Americas

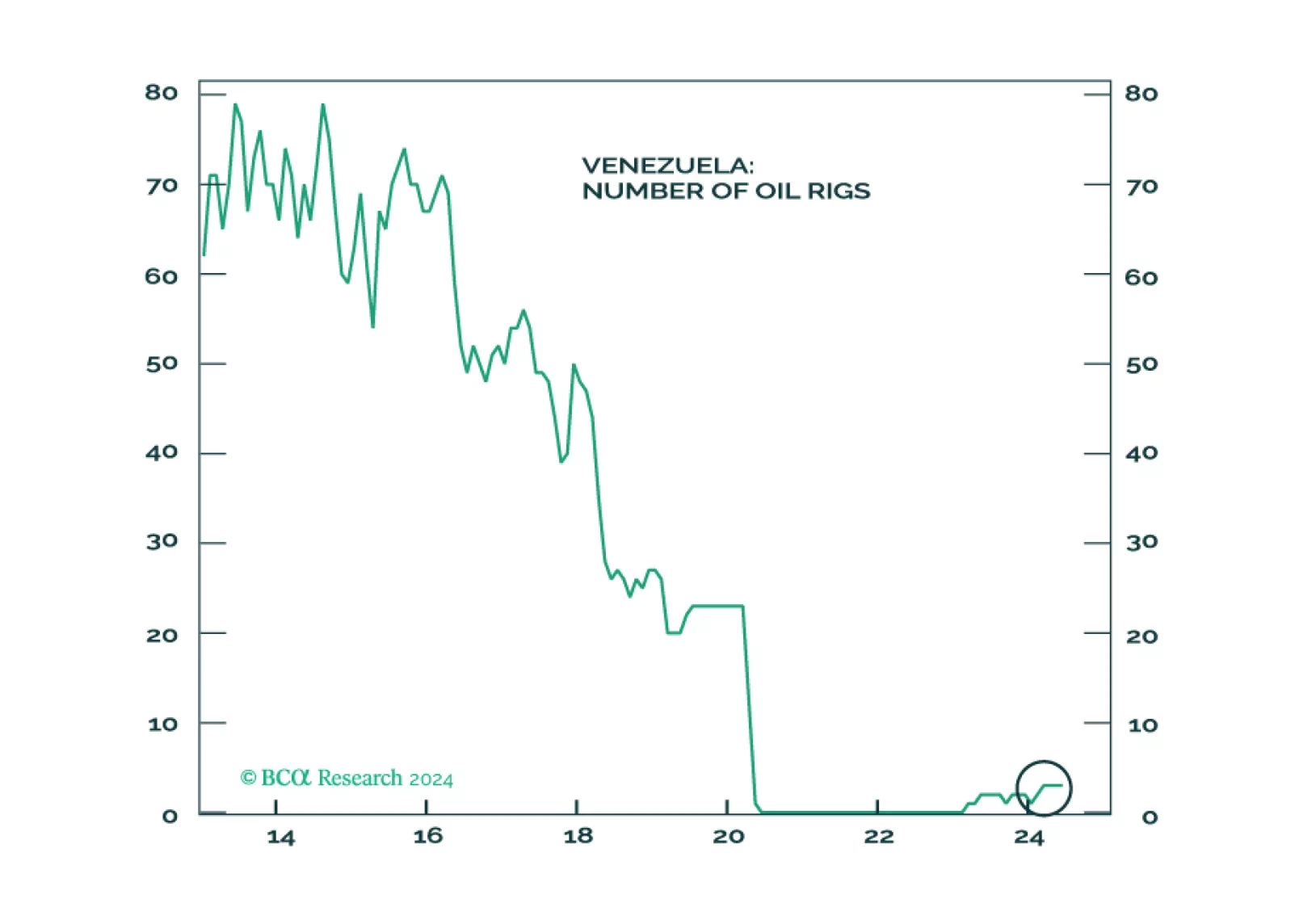

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.

In Section I, we examine some concerning signs of US economic weakness that emerged in June. We also discuss portfolio positioning in the face of falling interest rates and cross-check our recommended US equity overweight in the face of extremely optimistic expectations about AI’s impact on growth. We conclude that defensive positioning continues to be warranted. In Section II, we dig into those optimistic expectations for AI. We find that the US equity market is significantly overvalued unless the deployment of AI technology causes a 10-to-20 year productivity surge in line with what occurred during the IT revolution of the 1990s, with persistently high margins on the revenue generated from the improvement in growth. We doubt that AI will end up truly boosting economic activity by this magnitude.

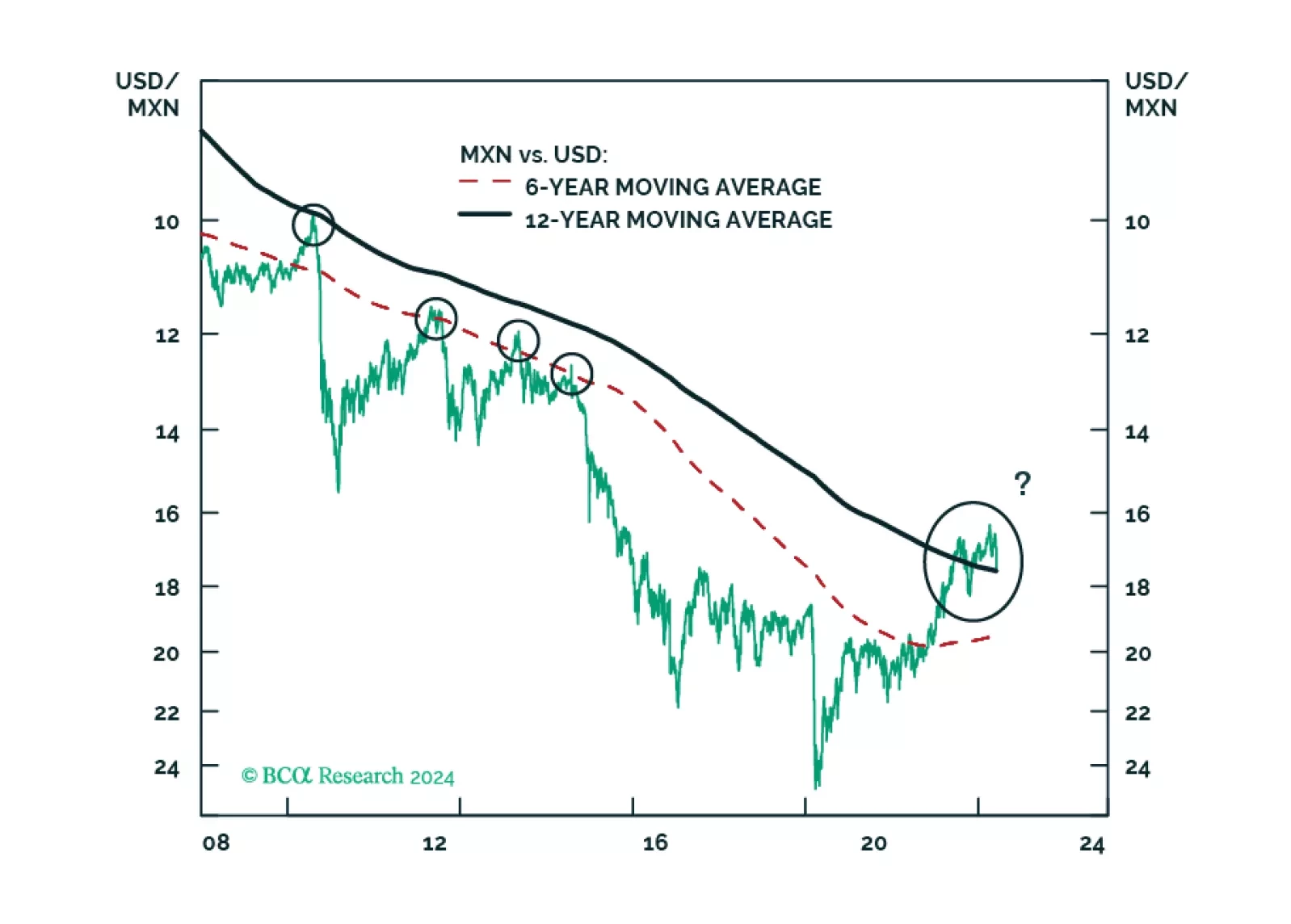

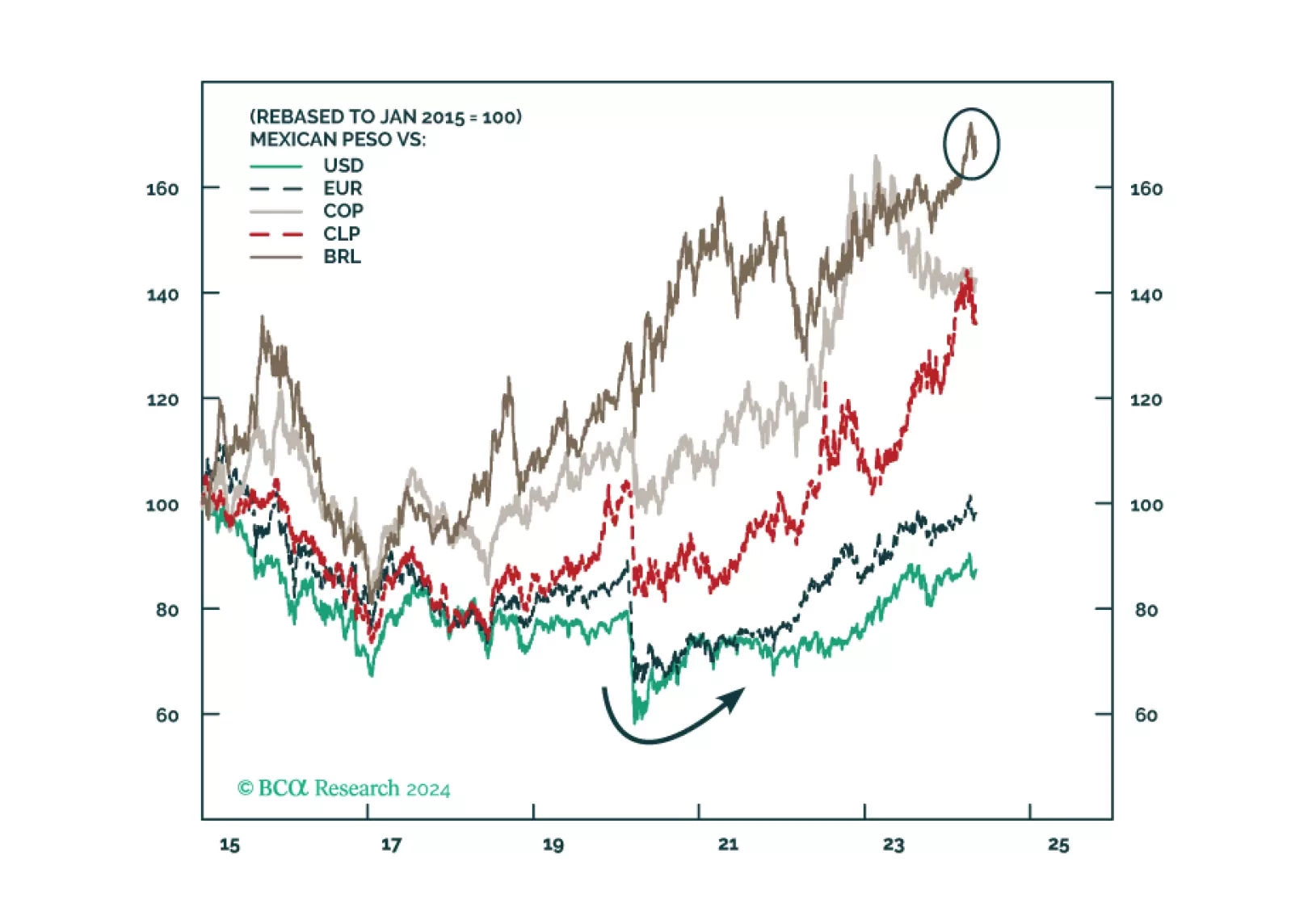

MORENA has once again swept the Mexican election: Claudia Sheinbaum will be president, with little to no constraint in Congress. All in all, Mexican politics will remain stable and overall supportive of markets. In the medium term, fiscal spending will return to conservatism and the constitutional reforms will lead to mixed fiscal and economic repercussions. In the long term, however, fiscal and institutional risks will rise. We advise investors to remain overweight Mexican risk assets relative to EM in cyclical and structural time horizons, but prepare for Mexican markets to sell off in absolute and relative terms in the next couple of months.

Mexico’s election and the US election pose short-term and potentially medium-term risks to Mexican financial assets. But unless the ruling party wins a double supermajority, we remain structurally overweight Mexico relative to global stocks excluding the United States.

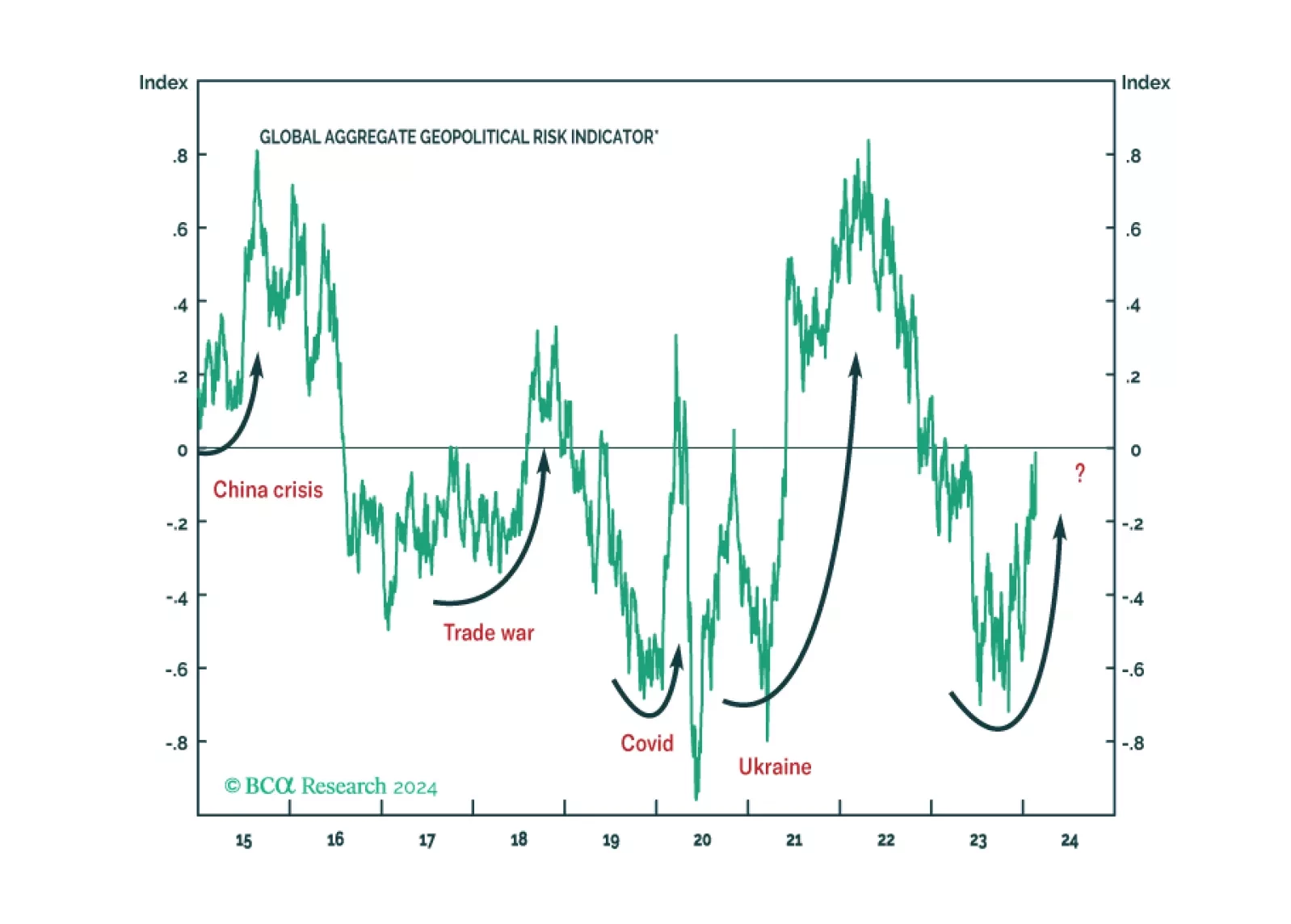

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.