Base Metals & Iron Ore

Highlights The slowdown in global industrial activity appears to have bottomed. This, along with an apparent shared desire for a ceasefire in the Sino-US trade war, points toward a measured recovery in manufacturing and global trade, which will contribute to higher iron-ore and steel demand beginning in 1H20. A trade-war ceasefire, should it endure, will reduce global economic uncertainty. Along with continued monetary accommodation from systematically important central banks, reduced economic uncertainty will boost global growth and industrial-commodity demand generally by allowing the USD to weaken. We expect Beijing policymakers to remain focused on keeping GDP growth above 6.0% p.a. To that end, we believe a boost in infrastructure spending next year is likely, which also will be bullish for steel demand. Given China’s growing share of global steel production, we expect price differentials for high-grade iron ore – most of which comes from Brazil – to widen as steel demand increases next year. Given this view, we are initiating a strategic iron-ore spread trade at tonight’s close: Getting long December 2020 high-grade (65% Fe) futures traded on the Singapore Exchange vs. short the benchmark-grade (62% Fe) December 2020 futures traded on the CME. We recommend a 20% stop-loss on this recommendation. Feature Iron ore and steel demand will get a lift from the rebound our proprietary Global Industrial Activity (GIA) index has been forecasting for the past few months (Chart of the Week). The GIA index is designed to pick up changes in Chinese industrial activity, given its outsized influence on world industrial output, and also makes use of trade data, FX rates, and global manufacturing data. The rebound we are expecting will get a fillip from an apparent shared desire for a ceasefire in the Sino-US trade war, which, based on media reports, is close to being agreed. Should this ceasefire prove to be durable, it would contribute to a lowering of global economic policy uncertainty (GEPU), which, as we have shown recently, has kept the USD well bid to the detriment of industrial-commodity demand.1 Chart of the WeekBCA GIA Index Pick-Up Points To Higher Global Steel Demand

BCA GIA Index Pick-Up Points To Higher Global Steel Demand

BCA GIA Index Pick-Up Points To Higher Global Steel Demand

While we do expect economic uncertainty to decline next year, it will remain elevated due to continued Sino-US trade tensions – even if a “phase-one” deal is agreed – ongoing hostilities in the Persian Gulf, and popular discontent with the political status quo globally. As global economic uncertainty fades, the USD broad trade-weighted index for goods (TWIBG) will fall, which will bolster EM GDP growth, and a recovery in global trade next year (Chart 2). If, as media reports suggest, this so-called “phase-one” agreement includes a relaxation – or complete removal – of tariffs by the US on Chinese imports, we would expect manufacturing activity to pick up as Chinese manufacturers spin-up capacity to meet demand. A reduction in tariffs also will lessen the deadweight loss they imposed on US households, which will support higher consumption.2 Chart 2Reduced Global Economic Uncertainty Bolsters Global Trade Volumes, EM GDP

Iron Ore, Steel Prices Set To Lift

Iron Ore, Steel Prices Set To Lift

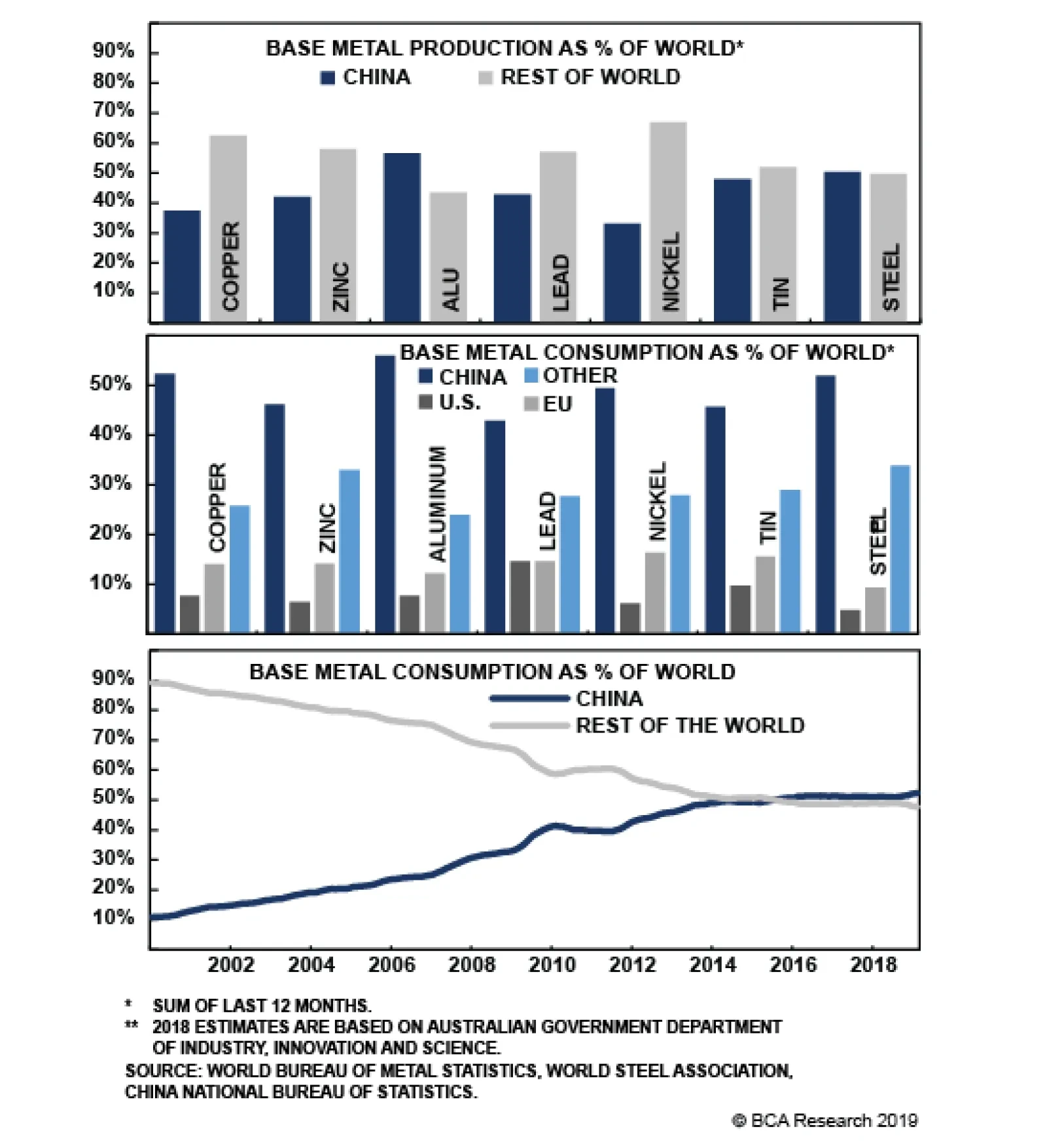

That said, economic uncertainty still remains high. This uncertainty is destructive of demand and will remain a key risk factor in 2020. While we do expect economic uncertainty to decline next year, it will remain elevated due to continued Sino-US trade tensions – even if a “phase-one” deal is agreed – ongoing hostilities in the Persian Gulf, and popular discontent with the political status quo globally. China’s Steel Demand Holds Up In Trade War China accounts for more than half of global steel production and consumption, and the lion’s share of seaborne iron-ore consumption (Chart 3). This makes its steel industry critically important to the global economy, and a key barometer of industrial activity worldwide. With global industrial activity bottoming and moving higher, and the USD expected to weaken, we expect iron ore demand and steel production in China to move higher next year as domestic and global demand for steel rises. China’s apparent steel demand held up fairly well during the slowdown observed in manufacturing and in commodity demand growth globally, averaging 8% y/y growth ytd (Chart of the Week, bottom panel). It now appears to be stalling in the wake of the global manufacturing slowdown. In addition, Chinese credit stimulus remains weak, contrary to expectations. However, with global industrial activity bottoming and moving higher, and the USD expected to weaken, we expect iron ore demand and steel production in China to move higher next year as domestic and global demand for steel rises.3 Chart 3China Dominates Global Steel Production and Consumption

China Dominates Global Steel Production and Consumption

China Dominates Global Steel Production and Consumption

Chart 4Construction, Real Estate Strength Offset Lower Chinese Auto Production

Construction, Real Estate Strength Offset Lower Chinese Auto Production

Construction, Real Estate Strength Offset Lower Chinese Auto Production

Greater demand for steel by the construction and real estate sectors offset lower consumption by the automobile industry in China this year, as manufacturing and trade slowed globally (Chart 4). Overall, apparent demand is still growing (Chart 5), which will continue to support iron ore imports, even though domestic production of low-grade ore picked up as steelmakers’ margins tightened earlier in the year (Chart 6). Chart 5China"s Apparent Steel Demand Growth Holds Up During Industrial Slowdown

China"s Apparent Steel Demand Growth Holds Up During Industrial Slowdown

China"s Apparent Steel Demand Growth Holds Up During Industrial Slowdown

Chart 6China Iron Ore Imports Remain Stout

China Iron Ore Imports Remain Stout

China Iron Ore Imports Remain Stout

Chinese imports from Brazil have rebounded following the Brumadinho tailings dam collapse in January at Vale’s Córrego do Feijão iron ore mine, which killed close to 300 people. The collapse in margins from steel mills combined with outages to Brazil and Australia high-grade ore exports led to a rise in imports and domestic production of low-grade iron ore. High-Grade Iron Ore Favored; Policy Uncertainty Persists Our overall view for industrial commodities – iron ore, steel, base metals and crude oil – is constructive but not wildly bullish going into next year. Our oil view, for example, calls for a rally in the average price of crude oil next year of ~ 10% from current levels for Brent crude oil, the world benchmark. While we expect global monetary stimulus to offset much of the tightening of financial conditions brought on by the Fed’s rate hikes last year, and China’s de-leveraging campaign of 2017-18, elevated economic uncertainty will keep the USD better bid that it otherwise would be absent the Sino-US trade war and global economic policy uncertainty. This translates into weaker commodity demand, generally, as a strong USD raises local-currency costs for consumers and lowers local-currency production costs for producers. At the margin, both push commodity prices lower. On a relative basis, we expect the more efficient, less-polluting technology likely will be called on to meet higher steel demand – in China and globally – next year, which means higher-grade iron ore will be favored by Chinese steel mills as profitability improves. For iron ore and steel in particular, environmental considerations also are important, given the Chinese government's “Blue Skies Policy” aimed at reducing the country’s high levels of air pollution.4 This policy has led to the forced retirement of older, highly polluting steelmaking capacity, which has been replaced with newer, less-polluting technology that favors high-grade iron ore. However, the application of regulations designed to reduce pollution has been uneven, and still relies on local compliance, which has been spotty. We expect demand for high-grade ore will increase as global manufacturing and trade also recovers. On a relative basis, we expect the more efficient, less-polluting technology likely will be called on to meet higher steel demand – in China and globally – next year, which means higher-grade iron ore will be favored by Chinese steel mills as profitability improves. The restoration of high-grade exports from Brazil means this ore will be available. It is worthwhile noting that these steelmakers account for an increasing share of global capacity. For this reason, we expect demand for high-grade ore will increase as global manufacturing and trade also recovers (Chart 7). Given our view, at tonight’s close we will get long December 2020 high-grade iron-ore futures (65% Fe) traded on the Singapore Exchange vs. short benchmark-grade iron-ore futures (62% Fe) traded on the CME. Both are quoted in USD/MT and settle basis Chinese port-delivery (CFR) indexes in cash. Given the uncertain nature of the durability and depth of the ceasefire currently being negotiated by the US and China, we will keep a stop-loss on this position of 20%. Bottom Line: China’s steel demand has held up relatively well despite the global slowdown in manufacturing and trade. Given our expectation for a pick-up in global growth – in response to global monetary and fiscal stimulus and lower economic uncertainty in the wake of a ceasefire in the Sino-US trade war – we expect Chinese steel demand to resume growing. This will support iron ore prices, particularly for high-grade ores. On the back of this expectation, we are recommending an iron-ore spread trade, going long high-grade futures vs. short benchmark-grade iron ore futures. Chart 7High-Grade Iron Ore Should Outperform Strategically

High-Grade Iron Ore Should Outperform Strategically

High-Grade Iron Ore Should Outperform Strategically

Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Hugo Bélanger Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com Market Round-Up Energy: Overweight. Bloomberg reported China is looking to invest between $5-$10 billion in the Saudi Aramco IPO through various vehicles. Such an investment would give China a deeper stake in the Kingdom’s oil industry, and a hedge to price shocks. In addition, it could open the way for deeper investment in the Saudi oil and petchems industries. For KSA, as we have argued in the past, a deepening of China’s investment and involvement in the Kingdom’s economy would diversify the states that have a vested interest in ensuring its safety.5 We will be updating our analysis of China’s pivot to the Middle East, and KSA’s pivot to Asia next week. Separately, we the last of our Brent backwardation trades – i.e., long December 2019 Brent vs. short December 2020 Brent – was closed last week with a gain of 110.8%. Base Metals: Neutral. Copper prices are up 6% vs. last month, supported by supply-side worries in Chile and, more recently, easing trade tensions. Cyclically, we believe copper prices are turning up – spurred by easy monetary conditions and fiscal stimulus directed at infrastructure and construction spending. Most of our key commodity-demand indicators have bottomed and are suggesting EM demand growth will move up. This supports a year-end base metal rally. Precious Metals: Neutral. A risk-on sentiment fueled by expectation the U.S. and China will sign a trade deal weighs on gold’s safe-haven demand. Prices fell 2% since last week. Additionally, U.S. 10-year bond yields shot higher – pushing gold prices lower – on Tuesday following a stronger-than-expect ISM services PMI data release. Gold-backed ETF holdings reached a new record in September at 2,855 MT (up 377 MT ytd), surpassing the December 2012 peak. A reversal in investors’ sentiment towards gold could send prices down. Ags/Softs: Underweight. The USDA reported that 52% of the U.S. corn has been harvested, a 13 percentage point increase relative to last week, yet the figure came shy of analysts’ expectation and far below the 2014-2018 average of 75%. On a weekly basis, corn prices are still down 2% due to drier weather forecast. Soybean harvest did better reaching 75%, and meeting expectations. Soybean price is almost unchanged on a weekly basis, despite having edged higher earlier in the week on the back of rising expectations the US and China will agree on a ceasefire in the ongoing trade war. Footnotes 1 We measure this uncertainty using the Baker-Bloom-Davis Global Economic Policy Uncertainty (GEPU) index. This is a GDP-weighted index of newspaper headlines containing a list of words related economic uncertainty. Newspapers from 20 countries representing almost 80% of global GDP are scoured for reports reflecting economic uncertainty. Please see our October 17 and October 31, 2019, reports Policy Uncertainty Lifts USD, Stifles Global Oil Demand Growth and Global Financial Conditions Support Higher Commodity Demand for the original research on this topic. Both are available at ces.bcaresearch.com. 2 We discuss deadweight losses to US households arising from the tariffs in Waiting To Get Long Copper, In China’s Steel Slipstream, published August 29, 2019. It is available at ces.bcaresearch.com. 3 BCA Research’s China Investment Strategy expects China’s business cycle likely will bottom in 1Q20 of next year, rather than in 4Q19. This aligns with our expectation. Please see China Macro And Market Review, published November 6, 2019. It is available at cis.bcaresearch.com. 4 We examined the implications of China’s “Blue Skies” policy in China's Anti-Pollution Resolve Critical To Iron Ore Markets, published April 4, 2019. It is available at ces.bcaresearch.com. 5 We discuss these issues in our Special Report entitled ضد الواسطة published November 16, 2018. The Arabic title of the report translates as "Against Wasta." Wasta means reciprocity in formal and informal dealings. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades TRADE RECOMMENDATION PERFORMANCE IN 2019 Q3

Iron Ore, Steel Prices Set To Lift

Iron Ore, Steel Prices Set To Lift

Commodity Prices and Plays Reference Table Trades Closed in 2019 Summary of Closed Trades

Iron Ore, Steel Prices Set To Lift

Iron Ore, Steel Prices Set To Lift

Highlights The global manufacturing cycle is likely to bottom soon, and consumption and services remain robust. The risk of recession over the next 12 months is low. This suggests that equities will continue to outperform bonds. But the risks to this optimistic scenario are rising. A denting of consumer confidence and worsening of geopolitical tensions could hurt risk assets. We hedge this by overweighting cash. China remains reluctant for now to use aggressive monetary easing. Until it does, the less cyclical U.S. equity market should outperform. We may shift into EM and European equities when China ramps up stimulus and the manufacturing cycle clearly bottoms. To hedge against this upside risk, we go tactically overweight Financials, and reiterate our overweight on Industrials and neutral on Australia. Bond yields should continue their rebound. We recommend an underweight on duration and favor TIPS. Credit should outperform on the cyclical horizon, but high corporate debt is a risk – we recommend a neutral position. Recommendations

Quarterly Portfolio Outlook: Hedges All Around

Quarterly Portfolio Outlook: Hedges All Around

Feature Overview Hedges All Around This is a particularly uncertain time for the global economy – and so a tricky one for asset allocators. Will manufacturing activity bottom soon, or will it drag down the services sector and consumption with it? Will bond yields continue their strong rebound? Is the Fed done cutting rates? Will China now ramp up monetary stimulus? Will Iran escalate a confrontation with Saudi Arabia? What will President Trump tweet about next? This is the sort of environment in which portfolio construction comes into its own. We have our view on all these questions, but our level of conviction is somewhat lower than usual. The way for investors to react is to plan asset allocation in such a way that a portfolio is robust in all the most probable scenarios. We expect the global manufacturing cycle to bottom soon. The Global Leading Economic Indicator is already picking up, and the Global PMI shows some signs of bottoming (Chart 1). The shortest-term lead indicator, the Citigroup Economic Surprise Index, has recently jumped in every region except Europe (Chart 2). (See also What Our Clients Are Asking on page 7 for some more esoteric indicators of cycle bottoms.) The bottoming-out is due to easier financial conditions over the past nine months, a stabilization in Chinese growth, and simply time – the down-leg in manufacturing cycles typically last 18 months, and this one peaked in H1 2018. Chart 1First Signs Of Bottoming

First Signs Of Bottoming

First Signs Of Bottoming

Chart 2Surprisingly Strong Surprises

Surprisingly Strong Surprises

Surprisingly Strong Surprises

At the same time, government bond yields should have further to rise. The Fed may cut rates once more but, given the resilient U.S. economy, no more than that. This is less than the 59 basis points of cuts over the next 12 months priced in by the Fed Fund futures. The recent pick-up in economic surprises suggests that the 10-year U.S. Treasury yield should return at least to where it was six months ago, 2.3-2.4% (Chart 3). This might be delayed, however, if there is an increase in political tensions, for example a break-up of the U.S./China trade talks (Chart 4). Chart 3Long-Term Rates To Rebound Further...

Long-Term Rates To Rebound Further...

Long-Term Rates To Rebound Further...

Chart 4...But Geopolitical Tensions Remain A Risk

...But Geopolitical Tensions Remain A Risk

...But Geopolitical Tensions Remain A Risk

This implies that equities are likely to continue to outperform bonds over the next few quarters, and so we remain overweight global equities and underweight global bonds on the 12-month investment horizon. However, the risks to this rosy scenario are rising. We remain concerned about the inverted yield curve, which has accurately forecast every recession since World War II, usually about 18 months in advance (Chart 5). The 3-month/10-year curve inverted in the middle of this year. We also worry that the weakness in the manufacturing sector may dent consumer confidence. There are some signs of this in Europe and Japan – but none significant yet in the U.S. (Chart 6). Accordingly last month, as a hedge against an economic downturn, we went overweight cash, which we see as a more attractive hedge, from a risk/reward point-of-view, than bonds. Chart 5Can We Ignore The Message From The Yield Curve?

Can We Ignore The Message From The Yield Curve?

Can We Ignore The Message From The Yield Curve?

Chart 6Some Signs Of Weaker Consumer Confidence

Some Signs Of Weaker Consumer Confidence

Some Signs Of Weaker Consumer Confidence

We also remain overweight U.S. equities, which are lower-beta and have fewer structural headwinds than equities in other regions. However, we continue to look for an entry point into the more cyclical equity markets which would also be beneficiaries of bolder China stimulus. China’s monetary easing remains more tepid than in previous stimulus episodes. It has probably been enough to stabilize domestic activity (Chart 7) but not to trigger a rally in industrial commodity prices, EM assets, and euro area equities, as it did in 2016. A pick-up in global PMIs and signs of stronger Chinese credit growth would clearly help EM and Europe (Chart 8) but we need higher conviction that these things are indeed happening before making that move. In the meantime, we are hedging the upside risk by raising the global Financials sector tactically to overweight, since it would likely do well if euro area stocks started to outperform. Earlier this year, we raised the Industrials sector to overweight and Australian equities to neutral, also to hedge against the upside risk from more aggressive Chinese stimulus. Chart 7Chinese Stimulus Has Merely Stabilized Growth

Chinese Stimulus Has Merelyy Stabilized Growth

Chinese Stimulus Has Merelyy Stabilized Growth

Chart 8Europe And EM Are The Most Cyclical Markets

Europe And EM Are The Most Cyclical Markets

Europe And EM Are The Most Cyclical Markets

Chart 9Oil Price Spikes Often Precede Recessions

Oil Price Spikes Often Precede Recessions

Oil Price Spikes Often Precede Recessions

The biggest geopolitical risk to our sanguine scenario is the situation in the Middle East, after the attacks on Saudi oil refineries. Every recession in the past 50 years has been preceded by a 100% year-on-year spike in the crude oil price (though note that Brent would need to rise to over $100 a barrel by year-end, from $61 today, for that to eventuate (Chart 9)). A short-term oil shortage is not the problem since strategic reserves are ample. But the attack demonstrates the vulnerability of the Saudi installations. And a reprisal attack on Iran could lead it to block the Strait of Hormuz, through which more than 20% of global oil passes. We have an overweight on the Energy sector, partly as a hedge against these risks. BCA’s oil strategists expected Brent crude to rise to $70 this year, and average $74 in 2020, even before the recent attack. They argue that the risk premium in the oil price (the residual in Chart 10) is too low, given not only tensions with Iran, but also other potential supply disruptions in Iraq, Libya, Venezuela and elsewhere. Chart 10Is The Oil Risk Premium Too Low?

Quarterly Portfolio Outlook: Hedges All Around

Quarterly Portfolio Outlook: Hedges All Around

Garry Evans, Senior Vice President Chief Global Asset Allocation Strategist garry@bcaresearch.com What Our Clients Are Asking Which Leading Indicators Should Investors Watch To Time The Rebound In Global Growth? Chart 11Positive Signals For Global Growth

Is Eurozone Manufacturing Close To A Bottom? Positive Signals For Global Growth

Is Eurozone Manufacturing Close To A Bottom? Positive Signals For Global Growth

During 2019, the global growth decline was a key driver of the bond rally and the outperformance of defensive assets. Thus, timing when this decline will reverse will be crucial, since it would also result in a change of leadership from defensive to cyclical assets. But how can this be done? Below we list three of our favorite indicators that have provided reliable leading signals on the global economy in the past: Carry-trade performance: The performance of EM currencies with very high carry versus the yen tends to be a leading indicator for global growth (Chart 11, panel 1). In general, carry trades distribute liquidity from countries where funds are plentiful but rates of return are low (like Japan), to places with savings shortfalls and high risk, but where prospective returns are high. Positive performance of these currencies tends to signal a positive shift in global liquidity, which usually fuels global growth. Swedish inventory cycle: The Swedish new-orders-to-inventories ratio is a leading indicator of the global manufacturing cycle (panel 2). Why? Sweden is a small open economy that is very sensitive to global growth dynamics. Moreover, Swedish exports are weighted towards intermediate goods, which sit early in the global supply chain. This makes the Swedish inventory cycle a good early barometer of the health of the global manufacturing cycle. G3 monetary trends: G3 excess money supply – measured as the difference between money supply growth and loan growth – is a leading indicator of global industrial production (panel 3). As base money and deposits become more plentiful in the banking system relative to the pool of existing loans, the liquidity position of commercial banks improves. This provides banks with the necessary fuel to generate more loan growth, a development which eventually provides a boon to economic activity. Importantly, all these leading indicators are sending a positive signal on the global economy. This confirms our view that rates should go up as global growth strengthens. Therefore, investors should remain overweight equities and underweight bonds in their portfolios. Is It Time To Buy Euro Area Banks? In a Special Report on euro area banks in December 2018, we noted that “Historically, when the relative P/B discount hits the lower band and the relative dividend yield hits the upper band, a rebound in relative return performance could be expected”.1 Our recommendation back then was that “long-term investors should avoid banks in the region, but investors with a more tactical mandate and much nimbler style could use the valuation indicators to ‘time’ their entry into and exit out of banks as a short-term trade.” Since then, banks have continued to underperform the overall market by over 10%, further pushing down relative valuation metrics. Currently, both relative P/B and relative dividend yield are at extreme levels that have historically heralded at least a short-term bounce. The euro area PMI is still below 50, but there are signs that the euro area economy could rebound later this year, which should be positive for banks’ relative earnings. Already, forward EPS growth has been stabilizing relative to the broad market (Chart 12, panel 4). In addition, two of the key concerns back in December 2018 were Italian government debt and the unwinding of QE. Now Italian debt is no longer in crisis and the ECB has relaunched QE. As such, investors with a tactical mandate and a nimble style should buy (overweight) banks in the euro area. Long-term investors should still avoid such a short-term trade because structural issues remain. Chart 12Tactically Upgrade Euro Area Banks

Tactically Upgrade Euro Area Banks

Tactically Upgrade Euro Area Banks

Is The Gold Rally Over? Spot gold prices have increased 17% year-to-date, on the back of global growth weakness, dovish central banks, and rising political tensions. Should investors now pare back their gold exposure? Common sense would suggest they should. However, these are not ordinary times. In the short term, gold prices might suffer from some profit-taking due to overbought technicals and excessively positive sentiment (Chart 13, panel 1). Moreover, gold prices have moved this year due to increased market expectations of central bank easing (panel 2). We expect that markets will be disappointed going forward by only limited rate cuts, which could put downward pressure on gold. On the other hand, with approximately 27%, or $14.9 trillion, of global debt with negative yields at the moment, investors will continue to shift to the next best asset – zero-yielding gold (panel 3). This is clear from the rise in holdings of gold over the past few years by both central banks and investors (panels 4 & 5). We expect this trend to persist as investors continue their search to avoid negative yields and focus on capital preservation. Geopolitical tensions have intensified since the beginning of the year: ongoing yet inconclusive trade negotiations between the U.S. and China, implementation of further tariffs, Brexit uncertainty, and the recent military attacks in the Middle East (panel 6). This environment should also continue to push gold prices higher. We continue to recommend gold as a hedge against inflation – which we see picking up over the next 12 months – as well as against any further deterioration in global growth and the geopolitical situation. Chart 13Gold: Sell Or Hold?

Gold: Sell Or Hold?

Gold: Sell Or Hold?

Risks to the rosy scenario are rising. We remain concerned about the inverted yield curve, which has accurately forecast every recession since World War II. How Low Can Rates Go? The zero lower bound is a thing of the past. Last month, Denmark’s central bank cut rates to -0.75%, and 10-year government bonds in Switzerland hit a historic low for any major country, -1.12%. In the next recession, how much further could interest rates theoretically fall? For individuals, cash rates might be limited by the cost of storing paper currency, which has a zero yield (unless governments find a way to ban cash or charge an annual fee on it). A bank safety deposit box costs about $300 a year, and a professional-quality safe big enough to store $1 million (which would be a pile of $100 bills 31 x 55 cms, weighing 10 kg) costs $2,000 with installation costs. Amortize the latter over 10 years, and the cost of storing $1 million is about 0.2%-0.3% a year. Swiss franc bills – maximum denomination CHF1,000 – would cost less to store. But storage costs for physical gold are around 2% a year. Since rates have fallen below this, there must be other constraints. Individuals would find storing money in cash possibly dangerous and certainly very inconvenient (imagine having to transport the cash to a bank to pay a tax bill). And the cost for a rich individual or company of storing, say, $1 billion (weighing 10 tonnes) would be much higher. Given the history in even low-rate countries (Chart 14, panel 1), we suspect around -1% is the level at which cashholders would seek alternatives to bank deposits of government bills. Chart 14How Low Can They Go?

How Low Can They Go?

How Low Can They Go?

Chart 15Yield Curves When Rates Are At Zero Or Below

Yield Curves When Rates Are At Zero Or Below

Yield Curves When Rates Are At Zero Or Below

At the long end, the yield curve does not typically invert much when short-term rates are zero or negative (Chart 15). The biggest 3-month/10-year inversion was in Switzerland earlier this year, -0.05%. This points then to the absolute lowest level for 10-year bonds anywhere, even in the middle of a nasty recession, at around -1.1%. That is a worry for asset allocators. It means that the maximum mathematical upside for Swiss government bonds from their current level (-0.8%) is 3% while it is 5% for German bonds (currently -0.5%). This is not much of a hedge. Only the U.S. looks better: if the 10-year Treasury yield falls to 0%, the total return is 18%. Global Economy Chart 16U.S. Growth Remains Solid

U.S. Growth Remains Solid

U.S. Growth Remains Solid

Overview: Industrial-sector growth globally has been weak, with the manufacturing PMI in most countries falling below 50. But consumption and services almost everywhere have remained resilient, even in the manufacturing-heavy euro area. And there are tentative signs of a bottoming-out in manufacturing. However, a full-scale rebound will depend on further monetary stimulus in China, where the authorities still seem cautious about rolling out easing on the scale of what was done in 2016. U.S.: U.S. manufacturing has now followed the rest of the world into contraction, with the ISM manufacturing index slipping below 50 in August (Chart 16, panel 2). However, consumption and services are holding up well. Employment continues to expand (albeit at a slightly slower pace than last year, perhaps because of a lack of jobseekers), there is no sign of a rise in layoffs, and consumer confidence remains close to a historical high (though it slipped slightly in September). Housing has recovered after last year’s slowdown, and the recent congressional budgetary agreement means fiscal policy will be mildly expansionary over the coming 12 months. Only capex (panel 5) has slowed, as companies postpone investment decisions due to uncertainty surrounding the trade war. The consensus expects U.S. real GDP growth of 2.2% this year, above most estimates of trend growth. Euro Area: Given its higher concentration in manufacturing, European growth is weaker than in the U.S. The manufacturing PMI has been below 50 since February, and fell further to 45.6 in August. Industrial production is shrinking by 2% year-on-year. Italy has experienced two negative quarters of growth, and Germany may also enter a technical recession in Q3 (GDP shrank by 0.1% in Q2). However, there are some tentative signs that manufacturing is bottoming: the ZEW survey in September, for example, surprised on the upside. And, like the U.S., consumption remains strong. Even in manufacturing-heavy Germany, employment continues to grow, and retail sales in July were up 4.4% year-on-year. In the U.K., however, uncertainty surrounding Brexit has damaged business investment, though employment has been strong.2 Chart 17First Signs Of A Rebound In The Rest Of The World?

First Signs Of A Rebound In The Rest Of The World?

First Signs Of A Rebound In The Rest Of The World?

Japan: Consumption has already slipped, even before the consumption tax hike scheduled in October. Retail sales in July fell 2% year-on-year, due to negative wage growth and consumer sentiment falling to a five-year low. Manufacturing continues to suffer from China’s slowdown and the strong yen (up 6% over the past 12 months), with exports falling 6% and industrial production down 2% year-on-year over the past three months. The effect of the consumption tax hike may be cushioned by government measures (lowering taxes on autos and making high-school education free, for example). And a pickup in Chinese growth would boost exports. But there are scant signs yet of a bottoming in activity. Emerging Markets: China’s growth appears to have stabilized, with both manufacturing and non-manufacturing PMIs above 50 (Chart 17, panel 3). But confidence remains fragile, with retail sales growth slowing to a 20-year low and car sales down 7% in August, despite the introduction of cars compliant with new emissions standards. The authorities have responded with further easing measures (including a further cut in the reserve requirement in September) but seem reluctant to launch a full-scale monetary stimulus, similar to what they did in 2016. Elsewhere in EM, growth has slowed in countries with structural issues (latest year-on-year real GDP growth in Argentina is -5.7%, in Turkey -1.5% and in Mexico -0.8%) but remains fairly resilient elsewhere (India 5%, Indonesia 5%, Poland 4.2%, Colombia 3.4%). Interest Rates: Central banks almost everywhere have turned dovish, with the Fed cutting rates for a second time, the ECB restarting asset purchases, and the Bank of Japan signaling it will ease in October. But further monetary accommodation will probably be less than the market expects. The Fed signaled that its cuts were just a mid-cycle correction and that further easing is unlikely. And the ECB and BoJ have little ammunition left. With signs of growth bottoming, and the market understanding that central banks’ dovish turn is reaching its end, long-term rates, which have already risen in the U.S. from 1.45% to 1.72% in September, are likely to move higher. Investors should also carefully watch U.S. inflation, which is showing signs of underlying strength, with core CPI inflation rising 2.4% year-on-year in August (and as much as 3.4% annualized over the past three months). Global Equities Chart 18Has Earnings Growth Bottomed?

Has Earnings Growth Bottomed?

Has Earnings Growth Bottomed?

Still Cautious, But Adding An Upside Hedge: Global equities registered a small loss of 8 basis points in Q3 (Chart 18) despite all the headline risks from geopolitics and weakening economic data. Overall, our defensive country allocation worked well in Q3, since DM equities outperformed EM by 4.5%, and the U.S. outperformed the euro area by 2.8%. Our sector positioning did not do as well since underweights in Utilities and Consumer Staples and overweights in Industrials, Energy and Health Care all went in the wrong direction, even though the underweight in Materials did help to offset the loss. During the quarter, however, both sector and country rotations were evident within the global equity universe, in line with the wild swings in bond yields. September saw some reversals in DM/EM, U.S./euro area and cyclical/defensives. Going forward, BCA’s House View remains that global economic growth will begin to recover over the coming months, albeit a little later than we previously expected. As such, our defensive country allocation remains appropriate. We did put euro area and EM equities on upgrade watch in April,3 but the delay in the global recovery also implies that it is still not the time to trigger this call. With our view that bond yields have hit bottom,4 we are making one adjustment in our global sector allocation by upgrading Financials to overweight from neutral. We are financing this by cutting in half the double overweight in Health Care to overweight (see next page for more details). This adjustment also acts as a hedge against two possible outcomes: 1) that the euro area outperforms the U.S., and 2) that Elizabeth Warren wins in the upcoming U.S. presidential election.5 Upgrade Global Financials To Overweight From Neutral Chart 19Upgrade Global Financials

Upgrade Global Financials

Upgrade Global Financials

The relative performance of global Financials to the overall equity market has been hugely affected by the movements in global bond yields (Chart 19, panel 1). As bond yields made a sharp reversal in September, so did the relative performance of Financials, even though it is barely evident on the chart given how much Financials have underperformed the broad market over recent years. It’s not clear how sustainable the sharp reversal in bond yields will be, but BCA’s House View is that bond yields will move higher over the next 9-12 months. As such, we are upgrading Financials to overweight from neutral, for the following additional reasons: Valuations are extremely attractive as shown in panel 2. More importantly, the relative valuation is now at an extreme level that historically heralded a bounce in Financials’ relative performance. Loan quality has improved. The U.S. non-performing loan (NPL) ratio is nearing the lows reached before the Global Financial Crisis (GFC). Even in Spain and Italy, NPL ratios have fallen significantly, though they remain higher than they were prior to the GFC (panel 3). U.S. consumption has been strong, housing has rebounded, and demand for loans is getting stronger (panel 4), in line with data such as the Citi Economic Surprise Index, suggesting that economic data may have hit bottom. To finance this upgrade, we cut the double overweight of Health Care to overweight, as a hedge against Elizabeth Warren winning next year’s U.S. presidential election and tightening rules on drug pricing. Government Bonds Maintain Slight Underweight On Duration. Our below-benchmark duration call was severely challenged by the global bond markets in the first two months of the third quarter. The U.S. 10-year Treasury yield hit 1.43% on September 3 in response to the weaker-than-expected ISM manufacturing index in the U.S., 57 bps lower than the level at the end of previous quarter, and just a touch higher than the historical low of 1.32% reached on July 6, 2016. The rebound in bond yields since September 5, however, was driven not only by the ebb and flow in the U.S./China trade policy dynamics, but also by the positive surprises in economic data releases, as shown in Chart 20. BCA’s Global Duration Indicator, constructed by our Global Fixed Income Strategy team using various leading economic indicators, is also pointing to higher yields globally going forward. Investors should maintain a slight underweight on duration over the next 9-12 months. Favor Linkers Vs. Nominal Bonds. Global inflation expectations have also rebounded after continuing their downtrend in the first two months of the quarter. This largely reflects the acceleration in August in realized inflation measures such as core CPI, core PCE, and average hourly earnings. In addition, historically, the change in the crude oil price tends to have a good correlation with inflation expectations. The oil price jumped initially by 20% following the attack on the Saudi Arabian oil production facilities. While it’s not clear how the geopolitical tensions will evolve in the Middle East, a conservative assumption of a flat oil price until the end of the year still points to much higher inflation expectations, supporting our preference for inflation-linked bonds over nominal bonds. We also favor linkers in Japan and Australia over their respective nominal bonds (Chart 21). Chart 20Bond Yields Have Hit Bottom

Bond Yields Have Hit Bottom

Bond Yields Have Hit Bottom

Chart 21Favor Inflation Linkers

Favor Linkers

Favor Linkers

We continue to look for an entry point into more cyclical markets which would benefit from a bolder Chinese stimulus. Corporate Bonds Since we turned cyclically overweight on credit within a fixed-income portfolio, investment-grade bonds and high-yield bonds have produced 220 and 73 basis points, respectively, of excess return over duration-matched government bonds. We remain bullish on the outlook for credit over the next 12 months, as we expect global growth to accelerate before the end of the year. Historically, improving global growth has resulted in sustained outperformance of credit over government bonds. Moreover, default rates should remain subdued over the next year given that lending standards continue to ease (Chart 22, panel 1). How long will we remain overweight credit? High levels of leverage, declining interest coverage ratios, and the high share of Baa-rated debt in the U.S. corporate debt market continue to make credit a risky proposition on a structural basis. However, with inflation expectations still very low, the Fed has a strong incentive to keep monetary policy easy. This dovish monetary policy should keep interest costs at bay, helping credit outperform over the next year. That said, we believe that there are some credit categories that are more attractive than others. Specifically, we recommend investors favor Baa-rated and high yield securities, given that there is still room for further credit compression in these credit buckets (panel 2 and panel 3). On the other hand, investors should stay away from the highest credit categories, as they no longer offer value (panel 4). Chart 22Baa-rated And High-Yield Credit Offer The Most Value

Baa-rated And High-Yield Credit Offer The Most Value

Baa-rated And High-Yield Credit Offer The Most Value

Commodities Chart 23No Supply Shock In The Oil Market

Quarterly Portfolio Outlook: Hedges All Around

Quarterly Portfolio Outlook: Hedges All Around

Energy (Overweight): September’s drone attack on Saudi crude facilities sent oil prices soaring as much as 20% in the days following, before falling back to pre-attack levels. Initial estimates estimated the supply disruption at 5.7 million barrels a day – approximately 5.5% of global supply – making it the largest crude supply outage in history. However, assuming the Saudis can return 70% of the lost output back online as they claim, OPEC’s spare capacity, approximately 1.8 million barrels a day, should be able to balance the market and cover the remaining lost production.6,7 In the longer-term, a pick-up in global oil demand, as economic growth rebounds, plus supply tightness should keep oil price elevated, with Brent reaching $70 this year and averaging $74 in 2020 (Chart 23, panels 1 & 2). Industrial Metals (Neutral): A combination of half-hearted year-to-date stimulus by Chinese authorities and a stronger USD in the second and third quarters of 2019 have driven industrial metals spot prices lower. However, the Chinese government announced additional stimulus in September, with further bond issuance to finance infrastructure projects and an easing of monetary policy (panel 3). This should give some upside for industrial metal prices over the coming six-to-12 months. Precious Metals (Neutral): We remain positive on gold, despite its strong performance year-to-date, since we see it as a good hedge against recession, inflation, and geopolitical risks. We discuss gold in detail in the What Our Clients Are Asking section on page 9. Silver also looks attractive in the short term. The nature of the use of silver has changed over the past two decades, from being mostly a base metal for industrial fabrication to becoming more of a precious metal viewed as a safe haven. The correlation between gold and silver prices has increased since the Global Financial Crisis from an average of 0.5 pre-crisis to 0.8 post-crisis (panels 4 & 5). Global growth and political uncertainty should support silver prices in the coming months. Currencies U.S. Dollar: The trade-weighted dollar has appreciated by 2.5% since we turned neutral in April. We expect that the steep drop in yields will continue to ease financial conditions and help global growth in the last quarter of the year. Given that the dollar is a counter-cyclical currency, an environment where global growth rallies have historically been negative for the greenback. Euro: Since we turned bullish in April, EUR/USD has depreciated by 2.7%. Overall, we continue to be positive on EUR/USD on a cyclical timeframe. After the ECB cut rates by 10 basis points and announced further rounds of quantitative easing, there is not much room left for the euro area to keep easing relative to the U.S. (Chart 24, panel 1). Moreover, improving expectations of profit growth in the euro area vis-à-vis the U.S. will drive money flows towards Europe, pushing EUR/USD up in the process (panel 2). Emerging Market Currencies: We remain bearish on emerging market currencies for the time being. That being said, they remain on upgrade watch for the end of the year. There are multiple signs that global growth is turning up, a consequence of the easy financial conditions caused by some of the lowest bond yields on record. Moreover, the marginal propensity to spend (proxied by M1 growth relative to M2 growth) in China, the main engine of EM growth, continues to point to further appreciation in emerging market currencies (panel 3). Chart 24Interest Rate And Profit Expectation Differentials Favor The Euro

The Euro Might Soon Pop Interest Rate And Profit Expectations Differentials Favor The Euro

The Euro Might Soon Pop Interest Rate And Profit Expectations Differentials Favor The Euro

Alternatives Chart 25Favor Hedge Funds Untill Global Growth Bottoms

Favor Hedge Funds Untill Global Growth Bottoms

Favor Hedge Funds Untill Global Growth Bottoms

Return Enhancers: Over the past 12 months, we have recommended investors pare back on private equity and increase allocations to hedge funds – macro hedge funds in particular. This was due to our judgement that we are late in the economic cycle. While we expect growth to pick up over the coming months, this is not yet clear in the data (Chart 25, panel 1). This uncertain macro outlook will prove tough for private equity funds, especially given an environment of rising multiples and increasing competition for deals. We continue to see global macro hedge funds as the best hedge ahead of the next recession and would advise investors to allocate funds now, given the time it takes to move allocations in the illiquid space. Inflation Hedges: In the current environment, TIPS are likely a better inflation hedge than illiquid alternative assets. Our May 2019 Special Report 8 showed that TIPS produce a particularly attractive risk-adjusted return during times when inflation is rising, but still fairly low (below 2.3%). TIPS should do well, therefore, in the environment we expect over the next few months, where the Fed remains dovish, cutting rates perhaps once more, while condoning a moderate acceleration of inflation (panel 2). Volatility Dampeners: Structured products – mostly Mortgage-Backed Securities (MBS) – have had an excellent record of reducing portfolio volatility (panel 3). Despite that, we do not recommend more than a neutral allocation to MBS currently due to a less-than-attractive valuation picture. Despite Treasury yields falling by more than 100 basis points this year and refinancing activity picking up, nominal MBS spreads remained near their all-time lows. However, as Treasury yields bottom, we expect refinancing to slow, putting downward pressure on spreads. Risks To Our View The most likely upside risk comes from the Fed being too dovish and falling behind the curve. Underlying inflation pressures in the U.S. remain strong (with core CPI up 3.4% annualized over the past three months). After two rate cuts, the Fed Funds rate is now comfortably below the neutral rate: 0.1% in real terms compared to a Laubach-Williams r* of 0.8% (Chart 26). Tightness in the money markets have pushed the Fed to start expanding its balance sheet again. If manufacturing growth accelerates next year, and wages and profits begin to rise, a stock market melt-up, similar to that in 1999, would be possible. Eventually, though, the Fed would need to raise rates (perhaps sharply) to kill inflation, which could usher in the next recession. There are a broader range of possible downside risks. As argued throughout this Quarterly, there are various possible triggers of recession: failure of China to stimulate, and a loss of confidence by consumers, in particular. Some models of recession put the risk over the next 12 months as high as 30% (Chart 27). Structurally, the biggest risk is probably the high level of corporate debt in the U.S. (Chart 28). A breakdown in the junk bond market, as seen briefly last December, could lead to companies failing to refinance the large amount of debt maturing over the next 18 months. Geopolitical risks also remain elevated and are, by nature, hard to forecast. The outcome of Brexit remains highly uncertain – though we see low risk of a no-deal exit. We expect trade talks between the U.S. and China to drag on, without a comprehensive deal, while a clear breakdown would be negative. Impeachment of President Trump is probably not a significant market event, but might hurt market sentiment briefly (particularly if it makes the election of Elizabeth Warren more likely). The Iran/Saudi conflict could escalate. Risk premiums may need to rise to take into account these threats. Chart 26Is The Fed Turning Too Dovish?

Is The Fed Turning Too Dovish?

Is The Fed Turning Too Dovish?

Chart 27What Risk Of Recession?

What Risk Of Recession?

What Risk Of Recession?

Chart 28Is Corporate Debt The Biggest Risk?

Is Corporate Debt The Biggest Risk?

Is Corporate Debt The Biggest Risk?

Footnotes 1Please see Global Asset Allocation Special Report, titled "Euro Area Banks: Value Play Or Value Trap?" dated December 14, 2018, available at gaa.bcaresearch.com. 2 Please see Foreign Exchange Strategy Special Report, “United Kingdom: Cyclical Slowdown Or Structural Malaise?”, dated 20 September 2019, available at fes.bcaresearch.com. 3Please see Global Asset Allocation Quarterly, titled "Quarterly - April 2019" dated April 1, 2019, available at gaa.bcaresearch.com. 4Please see Global Investment Strategy Weekly Report, titled "Bond Yields Have Hit Bottom," dated September 6, 2019, available at gis.bcaresearch.com. 5Please see Global Investment Strategy Weekly Report, titled "Elizabeth Warren And The Markets," dated September 13, 2019, available at gis.bcaresearch.com. 6Dmitry Zhdannikov and Alex Lawler “Exclusive: Saudi oil output to return faster than first thought - sources,” Reuters, dated Sepetmber 17, 2019. 7Please see Geopolitical Strategy Special Alert titled, “Attacks On Critical Infrastructure In KSA Raises Questions About U.S. Response,” dated September 16, 2019, available at gps.bcaresearch.com. 8Please see Global Asset Allocation Special Report, titled “Investors’ Guide To Inflation Hedging: How To Invest When Inflation Rises,” dated May 22, 2019, available at gaa.bcaresearch.com GAA Asset Allocation

Commodity demand appears to be turning up, based on our assessment of global industrial activity. As demand picks up, we expect industrial commodity prices will move higher (Chart of the Week, top panel). For all practical purposes, central banks and numerous governments have moved into recession-fighting mode, following the contraction in manufacturing activity brought on by the U.S. Fed’s rates-normalization policy last year, and China’s deleveraging campaign in 2017-18. Together, these policies severely retarded credit and liquidity available to markets, and drove the USD higher, to the detriment of commodity demand (Chart of the Week, middle panel). Current policy responses will support a revival of manufacturing, and with it, global trade (Chart of the Week, bottom panel). While we continue to expect a weaker USD on the back of additional Fed easing this year and recovery of ex-U.S. economic growth in line with our House view, we remain wary uncoordinated global monetary accommodation by a large number of central banks could leave the dollar well bid. This could stifle the commodity-demand revival by keeping local-currency commodity costs high (Chart 2). This would be especially bearish for base metals prices.1 Chart of the WeekGlobal Industrial Activity Moving Higher

Global Industrial Activity Moving Higher

Global Industrial Activity Moving Higher

Chart 2USD Strength Will Pose Risk To Industrial Commodity Demand

USD Strength Will Pose Risk To Industrial Commodity Demand

USD Strength Will Pose Risk To Industrial Commodity Demand

Highlights Energy: Overweight. The appointment of Prince Abdulaziz bin Salman as the Kingdom of Saudi Arabia’s (KSA) new Energy Minister signals the royal family will push harder to manage production and reduce global oil inventories ahead of the IPO of Saudi Aramco. The prince brings more than 30 years of experience to the role, making him something of an outlier among KSA’s ministers – technocrats typically have occupied the position, and he is the first royal to serve as Energy Minister. We believe the prince’s immediate goal is to get Brent into the mid- to high-$70/bbl ahead of the IPO later this year or early next year. The first leg of the IPO reportedly will be done locally in the Kingdom, with Saudi investors taking ~ 1% of the Saudi Aramco float. Base Metals: Neutral. China imported 1.82mm MT of copper concentrates in August, a 9.3% increase y/y, as smelters continue to buy partly processed ores to feed expanding capacity. Concentrate imports in July were a record 2.07mm MT. Precious Metals: Neutral. The World Platinum Investment Council (WPIC) forecasts a 9% increase in platinum demand this year, driven primarily by ETF investors. This “more than offsets expected demand decreases in the automotive and jewellery segments of 4% and 5% respectively.” WPIC reduced its expected physical surplus this year to 345k ounces, from its earlier expectation of 375k ounces. Our tactical long platinum position recommended August 29, 2019 is up 1.9%. Separately, we are taking profits on our Long 10-year TIPS position at tonight’s close. It was up 9.3% on September 10, 2019. The position was recommended July, 27, 2017. Ags/Softs: Underweight. A wet start to the planting season points to lower corn and bean yields this year vs. 2018. AccuWeather expects 2019 corn yields will fall 7.35% y/y to 13.36 billion bushels, and soybean yields will be down 19.5% y/y to 3.658 billion bushels. Besides stressing crops at the beginning of the season, weather-related delays also increase the risk some of this year’s crop will be exposed to frost at the end of the season before it is harvested. Weather effects continue to be apparent in the USDA’s crop conditions report, particularly for corn, where the USDA now rates 55% of the U.S. crop good or excellent, vs. 68% a year earlier. Last week, the USDA rated 58% of the corn crop good or excellent. Feature Leading indicators are signaling the slowdown in global growth – i.e., aggregate-demand growth – likely bottomed ex-Europe (Chart 3). The chart shows easing global financial conditions, along with fiscal stimulus, most likely have arrested the slowdown in industrial commodity demand (Chart 4). Chart 3Manufacturing Downturn Likely Arrested Following Broad Monetary Stimulus

Manufacturing Downturn Likely Arrested Following Broad Monetary Stimulus

Manufacturing Downturn Likely Arrested Following Broad Monetary Stimulus

Chart 4Global Financial Conditions Are Supportive Easier Financial Conditions Will Benefit Global Growth

Global Financial Conditions Are Supportive Easier Financial Conditions Will Benefit Global Growth

Global Financial Conditions Are Supportive Easier Financial Conditions Will Benefit Global Growth

We expect the recovery in demand will be most visible in the LMEX base metals index and in oil markets. Base metals demand is highly concentrated in China – accounting for ~ 50% of global demand – and EM Asia. Our EM Commodity-Demand Nowcast continues to signal oil demand also will revive in 2H19 as GDP growth picks up (Chart 5). Markets still could wobble, which is why the evolution of EM import volumes remains important, given their high correlation with GDP levels. A number of gauges we follow closely – particularly those associated with the movement of good on the sea (Chart 6) and in the air (Chart 7) – have turned up in 3Q19. We expect this to continue into 4Q19 and next year. Chart 5Monetary, Fiscal Stimulus Will Lift Oil Demand

Monetary, Fiscal Stimulus Will Lift Oil Demand

Monetary, Fiscal Stimulus Will Lift Oil Demand

Chart 6Shipping Gauges Signal Uptick in Movement of Goods

Shipping Gauges Signal Uptick in Movement of Goods

Shipping Gauges Signal Uptick in Movement of Goods

Chart 7Air Freight Gauges Signal Uptick in Movement of Goods

Air Freight Gauges Signal Uptick in Movement of Goods

Air Freight Gauges Signal Uptick in Movement of Goods

USD Strength Keeps Us Wary The contraction in manufacturing and EM trade volumes is largely the result of the Fed’s rates-normalization policy last year, and China’s deleveraging campaign in 2017-18, in our view. These policies raised the value of the USD, which raised local-currency costs of dollar-denominated commodities, and all other goods and services invoiced and funded with dollars (Chart 8). Indeed, as Chart 2 shows, oil prices and base metals prices in local-currency terms ex-U.S. are closer to their earlier highs when Brent was trading above $100/bbl. This redounded to the detriment of commodity demand.2 The Sino-U.S. trade war certainly does not help commodity demand. For the most part, however, we believe this affects demand expectations – i.e., capex- and investment-driven demand. We believe firms and households will reduce outlays and increase precautionary savings, as a buffer against an expansion of the trade war into a larger global conflict, which likely would impair global supply chains and growth prospects. Chart 8Strong USD Keeps Us Wary

Strong USD Keeps Us Wary

Strong USD Keeps Us Wary

While we expect the USD to weaken as the Fed cuts its policy rate, in line with our House view, we reiterate the non-trivial risk that global monetary accommodation still could leave the dollar well bid.3 Rising negative yielding debts globally makes U.S. yields relatively attractive despite the ongoing easing, supporting capital inflows in U.S. fixed income markets. Investment Implications The coincidence of fiscal and monetary policy easing is showing up in our gauges of global economic activity and in our leading indicators. We remain long oil exposure and precious metals – gold on a strategic basis, silver and platinum on a tactical basis. As we see industrial commodity demand picking up, we will look to go long copper. Bottom Line: Our gauges of economic activity continue to point to a bottoming of the global ex-U.S. slowdown in industrial activity, particularly in manufacturing, which has been hard-hit by a downturn in auto output. We expect USD weakness to become a tailwind for industrial commodities; however, we are wary continued strength in the dollar – it is above its 1Q02 peak – could crimp industrial metals, and maybe even oil, prices (Chart 9). Chart 9USD TWIB Strength Hampers Industrial Commodity Demand

USD TWIB Strength Hampers Industrial Commodity Demand

USD TWIB Strength Hampers Industrial Commodity Demand

Robert P. Ryan, Chief Commodity & Energy Strategist rryan@bcaresearch.com Footnotes 1 We use base metals demand, particularly for copper, as an indicator of EM industrial activity in our modeling. These markets are somewhat removed from the idiosyncratic forces driving oil supply-demand dynamics, particularly on the supply side, where OPEC 2.0 continues to maintain its policy of production discipline to reduce global inventory levels. OPEC 2.0 is the name we coined for the producer coalition lead by KSA and Russia, which was formed in 2016 with the explicit mission of reducing the global oil-inventory overhang resulting from the 2014-15 market share war launched by the original OPEC states in 2H14. 2 Last week we discussed USD strength vis-à-vis oil demand. Please see Central Bank Easing Key To Oil Prices. It is available at ces.bcaresearch.com. 3 A non-trivial risk is bounded at the lower end by Russian-roulette odds – i.e., 1:6 – in our usage of the phrase. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades TRADE RECOMMENDATION PERFORMANCE IN 2019 Q2

Industrial Commodity Demand Recovery Will Boost Metals, Oil

Industrial Commodity Demand Recovery Will Boost Metals, Oil

Commodity Prices and Plays Reference Table Trades Closed in 2019 Summary of Closed Trades

Industrial Commodity Demand Recovery Will Boost Metals, Oil

Industrial Commodity Demand Recovery Will Boost Metals, Oil

Prices for iron ore and steel have come back to earth, following their impressive rallies this year. However, copper prices languished, and retreated to $2.50/lb on the COMEX. This, despite a contraction of physical copper concentrates supply, which kept…

Away from the Sino-U.S. trade-war headlines – and the remarkable commodity price volatility they produce – apparent steel consumption in China is up 9.5% y/y in the first seven months of this year. This is being spurred by fiscal stimulus directed at infrastructure and construction spending, which remains strong relative to year-ago levels (Chart of the Week).1 Demand for copper normally drafts in the wake of China’s steel demand, and picks up when steel-intensive capital projects are being wired for use. In less uncertain times, getting long copper would make sense.2 Chart of the WeekFiscal Stimulus Boosts China Steel Consumption

Fiscal Stimulus Boosts China Steel Consumption

Fiscal Stimulus Boosts China Steel Consumption

We are holding off getting long for now, given the policy uncertainty – particularly in re trade policy – that dominates commodity markets, none moreso than steel and base metals. While the odds of a resolution to the trade war might be edging up from our 40% expectation, moving them closer to those of a coin toss does not justify taking the risk.3 Highlights Energy: Overweight. Retaliatory tariffs on $75 billion of U.S. imports, including crude oil, into China, provoked an additional 5% duty by President Trump on ~ $550 billion of goods shipped to the U.S. by China. This will lift the total tariff on $250 billion of U.S. imports from China to 30%, and on another $300 billion to 15%, starting Oct. 1 and Sept. 1. Following the imposition of Chinese tariffs, China Petroleum & Chemical Corp, or Sinopec, petitioned Beijing for waivers on U.S. crude imports. Base Metals: Neutral. Included in the latest Chinese tit-for-tat tariff retaliations is a 5% tariff increase on copper scrap imports from the U.S., which takes the duty to 30%; the re-imposition of 25% tariffs on U.S. auto imports, and a 5% tariff on auto parts. The latter tariffs go into effect December 15, according to Fastmarkets MB. Precious Metals: Neutral. We are getting long platinum at tonight’s close, but with a tight stop of -10%, given highly volatile – and uncertain – trading markets. In addition to following the wake of safe-haven demand for gold, a physical deficit for platinum is possible.4 Markets have been well supported technically – bouncing off long-term support of ~ $785/oz dating to the depths of the Global Financial Crisis in 2008 – 09. Ags/Softs: Underweight. The USDA reported 57% of the U.S. corn crop is in good or excellent condition this week, vs. 68% a year ago. The Department also reported 55% of the soybean crop was in good or excellent shape vs. 66% last year at this time. Feature Iron ore price surged more than 38.1% y/y, while steel prices rallied in 1Q19 off their year-end 2018 lows, helped by the Central Committee fiscal stimulus directed at infrastructure and construction, which hit the market after the collapse of Vale’s Brumadinho dam in January (Chart 2). The combination of the fatal dam disaster and fiscal stimulus in China lifted prices for iron ore and steel sharply.5 Chart 2Iron Ore and Steel Rally Leaves Copper Behind

Iron Ore and Steel Rally Leaves Copper Behind

Iron Ore and Steel Rally Leaves Copper Behind

Chart 3China's Construction, Real Estate Investment Spur Higher Steel Demand

China's Construction, Real Estate Investment Spur Higher Steel Demand

China's Construction, Real Estate Investment Spur Higher Steel Demand

While policymakers guide domestic markets to expect reduced stimulus for the real-estate sector, we continue to expect copper demand to pick up in the short term. Our modeling indicates strong steel consumption presages higher copper consumption, especially when construction’s contribution is high (Chart 3). This is because the projects accounting for that consumption typically are fitted out with electrical wiring six months or so after the structures built with all that steel are made ready for residential or commercial use (Chart 4).6 This should support copper prices as we go through 2H19, although a slowdown in steel’s apparent consumption in 1Q19 followed by a rebound in April could make for a bumpy ride. CPC Central Committee guidance is stressing the need to get stimulus to the “real economy, such as privately-owned manufacturers and high-tech firms, which are the engines of long-term growth.”7 Still, while policymakers guide domestic markets to expect reduced stimulus for the real-estate sector, we continue to expect copper demand to pick up in the short term, as completed construction and infrastructure and projects in the pipeline from past stimulus are made ready for use.8 Chart 4Higher Steel Demand Normally Presages Higher Copper Demand

Higher Steel Demand Normally Presages Higher Copper Demand

Higher Steel Demand Normally Presages Higher Copper Demand

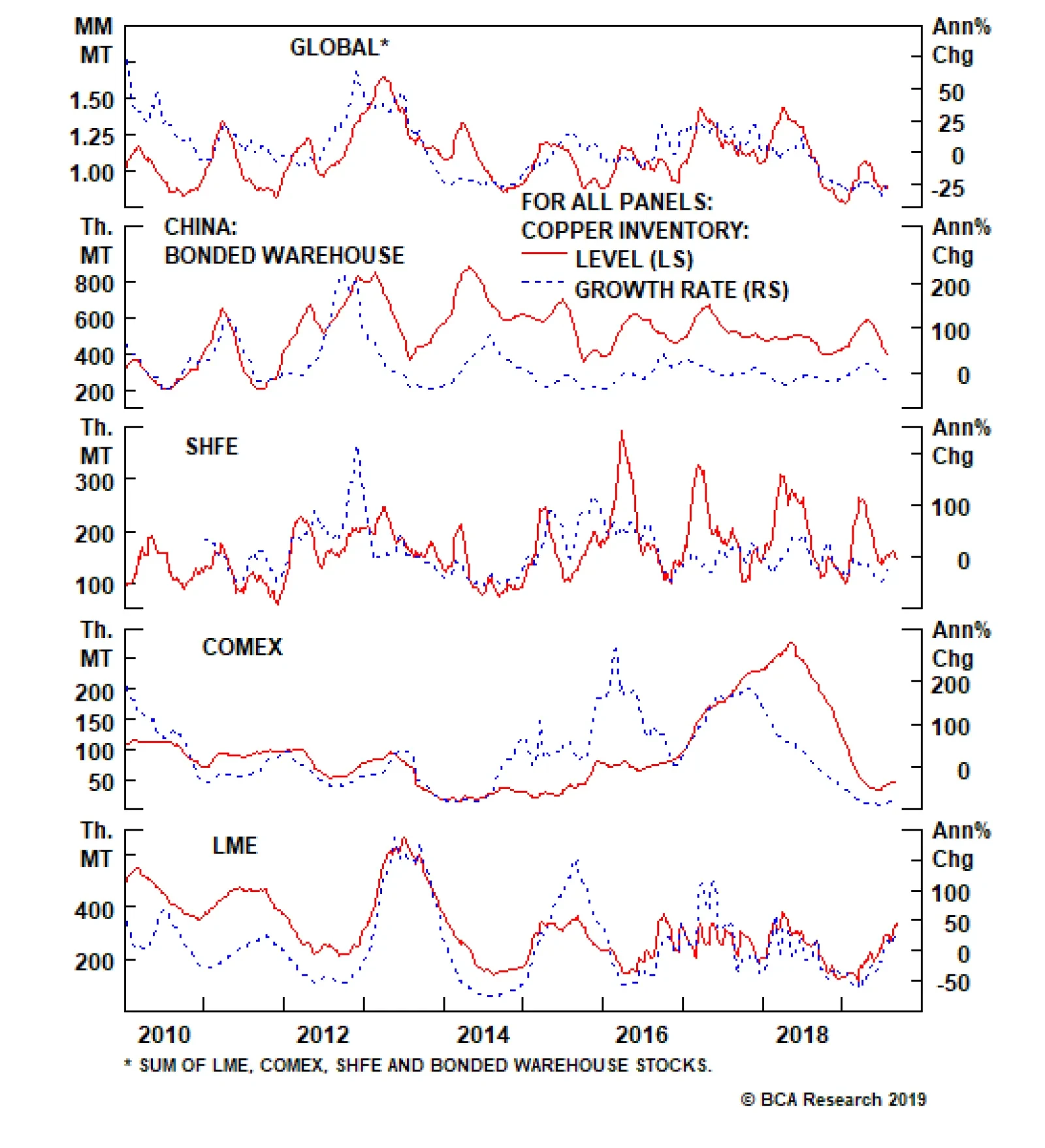

Copper Puzzle: Why Was It Left Behind? Part of the explanation for copper’s lackluster relative performance likely is USD-related: A strong dollar will reduce demand. Prices for iron ore and steel have come back to earth, following their impressive rallies this year. However, as Chart 2 illustrates, copper prices languished, and retreated to $2.50/lb on the COMEX. This, despite a contraction of physical copper concentrates supply, which kept copper treatment and refining charges (TC/RC) close to record lows, and inventories tight globally (Chart 5).9 Part of the explanation for copper’s lackluster relative performance likely is USD-related: A strong dollar will reduce demand (Chart 6).10 Our House view continues to expect the U.S. Fed to deliver a 25bp rate cut at its mid-September meeting. This could be followed by additional easing if Sino-U.S. trade tensions persist or get worse. Our House view expects Fed easing and a recovery in EM GDP growth will weaken the USD later this year. As iron ore shipments pick up from Brazil and Australia, we would expect pressure on those prices as the additional supply arrives at Chinese docks, and residential construction wanes (Chart 7). This should, in relative terms, mean copper outperforms iron ore, all else equal, since copper supplies and inventories are contracting. And, as construction spending moderates and winter restrictions on steel mills go into effect, we would expect copper to outperform steel. Chart 5Global Copper Inventories Remain Tight

Global Copper Inventories Remain Tight

Global Copper Inventories Remain Tight

Chart 6Strong USD Restrains Base Metal Demand

Strong USD Restrains Base Metal Demand

Strong USD Restrains Base Metal Demand

Chart 7China's Iron Ore Imports Remain Strong

China's Iron Ore Imports Remain Strong

China's Iron Ore Imports Remain Strong

Lastly, we would note from a technical perspective that copper has been – and remains – oversold (Chart 8). This could reflect the fact that, among base metals, it has the deepest liquidity, so that when hedgers or speculators are looking for a way to hedge trade-war risk vis-à-vis China – or to simply take a view on EM GDP prospects – copper is the preferred vehicle. It still is too early to wade into buying based on technicals, and, historically, copper has dipped further into oversold territory than where it now sits. But continued excursions into oversold territory will get our attention, and incline us to revisit our bullish bias. Chart 8Technically, Copper's Oversold

Technically, Copper's Oversold

Technically, Copper's Oversold

Trade War Deadweight The foregoing analysis suggests copper is due to rally. That is our expectation, at any rate. But uncertainty re the Sino-U.S. trade war and other exogenous policy issues – chiefly increasing recession risks arising from higher tariffs on Chinese imports to the U.S., a possible oil-price spike driven by military action in the Persian Gulf, and a disorderly Brexit – forces us to stand aside. Back in May, the N.Y. Fed conducted an analysis of U.S. President Donald Trump’s increase in tariff rates on $200 billion of Chinese imports from 10% to 25%.11 The N.Y. Fed estimated this increase in the tariff rates on that $200 billion would cost the average American household $831/yr, owing to a sharp increase in the deadweight loss arising from the increase. The deadweight loss estimated by the bank arising from tariff increase on the $200 billion of goods subject to the duty went from $132/household/year to $620/household/year. This means the total cost of the tariffs on the $200 billion of goods went from $414/household/year to $831/household/year. The N.Y. Fed notes: Economic theory tells us that deadweight losses tend to rise more than proportionally as tariffs rise because importers are induced to shift to ever more expensive sources of supply as the tariffs rise. Very high tariff rates can thereby cause tariff revenue to fall as buyers of imports stop purchasing imports from a targeted country and seek out imports from (less efficient) producers in other countries. The deadweight loss that comes from importers being forced to buy tariffed goods from higher-cost suppliers is, in other words, highly non-linear. This latest round of tariff increases is being levied on $550 billion of imports come September 1 and October 1. According to the Urban-Brookings Tax Policy Center, a Washington-based research joint-venture between the Urban Institute and the Brookings Institute, U.S. middle-class households earning $50k to $85k, received an average income tax cut of about $800 last year following passage of the 2017 Tax Cuts and Jobs Act (TCJA), which was signed in to law by President Trump December 22, 2017.12 Further increasing tariffs, as proposed, means the after-tax income of average U.S. households will contract, as the total cost of tariffs overwhelms the value of TCJA tax cuts for middle-income households, if they are imposed as scheduled. China's economy is struggling under the strain of the trade war, as it overlaps with President Xi’s reform and deleveraging campaign of 2017-18. While these campaigns have been postponed, the lingering effects are weighing on growth. In addition, banks and corporations appear to be backing away from taking on new risks. The state’s reflationary measures, including a big boost to local government spending, have so far been merely sufficient for domestic stability.12 Bottom Line: Fundamentals and technicals align to support copper prices. However, given the uncertainty surrounding the evolution of the Sino-U.S. trade war we are staying on the sidelines, and avoiding putting on a long position at present. Rising tariffs by the U.S. and China increases the risk of recession in both countries. Robert P. Ryan, Chief Commodity & Energy Strategist rryan@bcaresearch.com Footnotes 1 In Copper Will Benefit Most From Chinese Stimulus, published April 25, 2019, we noted China would deploy $300 billion (~ 2 trillion RMB) to support policymakers’ GDP growth targets this year. See also the June 2019 issue of Resources and Energy Quarterly, published by the Australian Government’s Department of Industry, Innovation and Science, particularly Section 3 beginning on p. 22. 2 We are referring to Knightian uncertainty here, a distinction developed by economist Frank Knight in his 1921 book "Risk, Uncertainty and Profit". Uncertainty in Knight’s sense refers to a risk that is “not susceptible to measurement,” per the MIT.edu reference above. This differs from the “risk” we routinely consider in this publication, which can be measured via implied volatilities in options markets. A pdf of the book can be downloaded at the St. Louis Fed’s FRASER website. 3 These odds were calculated by BCA Research’s Geopolitical Strategy group. For a discussion, please see our article entitled Expanded Sino – U.S. Trade War Could Be Bullish For Base Metals, published May 9, 2019. It is available at ces.bcaresearch.com. 4 This is not a certainty. In its PGM Market Report for May 2019, Johnson Matthey, the platinum-group metals refiner, forecast a slight physical platinum deficit this year of ~ 4MT, while Metals Focus expects a 20MT surplus. 5 The Australian Government DIIS report footnoted above (fn 1) states, “Production growth in China was driven by stimulatory government spending, which focused on higher infrastructure investment and boosting construction activity.” This is consistent with our framework for analyzing Chinese bulks (iron ore and steel) and base metals markets: Steel production and consumption are directed by the Communist Party of China (CPC) Central Committee, which motivates us to treat China’s steel market as a unified vertically integrated industry. Chinese steel production, accounts for ~ 50% of the global total. Its strong showing this year pushed world steel production up ~ 5% y/y in the first five months of this year, according to the DIIS. 6 In our modeling of copper prices, we lag steel apparent consumption by six months. 7 Please see Property sector cooling to help real economy funding, published by China Daily on August 1, 2019. 8 BCA Research’s China Investment Strategy noted, “The July Politburo statement signaled a greater willingness to stimulate the economy; as a result, we are penciling in a slightly more optimistic scenario on forthcoming credit growth through the remainder of the year, by adding 300 billion yuan of debt-to-bond swaps and 800 billion yuan of extra infrastructure spending to our baseline estimate for the rest of 2019. However, this would only add a credit impulse equivalent of 1 percentage point of nominal GDP and would only marginally reduce the probability of an earnings recession to 40%.” Please see Don’t Bottom-Fish Chinese Assets (Yet), published August 14, 2019. It is available at cis.bcaresearch.com. 9 The International Copper Study Group reported world mine production fell ~ 1% in the January – May 2019 period to ~ 8.3mm MT. Global refined copper production also was down ~ 1% to 9.8mm MT, while refined copper usage was down less than 1% over the same period. China’s refined usage – ~ 50% of world demand – was up 3.5%. 10 Our modeling indicates a 1% y/y increase in the broad trade-weighted USD translates into a 0.7% y/y decrease in the price of copper. Iron ore also is affected by USD levels, but price formation in this market is dominated by the overwhelming influence of Chinese demand on the seaborne iron-ore market, which accounts for close to 70% of global demand. For steel, China accounts for slightly more than half of global supply and demand, which somewhat insulates it from USD effects. 11 Please see New China Tariffs Increase Costs to U.S. Households, published by the N.Y. Fed May 23, 2019. 12 Please see Big Trouble In Greater China, a Special Report published by BCA Research's Geopolitical and China Investment strategies August 23, 2019. It is available at gps.bcaresearch.com. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades TRADE RECOMMENDATION PERFORMANCE IN 2019 Q2

Image

Commodity Prices and Plays Reference Table Trades Closed in 2019 Summary of Closed Trades

Image

Chart II-1Is Deflation In Steel And Coal Back?

Is Deflation In Steel And Coal Back?

Is Deflation In Steel And Coal Back?