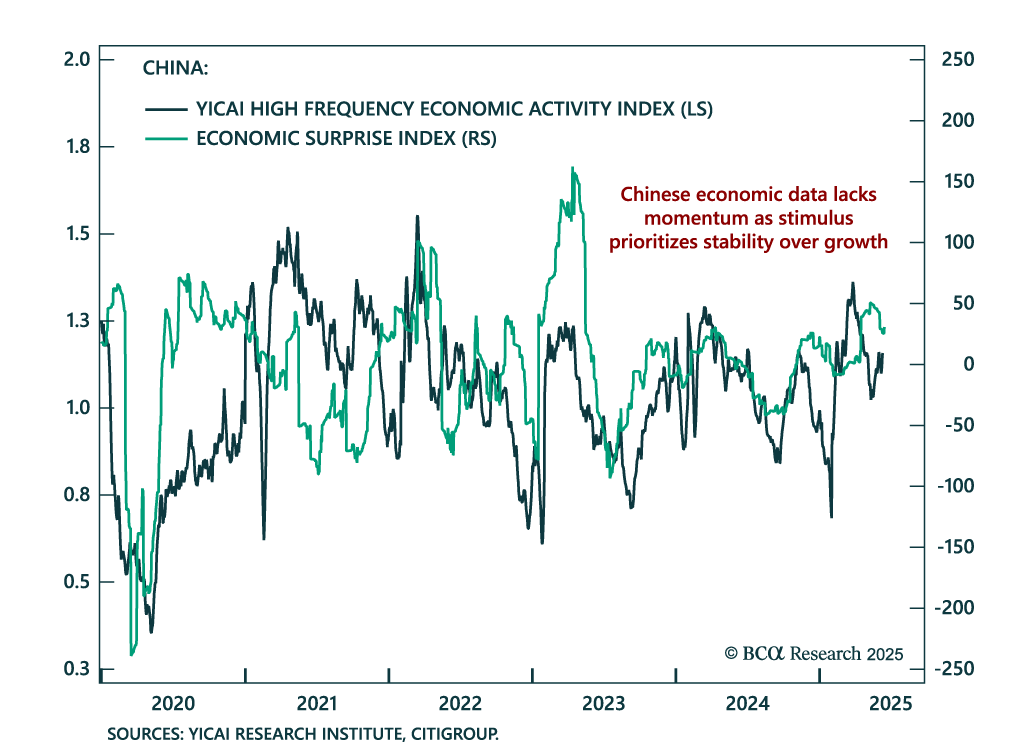

China

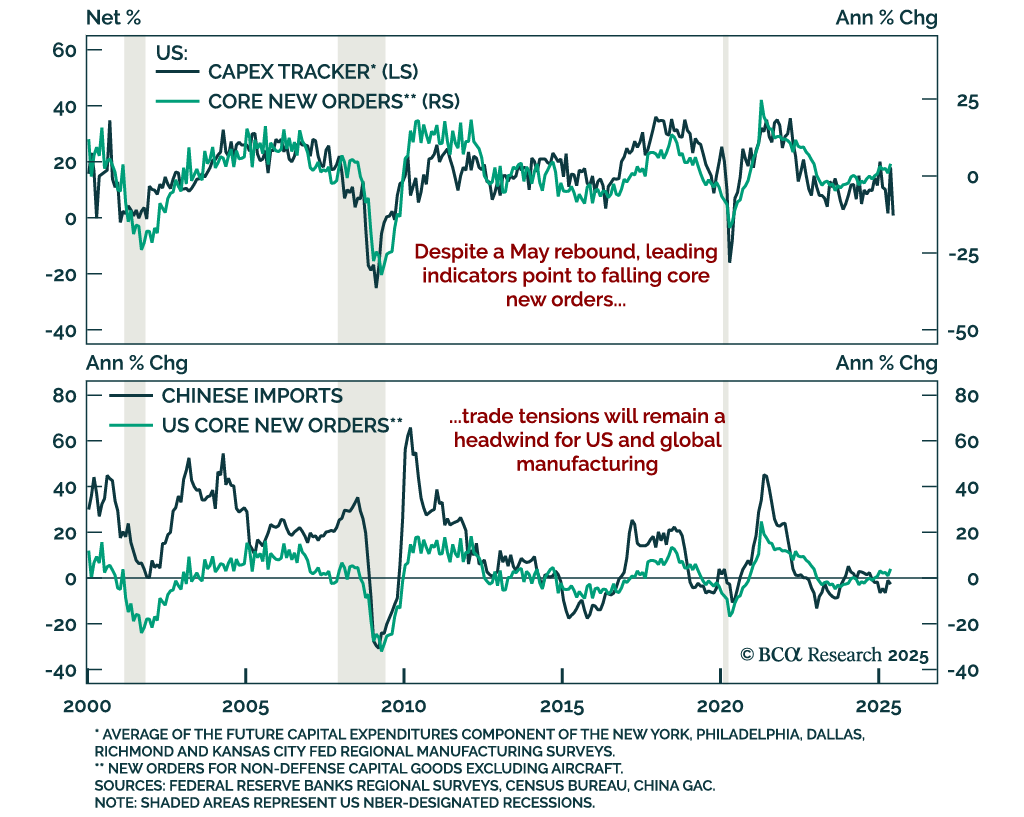

Acute geopolitical risks, like a massive oil shock, may be abating. But structural geopolitical risk remains high and could upset a blithe market. Cyclical economic risks are underrated as the US slows down and China continues to stumble. Investors should book some profits in anticipation of tariff implementation and a downturn in hard economic data.

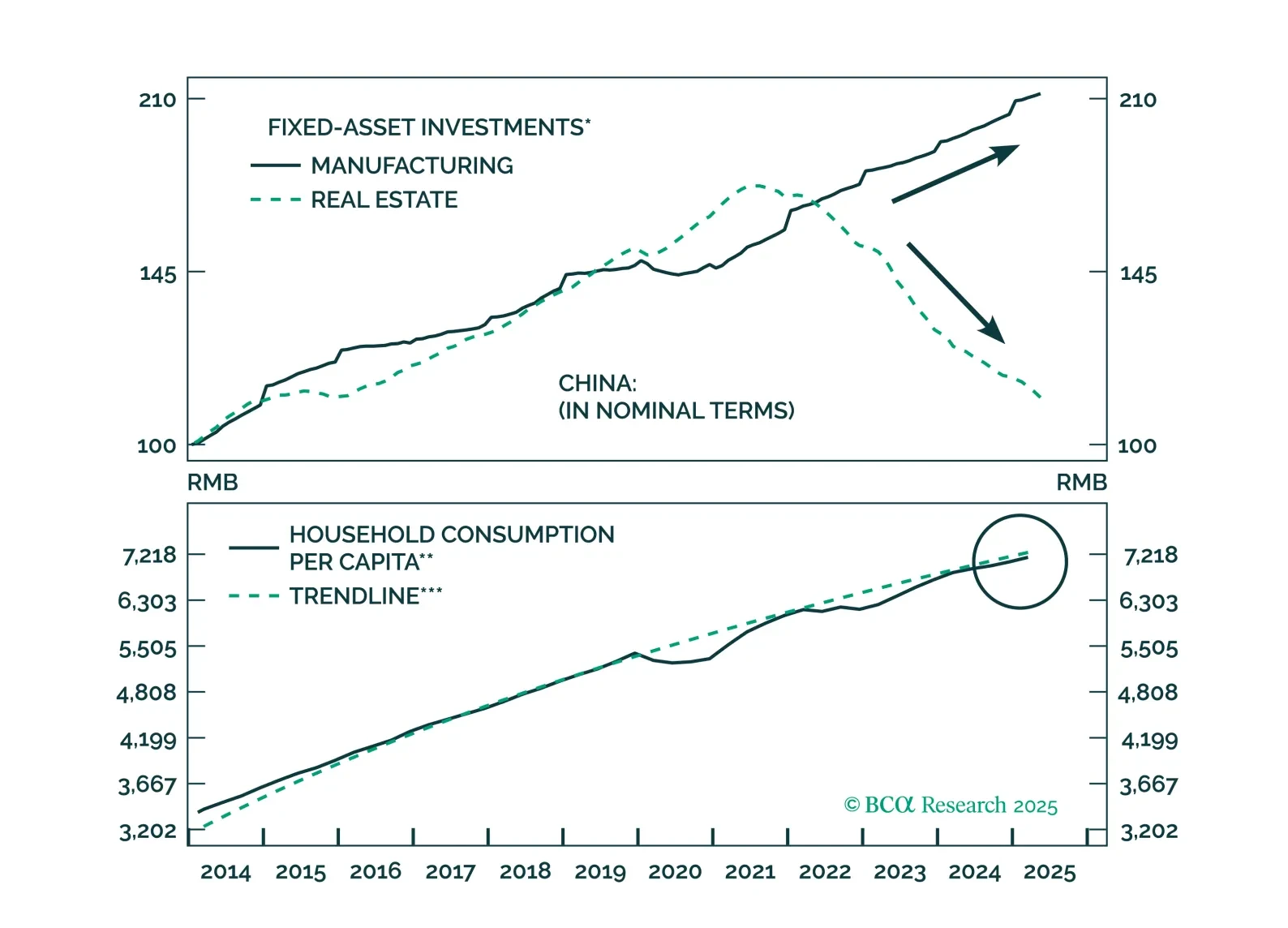

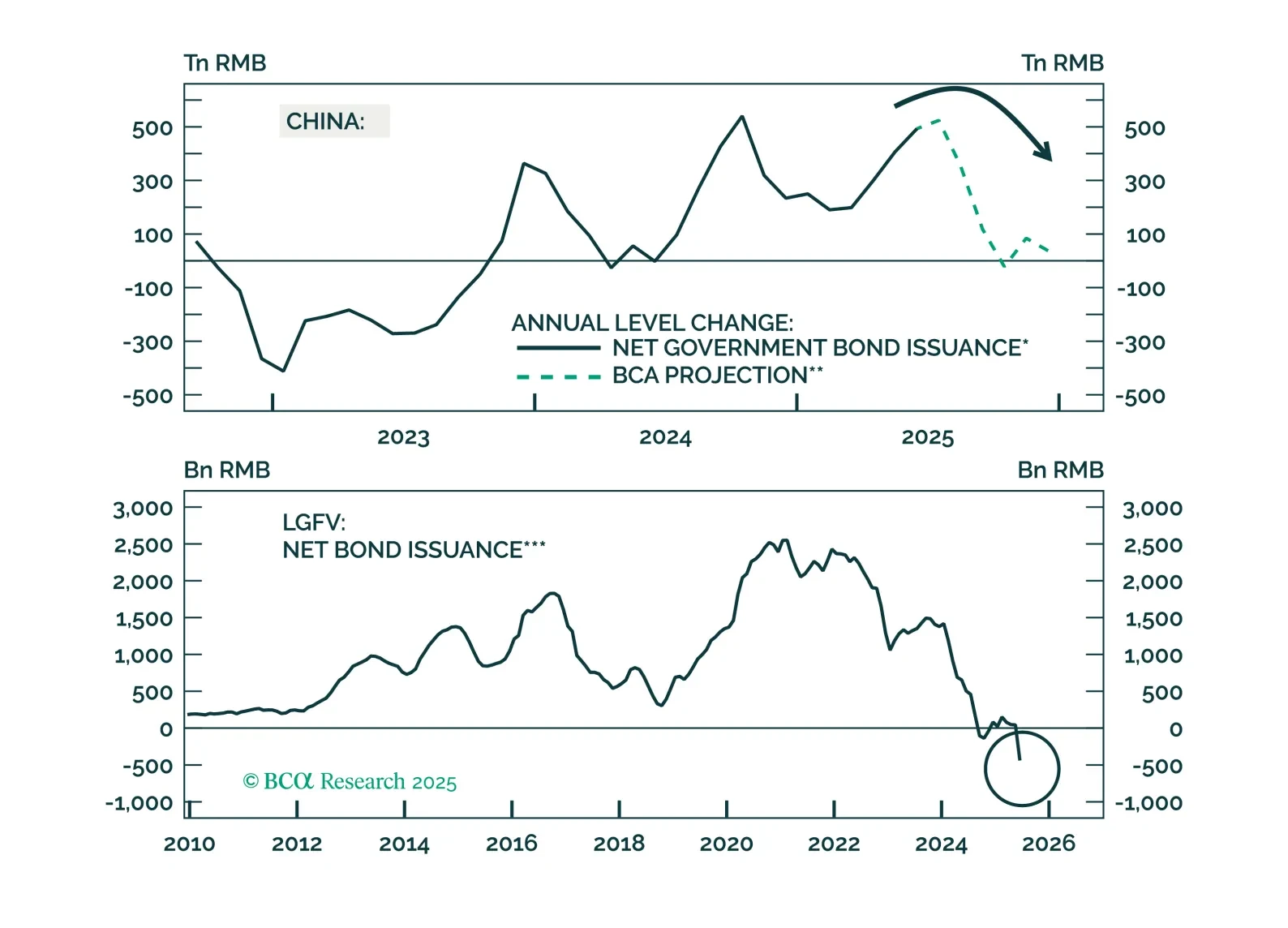

This report analyzes China’s persistent deflation, which is rooted in supply-side forces. Consumption support will be slow and incremental, keeping deflationary pressures elevated for the next 6–12 months.

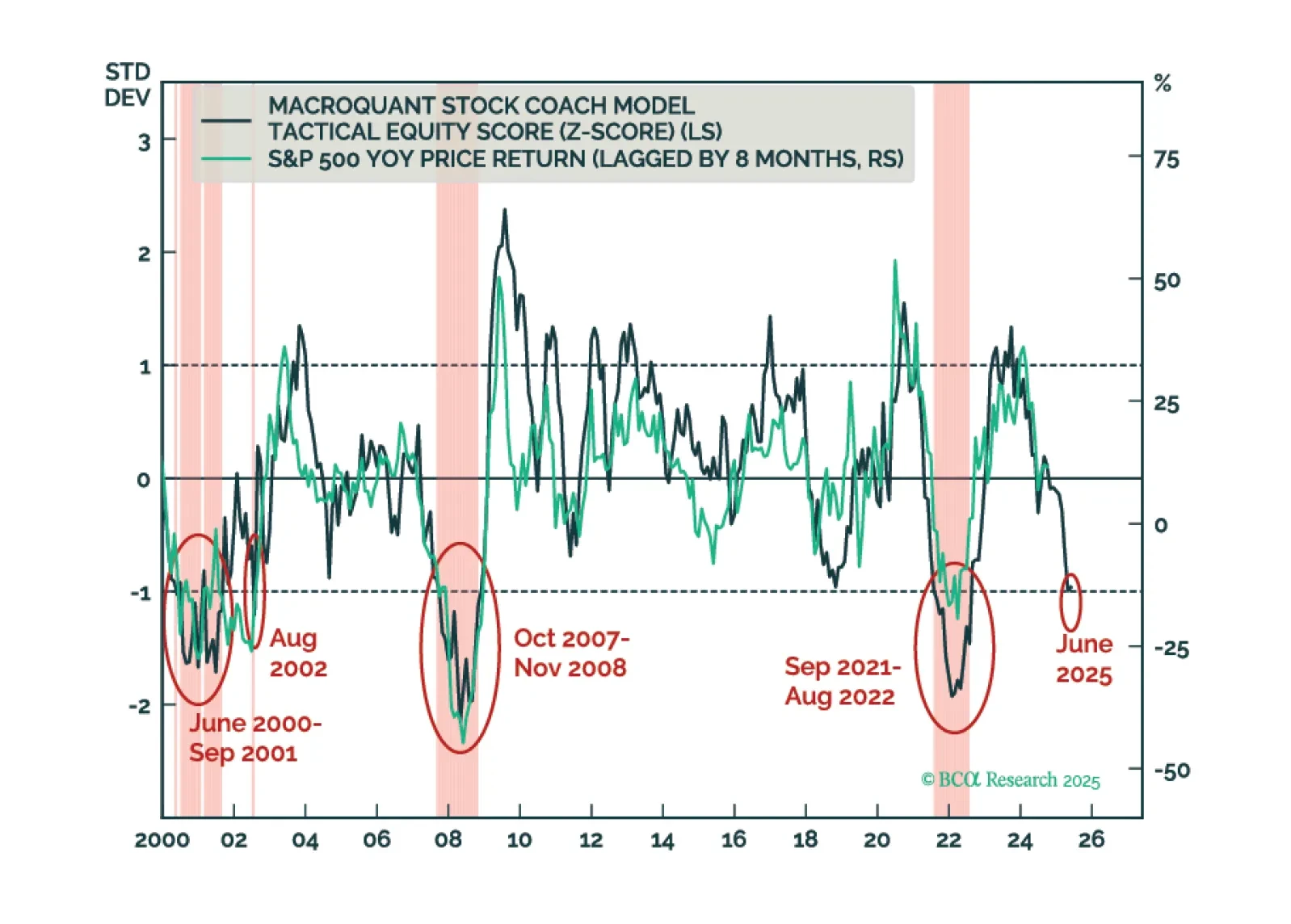

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

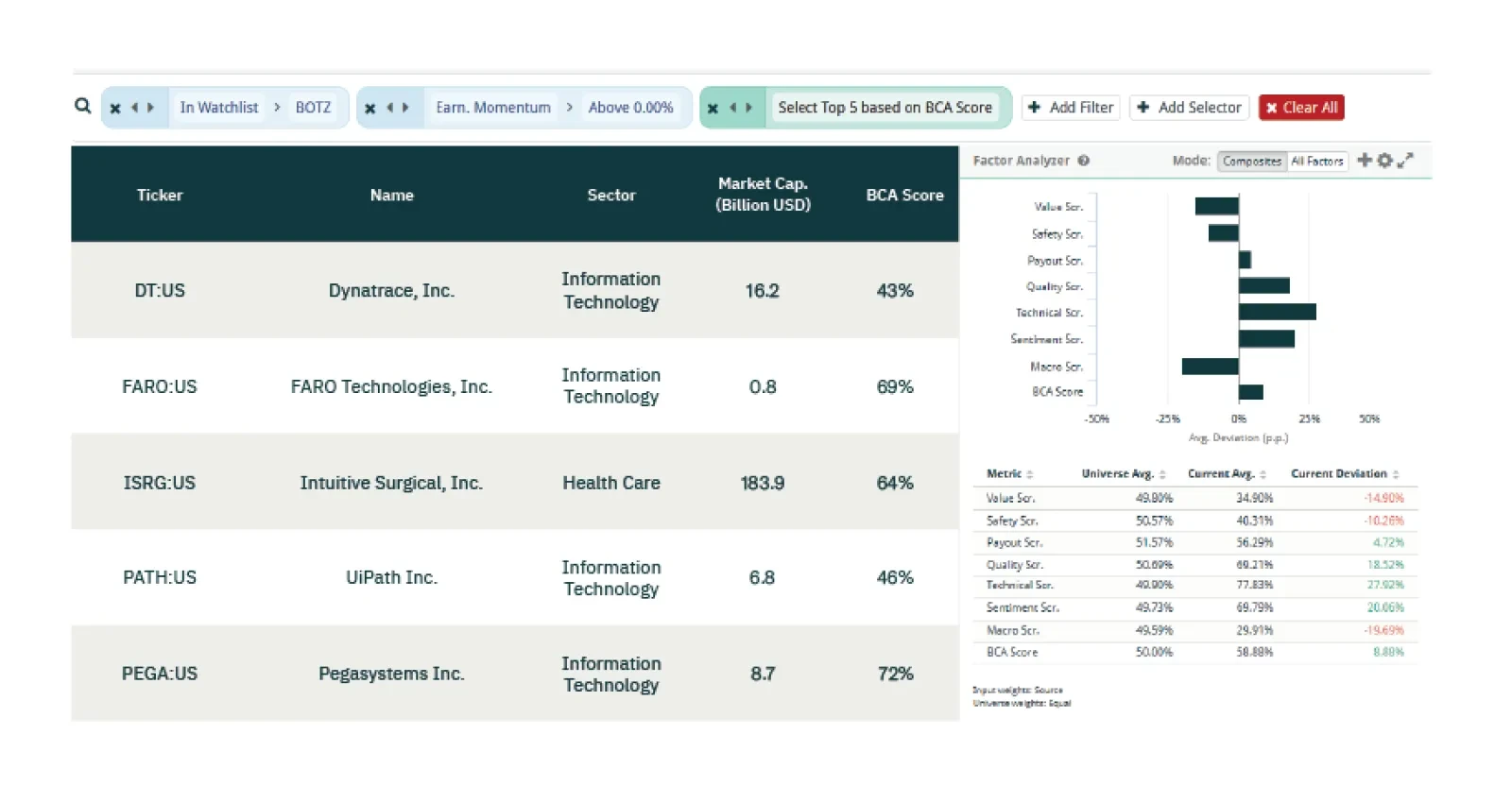

This week our three screeners explore equity trades in Robotics, European Quality and Technical, and Hong Kong.

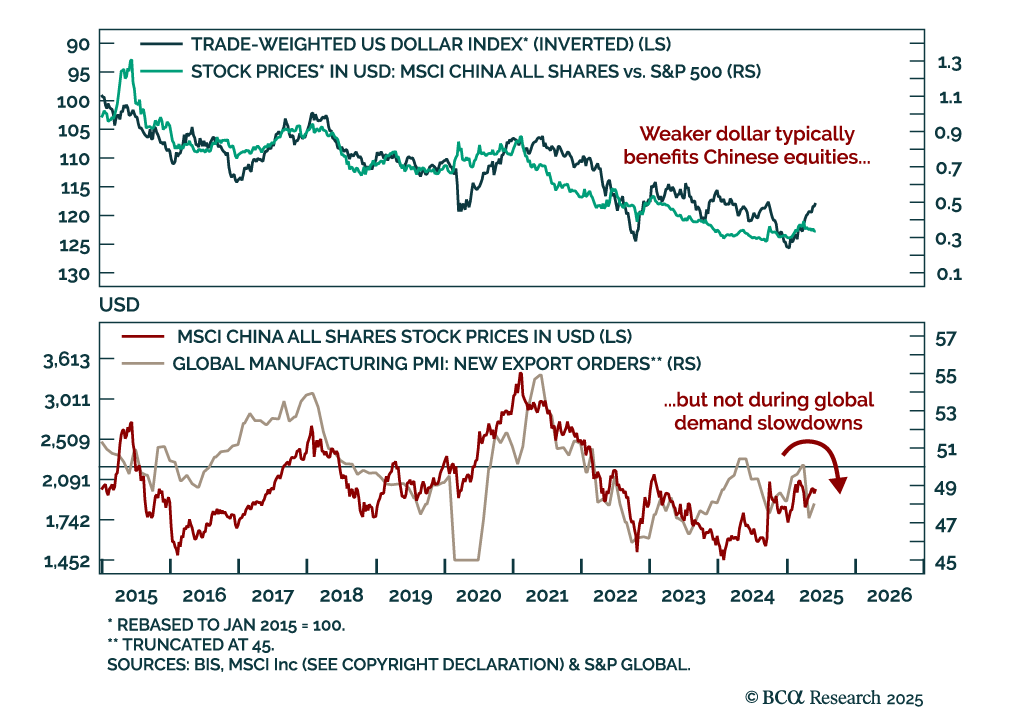

The London Sino-US trade talks offered hope of de-escalation, but Chinese equities remain under pressure from deflationary headwinds and lack a clear macro catalyst to trend higher.