Asset Allocation

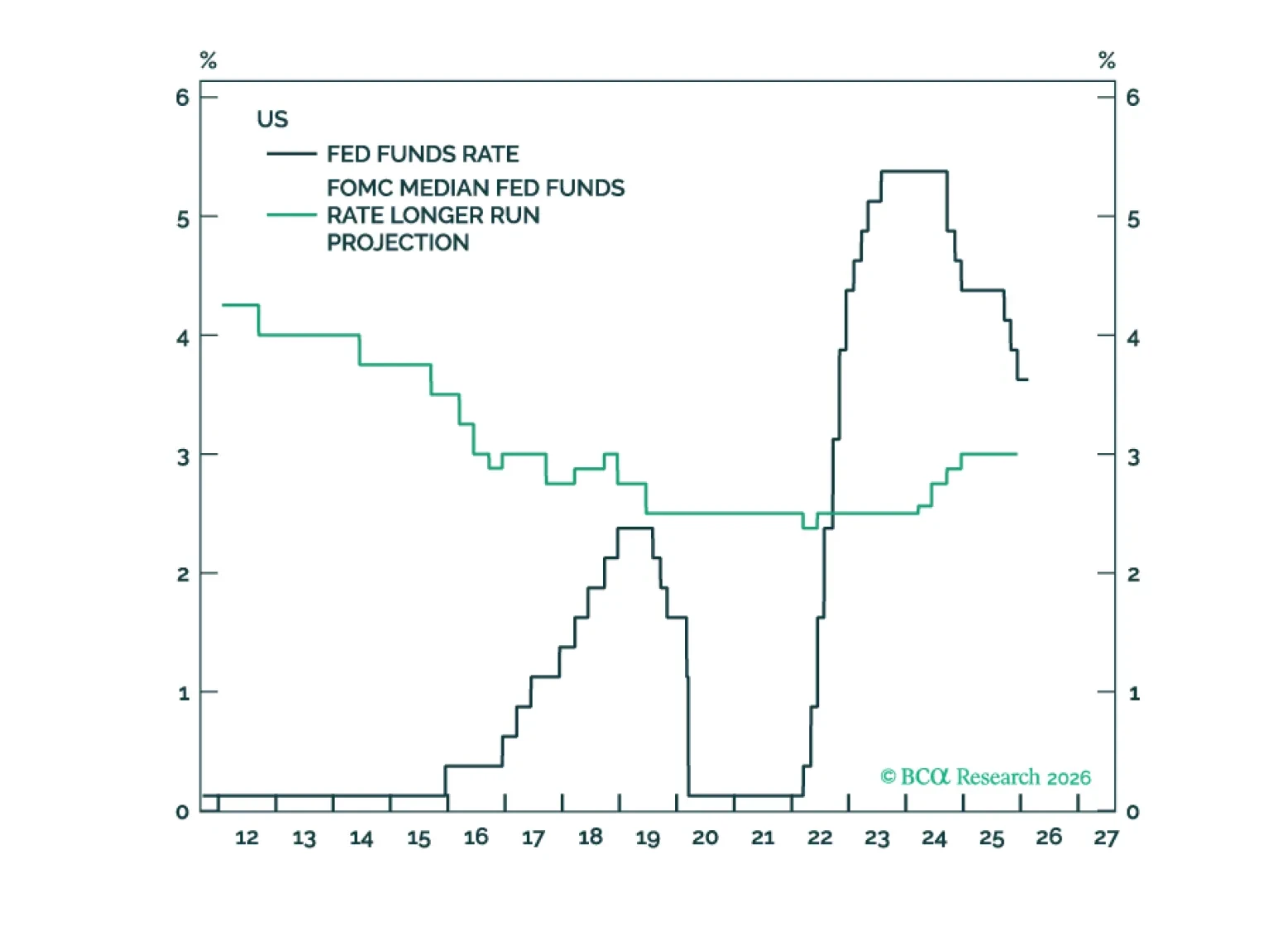

The neutral rate in the US is being propped up by a variety of forces that are at risk of reversing. These include the AI capex boom, large budget deficits, and the extraordinarily high level of household wealth. As such, interest rates are likely to surprise to the downside over the next few years.

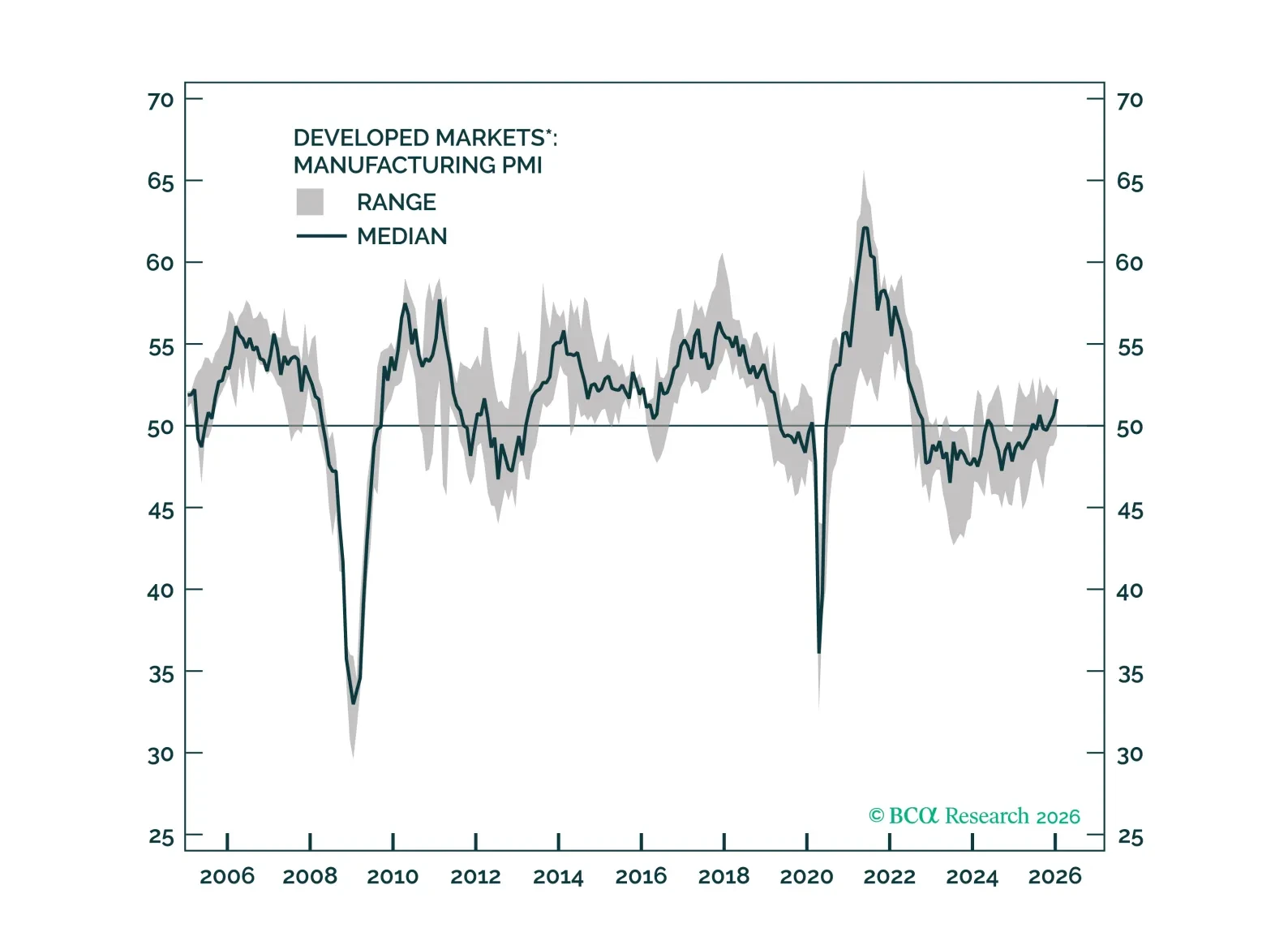

The actions of the Trump administration have dominated the headlines over the past month. They are all noise. Focus on the reactions from the rest of the world. Policy makers outside of the US are now determined to stimulate and reform their domestic economies. Global growth is accelerating without a corresponding increase in inflation. This combination is not only positive for risk assets but is also supercharging returns for Ex-US stocks. Downgrade Fixed Income and duration.

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

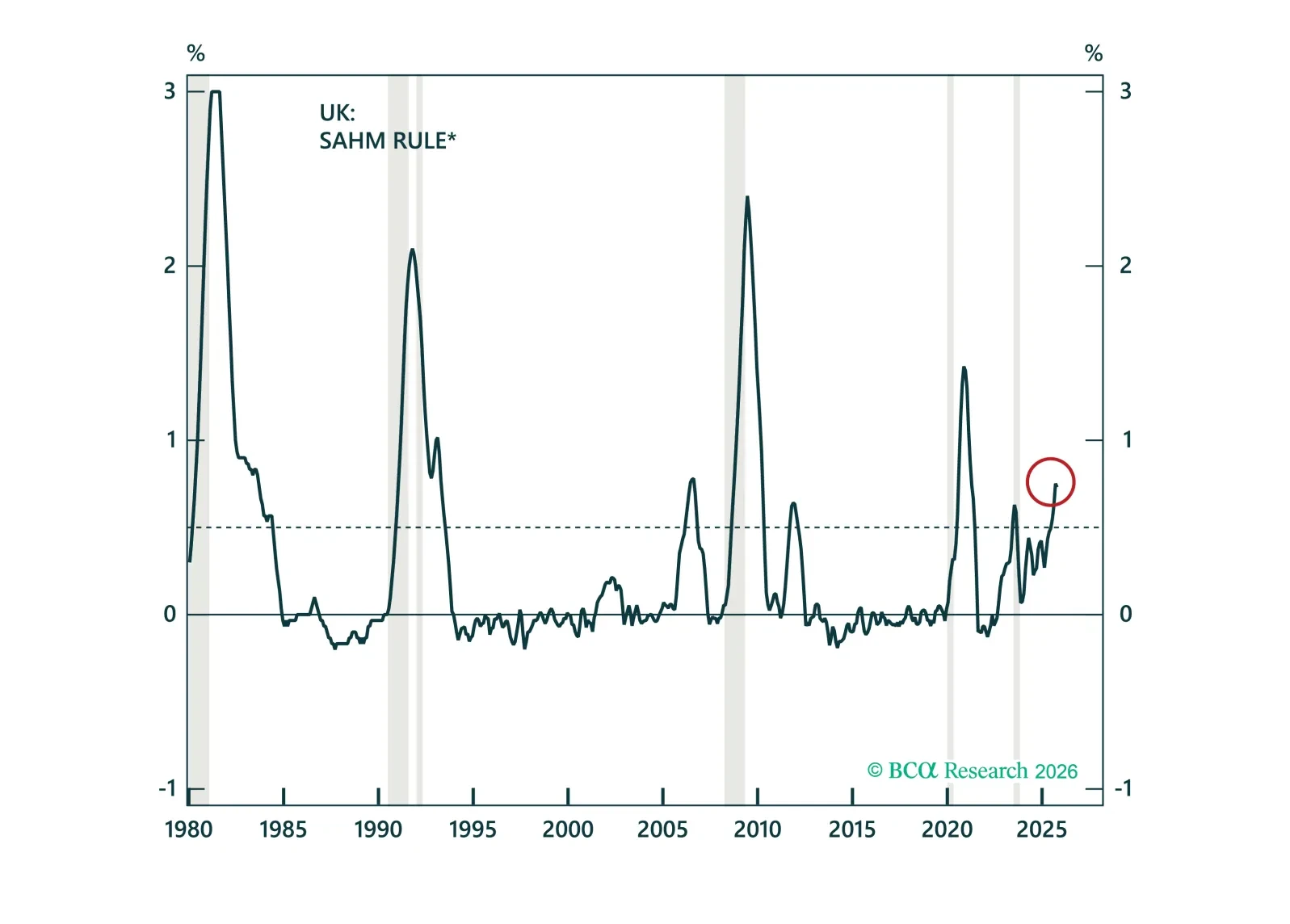

Recession risks in the UK are clearly rising. In this Special Report, we unpack why labor market deterioration, falling wage growth, and normalizing inflation support deeper BoE cuts ahead. We then discuss how to position across gilts, the pound, and UK equities.

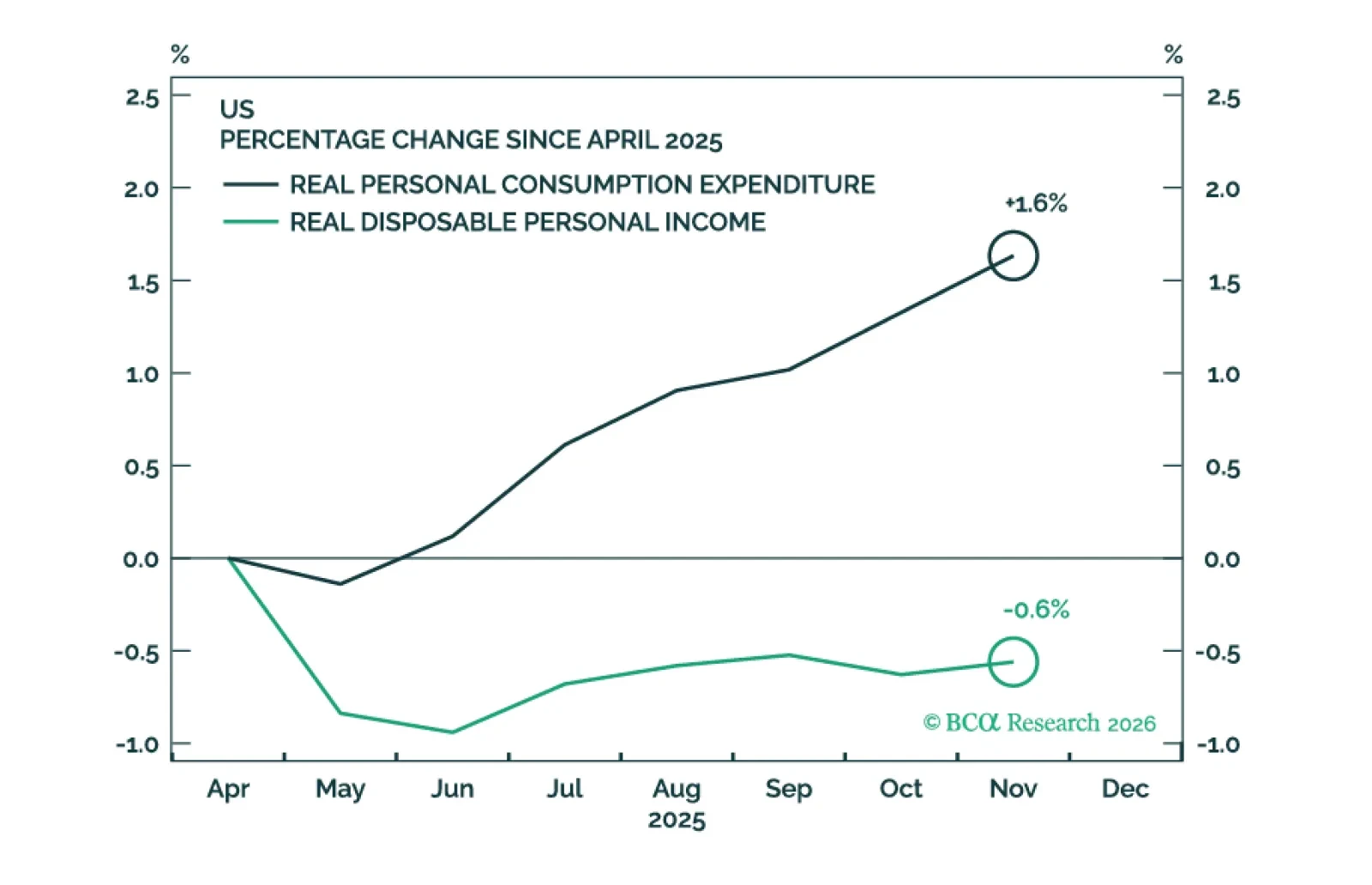

Recent economic data have been reasonably firm. We will cut our 12-month US recession probability to 40% from 50% if the Supreme Court strikes down President Trump’s tariffs. This would take our scenario-weighted year-end 2026 price target for the S&P 500 to 6375 from 6200.

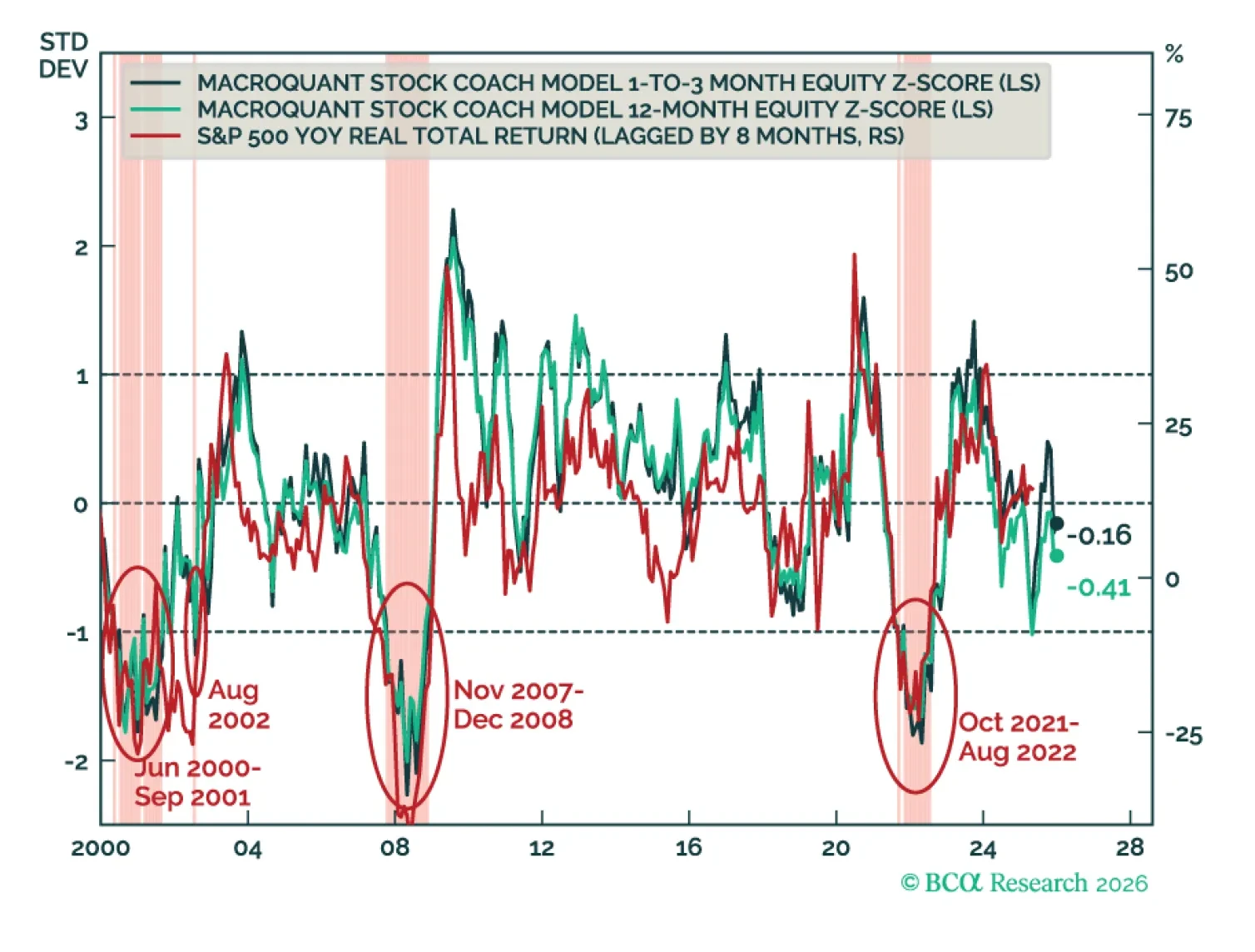

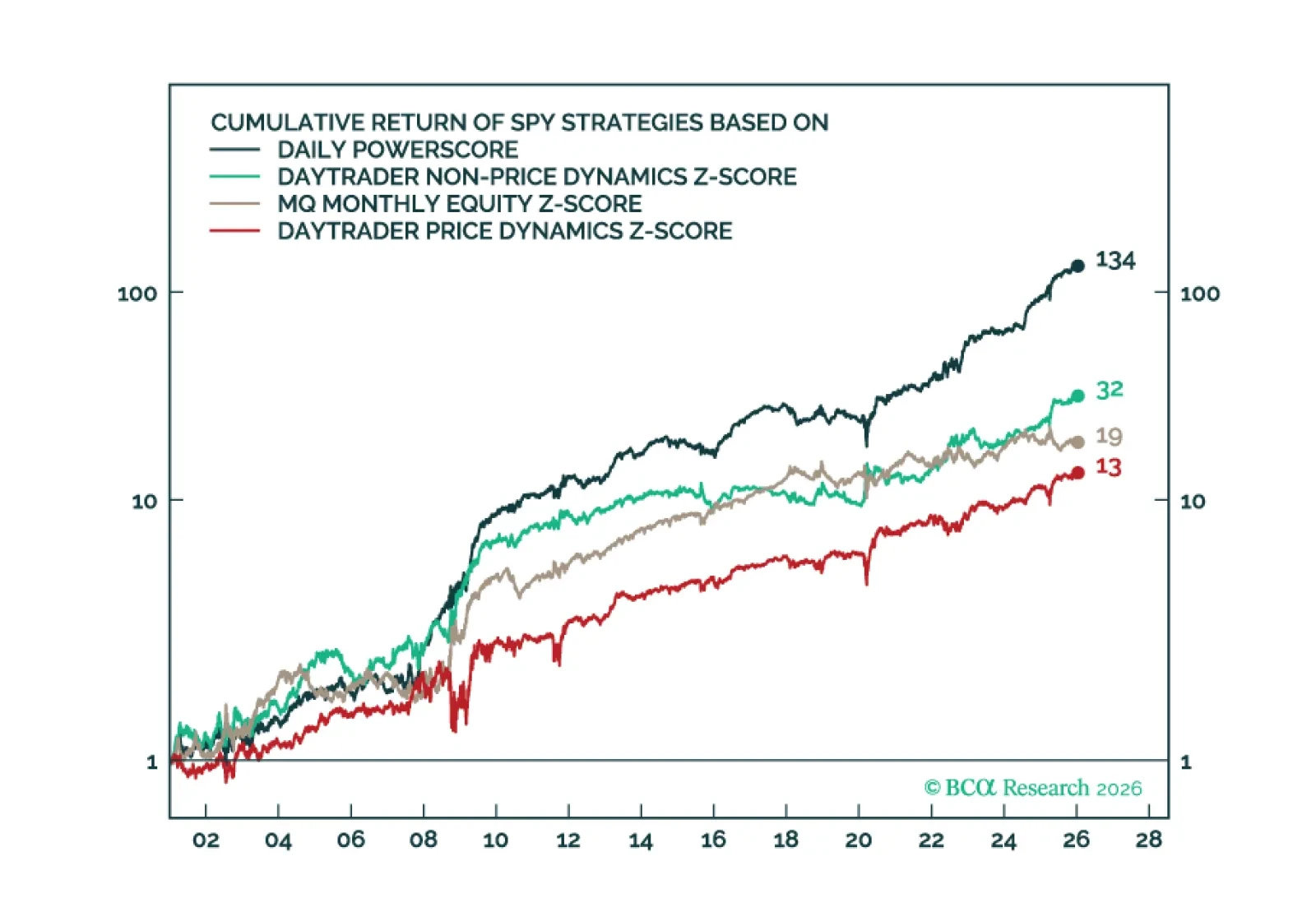

Over the past few months, we have been deploying new market-timing tools aimed at improving the accuracy of our calls. Today’s report highlights our ultra high-frequency Daily Oscillators, which provide daily signals on the near-term direction of the S&P 500 and long-term Treasuries.

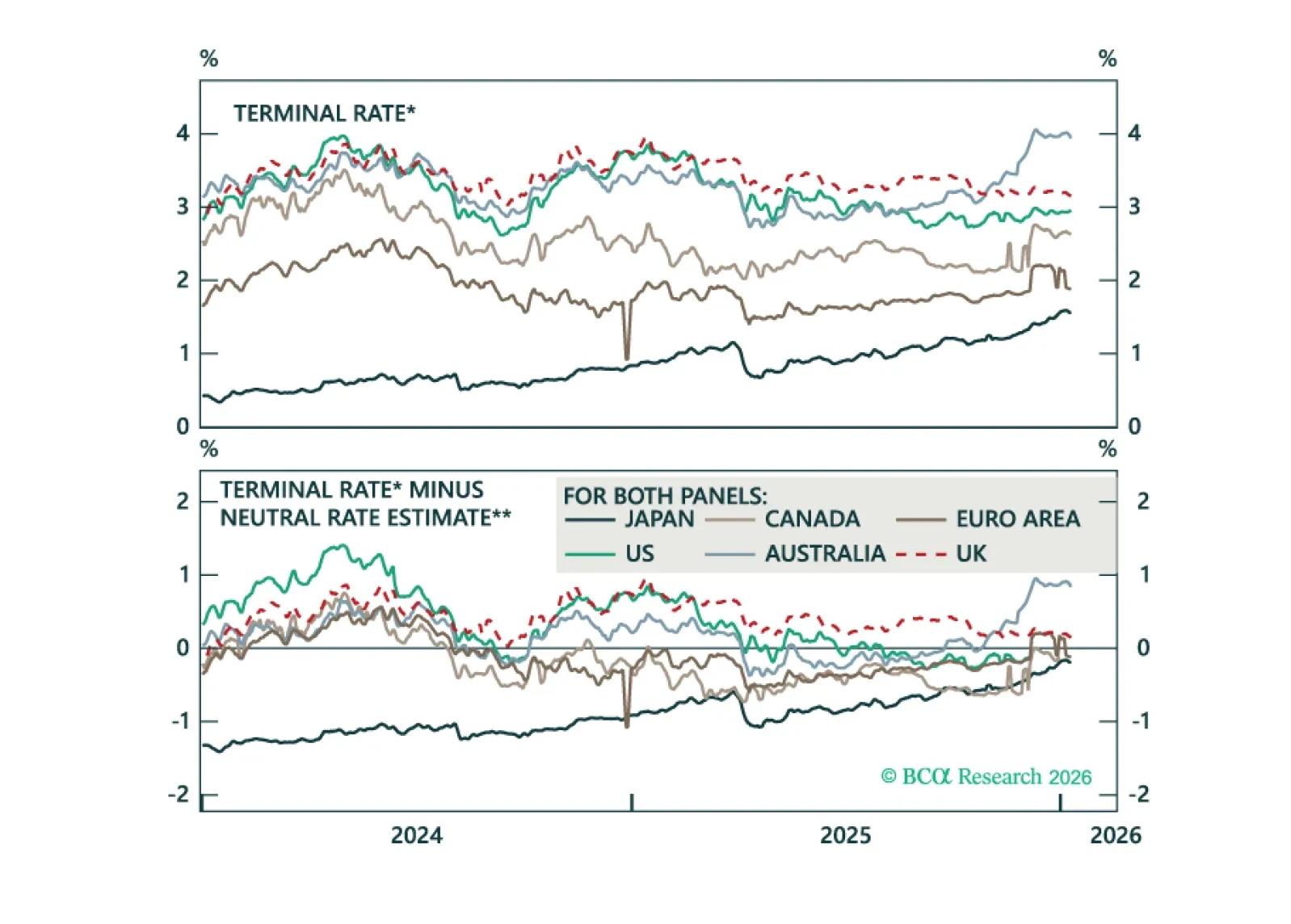

Our Q1 outlook maps global growth, curve dynamics, and policy surprises, which we then translate to our recommended global fixed income portfolio allocations and trades.

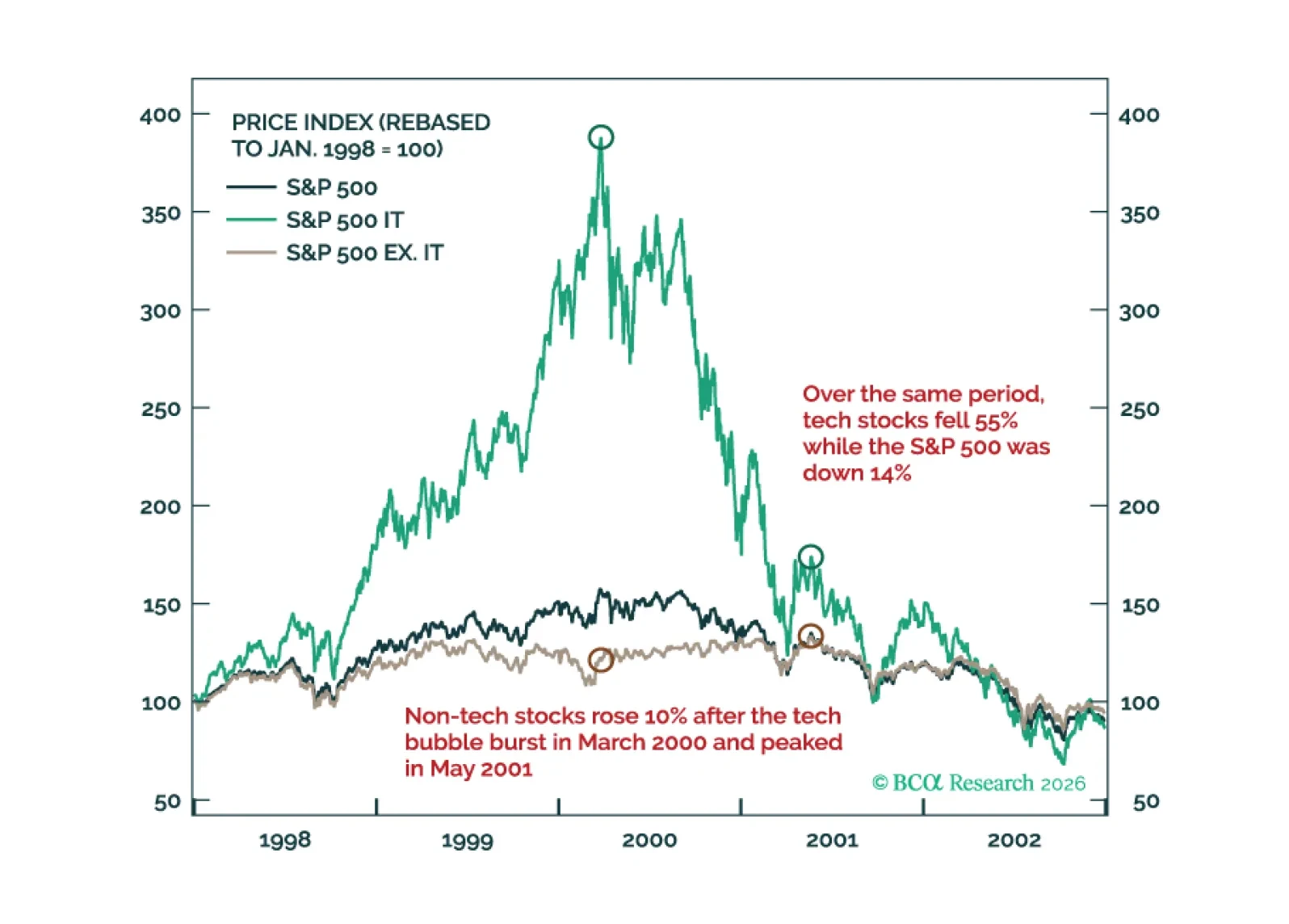

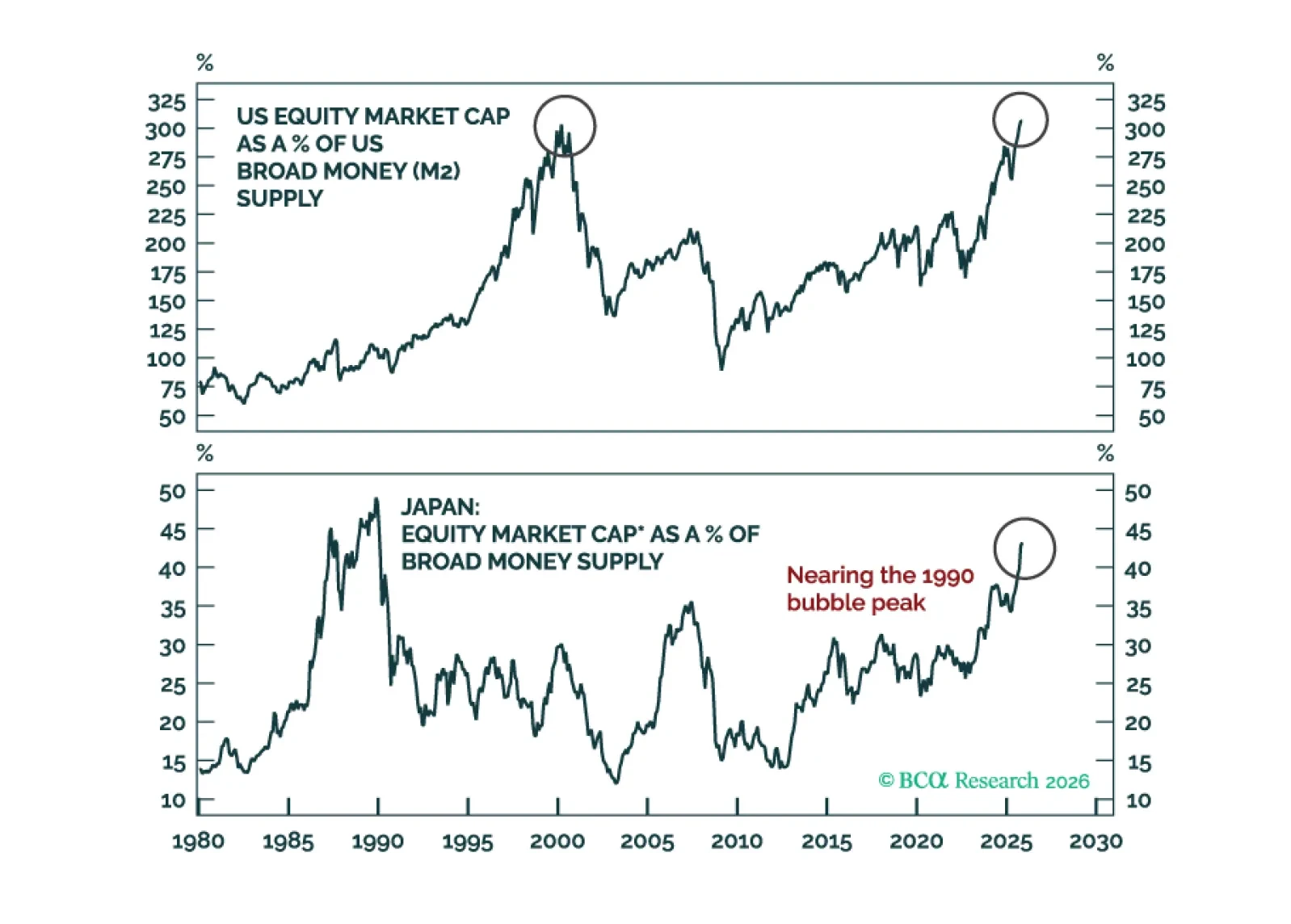

Much like the 2000 episode, we expect this year to unfold in two stages: A “Great Rotation” from tech stocks to non-tech names in the first half of 2026 followed by a broad-based selloff in stocks in the second half on the back of a weakening US economy.

At major technical crossroads, markets eitherpull back before staging a sustainable breakout, or attempt to break out only to drop considerably (i.e., a fakeout). We believe the latter dynamics are more likely to play out.

MacroQuant has downgraded equities to underweight, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is still bullish on gold.