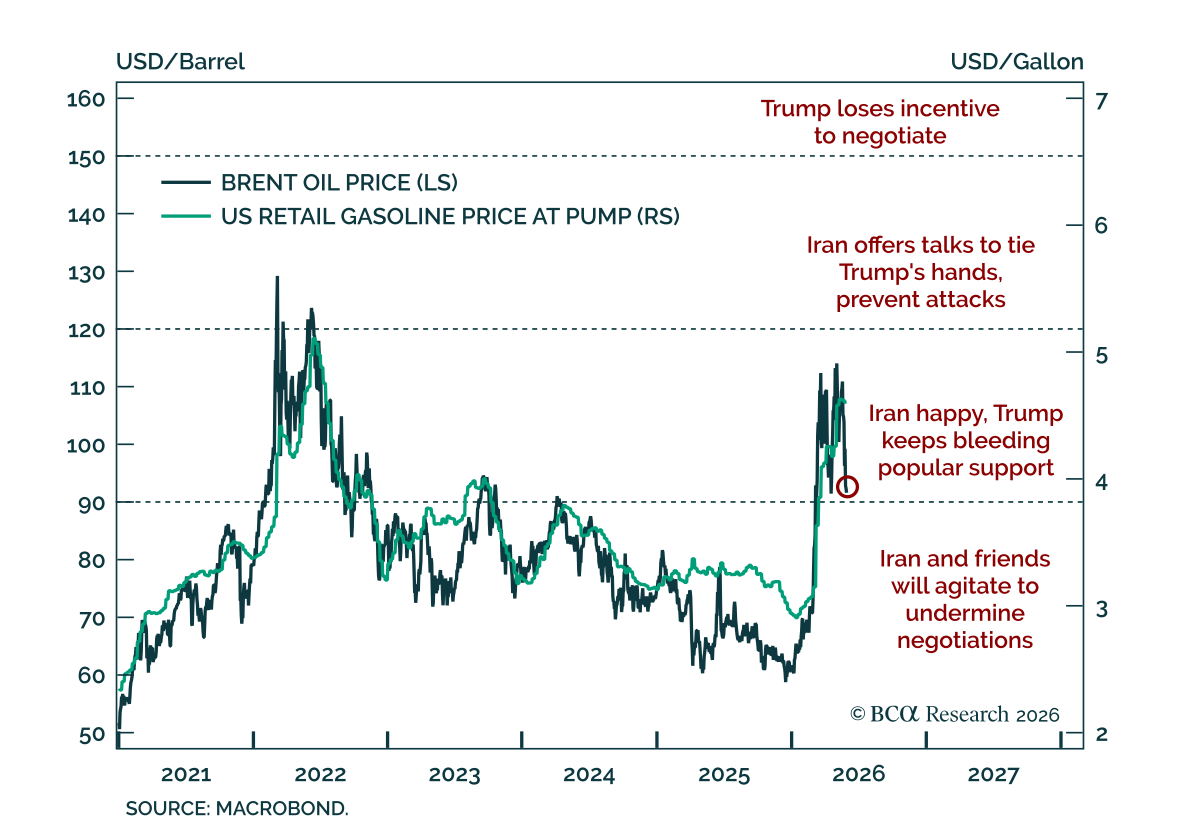

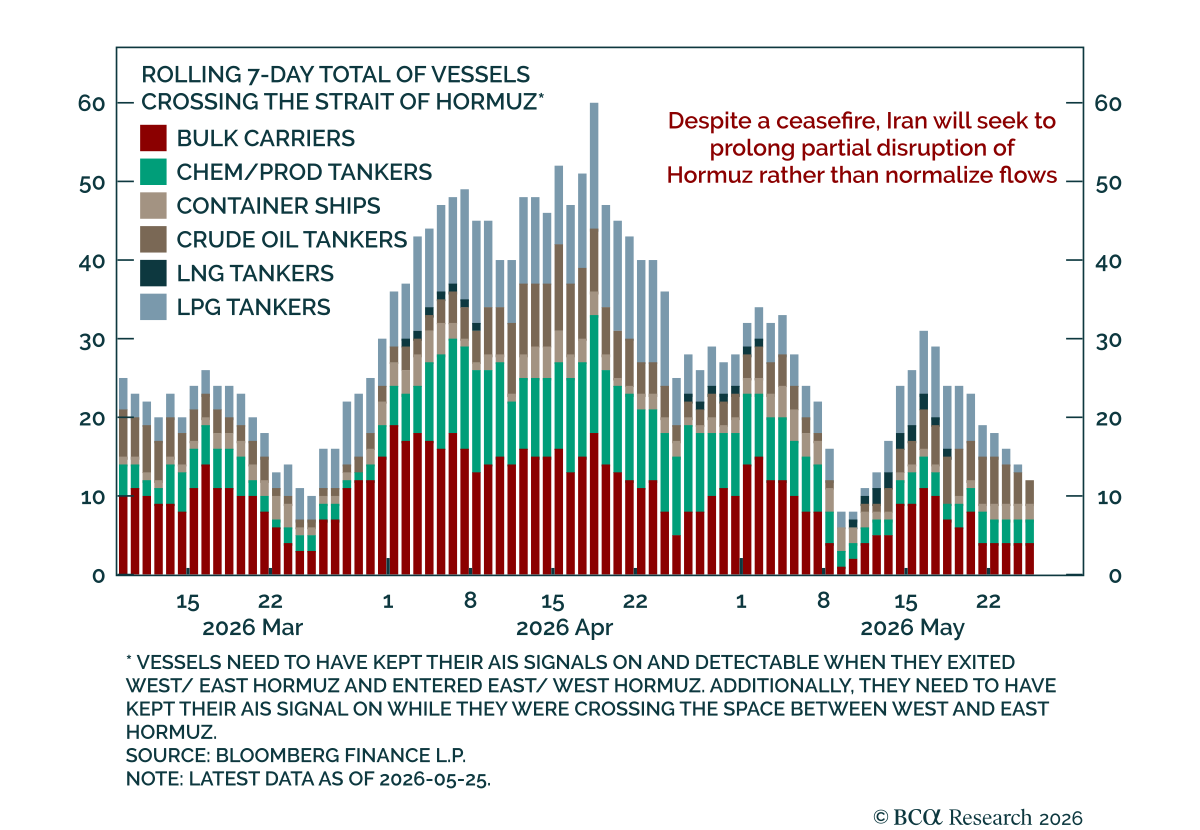

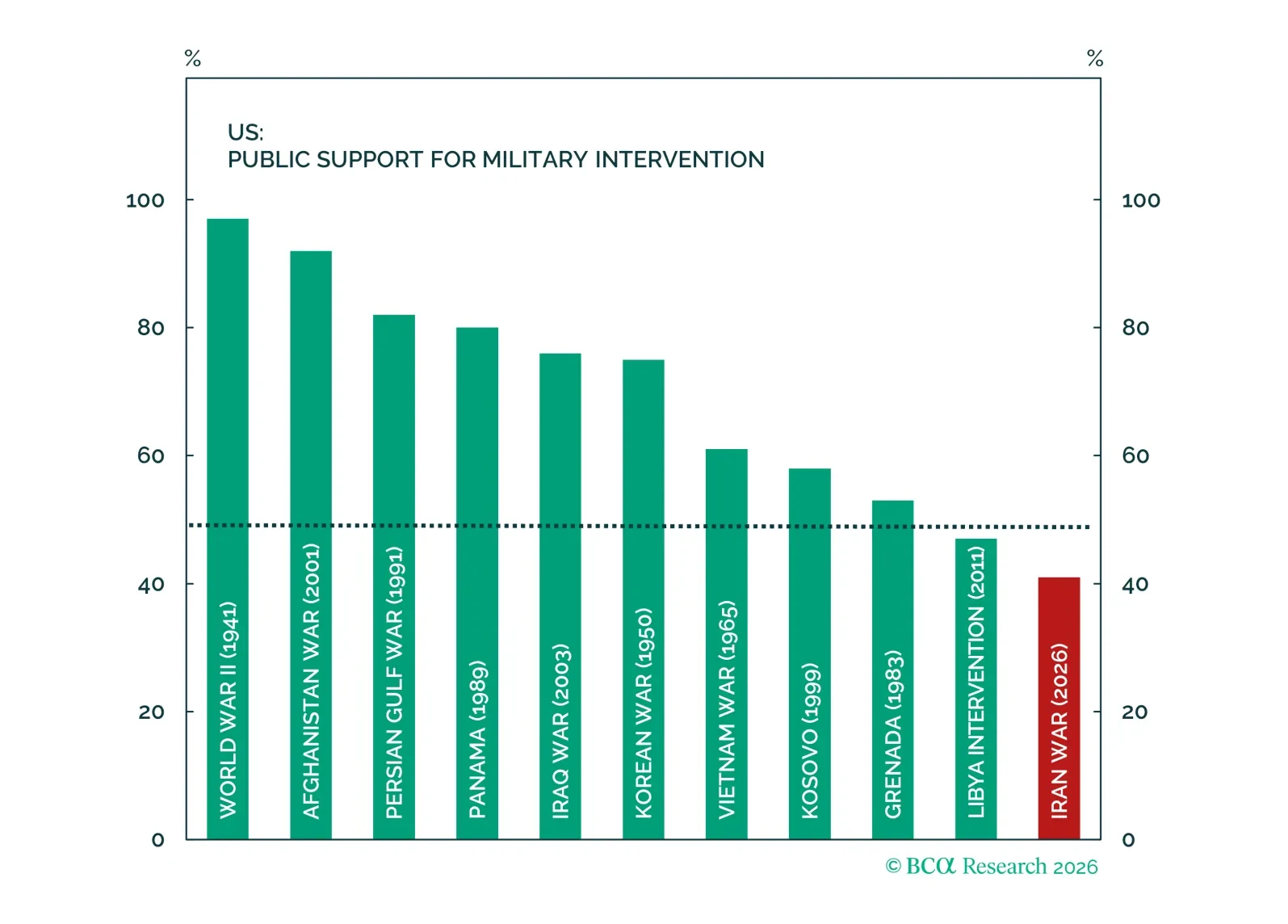

Iran

Midterms matter but geopolitics are the main risk this year. Markets will eventually refocus on geopolitical and inflation risks, raising Fed rate hike odds and supporting US dollar and stocks over global counterparts this year.

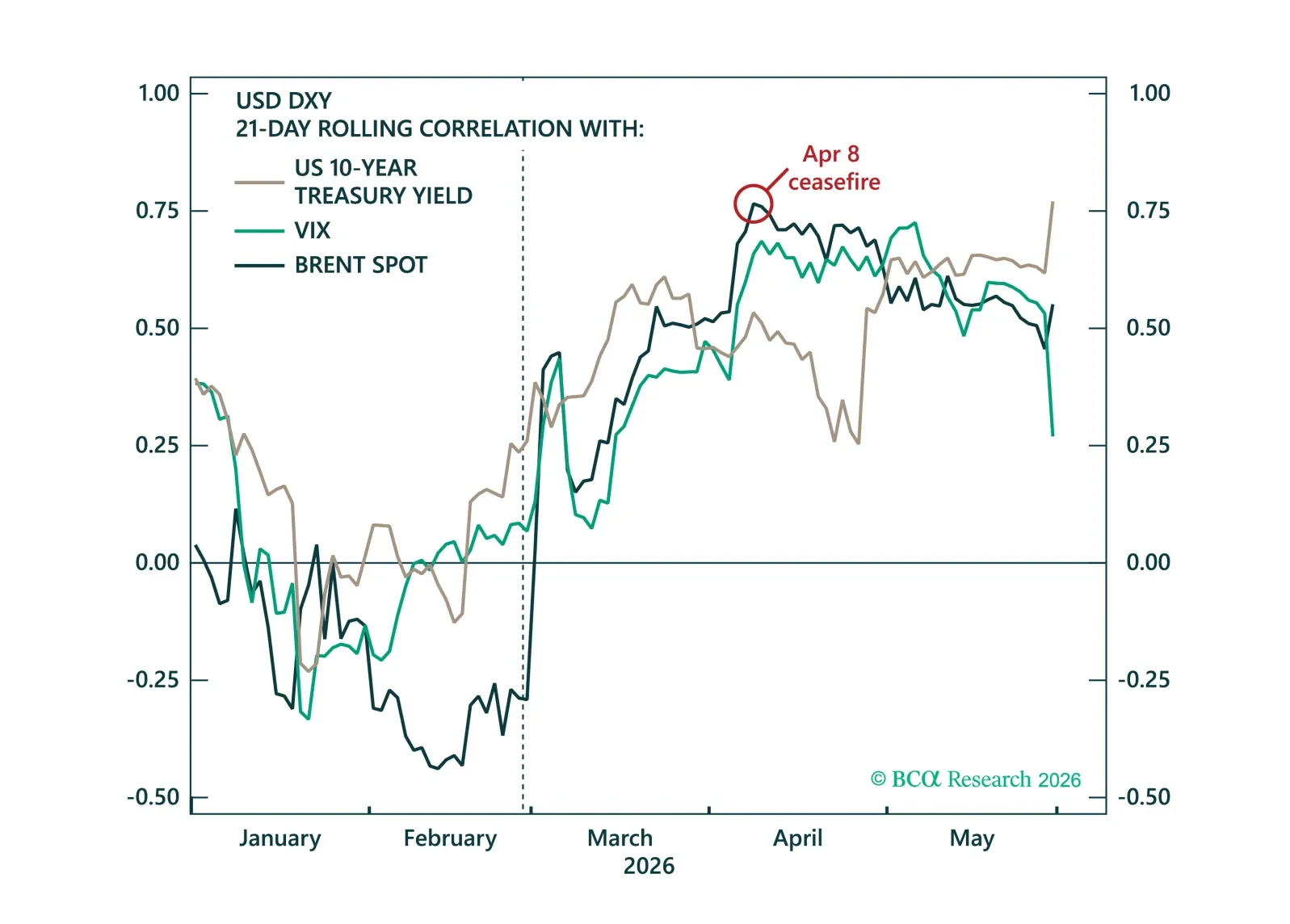

The dollar's muted response to the Iran conflict has led many to question its safe-haven appeal. We argue the opposite – the dollar's defensive properties have returned, while improving growth and rate dynamics should underpin further USD strength in the months ahead.

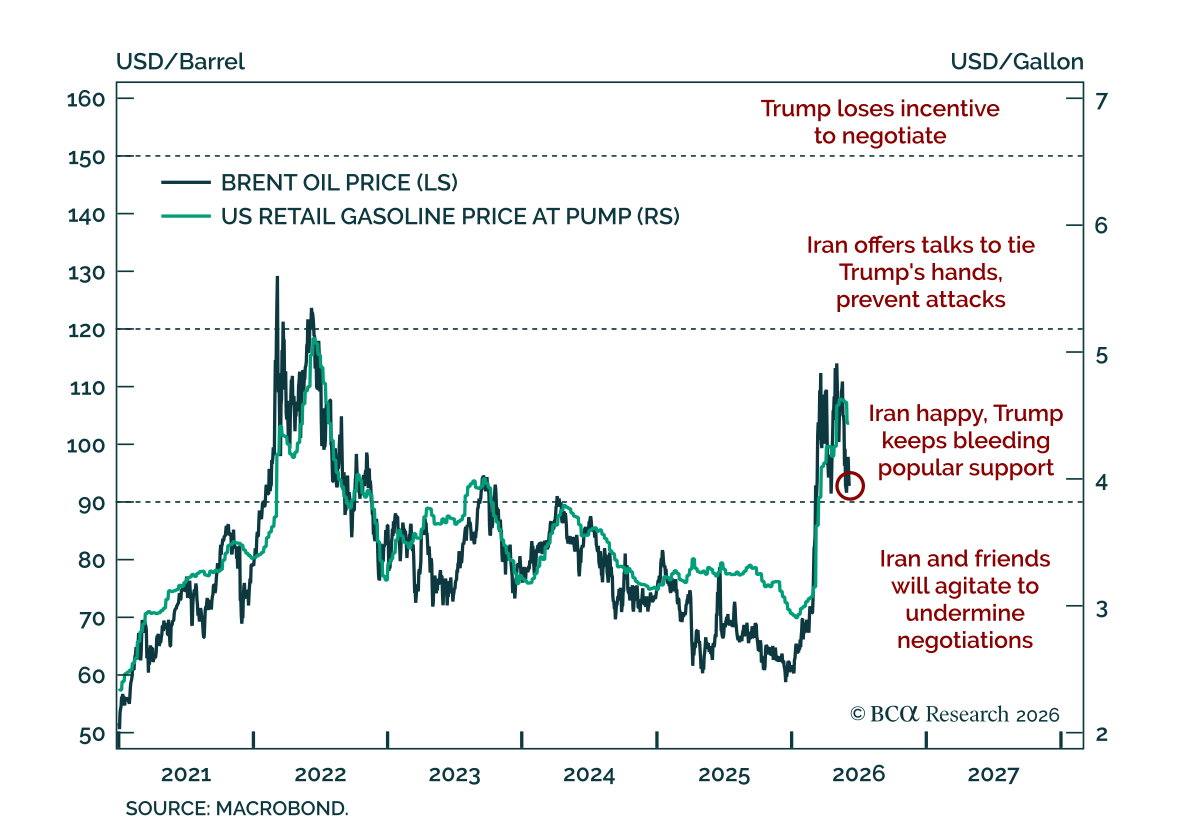

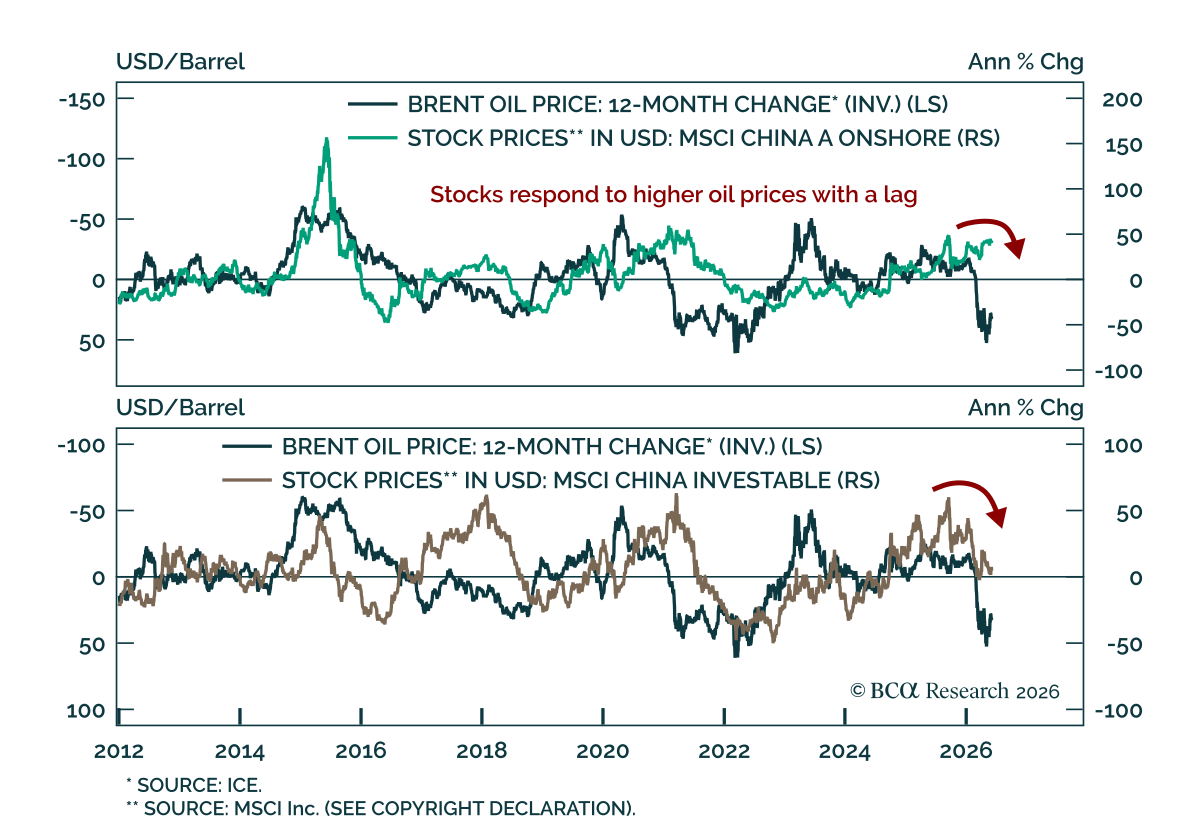

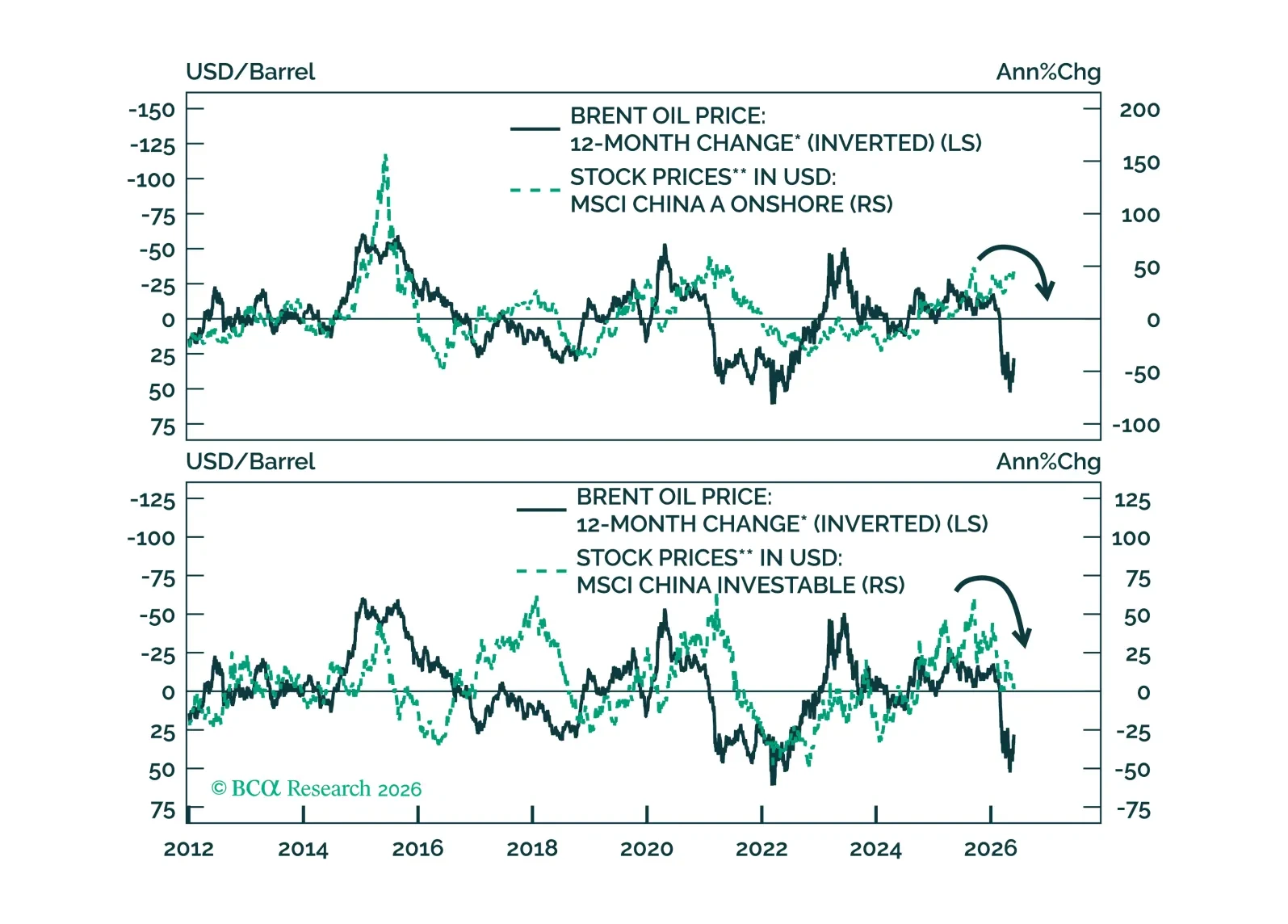

Oil shocks hit economies with a lag. China will feel the delayed pain of surging oil prices, pushing Beijing toward infrastructure spending as its main tool to prop up growth.

I spent the last week in London, speaking to a wide array of BCA Research clients. Throughout the early part of the week, well connected friends and sources in the Middle East warned me that a renewed US attack on Iran was imminent (by Friday, May 22, after the market close, bien sûr). Several clients with hefty AUM’s – and thus an impressive geopolitical consulting budget – in London confirmed that the US attack was all but assured.