Argentina

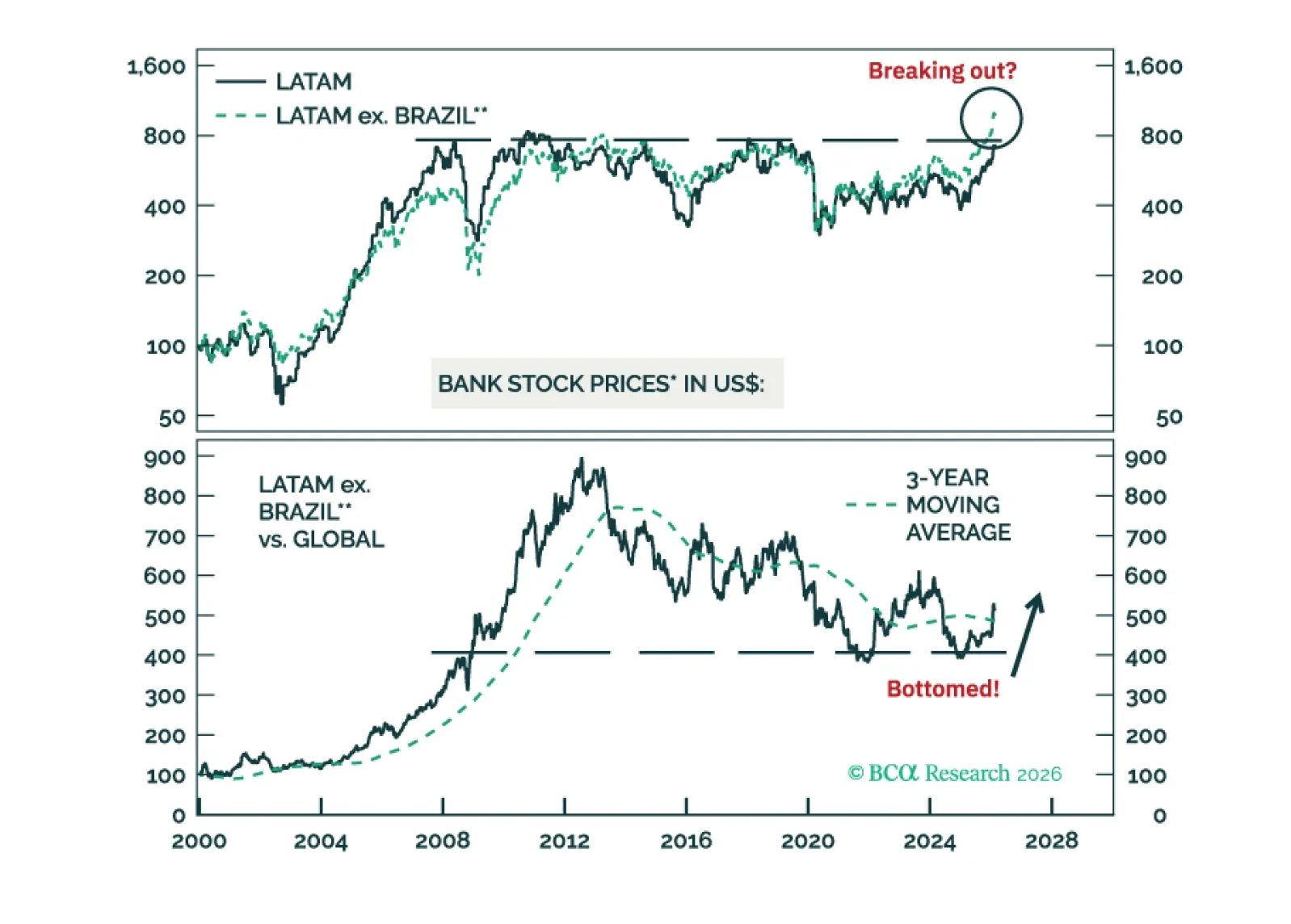

Go long LATAM ex. Brazil banks / short global bank stocks. Brazilian bank equities will underperform due to poor and worsening macro fundamentals.

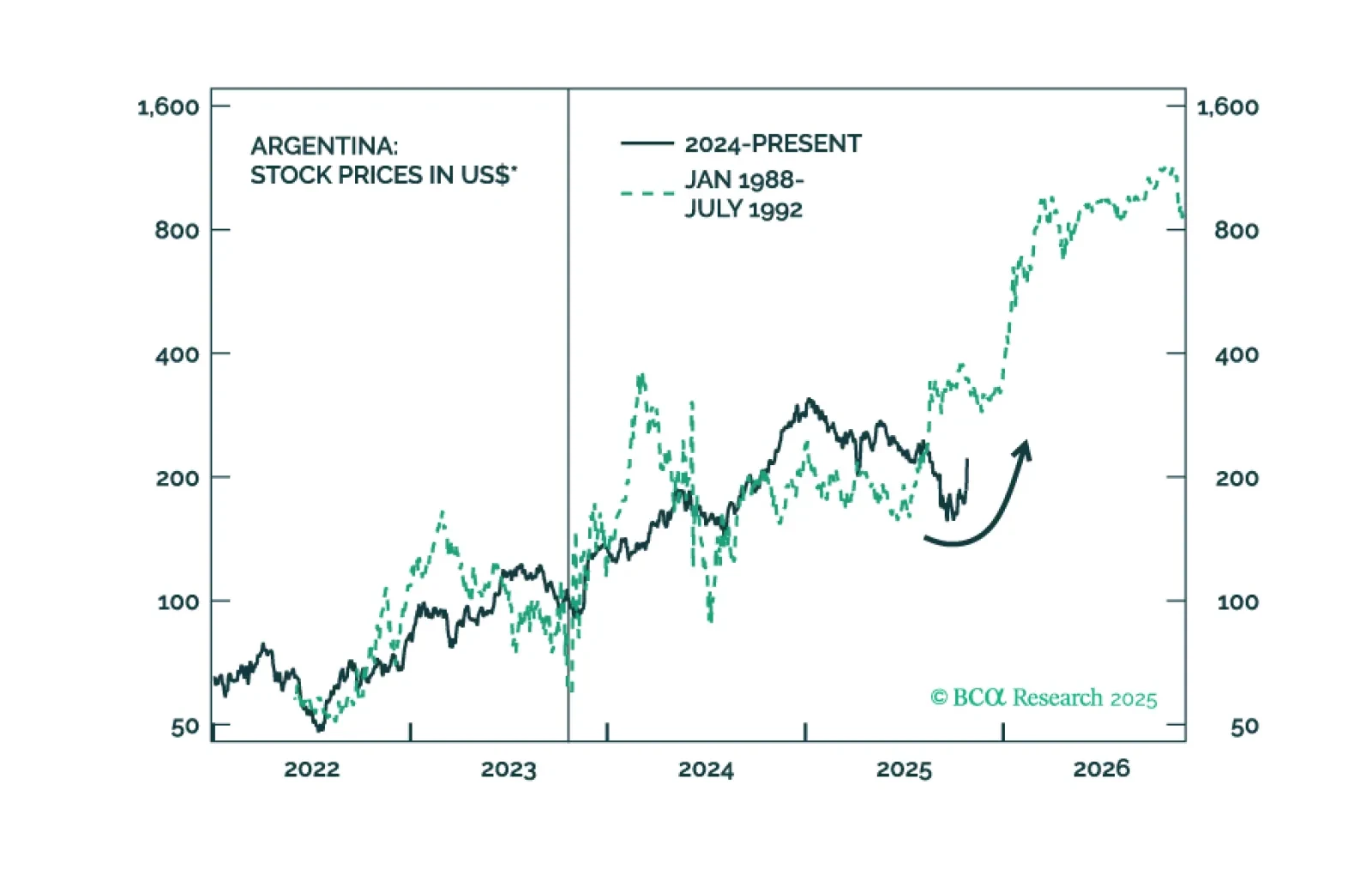

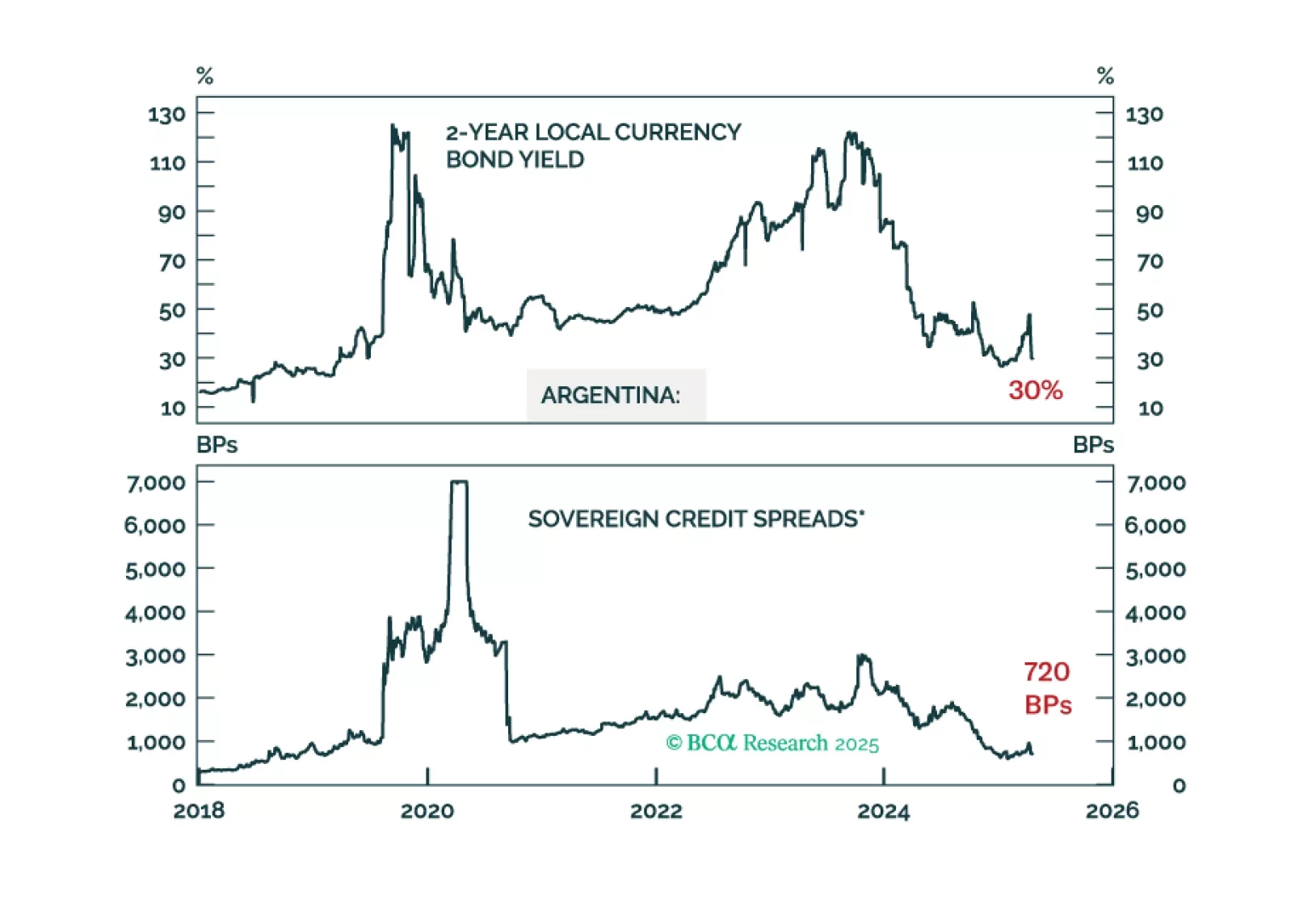

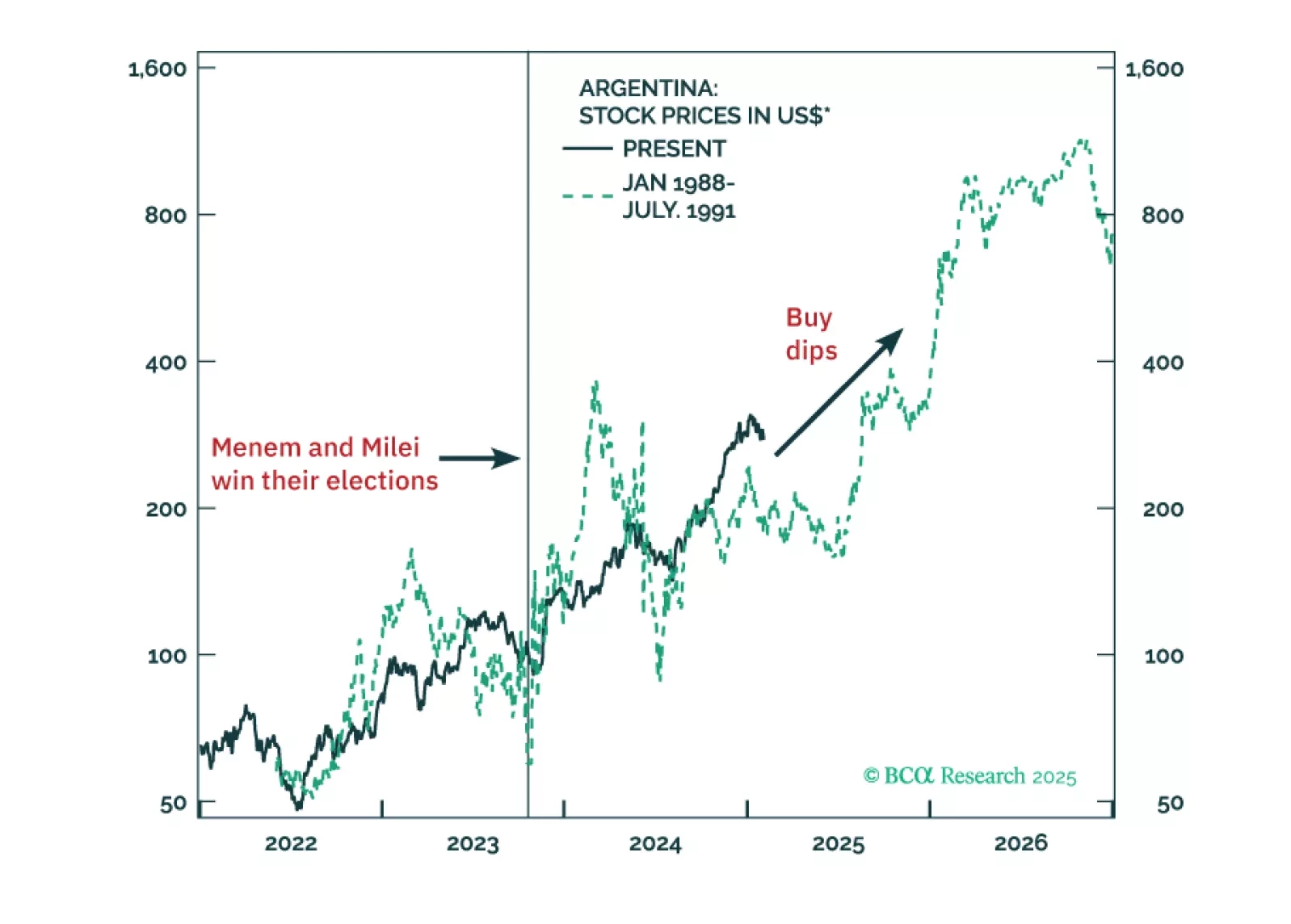

President Javier Milei’s electoral win has massively outperformed expectations. Meaningful legislative support and renewed market confidence will revitalize his liberalizing economic program. Our recommendation not to sell Argentine assets following the post-Buenos Aires election carnage has been validated.

The Buenos Aires election results are a setback for the government's political momentum, but not the endgame. Our long-term bullish view remains in place, but short-term investors should stay on the sidelines in the near run.

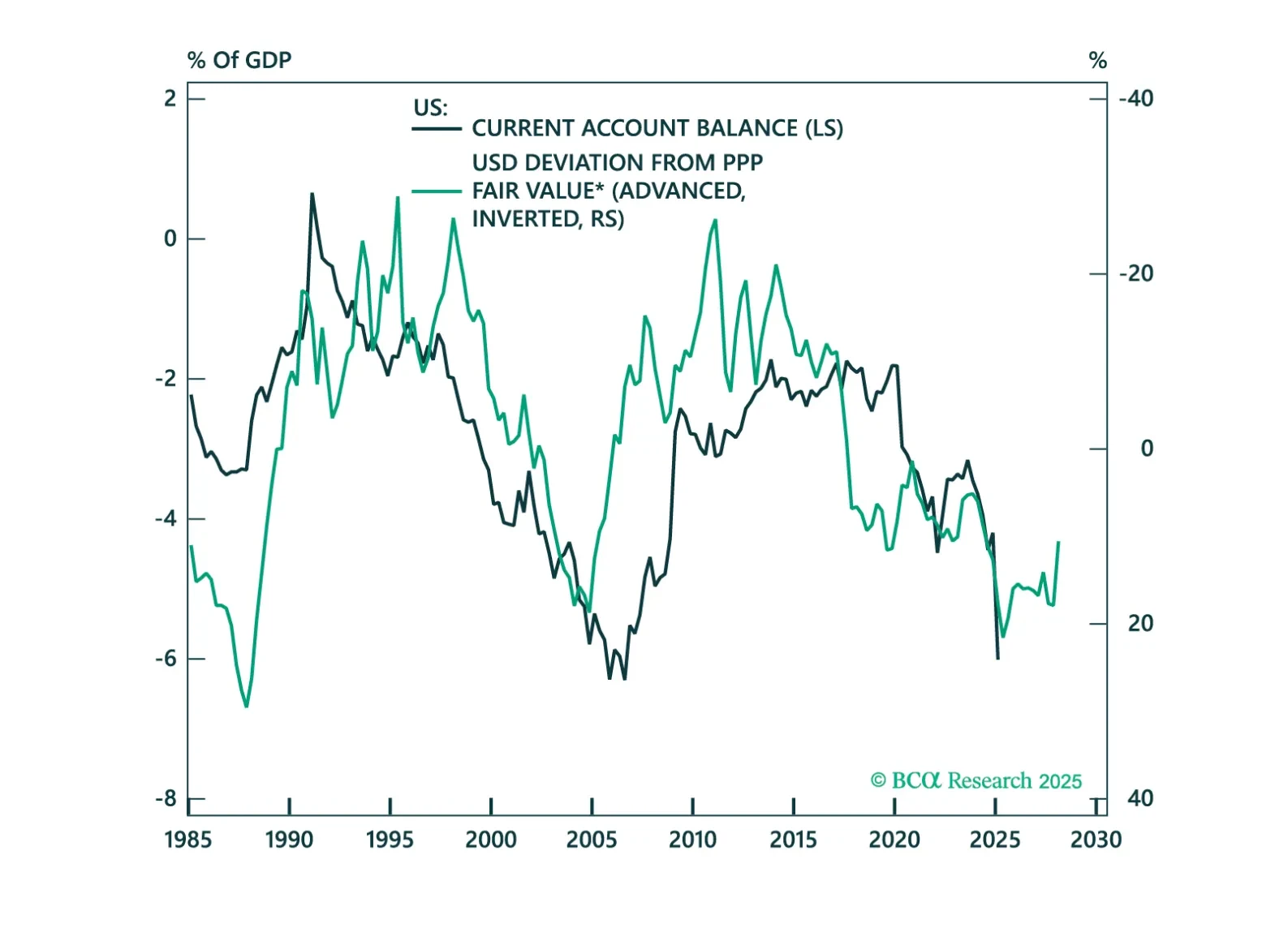

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.

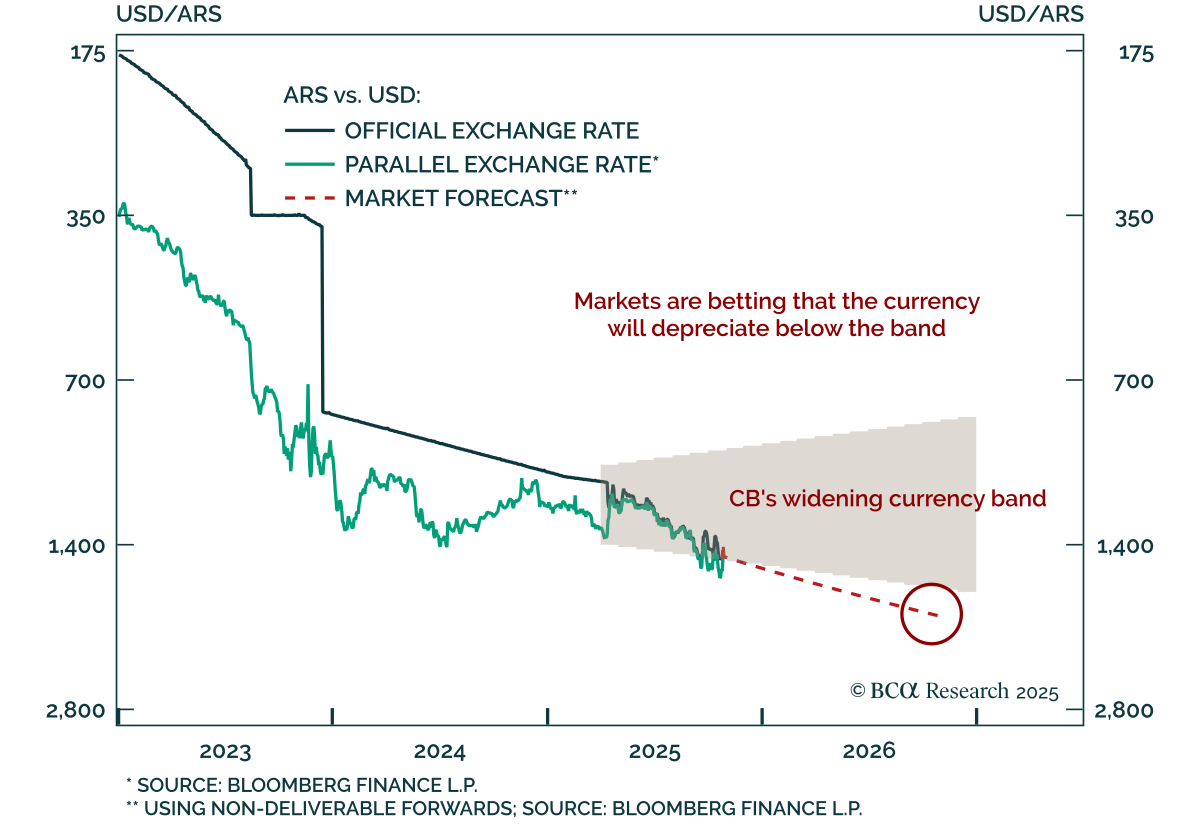

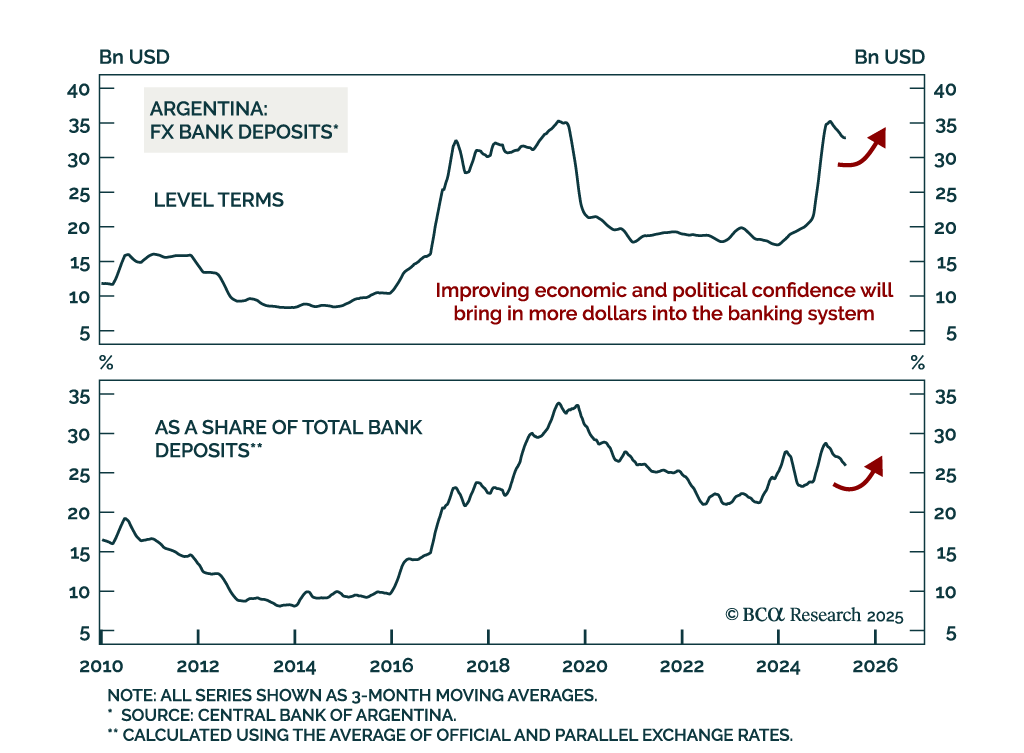

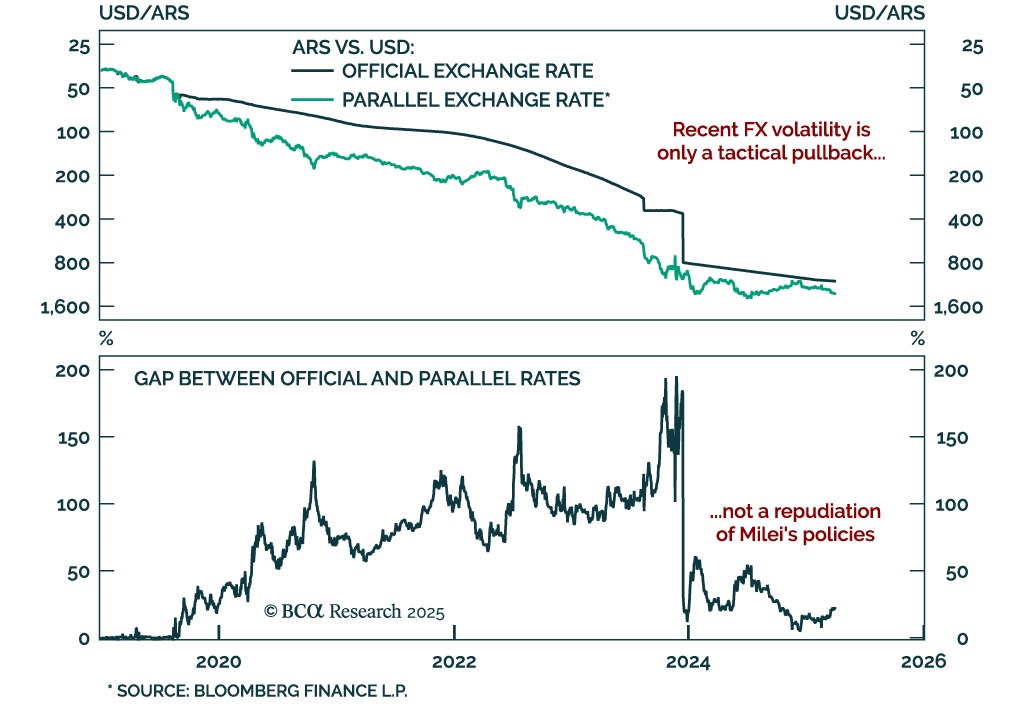

Amid the storm of global financial uncertainty, Argentina stands out as a free-market safe haven. The lifting of currency controls was the last step taken by this country to embrace market mechanisms. We recommend that investors buy Argentine equities, sovereign credit, and domestic bonds, and overweight Argentina within EM equity and fixed-income portfolios.

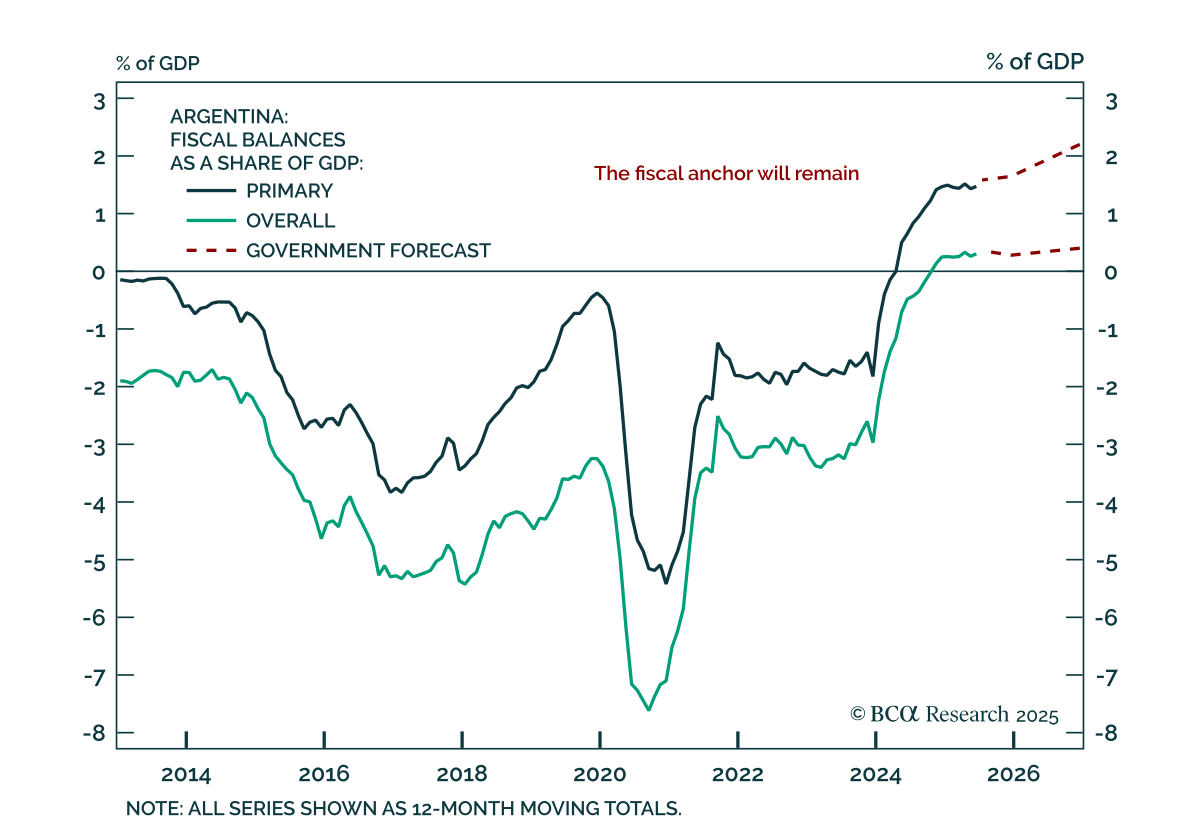

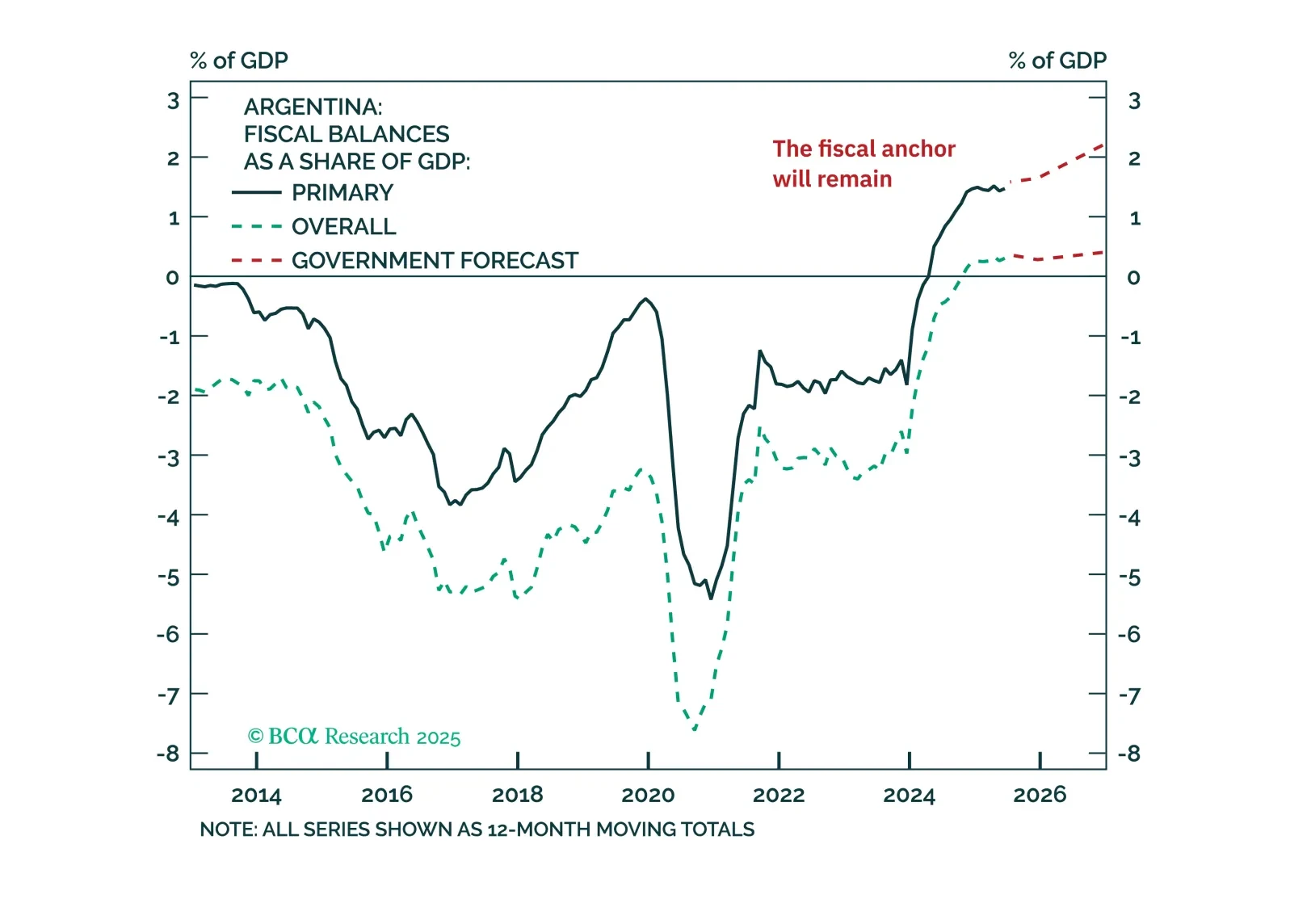

Argentina is entering a regime shift from the traditional short boom-bust cycles of the past 50 years. Profound structural reforms will result in a productivity boom, leading to a more durable economic expansion while keeping with the disinflation trend. Authorities will likely lift capital and currency controls in the second quarter of this year. All in all, odds are that Argentinian assets have entered a multi-year bull market.