Brazil

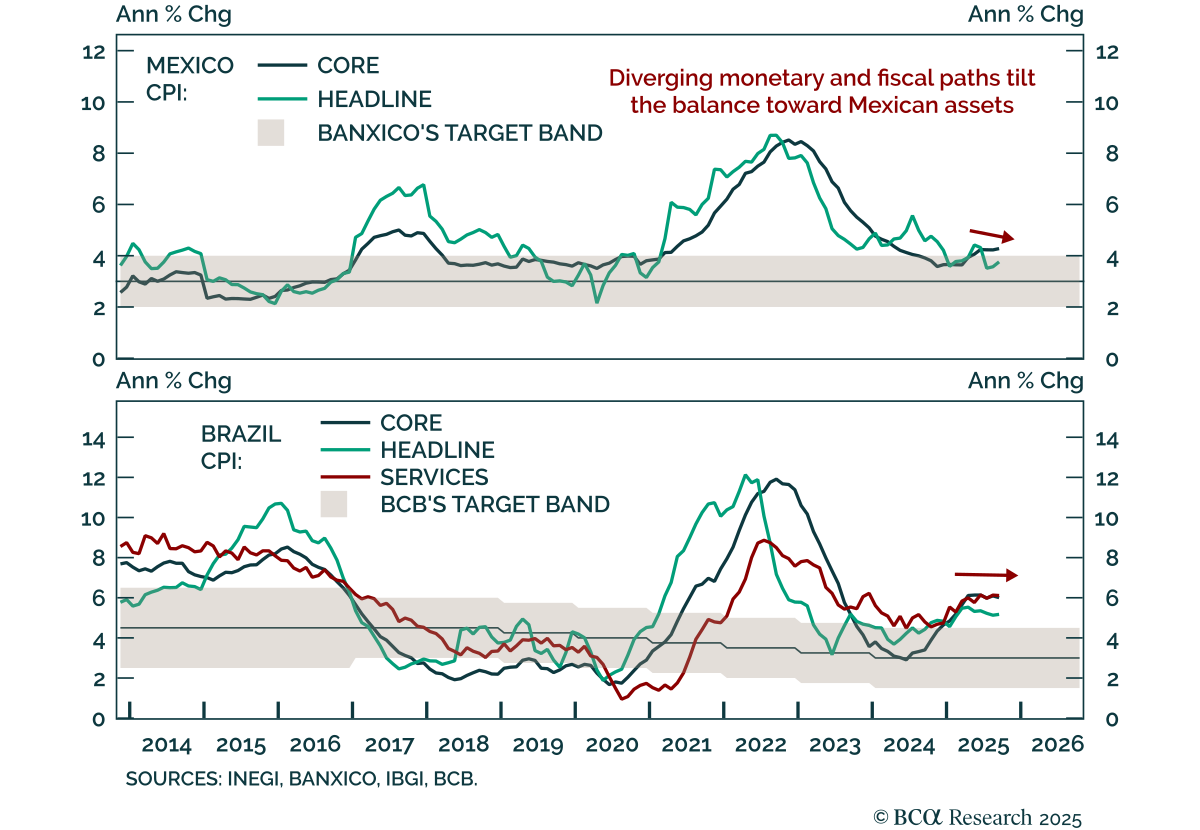

September CPI releases in Brazil and Mexico reinforce a divergent inflation and policy outlook that supports an overweight stance in Mexican local bonds and currency relative to Brazilian assets. Brazil’s headline CPI at 5.2% was slightly higher than in…

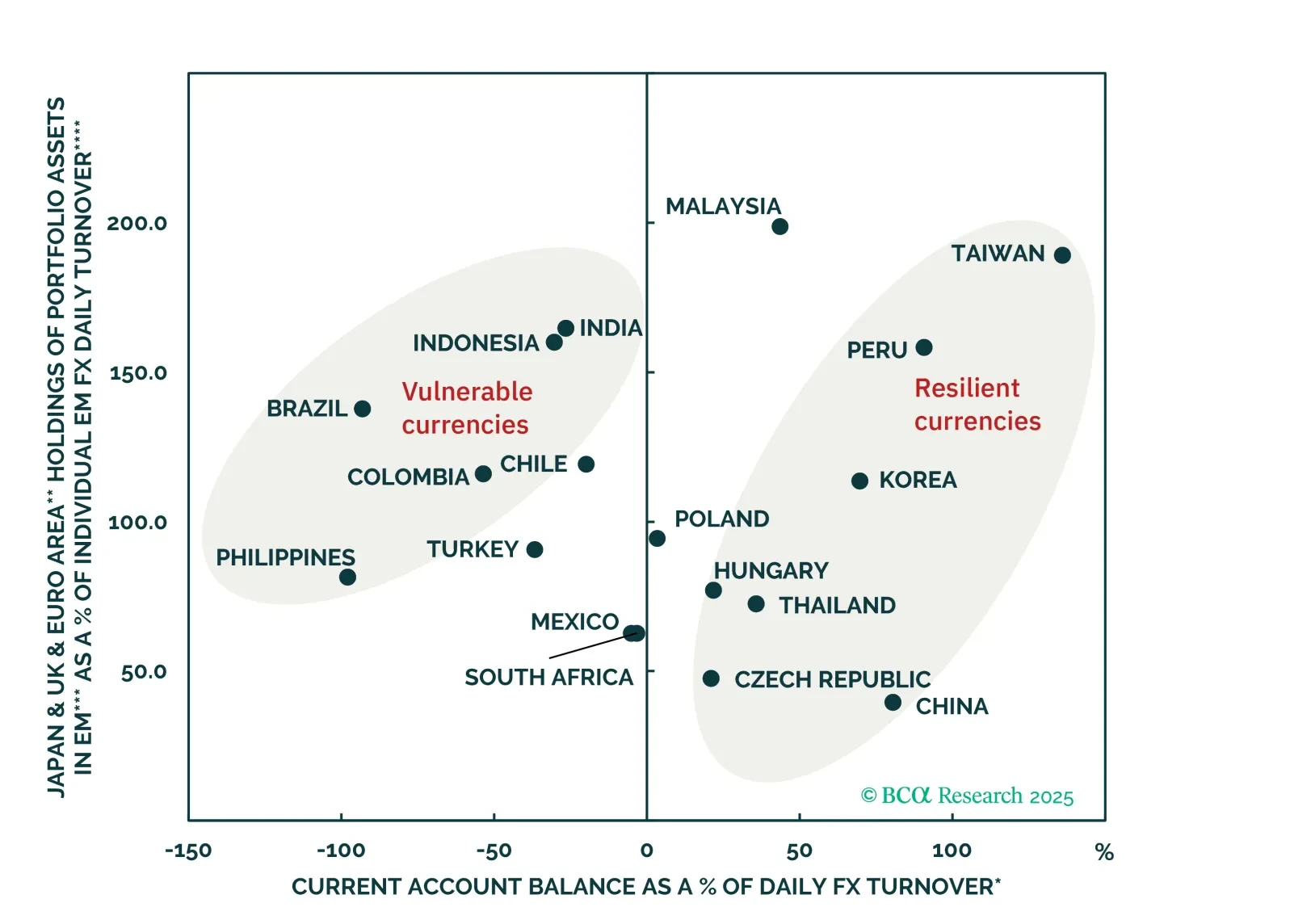

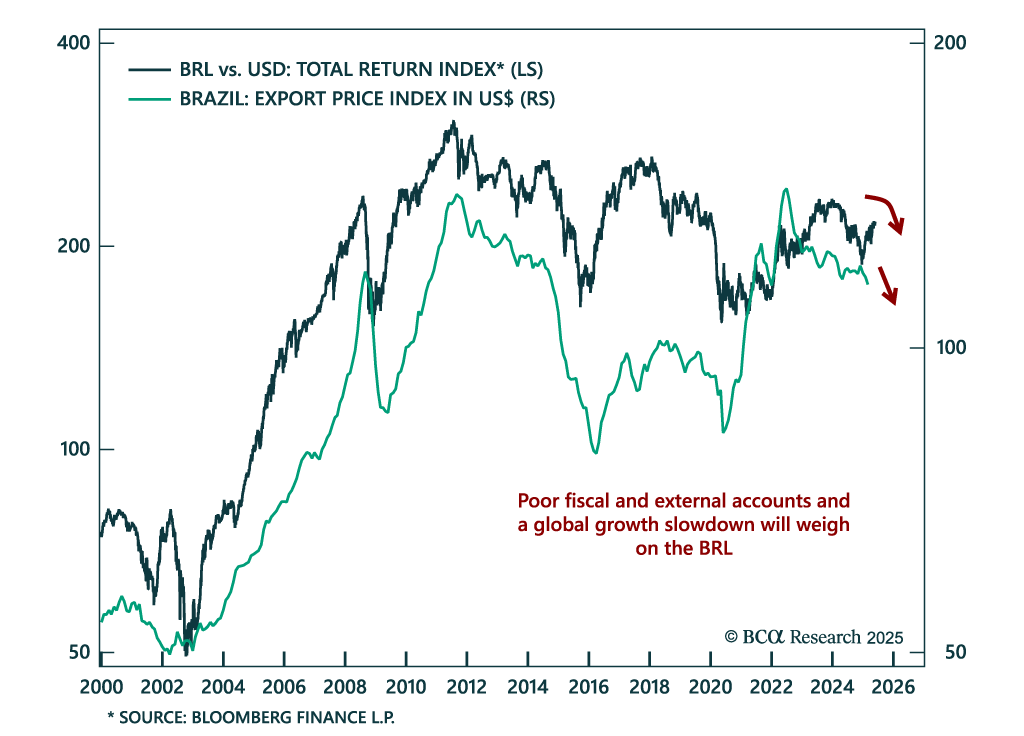

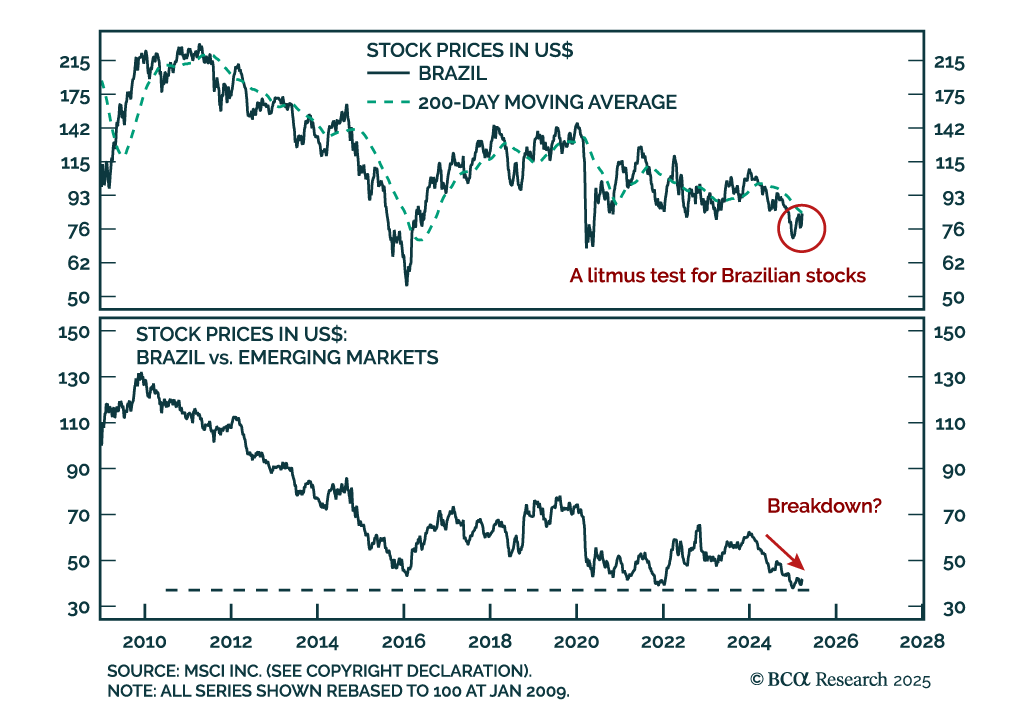

Despite widespread investor optimism Brazil’s currency outlook is challenged by a toxic mix of poor external, fiscal, and macro fundamentals. Expect BRL to underperform most EM peers.

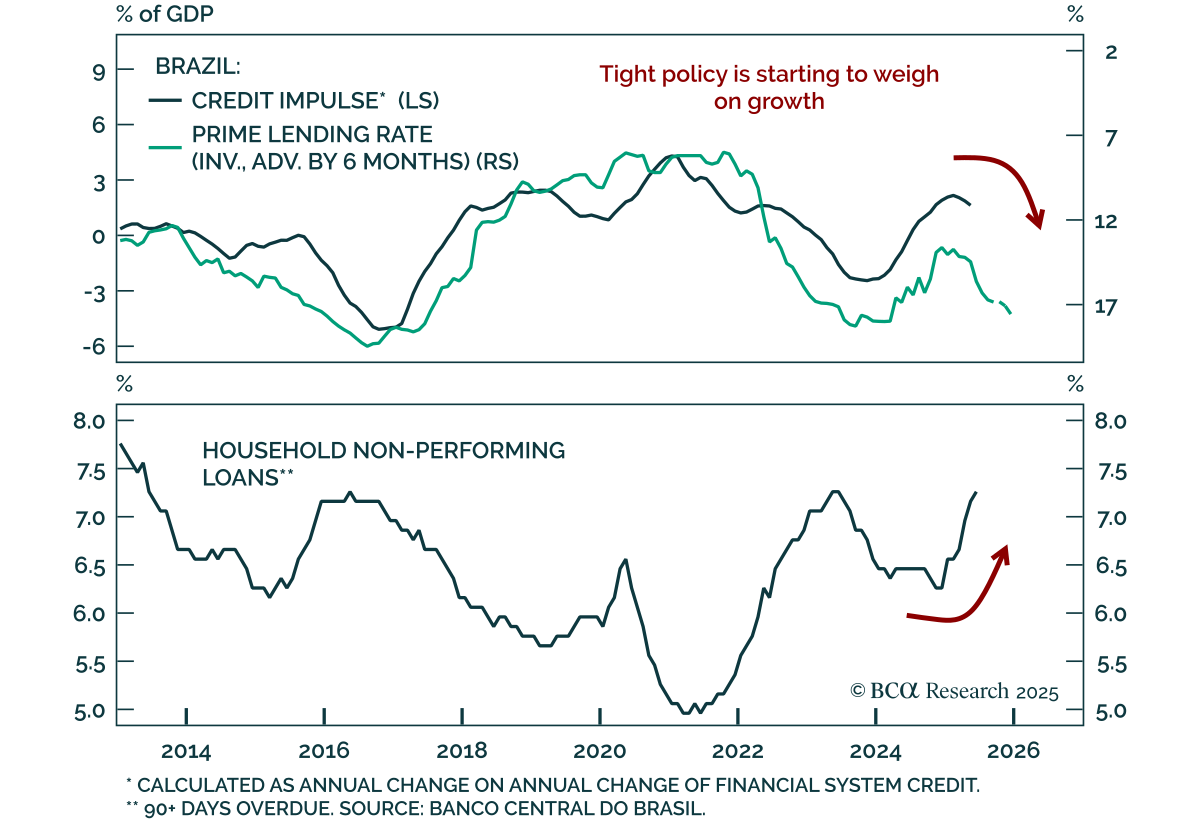

The Central Bank of Brazil (BCB) held rates at 15%, guaranteeing a sharp growth slowdown and reinforcing our underweight stance on Brazilian equities versus EM. All Copom board members voted to maintain an ultra-hawkish policy due to unanchored inflation…

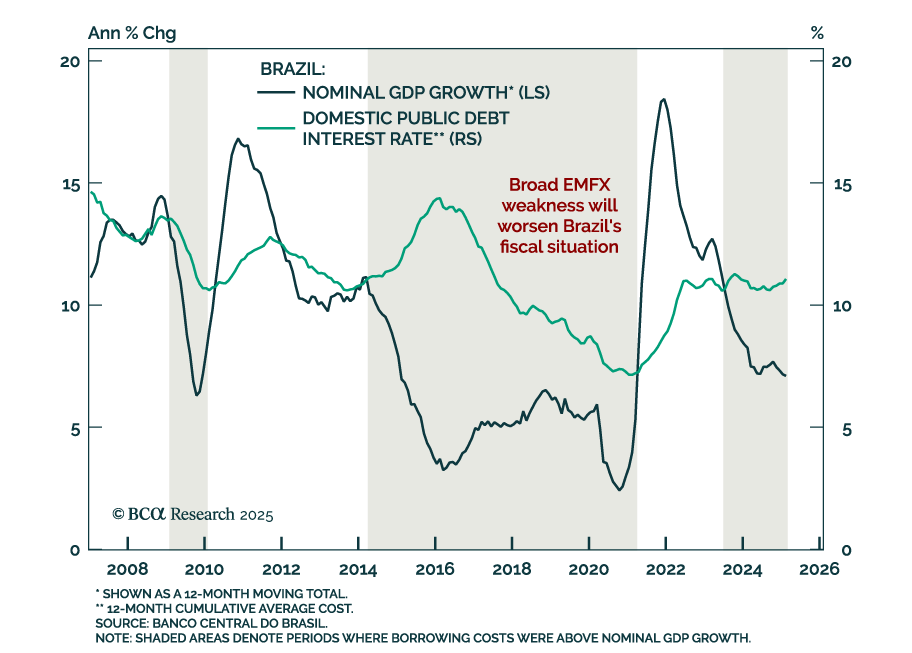

BCA’s Emerging Markets strategists continue to underweight Brazilian equities, local bonds, and sovereign credit, and initiated a receiver position in 2-year swap rates. Brazil’s public debt remains on an unsustainable trajectory, with neither current policy…

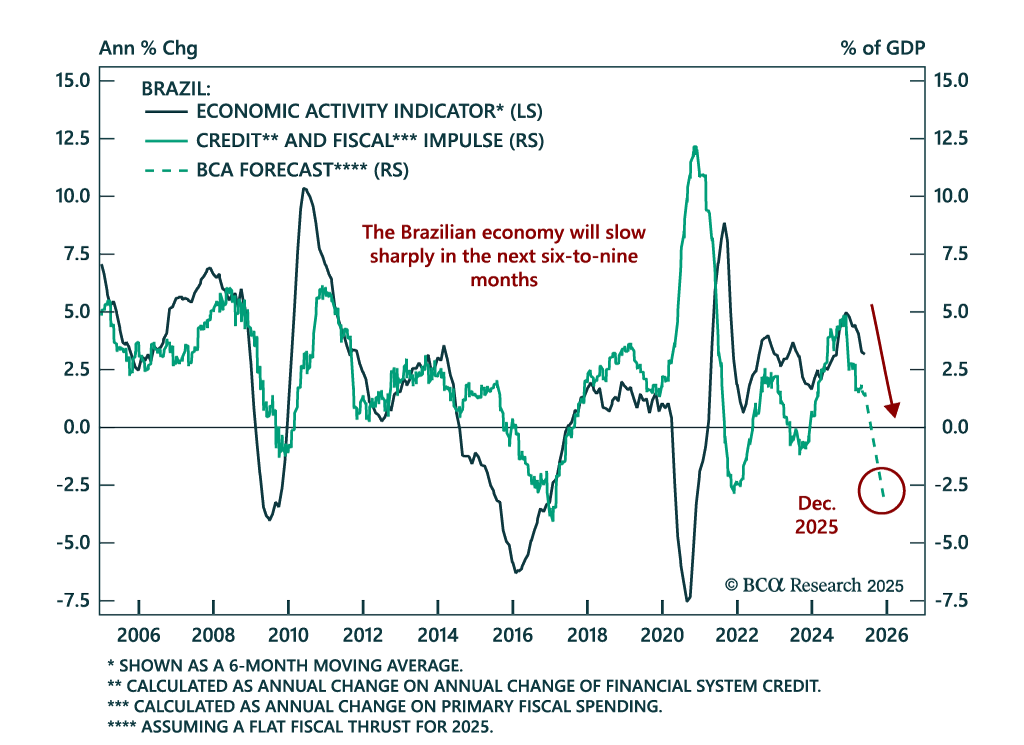

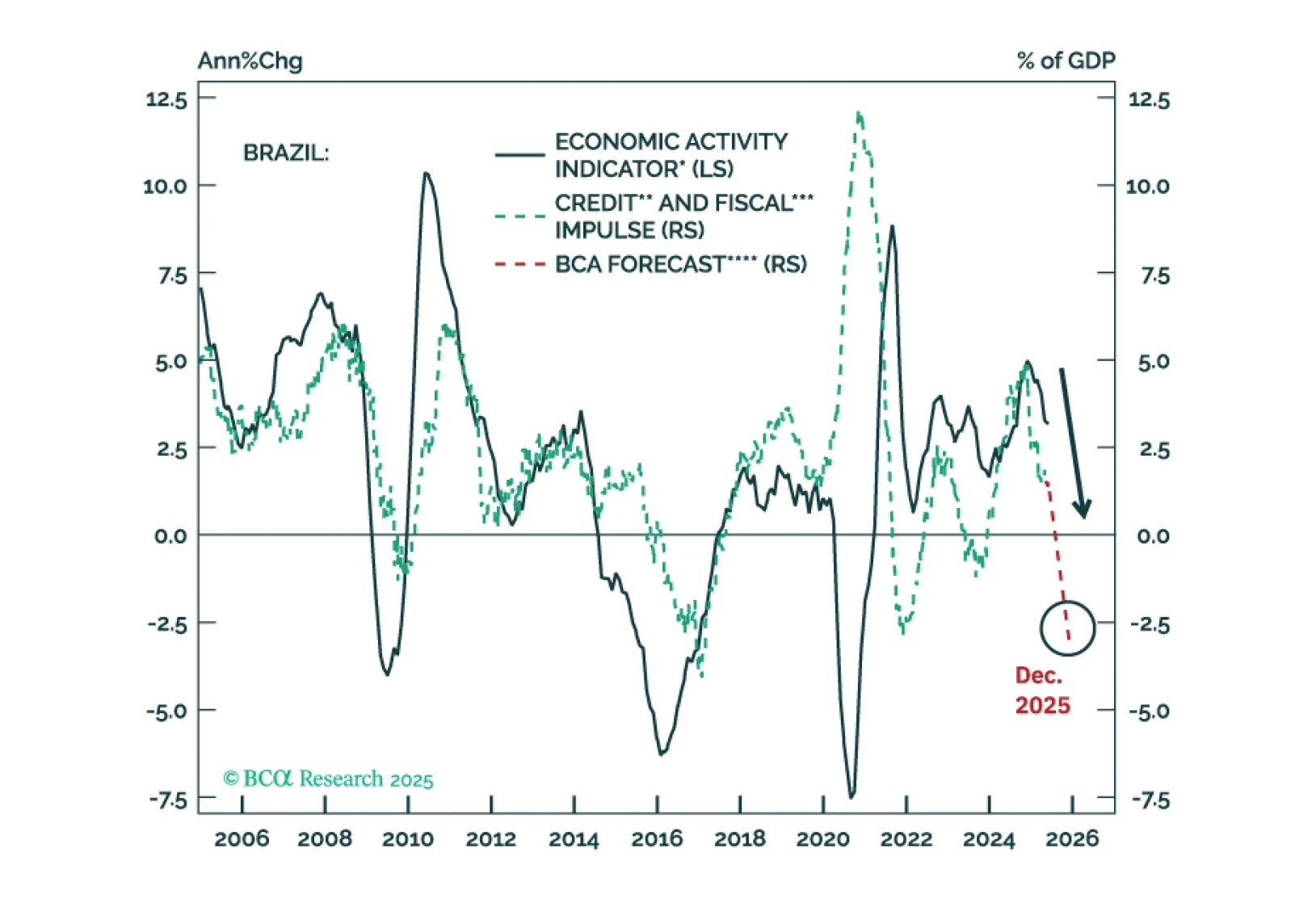

A potential right-wing government in 2027 will not stabilize the trajectory of the public debt-to-GDP ratio. Unsustainable public debt, a large current account deficit, and a sharp growth slowdown will lead Brazilian markets to underperform EM. Yet, to benefit from a quickly decelerating economy, we recommend receiving 2-year swap rates.

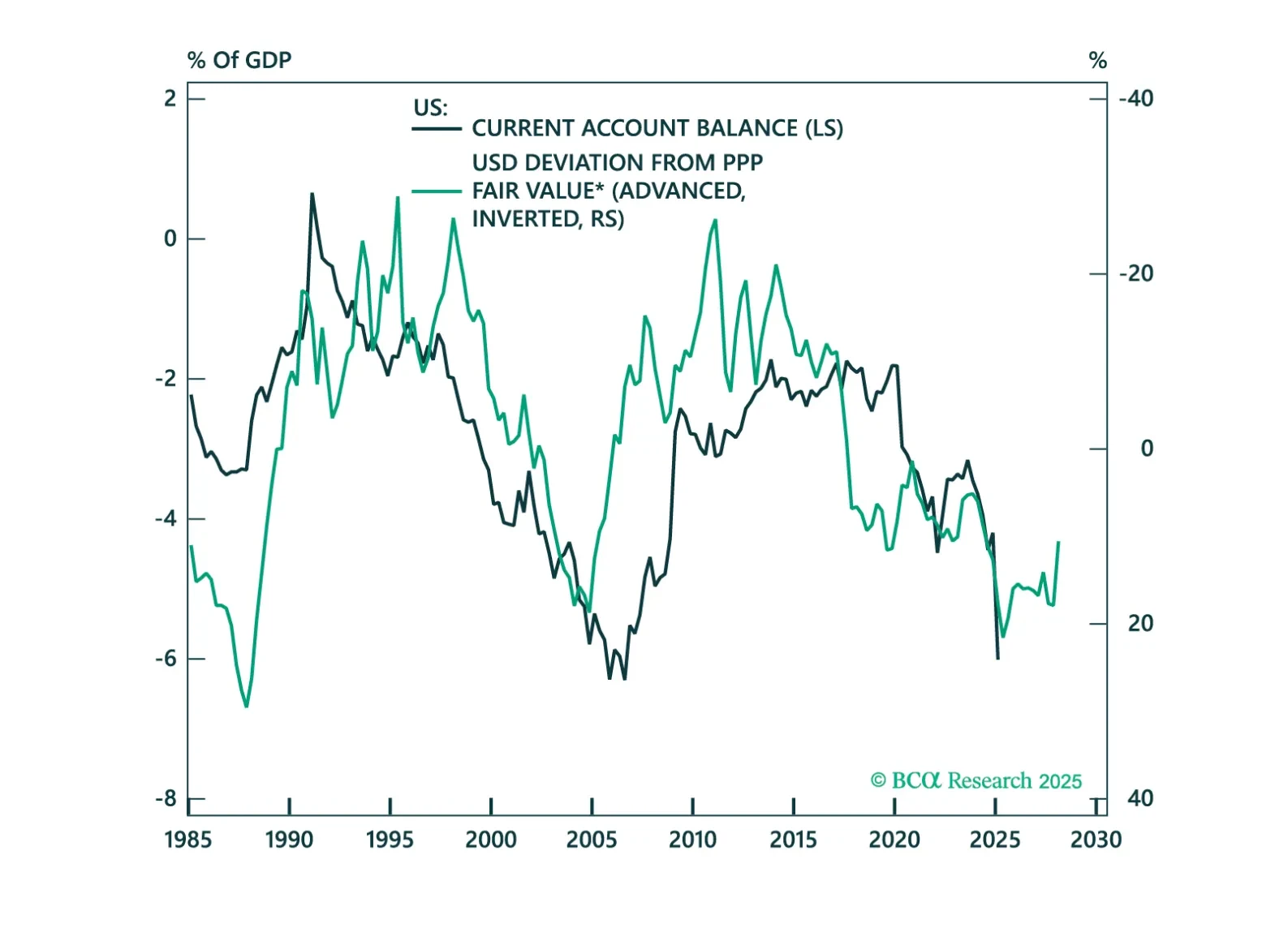

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.

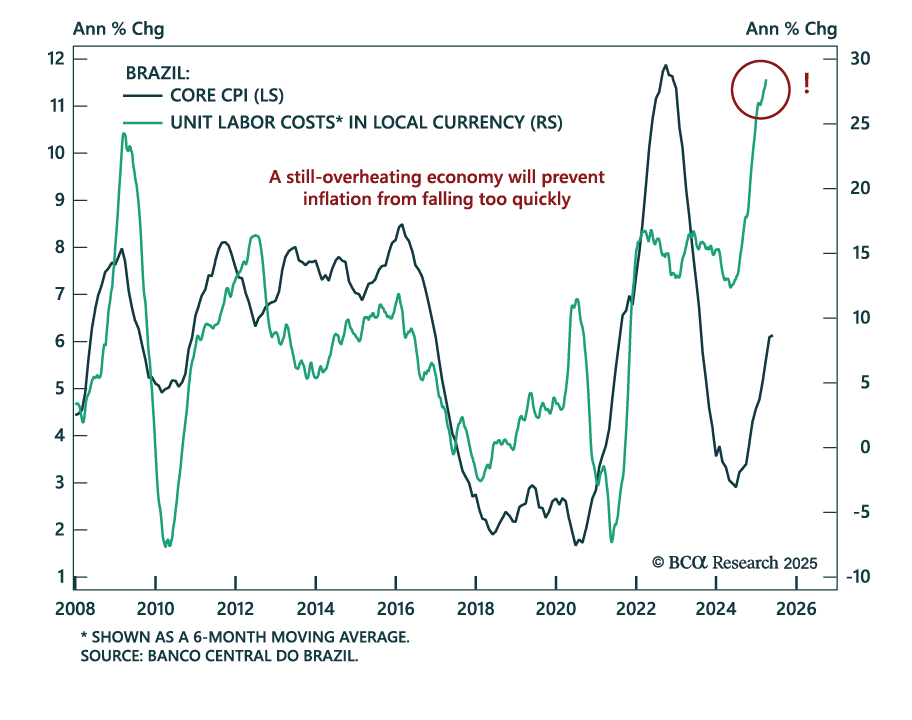

The May Brazilian CPI suggests that price pressures may have reached a peak, but do not expect immediate monetary easing to support fixed income markets. Headline CPI slowed to 5.3% y/y from 5.5% April, but core CPI remained flat at 6.1%. Despite…

The most recent Brazilian data surprised positively, but underlying economic troubles will spoil the party for the country’s financial markets. Wholesale inflation came in at -0.49% in May relative to last month, while the unemployment rate fell from 7%…

Brazil’s deteriorating fiscal dynamics and rising stagflation risks reinforce our negative stance on Brazilian assets, both outright and relative to EM peers. The latest global financial turmoil, combined with President Trump’s disruptive tariffs and China’s…

Our Emerging Market strategists downgraded Brazilian equities as public debt dynamics deteriorate and macro fundamentals weaken. While they previously maintained a neutral stance despite being bearish on the Bovespa, the risks have become too pronounced to…