BCA Indicators/Model

MacroQuant recommends a slight underweight position in equities, and favors a below-benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, neutral on gold, constructive on copper, and very bullish on oil.

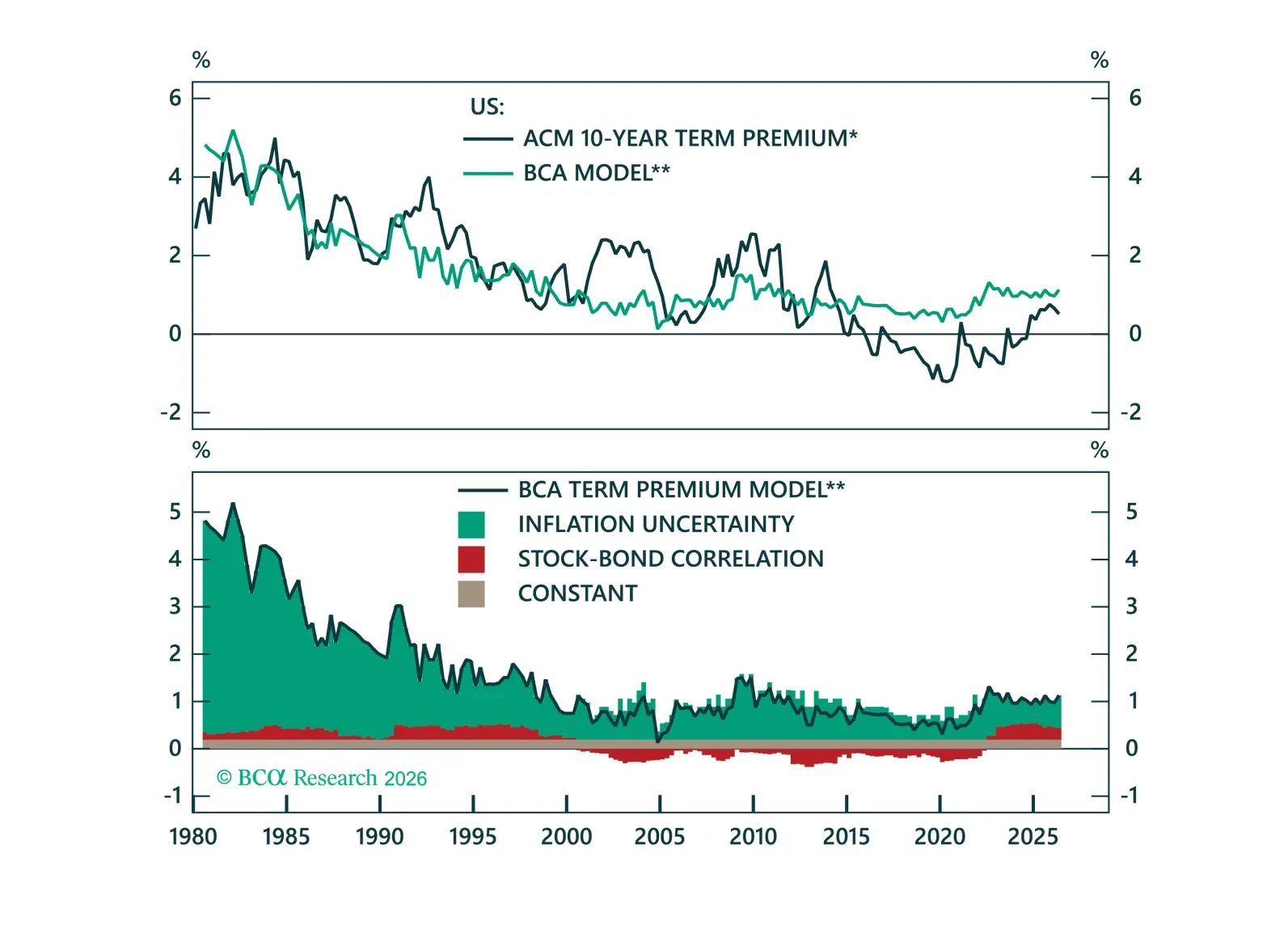

Rising term premium is often read as a fiscal warning sign. We show the real driver is monetary policy uncertainty, and what the implications are for global term premia going forward.

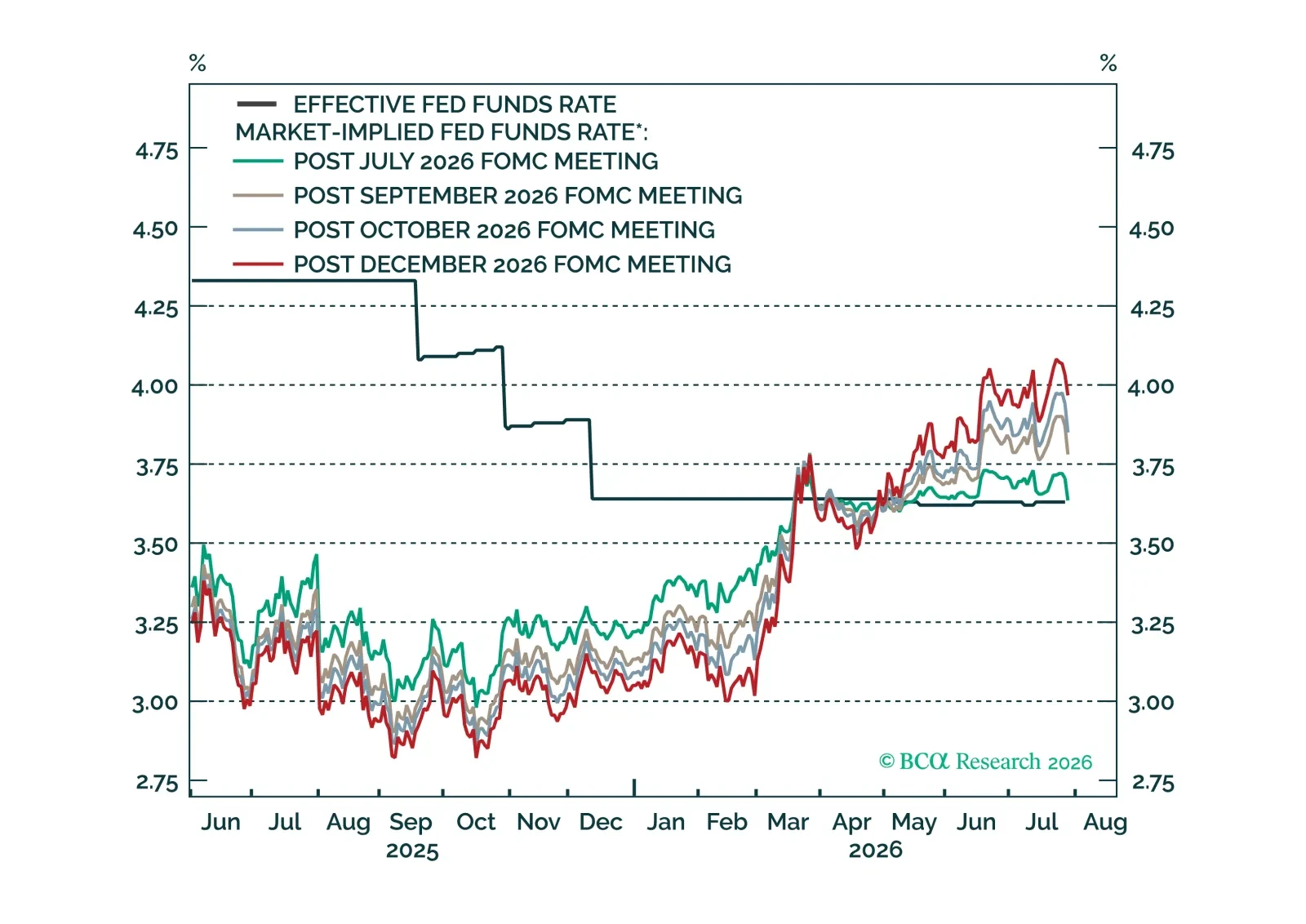

Despite today’s hold, the bar for a rate hike in September remains low and contingent on the next two core CPI reports.

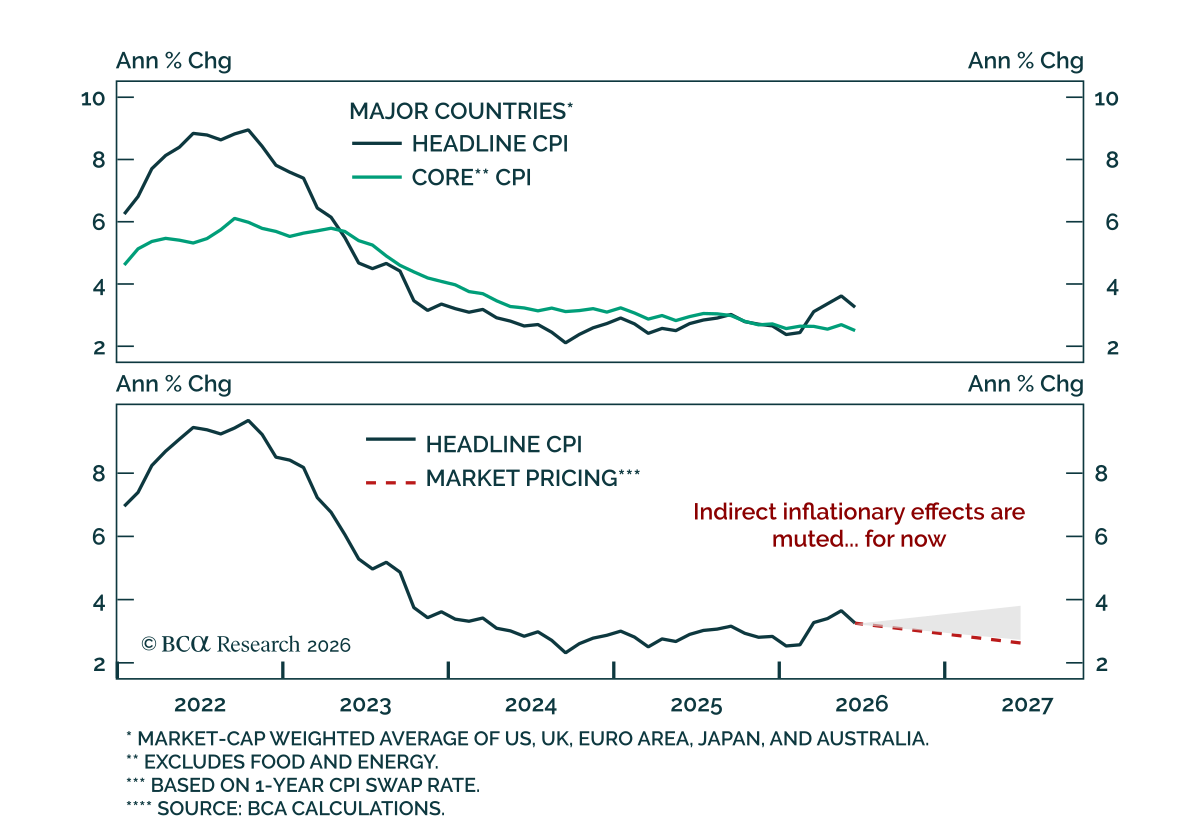

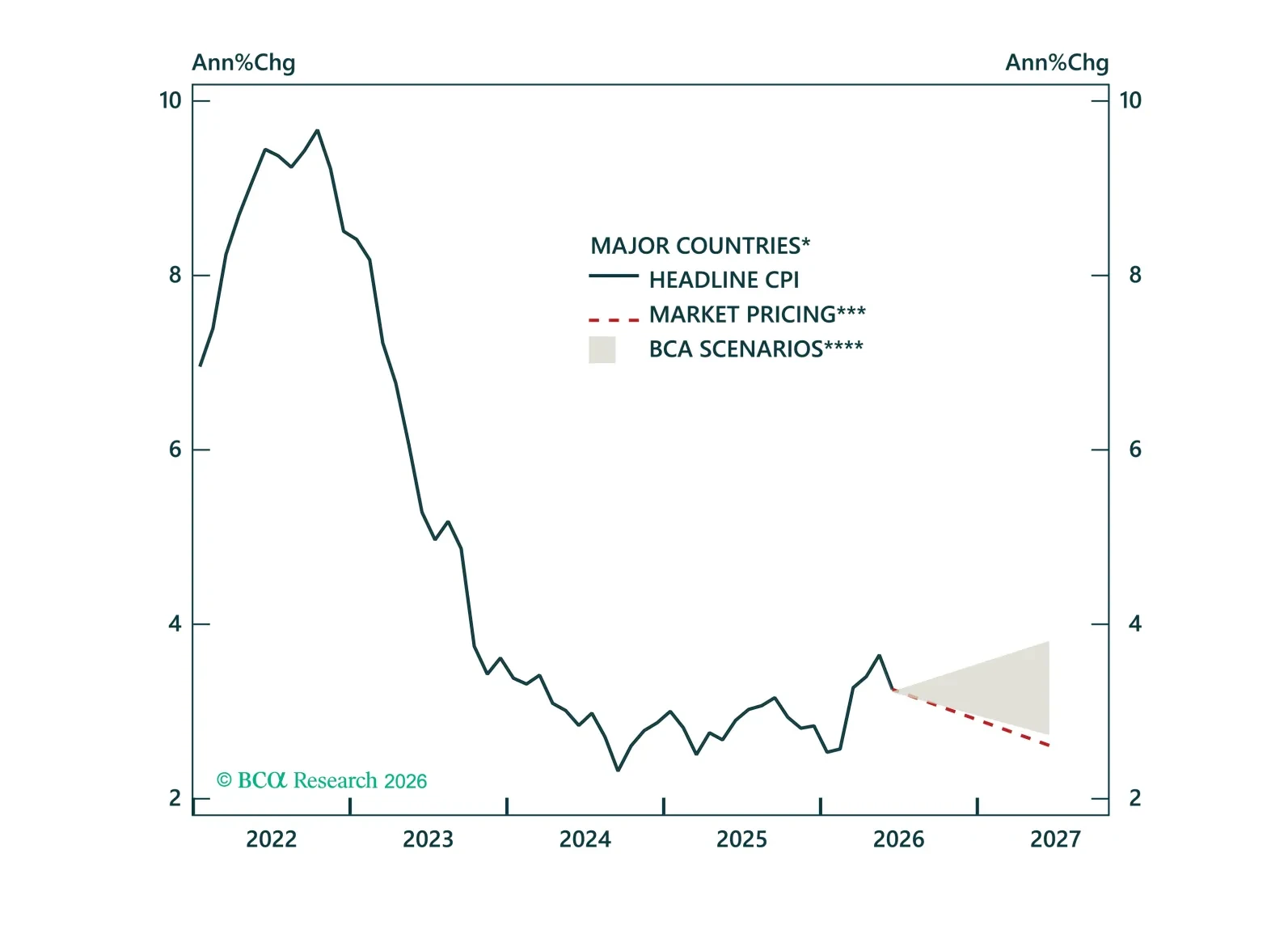

In this Strategy Insight, we assess how Middle East-related energy and shipping disruptions are shaping the global inflation outlook and review the implications for inflation-linked bond markets. We also examine the outlook for core inflation and the resulting implications for central bank policy and duration positioning.

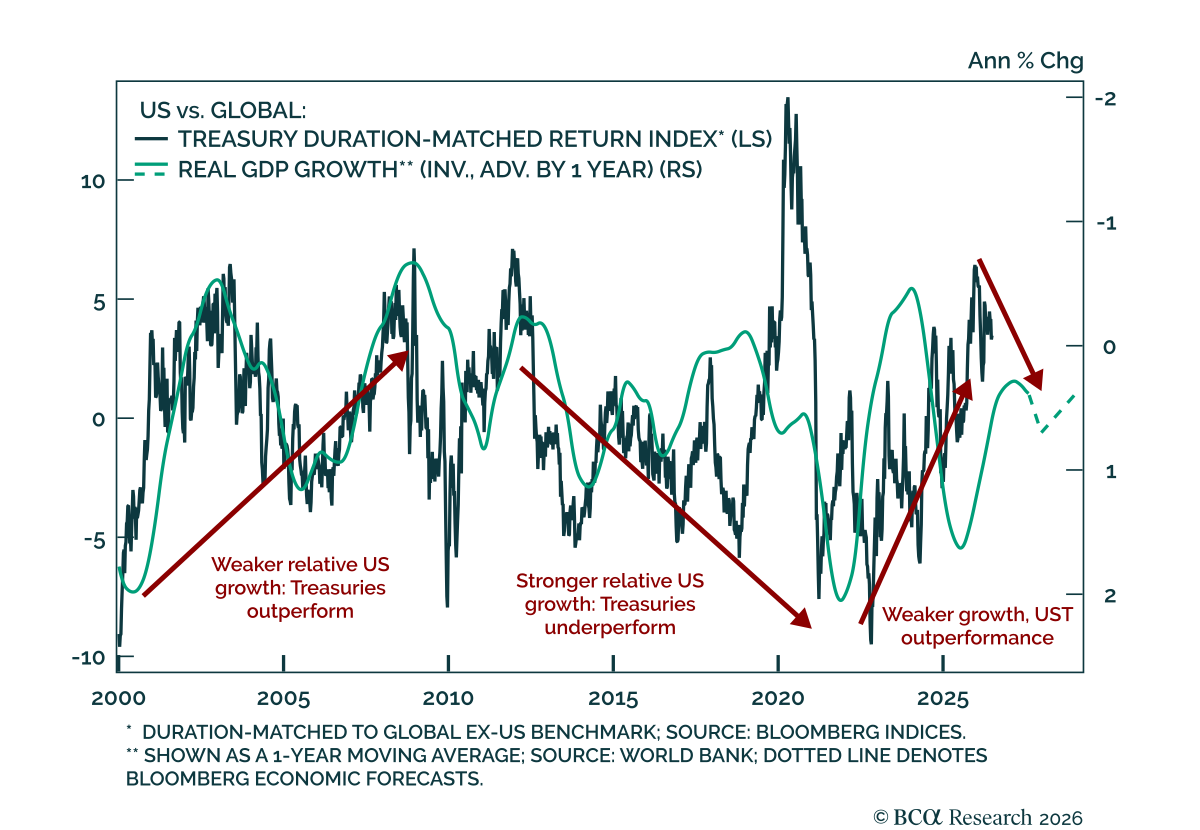

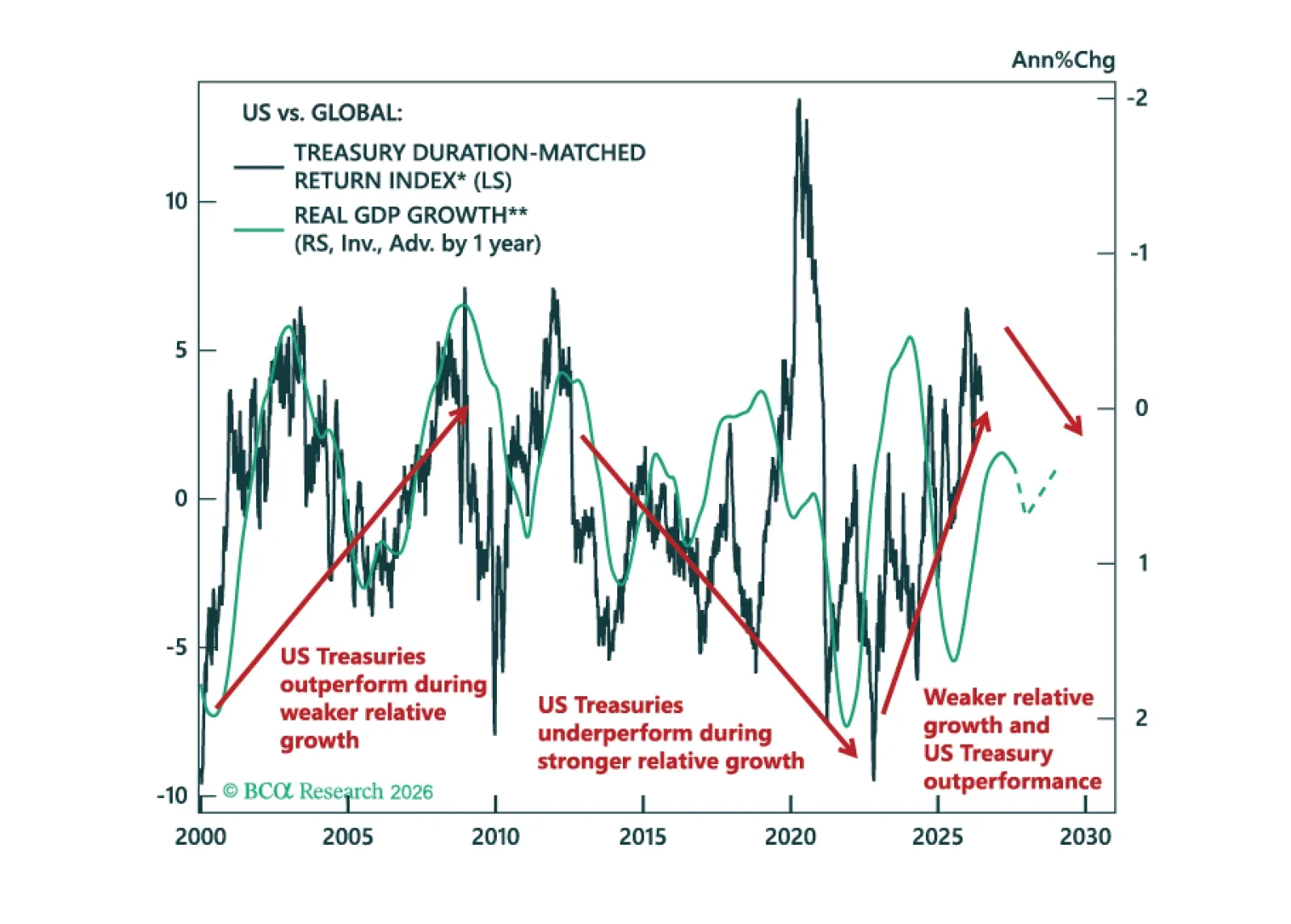

We review our Model Bond Portfolio performance for Q2 and look ahead as fixed income markets move beyond the US-Iran conflict, which is finding its kinetic equilibrium. Valuations and growth differentials are moving against continued US Treasury outperformance.

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.