Asset Allocation

MacroQuant recommends an underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is neutral-to-slightly positive on the US dollar, remains neutral on gold, upgrades copper to neutral, and is very bullish on oil.

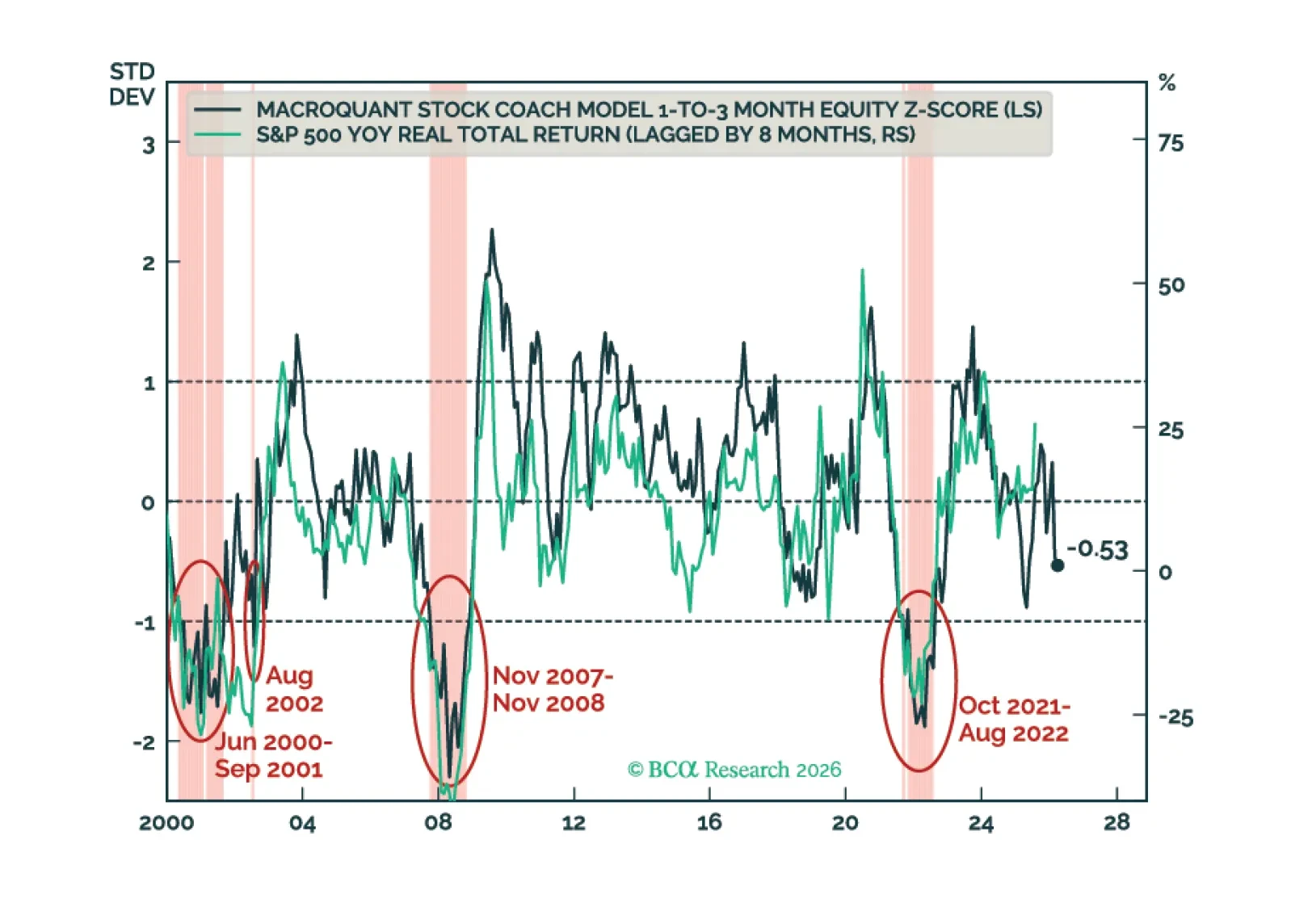

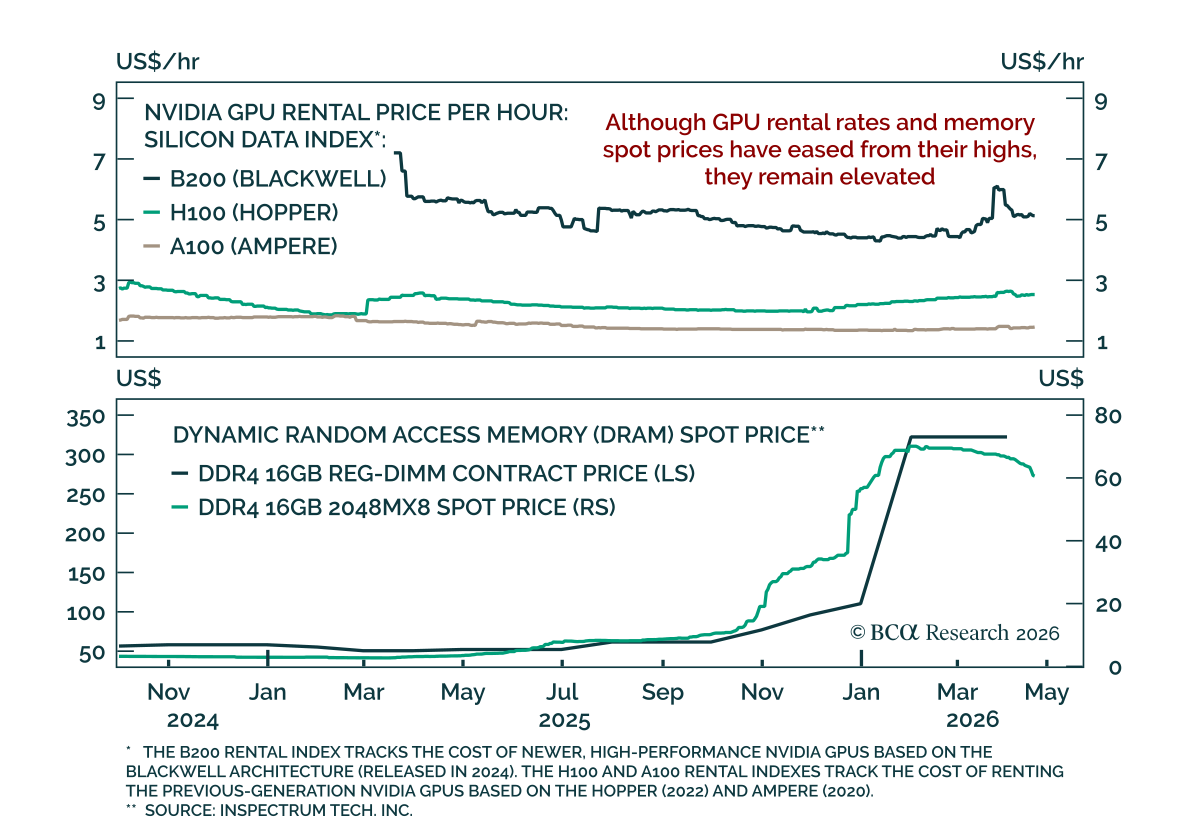

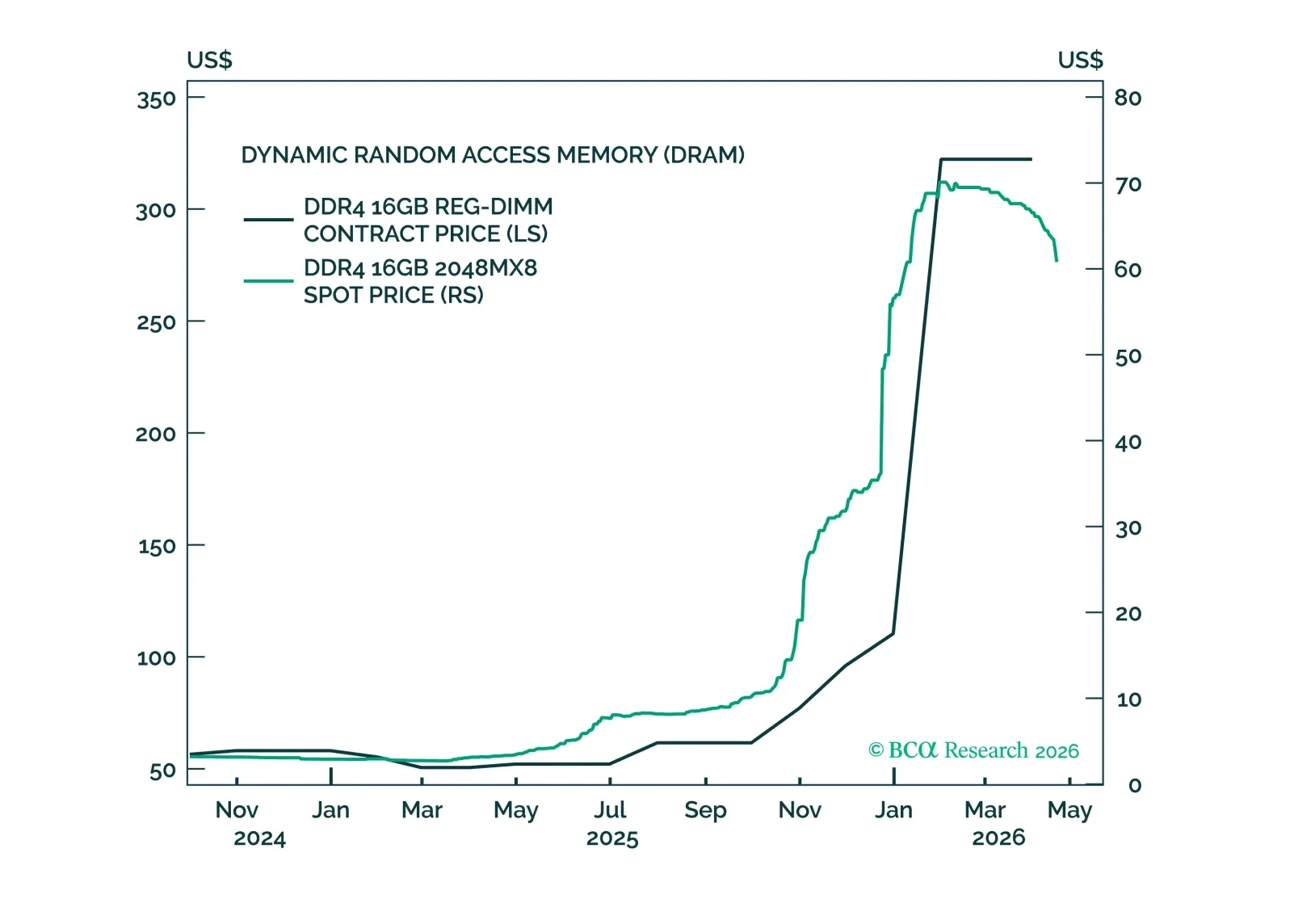

Most of the increase in S&P 500 earnings estimates this year has stemmed from shortages. The oil shortage, which has pushed up estimates for energy companies, will fade once the military conflict is resolved. However, the shortage of semiconductors and other AI paraphernalia could persist for a while longer. As such, we are moving our recommended 12-month equity allocation from a slight underweight to neutral. We are already neutral on a 3-month horizon.

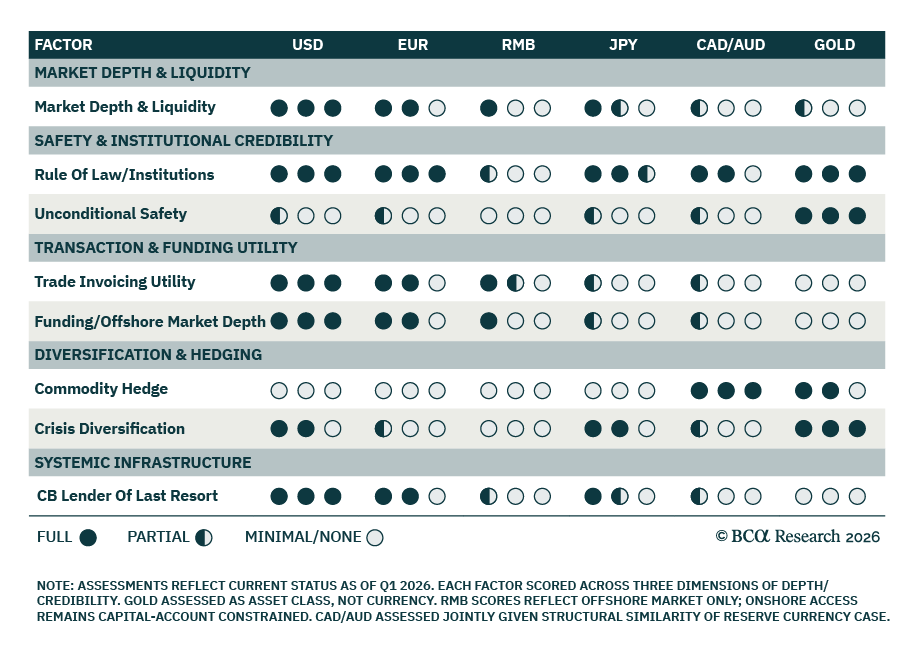

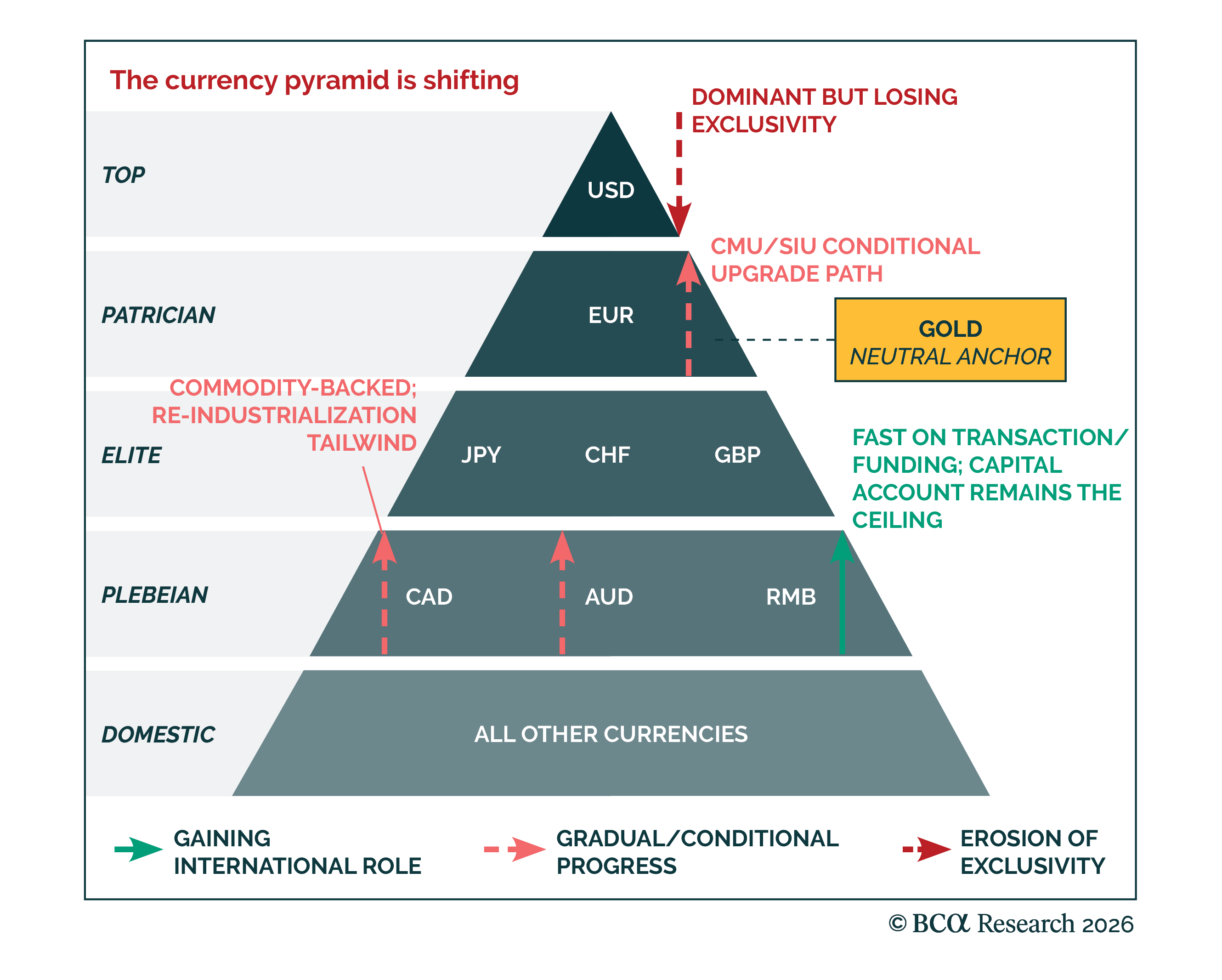

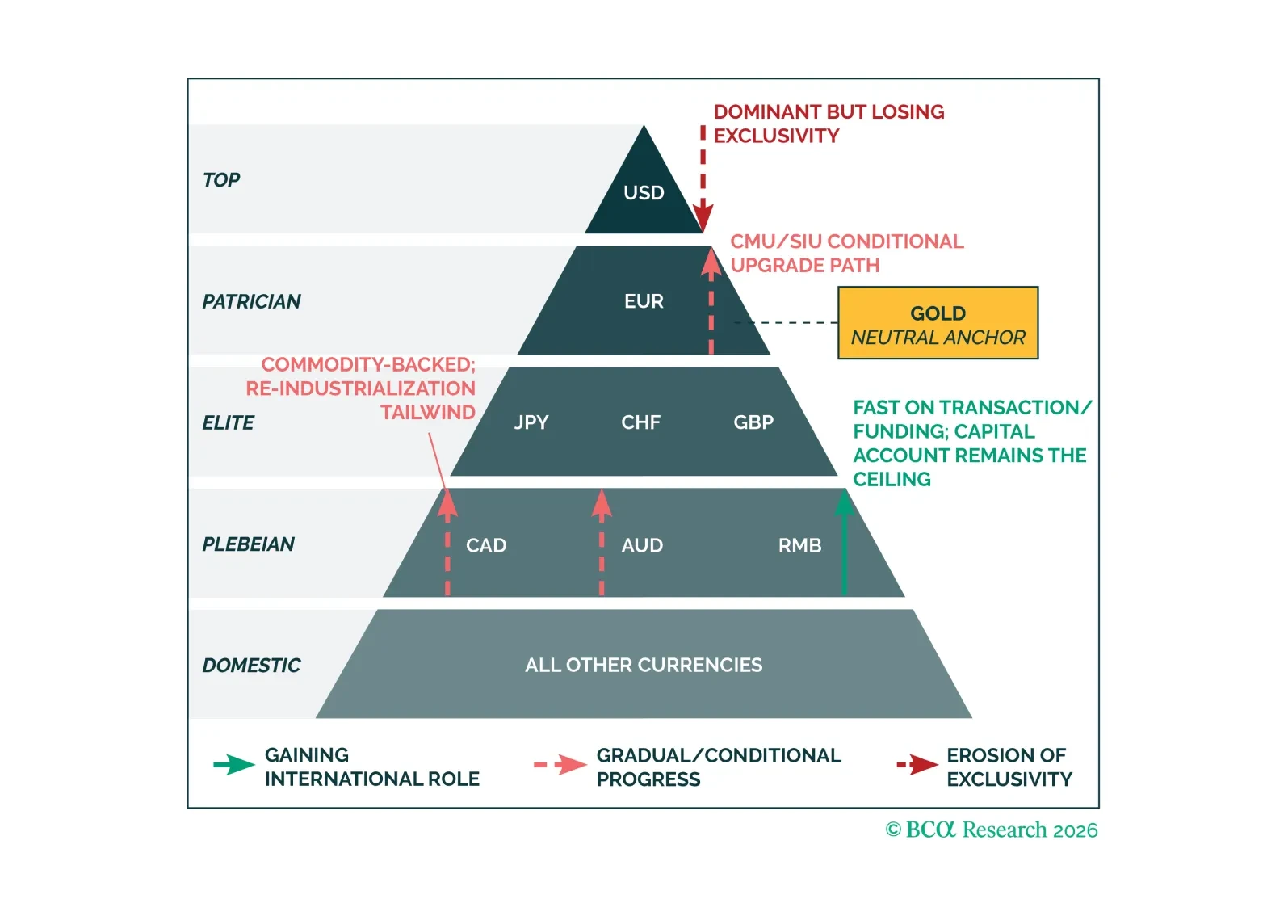

The debate over “what replaces the dollar” is misguided. The real shift is toward a multi-anchor system where reserve functions fragment. That changes everything from term premia to cross-asset correlations. The implication: portfolios built for the old regime are already behind the curve.

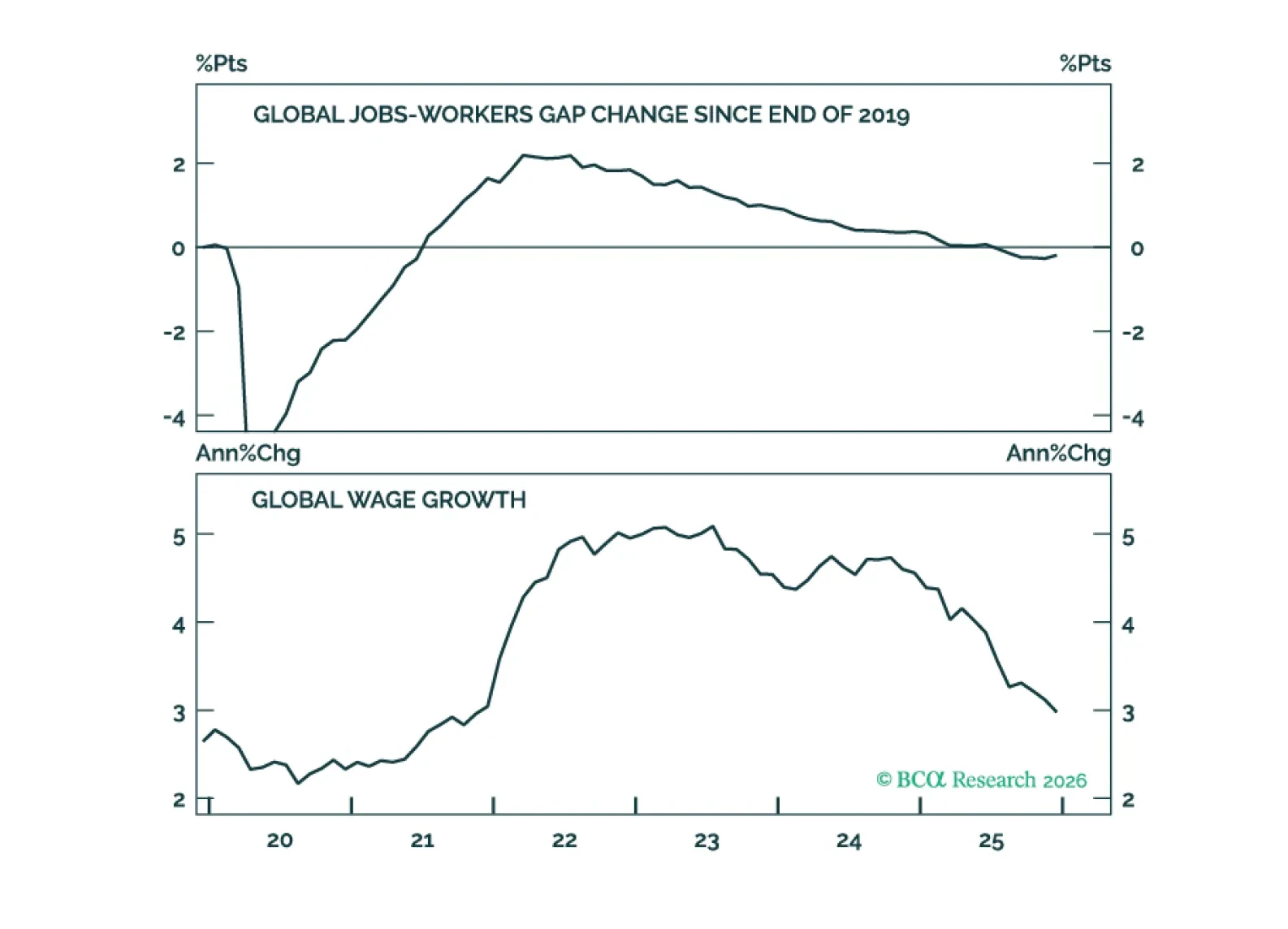

We do not expect the oil shock to have a lasting effect on inflation. Looking further out, a variety of structural forces will influence inflation, including fiscal policy, globalization, demographics, and AI.