Geopolitics

Feature “Bayesian: …statistical methods that assign probabilities or distributions to events…based on experience or best guesses before experimentation and data collection and that apply Bayes' theorem to revise the probabilities and distributions after obtaining experimental data.” — Merriam-Webster Dictionary Markets have reacted pretty rationally to the outbreak of the COVID-19 virus. Equities initially rebounded a few days ahead of the peak of new cases in China (Chart 1). But then, once the number of cases in the rest of the world started to accelerate, stock markets sold off again sharply. The MSCI All Country World Index is now down 13% from its peak on February 12. Recommended Allocation

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Chart 1Markets Have Reacted In Line With New COVID-19 Cases

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

No one knows whether this episode will turn into an unprecedented pandemic, which will kill millions worldwide, last for months, and trigger a global recession. So it is the sort of environment in which Bayesian analysis becomes useful. Our “prior” for the probability of a full pandemic would be around 10-20%. If it doesn’t happen, an attractive buying opportunity for risk assets should present itself soon. But there could be further downside first, especially if the number of cases in major countries such as the US, Germany, and the UK were to accelerate significantly. There are some sign that Chinese activity is beginning to recover. There are some signs that Chinese activity is beginning to recover, as new cases of COVID-19 slow, thanks to the draconian measures taken by the authorities. Big Data can help analyze this. For example, live traffic statistics from TomTom show that by February 28, weekday road congestion in Shanghai was back to 50% of its normal level, compared to 19% on February 14 (Chart 2). The Chinese authorities have relaunched fiscal and monetary stimulus, causing short-term rates to fall to their lowest level since 2010 (Chart 3). Monetary policy has been upgraded from “prudent” to “flexible and moderate.” BCA Research’s China strategists believe there is even an increasing possibility of a stimulus overshoot in the next 6-12 months, as the authorities plan for the worst-case scenario but the economy rebounds.1 Chart 2Chinese People Getting Back On The Roads

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Chart 3Chinese Stimulus Pushing Down Rates

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

In the short-term, it is clear that global growth will weaken, though quantifying this is hard. A 1% quarter-on-quarter decline in Chinese GDP in Q1 would bring growth down to 3.5% year-over-year. Our colleagues in BCA’s Global Investment Strategy estimate this would cause global growth to fall 0.8% below trend in Q1, mainly from a contraction in tourism, but that this would be largely made up in Q2, assuming that the epidemic is over by then (Chart 4).2 Could even a limited epidemic tip the world into recession? We doubt it. Consumer confidence remains strong in developed economies (Chart 5) and the virus is not yet serious enough to stop most consumers going out to spend. The global economy was in the process of bottoming out before COVID-19 hit (Chart 6) and there is little reason to think that we will not return to the status quo ante. Chart 4Global Growth To Slow In Q1, But Rebound In Q2

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Chart 5Consumers Remain Confident

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Chart 6Before COVID-19, Growth Was Bottoming Out

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

We see the two biggest risks being: 1) a rise in defaults in China, especially among smaller companies, that the government is unable or unwilling to prevent (Chart 7); and 2) a deterioration in the jobs market in the US, as companies start to postpone hiring, or lay off staff (Chart 8). We will watch these carefully over coming weeks. Chart 7Are Chinese Companies Vulnerable?

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Chart 8Is The US Job Market Starting To Wobble?

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Chart 9Markets Believe Trump Would Beat Sanders

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

There is one other risk that might give equity markets an excuse for a further sell-off: November’s US presidential election. The probability that Bernie Sanders wins the Democratic nomination has risen to 60% from 15% over the past two months. The consensus believes that Trump can easily defeat Sanders, which is why the President’s probability of being reelected has risen in tandem (Chart 9). But, if the economy starts to weaken and Trump’s approval rating slips, investors could become nervous about the likelihood of a market-unfriendly Sanders administration. We would not recommend long-term investors sell out of risk assets at this point. There could be an attractive buying opportunity over the next few weeks, and investors who have derisked should be looking for a reentry point. With US 10-year bonds yields at 1.2% and German yields at -60 basis points, it is hard to see much further upside for risk-free bonds. Equities should be able to outperform over the next 12 months, as growth rebounds following the COVID-19 episode. We have been recommending overweights in cash and gold, as hedges, since December, and these still make sense. However, if events over the coming weeks point to the risk of global pandemic being higher than we currently think, then investors should Bayesianally adjust and move more risk-off. Otherwise, a peak in COVID-19 cases ex-China should be a strong signal to buy risk assets again. Chart 10Why Should Long-Run Inflation Expectations Fall?

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Fixed Income: US Treasurys have become investors’ safe haven of choice over the past few weeks. A marked drop in long-run inflation expectations (Chart 10), in particular, has pushed the 10-year yield to a record low. This seems somewhat illogical, since the Fed will announce this summer the results of its review of monetary policy, which is likely to lead to a more dovish long-term inflation target (perhaps a commitment to achieve 2% on average over the cycle). The market has also priced in at least three Fed rate cuts by year-end (Chart 11). The Fed will certainly cut rates if US growth falters as a result of COVID-19, but this is by no means a certainty. History shows that Treasury yields jumped sharply once previous viral outbreaks ended (Chart 12). We expect yields to be significantly higher in 12 months, and so are underweight duration and prefer TIPS over nominal bonds. Credit will continue to underperform in the risk-off phase, but some interesting opportunities should arise soon, especially among the lowest-rated credits and in the Energy sector. Chart 11Will The Fed Really Be This Accommodating?

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Chart 12After Previous Virus Outbreaks, Rates Leapt

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Equities: The sell-off has already put on fire sale some stocks most affected by the epidemic. For example, cruise lines are down by 40% over the past month or so, European oil stocks 25%, some luxury goods makers 30%, and airlines 30%. Opportunistic investors might want to buy a basket of the most oversold quality names. Our overweight on euro area stocks has not worked in the sell-off. But, as a cyclical, export-oriented market, we continue to expect Europe to outperform when global growth rebounds. Euro area banks, in particular, represent the best call option on a rise in bond yields, since their performance is highly correlated to the shape of the yield curve. We continue to have a somewhat cyclical tilt among our sector weightings (with overweights on, for example, Energy and Industrials), but may adjust this in our Quarterly Portfolio Outlook in early April if we decide to reduce risk. The sell-off has already put on fire sale some stocks most affected by the epidemic. Currencies: The dollar is a safe-haven currency and so, unsurprisingly, has benefitted from the rush to safety in recent weeks. However, it remains overvalued (Chart 13), and interest rate differentials would move further against it if the Fed does cut rates, since other major developed central banks have much less room to move (Chart 14). This suggests that it will probably resume the weakness it experienced from August to December last year as soon as global growth rebounds. Chart 13Dollar Is Overvalued...

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Chart 14...And Interest Differentials Have Moved Against It

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Chart 15Metals Prices Stabilized In Recent Weeks

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Commodities: Industrial metals fell sharply on the outbreak of COVID-19 in China, but have bottomed in line with the stabilization of the situation in that country (Chart 15). Gold has worked predictably as the best hedge in the sell-off. While it is starting to look technically overbought and would be hurt by a rise in bond yields (Chart 16), for prudent investors it remains a useful hiding place amid heightened risk and ultra-low interest rates. Oil is the commodity that has fallen the most surprisingly, with Brent close to the low it reached during the sell-off in December 2018 (Chart 17). It is much less dependent on Chinese demand than metals are, and so is maybe pricing in a global recession – as well as questioning the commitment of OPEC to cut production further. This would suggest upside to the oil price if global growth turns out not to be so bad, oil demand continues to pick up, and supply remains constrained. Chart 16How Much Could Gold Overshoot?

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Chart 17Oil Discounting A Global Recession

Monthly Portfolio Update: A Classic Bayesian Dynamic

Monthly Portfolio Update: A Classic Bayesian Dynamic

Garry Evans, Senior Vice President Chief Global Asset Allocation Strategist garry@bcaresearch.com Footnotes 1 Please see China Investment Strategy Weekly Report, “China: Back To Its Old Economic Playbook?” dated 26 February 2020, available at cis.bcaresearch.com 2 Please see Global Investment Strategy Weekly Report, “Market Too Complacent About The Coronavirus,” dated 21 February 2020, available at cis.bcaresearch.com GAA Asset Allocation

Highlights We spent last week meeting with clients in South Africa, who maintained their equanimity despite the spread of the coronavirus: Maybe it was because there were not yet any reported cases close to home, but investors discussed the global outbreak dispassionately. We repeated our view that a US recession is not imminent, ex-a significantly adverse exogenous event: Tight monetary policy is a necessary precondition of a recession, and there’s no reason to expect that the Fed will make any move to remove accommodation in 2020. Investors were open to our view that the US economy is subject to upward inflation pressures, even if the time is not yet ripe for them to manifest themselves: Excess global capacity is still thwarting goods inflation, but it appears to be on its way to being absorbed. In the meantime, the Fed is deliberately encouraging the economy to run hot. Inflation just might surprise investors who have been lulled to sleep by its post-crisis absence. The presidential election is a hot topic in South Africa, too: The Democratic nomination appears to be Bernie Sanders’ to lose, and he has more of a chance in the general election than investors might expect. Feature We spent last week meeting with clients in South Africa. They expressed considerably more optimism about financial markets and the global economy than they did on our previous visit in January 2019, though we all conceded that the coronavirus outcome was unknowable. We discussed a wide range of topics, with COVID-19, recession prospects, the inflation outlook, and November’s election coming up in nearly every meeting. A summary of our discussions, organized by topic, follows below. Coronavirus Impressions We discussed the coronavirus at the beginning of every meeting, albeit after acknowledging that no one can know for sure how it will unfold. We discussed the virus’ potential outcomes, our base-case expectation, and the news and data we’re monitoring to track its course. Everyone is familiar by now with the best- and worst-case scenarios, and the continuum of possibilities in between, so we will not rehash them here. The main variables we have been watching – infection, mortality and recovery rates – are also surely familiar. From a review of those metrics within China – the daily rate of new incidences inside and outside of Hubei province (Chart 1), mortality (Chart 2) and recovery rates (Chart 3) within and without Hubei – there is good reason to conclude that China is gaining the upper hand, having sharply limited the virus’ spread beyond Hubei, and steadily slowing its spread in the epicenter. Chart 1Stringent Quarantine Measures Seem To Have Gotten Some Traction

Road Trip

Road Trip

Chart 2Mortality Rates Are Inconclusive, ...

Road Trip

Road Trip

Chart 3... But Recovery Rates Are Encouraging

Road Trip

Road Trip

Unfortunately, however, other countries cannot perfectly replicate China’s template for corralling the virus, as their governments have considerably less ability to limit their citizens’ movements. It is a lot easier to impose and enforce a quarantine or other emergency restrictions in China than it is in any other major country. It is important, then, to consider not just the number of countries to which the virus spreads, but the characteristics of the countries themselves. In this sense, Italy and Iran may offer some insight. The Italians reacted swiftly and decisively when the first cluster emerged in northern Italy. They drew a circle with a large radius around the cluster, restricted movement in and out of that circle, and sharply limited activities within it. Carnival celebrations in Venice were called off, and Sunday’s slate of matches in Italy’s Serie A professional soccer league were cancelled (subsequent matches are being played in empty stadiums). Although the number of reported infections in Italy has been rising, and infections have begun to pop up in western and central Europe, Italian officials appear to have both the ability and the will to contain it. The Iranian experience contrasts with Italy’s. In Iran, the mortality rate (deaths divided by confirmed cases) is roughly five times greater than it has been everywhere else the virus has erupted. That seems improbably high, and our best guess is that the infections denominator is being undercounted. A country that cannot provide a reliable count (or a reasonably accurate estimate) of infections presumably lacks the public health infrastructure to contain the virus. We conclude that it matters where the infections occur – the wealthy countries of western Europe, North America, Asia and Oceania likely have a better chance of bringing the virus to heel than developing countries. Our interactions in South Africa, among the wealthiest countries in the developing world, may further reinforce the point. In several meetings, clients asked what entering the country was like. I told them that when I arrived at the Johannesburg airport on the morning of Sunday the 23rd, all passengers from international destinations had to pass by a screener who pointed a clunky object shaped like a radar gun in the vicinity of their nose and forehead. Several planes had landed just before mine and the passport control line wound around three or four times, affording repeated opportunities to look over the radar-gun employee’s shoulder at the images on her screen. They appeared to be simple black-and-white video of the arriving passengers without any color imagery to indicate body temperature ranges. The clients uniformly laughed at that detail, exclaiming that of course the screening was ineffectual. They then soberly conceded that Africa is especially vulnerable to an outbreak. If the coronavirus or another severe adverse exogenous event doesn't do it, it will take restrictive monetary policy to induce a recession. Infections outside of China are rising with no end yet in sight (Chart 4), but the news isn’t all bad. There are some promising treatment developments that may yield effective therapies, either from the conventional drug that worked wonders on an infected patient in Washington State and is now being tested on infected groups in China, or from antibody-based therapies of the type that were successfully deployed against Ebola. Our own views are conditional upon COVID-19’s evolution, but our current base case is that it is more likely to produce a soft patch within the context of a global expansion, and a correction within the context of a continuing equity bull market, than it is to trigger a recession or a bear market. Chart 4Now It's The Rest Of The World's Turn

Road Trip

Road Trip

Recession Prospects Chart 5Necessary, If Not Sufficient

Necessary, If Not Sufficient

Necessary, If Not Sufficient

Nearly every client asked us about the prospects for a US recession. We discussed how the negative term premium had made the yield curve more prone to invert, thereby diluting its predictive value, and asserted our view that restrictive monetary conditions are a necessary precondition of recessions (Chart 5). We touched on the rest of the points covered in last week’s report, which argued that a strong near-term outlook for consumption, dependable government spending and a post-trade-tensions recovery in investment would keep the US out of recession over a 12-month horizon. But we spent the most time outlining what we see as the most likely route to the next recession. Expansions don’t die of old age, they die because the Fed murders them, and we told our clients that we expect that maxim will be especially apropos in this cycle. Investors should therefore focus on the factors that will prod the Fed to embark on a tightening cycle with the express intent of reining in an overheating economy. We see two main catalysts: concern that inflation may get away from the Fed on the upside (discussed in the following section), and/or concern that there are unsustainable excesses in either the economy or financial markets. Chart 6The Real Economy Isn't Close To Overheating

The Real Economy Isn't Close To Overheating

The Real Economy Isn't Close To Overheating

We contend that there are currently no signs of excesses in the real economy. Its most cyclical elements, which have driven overheating in the past, have not gotten back to their mean level, much less the red-line levels that have been associated with previous business cycle peaks (Chart 6, top panel). Proportional spending on consumer durables remains around the bottom of its 60-year range (Chart 6, second panel), investment in non-residential structures is quite low relative to history and comfortably in the middle of its post-1990-91-recession range (Chart 6, fourth panel), and residential investment is sitting at the level that previously marked business-cycle troughs (Chart 6, bottom panel). The only cyclical activity that looks a little frisky is equipment and software spending (Chart 6, third panel), which has the best chance of enhancing productivity and thereby yielding ongoing dividends. Financial market excesses are in the eye of the beholder, and reasonable people can disagree about their existence. The promiscuous application of the word “bubble” to anything and everything market related, however, has become as familiar and tiresome as rappers’ boasts of their prowess. The S&P 500’s steady climb higher doesn’t begin to approach the manic paths of prior decades’ hot assets (Chart 7). The key takeaway is that the economic or financial overheating likely to trigger the expansion’s ultimate denouement is yet to arrive. Until it does, the Fed will have no reason to intervene to stop it. Chart 7Which One Of These Is Not Like The Others?

Which One Of These Is Not Like The Others?

Which One Of These Is Not Like The Others?

Inflation Prospects Many clients asked about inflation prospects before we could bring up the subject, a notable turnabout from our last visit thirteen months ago, when our arguments for accelerating wage gains met mostly with indifference. We were happy to oblige, as inflation occupies an essential place in our base-case cyclical scenario. Tight monetary policy is a necessary precondition for an endogenously occurring recession. Ex-a severe exogenous shock, like a global pandemic, the expansion cannot end without tight monetary conditions, and the Fed won’t knowingly impose them unless it is concerned that inflation is getting away from it on the upside. Q: Why has there been no whiff of US inflation in the last eleven years? A: Because the negative US output gap rendered it impossible until 2018. We are not daunted by inflation’s post-crisis hibernation. Meaningful price increases at the level of the entire economy cannot occur when an economy has a negative output gap (aggregate demand persistently falls short of economic capacity) unless its currency is sliding and it imports a lot of goods and services. From that perspective, inflation has only been possible in the US since 2018, because it didn’t close its output gap until 2017, according to estimates from both the IMF and the CBO. 2018 was the year that the US embarked on an unprecedented macroeconomic experiment (Chart 8), injecting fiscal stimulus amounting to one half of the economy’s long-run capacity (about 100 basis points) at a time when it was already operating at full capacity (2-2.25%). If corporations and other businesses viewed the surge in aggregate demand as a one-off event that couldn’t be replicated in the future, they would likely choose not to invest in additional capacity to meet it. The net result was demand in excess of supply in 2018 and in 2019, when an additional 50 basis points of stimulus was deployed. Inflation did not break out in either year, but negative output gaps in the rest of the developed world provided the US with the convenient out of importing other countries’ excess capacity. Chart 82018's Unprecedented Macroeconomic Experiment May Yet Produce Inflation

2018's Unprecedented Macroeconomic Experiment May Yet Produce Inflation

2018's Unprecedented Macroeconomic Experiment May Yet Produce Inflation

The Bank of Canada estimated that Canada closed its output gap in 2018, and the IMF estimates that Europe’s output gap has now closed (Chart 9, top panel), and while even Japan has made a lot of progress on narrowing its output gap (Chart 9, bottom panel). Goods inflation is largely globally determined, and with excess capacity being absorbed around the world, it’s possible that the conditions that would allow for higher goods prices could soon lock into place. Services inflation, a predominantly domestic phenomenon, is poised to rise thanks to the tight-as-a-drum labor market. Just when inflation will rear its ugly head is uncertain, however, as it is a lagging indicator that often doesn’t peak, until a recession has nearly ended, or trough for nearly three years after a recession begins (Chart 10). Chart 9The Slack Is Being Absorbed

The Slack Is Being Absorbed

The Slack Is Being Absorbed

Chart 10It May Take A Long Time For 2018's Seeds To Germinate

Road Trip

Road Trip

We find supply and demand arguments compelling, and the excess-supply constraint on global goods inflation has quietly been easing. The bottom line is that we think the US economy harbors upward inflation pressures, though it is highly unlikely that they will manifest themselves this year. That will give the Fed free rein to allow the economy to run hot across all of 2020, in service of its primary goal of pushing inflation expectations higher, and the labor market as well, in service of its secondary goal of spreading the benefits of easy policy more evenly across the economy. The upshot is that the longer inflation remains outwardly dormant, the harder it will be to root it out once it eventually does begin to bloom. The World Is Watching American Voters As an indication of the anticipation surrounding November’s election, South African investors, who recognized Bernie Sanders’ name, asked about it in every meeting. We laid out our geopolitical strategists’ views, augmented in places by our own, on the key issues as follows: Presidential elections are referendums on the incumbent party. An incumbent president running for re-election has a sizable built-in advantage. In the postwar era, only major economic, social or international shifts have been sufficient to erode that advantage. Incumbents lose when a recession occurs near an election, but the president has to be considered a favorite if the expansion continues. The president may be an especially poor front-runner. Donald Trump personifies variability. That’s a great trait to have as an underdog, because a wide dispersion of individual outcomes broadens the range of possible competitive outcomes, but it’s a vulnerability for a favorite. It is nearly impossible for a golfer with a two-stroke lead ahead of the final par-four eighteenth hole to lose if s/he conservatively plays for par. It seems to us that the president is not wired to play conservatively, and our geopolitical strategists currently give him just a 55% chance of re-election. Bernie Sanders is not unelectable. Our geopolitical strategists note that the median voter is moving to the left, and that Sanders is many Biden supporters’ second choice. He may not be anathema to the broader public in the general election, and his leveling platform may play well in the Rust Belt states that are poised to decide the election once again. A Sanders administration would not transform America into France, but it would chip away at corporate profits. Our personal view is that a President Sanders would not mark the end of the US as a beacon of free enterprise. The Constitution was designed to obstruct dramatic changes, and his ability to pass major legislative initiatives is likely exaggerated. We think he could make his influence felt much more directly in the bureaucratic and regulatory spheres, where a president can act virtually unimpeded. A Sanders administration would be a devoted and presumably activist friend of labor, and a tenacious foe of corporate concentration. An administration that energetically champions organized labor and vigorously enforces anti-trust statutes would exert downward pressure on corporate profit margins. Bullish Or Bearish Borrowing a line from longtime Street economist and strategist Ed Yardeni, our mandate is bullish or bearish, not good or bad. We are charged with making objective decisions about what is most likely to occur in markets, not to daydream about what we would most like to happen. Our base-case scenario turns on our expectation that accommodative monetary policy will remain in place until well into 2021, and will continue to be effective in forestalling defaults and inflating asset valuations. It may not be the most comforting basis for being long risk assets, and we make no implied endorsement of its quality, but if we think it’s going to continue to work beyond the edge of the visible horizon, then we have to reiterate our recommendation that investors should remain at least equal weight equities in multi-asset portfolios, and at least equal weight credit in fixed income portfolios. Austrian adherents and self-styled monetary policy experts can howl about moral hazard and manipulation all they want, but we have to invest in the backdrop that we have, not the backdrop that we want. We do not yet see the approach of a catalyst that will prevent life insurers, pension funds, endowments and other investors who need yield from continuing to go further out the risk curve in search of it. And we don’t yet see the approach of a catalyst that will prevent equity investors from continuing to bid multiples higher. We remain constructive over the cyclical twelve-month timeframe. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com

Highlights It is too soon to bottom feed with fears of a global pandemic and “socialist” boom in the United States. China’s government will do “whatever it takes” to stimulate the economy – but animal spirits need to revive for it to work. European political risk and policy uncertainty are clearly on the rise, albeit from low levels. Bernie Sanders could become the presumptive nominee for president on Super Tuesday – if Biden fails to make a comeback. The market is underrating the Sanders risk to US equities – particularly tech and health. Assuming pandemic fears subside, the Fed put, the China put, and the Trump reflation put will fuel risk-on sentiment in H2 2020. Feature Chart 1Risk-Off Mood Dominates Markets...

Risk-Off Mood Dominates Markets...

Risk-Off Mood Dominates Markets...

Financial markets awoke to the confluence of negative news this year on February 20. The S&P 500 has fallen 8.0% from this year’s peak while the 10-year US Treasury yield dove to 1.33%. Gold reached the highest level since 2013. The yield curve inverted again (Chart 1). It is too soon to buy into the equity selloff. Fear of the coronavirus is spreading, not abating, while Vermont Senator Bernie Sanders – a democratic socialist who would turn the regulatory pen against corporations – is running away with the Democratic Party’s nomination for US president. Chart 2...Amid Fears Over Coronavirus And Sanders

...Amid Fears Over Coronavirus And Sanders

...Amid Fears Over Coronavirus And Sanders

The market selloff is well correlated with fear of the coronavirus, but there is also some correlation with Sanders’s success (Chart 2). This should intensify if Sanders becomes the presumptive nominee following “Super Tuesday,” March 3, by which time 39% of the Democratic Party delegates will have been chosen. Sanders poses a more systemic risk to corporate profits than the virus as he emblematizes a generationally driven sea change looming over US national policy: a shift from capital to labor. A greater tightening of financial conditions would prompt the Federal Reserve to cut interest rates, possibly as soon as its meeting on March 17-18. But the Fed is not yet signaling cuts. Also, cuts may not pacify the market as easily this time as in the last major pullback in Q4 2018. Tightening monetary policy was the culprit for that selloff and therefore the Fed’s policy reversal on January 4, 2019 gave the market just what it needed to rally. Today the Fed has no control over the causes: virus fears and “socialism.” President Trump is manifestly uneasy as the virus spreads. Anything that weakens the US manufacturing sector is a direct threat to his reelection, regardless of how he spins it. The statewide coincident indicators provided by the Philadelphia Fed show that Pennsylvania’s economy is deteriorating, while a relapse in Michigan will push it into the Democratic camp according to our quantitative election model. This would leave Trump with only Wisconsin standing between him and the shame of a one-term presidency (Chart 3). Chart 3Trump’s Narrow Victory At Risk Of Virus-Induced Slowdown

GeoRisk Update: Leap Year, Or Steep Year?

GeoRisk Update: Leap Year, Or Steep Year?

What can Trump do to feed the markets and economy some good news? Not much. The Democrats control the House of Representatives and will refuse any fiscal stimulus unless a total collapse is occurring, in which case Trump is doomed anyway. Given the strong dollar, the Fed’s reluctance to cut rates, and Trump’s paternalist proclivities, we can fully envision him attempting to strong-arm the Treasury Department into intervening against the dollar. But intervention would have a fleeting impact without Fed cooperation – and again, the economic crisis required for the Fed to intervene decisively would likely seal Trump’s fate regardless. What remains for Trump is his ability to enact surprise “rate cuts” of his own via tariff rollback on China. This is fully within his power. All he has to do is hold a phone conference with Xi Jinping and then declare that China is complying with the “phase one” trade deal in good faith and therefore deserves assistance amid the coronavirus economic shock. But the impact of a positive tariff surprise would be limited. And such rate cuts are likely to be reactive rather than proactive, as with the Fed. We shifted to a cautious, neutral stance on global risk assets on January 24 and we maintain that position. China is stimulating the economy, meaning that the dominant trend in H2 should be a global “risk on.” Thus we are keeping our China and emerging market trades open. But volatility will likely remain elevated through March, at minimum, given the toxic combination of a slowing global economy and an increasingly likely Sanders nomination. China Stimulus: "Whatever It Takes" Chart 4Xi Administration Is Getting Out The Big Guns

Xi Administration Is Getting Out The Big Guns

Xi Administration Is Getting Out The Big Guns

One near certainty of the coronavirus outbreak is that it will catalyze greater economic stimulus in China. Last year we argued that the trade war had derailed Beijing’s financial deleveraging agenda and hence that the risk of a stimulus overshoot was greater than an undershoot. The Xi Jinping administration limited the degree of reflation for most of the year, but by autumn it was incontrovertible: stabilizing growth and the labor market had taken priority over deleveraging. Local government bond issuance picked up and the government relaxed its grip on informal lending and the shadow banks (Chart 4). Now, with the coronavirus outbreak, the Xi administration is getting out the big guns. The People’s Bank of China has cut key interest rates below where they stood in 2015-16, the last major bout of stimulus (Chart 5), as our China Investment Strategy has noted. Beijing officials have announced they will dial up fiscal policy to build infrastructure and boost purchases of homes and cars. President Xi Jinping has personally assured the world that China will meet its economic growth target for the year. Compared with the 6.1% real GDP growth achieved in 2019, our China Investment Strategy believes a conservative estimate is 5.6% for 2020. Assuming China’s real GDP growth slows to 3.5% in Q1 on a year-over-year basis, China would need at least 6.3% average real growth year-over-year for the next three quarters to hit its target. This growth rate would be 0.3 percentage points higher than in the second half of 2019. Credit expansion and government spending in the next six-to-12 months would need to outpace that of last year. Will the government succeed in firing up demand? If getting back to work results in further outbreaks, then China may see greater difficulty in using its old-fashioned stimulus tools. Moreover Chinese households and corporates are more indebted than ever and have suffered a series of blows in recent years that have weighed on animal spirits: a political purge, slowing trend growth, corporate deleveraging, trade war, and now the virus. It is essential for consumer confidence and the velocity of money to keep recovering (Chart 6). Our Emerging Markets Strategy rightly insists that without a revival in animal spirits, stimulus will be pushing on a string. Chart 5Key Chinese Interest Rates Now Below 2015-16 Levels

Key Chinese Interest Rates Now Below 2015-16 Levels

Key Chinese Interest Rates Now Below 2015-16 Levels

Chart 6Animal Spirits A Precondition For Chinese Recovery

Animal Spirits A Precondition For Chinese Recovery

Animal Spirits A Precondition For Chinese Recovery

Yet it is also true that most of the negative shocks were policy decisions, especially deleveraging and trade war. With these decisions reversed – and likely to stay that way for at least this year – there is no reason to assume a priori that animal spirits will remain depressed. Furthermore, we see little room for the Xi administration to revert to tightening measures until a general economic recovery is well advanced. As we highlighted in our annual strategic outlook, it is necessary to stabilize the economy ahead of the 100th anniversary of the Communist Party in 2021 and – more importantly – the leadership reshuffle to take place in 2022. Chinese consumer confidence and the velocity of money need to recover for stimulus to have an impact. On a side note, Hong Kong is also implementing stimulus measures. This is positive for the city-state in the short run but it is unlikely to revive its fortunes over the long run. What made Hong Kong special was its position as a well-governed ally of the West during the heyday of globalization and the backdoor to mainland China during its rapid, catch-up phase of industrialization. Now globalization is slowing, Beijing is tightening central control, and the West has lost the appetite to defend its influence in Hong Kong. This influence is part and parcel with Hong Kong’s freedoms and privileges. This means that while the country’s equities can see a cyclical improvement we are structurally negative. Bottom Line: We are maintaining our cyclically constructive outlook on global growth and risk assets, as our view on China’s “Socialism Put” has been reinforced. We are keeping open our China Play Index and other EM trades. However, near-term risks are extremely elevated and our cyclical view could change quickly if the virus fear factor proves insurmountable for China and the global economy. China Sneezes, Europe Catches A Cold … And Its Immune System Is Weak Chart 7Our European GeoRisk Indicators Are Springing Back

Our European GeoRisk Indicators Are Springing Back

Our European GeoRisk Indicators Are Springing Back

The European economy was on track to rebound in 2020 prior to the coronavirus, but only tentatively, as sentiment and manufacturing were fragile. The virus struck at the heart of demand for European exports, China, and now is hitting European demand directly via the outbreak in Italy and across the continent. As fear of the virus spreads country by country, households and corporations will cut back on activity. It could take weeks or even months to resume business as usual. And it will take 6-12 months for China’s stimulus to kick in fully and lift demand for European goods. European political risk is thus no longer slated to remain subdued. Our indicators already show it is springing back. The most significant player is Germany, but Italy is the weakest link in the Euro Area, and non-negligible risks are affecting France, Spain, and the United Kingdom (Chart 7). German political risk will be highly market-relevant between now and the federal election slated for October 2021. De-globalization is a structural headwind for the German economy and Chancellor Angela Merkel’s attempt to stage manage a smooth succession has collapsed. The Christian Democratic Union is now plunging into a truly competitive leadership contest that will keep uncertainty elevated, at least until the aftermath of the election. Friedrich Merz is the leading contender (Chart 8) and is attempting to rope more conservative voters back into the Christian Democratic fold so that they do not stray into the populist Alternative für Deutschland (AfD). While a similar dynamic led the British Conservative Party into Brexit, German politics are less polarized than British politics. The Christian Democrats are nowhere near being overtaken by the far right. First, the CDU is still the most popular party and its closest competitors are the Green Party and the Social Democrats, while the AfD polls at 13.3% support and is opposed by all other parties. The AfD’s popularity, while growing, is still very small. Second, a majority of the public still approves of Merkel (Chart 9), signaling a tailwind for centrists within and without her party. Chart 8Merz Is The Top Contender In Germany’s Leadership Contest

GeoRisk Update: Leap Year, Or Steep Year?

GeoRisk Update: Leap Year, Or Steep Year?

Third, the German public is still the most supportive of the euro and EU, for the obvious reason that its economic success is integrally bound up in the union (Chart 10A). Nor is Germany alone, since the only country that looks truly concerning by these measures is Italy and even Italy’s populists remain engaged in the European project (Chart 10B). Chart 9Merkel's Popularity A Sign Of German Centrism

Merkel's Popularity A Sign Of German Centrism

Merkel's Popularity A Sign Of German Centrism

Chart 10ASupport For The Euro Still Strong (But Watch Italy) (I)

Support For The Euro Still Strong (But Watch Italy) (I)

Support For The Euro Still Strong (But Watch Italy) (I)

Chart 10BSupport For The EU Still Strong (But Watch Italy) (II)

Support For The EU Still Strong (But Watch Italy) (II)

Support For The EU Still Strong (But Watch Italy) (II)

Immediate economic challenges favor Merz’s bid to lead the party. However, if they do not give way to an economic rebound by fall 2021 (i.e. if Chinese and global growth worsen in the lead-up to the general election), then these challenges will undercut the Christian Democrats’ bid to remain in power regardless of whether Merz or a more dovish chancellor-candidate emerges from Merkel’s exit. The Green Party offers a viable alternative to lead the next government. Chart 11Coronavirus Will Weigh On France's Tourism Sector And Macron's Popularity

Coronavirus Will Weigh On France's Tourism Sector And Macron's Popularity

Coronavirus Will Weigh On France's Tourism Sector And Macron's Popularity

In the short run, Germany can ease fiscal policy marginally to help offset the current slowdown. But a game changer in fiscal policy will require either for the current economy to collapse or a resolution to the succession crisis. Finance Minister Olaf Scholz, of the Social Democrats, has just proposed a significant revision to the schuldenbremse, or “debt brake,” which keeps budget deficits pinned above -0.35% of GDP. He would allow Germany’s state and local governments to suspend the debt brake temporarily so as to boost fiscal spending to mitigate the slowdown. A formal suspension requires a constitutional change that would in turn require a two-thirds vote in both houses of the legislature. There are enough votes in the Bundestag and possibly in the Bundesrat but it requires the economic shock to get bigger first so as to force the conservatives to capitulate and court the help of smaller parties. Otherwise Scholz is making an election gambit to distinguish the Democratic Socialists from the fiscally conservative Christian Democrats. In the meantime, limited moves to loosen the belt are perfectly countenanced by existing law which allows for deviations from the debt brake during recessions and emergencies. France is also seeing a spike in political risk. President Emmanuel Macron has slogged through the massive labor strikes against his pension reform, as we expected. The reform would streamline a complex web of pension programs into a single national program, providing incentives for workers to work longer without making spending cuts. It will likely pass into law through his En Marche party’s control of the National Assembly. However, Macron’s political capital is spent and his party is expected to sustain heavy losses in municipal elections from March 15-22. The service-oriented economy will also suffer a blow from reduced tourism amid the coronavirus scare (Chart 11), further eroding Macron’s already low popularity. The loss of influence at home will reinforce Macron’s pivot to foreign policy. Macron can play the leader of Europe at a time when the UK is leaving and Germany is consumed with a leadership contest. In this role he will clash with the UK over Brexit and the US over trade – but this can only go so far given the need to sustain the French economy. Negotiations with the UK will involve brinkmanship but will result in a delay of the end-of-year deadline, or a deal, given the fragile economic backdrop affecting all players. Economic constraints also imply that negotiations with the US will not spiral into a major confrontation unless and until Trump is reelected. Therefore Macron’s gaze will turn to security and immigration, challenges that have the potential to fuel anti-establishment sentiment that could hurt him in the French election of 2022 and undermine his vision of a more integrated Europe. While terrorism has abated for the time being (Chart 12), the trend cannot be guaranteed. The Middle East is extremely unstable amid the global slowdown, virus, drop in oil prices, and general destabilization emanating from the underlying US-Iran conflict. Immigration is also starting to rise again, particularly along the western North African route into Spain and France that bypasses the fighting in Libya (Chart 13). Chart 12A Pickup In Terrorism Would Fuel Populist Sentiment...

A Pickup In Terrorism Would Fuel Populist Sentiment...

A Pickup In Terrorism Would Fuel Populist Sentiment...

Turkey’s foreign policy confrontation with the West threatens an increase in immigration in the east as well as a Turkish client-state in western Libya that France fears could become a militant safe haven. Chart 13...As Would An Increase In Immigration

...As Would An Increase In Immigration

...As Would An Increase In Immigration

France is therefore taking a harder line with Turkey and providing maritime assistance to Greece (see Chart 13 above). The Mediterranean is becoming a geopolitical hot spot that could lead to negative surprises – and not only for Turkish assets. European populism is under control for now but a new wave of immigration would spark a new wave of populism that would increase policy uncertainty and the risk premium in equities. Italy has shifted from being an overstated to an understated political risk. Chart 14Italian Right-Wing Parties Are Gaining Strength

Italian Right-Wing Parties Are Gaining Strength

Italian Right-Wing Parties Are Gaining Strength

Politically, Italy remains the weakest link in Europe – and this long-term risk is now becoming more pressing. Support for the euro and EU is among the weakest (see Chart 10 above). The ruling coalition is rickety and groping toward an election, with a popular referendum on the electoral law dated March 29. The country is poorly equipped to handle the virus outbreak. The virus will also call attention to the porous borders, fueling anti-establishment sentiment – after all the anti-establishment League is still the top party in polls while the right-wing Brothers of Italy’s support is surging (Chart 14). This is the case even though immigration into Italy is under control at the moment, particularly with renewed fighting in Libya discouraging flows through the central North African route. In short a full-fledged recession will unleash the furies in Italian politics and the country has shifted from being an overstated to an understated political risk. Bottom Line: The UK-EU trade talks threaten volatility for the pound this year, on top of the key continental risks: succession crisis in Germany, the potential for Macron’s centrist political movement to falter in France, and the possible election of a right-wing anti-establishment government emerging in Italy. Populist sentiment can emerge from the economic slowdown even if terrorism and immigration remain contained, but the recent uptick in immigration and new sources of instability in the Middle East, North Africa, and the Mediterranean show clouds gathering on the horizon. The Euro Area’s fiscal thrust is expected to be a measly 0.015% of potential GDP in 2020. The trends above suggest that this number could increase substantively, albeit reactively, due to fiscal easing in Germany and several other states along with France’s lack of real cuts in its pension reform. United States: Can A Northern Progressive Win In The South? In February 1980, Democratic presidential contender Jimmy Carter won the New Hampshire primary with 51% of the vote. Carter would go on to become the first Democrat from the Deep South to win the presidency since Woodrow Wilson. His triumph in New Hampshire proved, as he said, “that a progressive southerner can win in the North.” Fast forward to February 2020 and Vermont Senator Bernie Sanders, the most left-wing candidate vying for the nomination, is attempting to perform the equally dazzling feat of winning a primary election in the conservative southern state of South Carolina. If Sanders pulls it off then it will trigger an earthquake. For a progressive who can win in the South is likely to score big on Super Tuesday, March 3, and if Sanders pulls that off then he will become the country’s first “socialist” presumptive nominee for president (Chart 15). This would be a huge upset, primarily for former Vice President Joe Biden, who has long led the opinion polls in South Carolina and recently has even rebounded. Biden expects strong support from the African American community – which is staunchly Democratic, moderate in ideology, and favorable toward Biden due to his close association with former President Barack Obama. The problem is that Biden’s latest rebound in the polls may be too little, too late. He made more gaffes in the debate performance and, most importantly, Sanders’s polling has improved among African Americans (Chart 16). Chart 15A Sanders Win In The South Will Help Him Score Big On Super Tuesday

GeoRisk Update: Leap Year, Or Steep Year?

GeoRisk Update: Leap Year, Or Steep Year?

Chart 16Sanders’s Polling Has Improved Among African-Americans

GeoRisk Update: Leap Year, Or Steep Year?

GeoRisk Update: Leap Year, Or Steep Year?

Sanders performed well with almost every demographic in Nevada – if he can do well among blacks, and in the south as well as the north and west, then his ability to unify the party will be incontrovertible and moderate Democratic primary voters looking for a winner will start to resign themselves to his nomination. What is more likely is that Biden wins in South Carolina, declares himself the “comeback kid,” and prolongs the uncertainty regarding the Democratic nomination. Chart 17A Biden Win In Texas Would Reenergize The Establishment

GeoRisk Update: Leap Year, Or Steep Year?

GeoRisk Update: Leap Year, Or Steep Year?

If South Carolina propels Biden to a strong performance on Super Tuesday, particularly a win in Texas, it could usher in a new phase of the primary election since it would suggest the possibility that the establishment has not lost the nomination and is striking back against Sanders (Chart 17). Failing that, any “Never Sanders” movement will face an uphill battle. After March 3, about 39% of the Democratic Party’s delegates will be “pledged,” or committed, to one of the candidates. Two weeks later, fully 61.5% of delegates will be chosen. Which means that the best chance for a conservative counter-revolution against Sanders comes over the next three weeks. Regardless of South Carolina, Biden’s structural limitation on Super Tuesday is the well-known phenomenon of vote-splitting. Five centrist candidates are dividing the moderate vote, leaving Sanders to engross the 40%-45% of the vote that is progressive all to himself.1 This is a compelling reason to believe that Sanders will continue to amass the most delegates. What would change the equation would be a mustering of the centrists under a single competitive candidate. The latter requires candidates to be forced out of the race through defeat or to drop out of the race willingly for the good of the party. If Mayor Pete Buttigieg or Senator Amy Klobuchar should fall short of the 15% to qualify for delegates in South Carolina, they would need to bow out of the race (they might be persuaded by promises of high appointments). Most importantly, if Biden should squander South Carolina then he would need to take one for the team and drop out, passing the baton to Bloomberg. It will be hard for any one of these politicians to quit unless it is coordinated with the others; he or she would have to forgo any hopes of emerging at the top of the ticket at a contested Democratic National Convention in July. If coordination fails, the centrist vote will become even more fragmented when Mayor Michael Bloomberg finally appears on the ballot on March 3. Last week we argued that if Sanders cannot clinch the nomination by winning a majority of the delegates by June, then he needs to win a commanding plurality of the delegates so that moderate unpledged delegates are forced to capitulate and vote for him at the Democratic National Convention. We argued that for this to happen he needs, at minimum, to improve upon his score in 2016, which was 43% of the popular vote and 40% of the delegate count. Otherwise, a sequential voting procedure among roughly equally weighted blocs will likely lead to his defeat, as the two other factions of the party (establishment Washington insiders like Biden and centrist Washington outsiders like Bloomberg) view Sanders-style socialism as their least preferred option. Is this 40%+ threshold enough? Nobody knows. Clearly it is harder to win the nomination with 40% of the delegates than with 49%, even if you are in first place. But if Sanders leads by double digits in terms of the share of delegates, has captured 43%+ of the popular vote, and has won the big swing state primaries across regions, then it will be hard for Democratic delegates to conclude that he is not the most competitive in the general election. Currently Sanders is slated to win California, Michigan, Wisconsin, Pennsylvania, Ohio, and possibly Texas. This is a strong argument for moderate unpledged delegates to swing behind him. It is even compelling for some of the Democratic Party’s “super delegates,” at least those who are wavering. Otherwise these party elders would break up an enormous amount of momentum in the name of a less popular Democratic candidate – and strengthen Trump. Bottom Line: Super delegates will vote as political actors facing constraints inherent in their situation. If the situation is that Sanders has won 43% of the vote, leads the next candidate by double digits, has won the most primary elections, and has won in the major states, including the swing states, then it will be a compelling constraint on voting against him. Investment Conclusions The daily new cases of the coronavirus outside China continues to surge, creating near-term headwinds for global risk assets. Ultimately the negative shock of the virus may be overstated, but we remain on the sidelines of any near-term equity rally due to the confluence of a global demand shock and a US socialism boom. With manufacturing already vulnerable, the coronavirus, insofar as it causes a harder hit to global and hence American manufacturing, is a threat to Trump’s reelection odds. This is true regardless of who takes the Democratic nomination. It is also true notwithstanding that pandemic risks may ultimately fuel xenophobic sentiment. Trump cannot argue his way out of rising unemployment in the Rust Belt. The market is underrating the Sanders risk to health care and technology stocks. This means that Sanders has a greater chance of winning the White House than the consensus holds. Financial markets should continue to discount his rising odds, at least until it becomes clear either that he is falling short of a strong plurality or that the global economy is shaking off its jitters. As the financial market stumbles Sanders will get more steam than other candidates, while Trump’s odds will suffer, which is a potentially self-reinforcing dynamic. Looking at the correlations between different candidates and US equity sectors, the market is underrating the Sanders risk to health care and technology stocks (Table 1). Sanders poses a threat to regulation in these spheres even if the Democrats do not take a majority in the Senate. And they are likely to take the Senate and have a one-seat majority in the event that they prove capable of ousting Trump (via the vice president). Table 1The Market Is Underrating The Sanders Risk To US Equities

GeoRisk Update: Leap Year, Or Steep Year?

GeoRisk Update: Leap Year, Or Steep Year?

Ultimately Trump’s reelection also represents a threat to the tech sector, due to a “Phase Two” trade war, but the initial market reaction is likely to be risk-on. Assuming our base case that the virus fear eventually subsides, people get back to work, the world economy regains its footing, and monetary and fiscal stimulus get pumping (especially in China), the swing state economies may well be banging by November. In that context, the three pillars of our bullish 12-month view will be restored: the Fed put, the China put, and Trump’s reelection as a “buy the rumor, sell the news” phenomenon. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 This assumes Senator Elizabeth Warren of Massachusetts continues to fall short of the 15% threshold qualifying a candidate to receive pledged delegates to the Democratic National Convention. Appendix Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

UK

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Canada

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

China

China: GeoRisk Indicator

China: GeoRisk Indicator

Taiwan

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Section III: Geopolitical Calendar

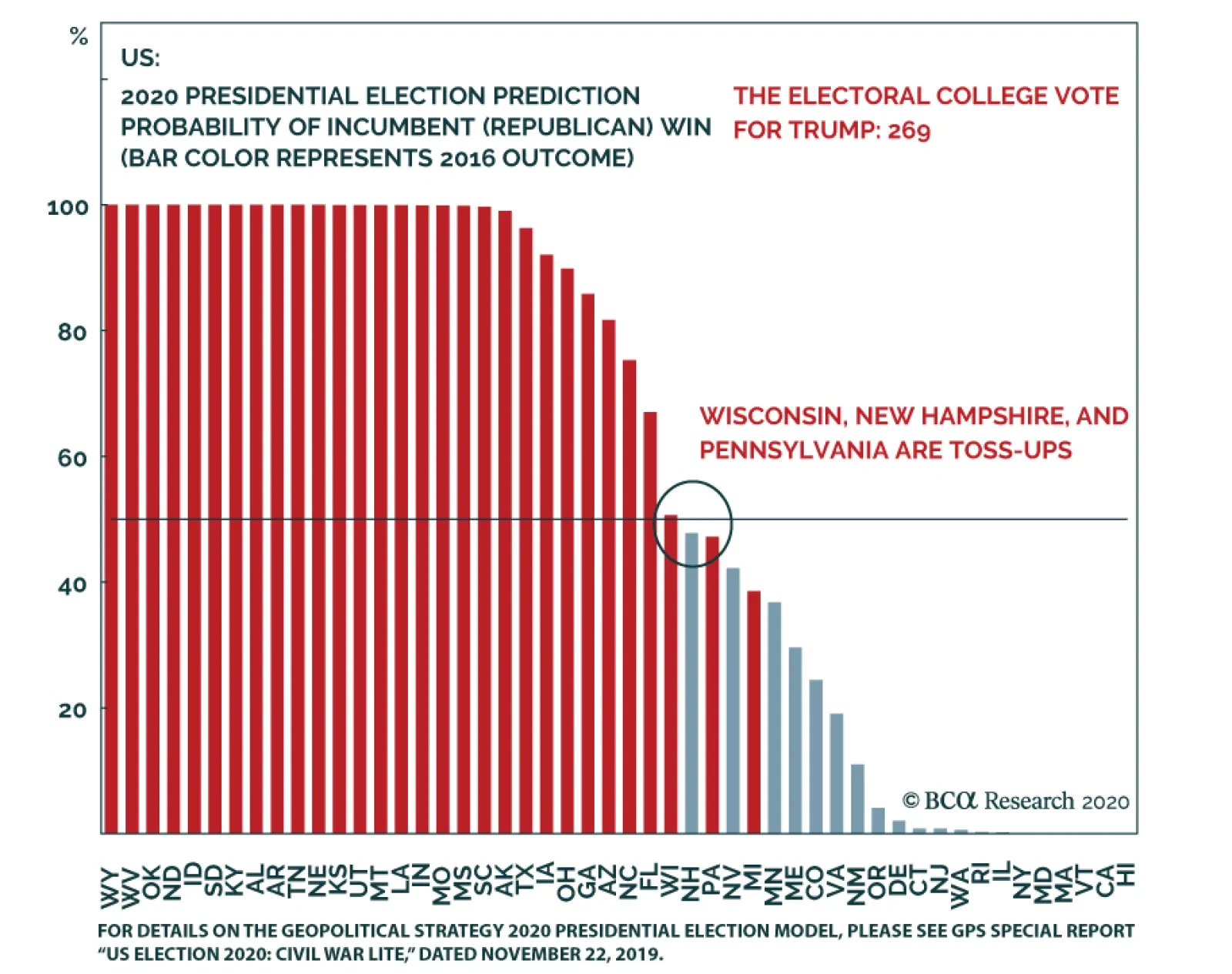

Highlights Expect more volatility in the near-term. The roughly 45% odds of a total US policy reversal in the November election are higher than the market expects. A “Gray Swan” event in the election would be a tie in the Electoral College at 269 versus 269 votes. While Trump would win in this scenario, the process is arcane and the election’s legitimacy would be challenged. Feature Constraints suggest the Democratic Primary nomination will go to a moderate candidate, but only if Bernie Sanders falls short of a strong plurality (~40%) of the vote. Currently, Sanders has momentum, so the risk is that he wins just such a plurality. The world remains spellbound by the risk that the coronavirus outbreak in China will cause a substantial slowdown with knock-on effects. We maintain a cautious stance toward risk assets in the near term in order to get clarity that the virus is indeed being contained. Our latest analysis of the virus impact can be found here and here. Our analysis of the impact on Chinese politics and policy — and forthcoming economic stimulus — can be found here and here. Meanwhile we continue to focus on the US election cycle — which threatens additional volatility both in the immediate term and in Q4. An Electoral College Tie?!? Our expectation that President Trump is slightly favored to win the election hasn’t changed, but our quantitative election model continues to signal that the race is “too close to call.” Specifically it awards Trump with the narrowest possible Republican victory in November. It suggests the president will lose Maine, Michigan, and Pennsylvania, yet keep Wisconsin (Chart 1). Chart 1Our Quant Model Signals That The Race Is "Too Close To Call"

An Electoral College Tie?!?

An Electoral College Tie?!?

The intriguing thing about this combination of states is that it would produce an Electoral College tie, with the Republicans and Democrats each winning 269 votes! While the model generally should not be read so literally — the correct reading is “too close to call” — nevertheless a tie combination is not far-fetched and therefore constitutes a “Gray Swan” risk for this year: a high impact event whose probability is not all that low. The demographic data that we use to project the size and composition of the American voting public in 2020 — provided by the Center for American Progress and a coalition of high-powered Washington think tanks — provides at least one specific election scenario in which such a tie would result. This is a scenario in which the voter turnout and party support rates remain the same as in 2016 yet the elevated 5.7% of votes that went to third party candidates that year reverts back to its historical mean of 1.7%, where it stood in the 2012 election (Chart 2).1 A repeat of the 2016 election with third-party mean-reversion is not implausible. In 2020, President Trump still has a relatively weak approval rating, while none of the Democratic candidates is particularly charismatic or inspiring for key voting groups like African-Americans. (Charisma or a special demographic advantage are factors that could increase Democratic turnout and support from Hillary Clinton’s 2016 levels.) This year’s contest is a “closed election” with an incumbent president running, while 2016 was an “open election” in which voters had greater ability or willingness to flirt with parties outside the Republican-Democratic duopoly. Democratic candidate Hillary Clinton polled as the least favorable candidate in history at that time, with the sole exception of her rival, Republican candidate Donald Trump. The economy was also soft. A symbolic or strategic vote for the Libertarian Party or Green Party seemed a better option for about 6% of voters. Trump would be re-elected in the event of a tie. How is the presidency decided in the event of a tie? The House of Representatives votes to choose the president, albeit with each state only getting one vote. Currently Republicans have a majority in more congressional state delegations than Democrats — even if Pennsylvania is allotted to the latter (Chart 3). As a result President Trump would be re-elected. Chart 2A Tie In The Electoral College Is A "Gray Swan" Risk

An Electoral College Tie?!?

An Electoral College Tie?!?

Chart 3Trump Would Be Re-Elected In The Event Of A Tie

An Electoral College Tie?!?

An Electoral College Tie?!?

Needless to say, the American public is not familiar with the details of the twelfth amendment governing this process and there would be much heartburn from the losing party. The Democrats would highlight the popular vote (which Trump is highly likely to lose in most scenarios) and the “unrepresentative” nature of both the Electoral College and the House voting procedure. Such complaints would be ineffectual but the outcome would trigger a “legitimacy crisis” that would weaken the government’s mandate and exacerbate the country’s extreme polarization. Partisanship and polarization would also shoot through the roof if extremely thin margins of victory resulted in contested election results. Indeed the outcome of the election may not be clear on November 3. The 2000 election, the last time prior to 2016 that the Electoral College and popular vote produced different results, is the obvious example. President George W. Bush won by carrying Florida with 537 votes, but only after the Supreme Court intervened to put a stop to the contested recounting process in the state. President Trump won the critical swing states of the 2016 election by larger margins than that, but they were still thin and his net negative approval rating suggests thin margins could occur again in 2020 (Chart 4). Democratic contender Al Gore did not concede the election till a month later — would populist candidates like President Trump or Senator Bernie Sanders concede their loss? What would they do if the voting system somehow malfunctioned? The reporting debacle at the Democratic Party’s Iowa Caucus this month should serve as a reminder that voting systems are vulnerable to flaws and failures. Chart 4Trump’s Thin Margins In Swing States Could Occur Again In 2020

An Electoral College Tie?!?

An Electoral College Tie?!?

Even more controversial and polarizing, the Electoral College could swing because of the rogue actions of individuals. There can be no confidence in any prediction of a 269-269 Electoral College tie because college members are not always legally bound to vote for the candidate who carried the state they represent. “Faithless electors” are those who vote according to conscience rather than the strict mandate of their state. There were seven faithless electors in 2016, five of whom defected from Clinton and two of whom defected from Trump. In an election with tight margins in the Electoral College, it is conceivable that half of the population could be deprived of its democratic rights by the actions of a few individuals. There is a justification for the independence of electors but the point is that if they swung the election the results would be illegitimate in the eyes of around half of the country. In sum, the US election is shaping up to be extremely close, which means that frictions in the electoral system are likely to emerge. Thin and contested vote margins — or constitutional yet “unrepresentative” solutions to disputes — may deprive the government of legitimacy in the eyes of many and prolong America’s crisis of polarization. While financial markets expect a clear answer on November 3, they may not get it. Uncertainty may go up instead of down. Extreme polarization also has negative effects like abrupt vacillations in national policy — see the Iraq War, the 2015 Iranian nuclear pact, and domestic issues like the debt ceiling and the Affordable Care Act. Polarization can produce a self-feeding spiral that harms institutions and reduces predictability over the long run. Bottom Line: Can the equity market rally through contested elections and crises of legitimacy? Yes. It may even cheer a hamstring government for a while. But prolonged uncertainty — or social instability — would weigh on business and consumer sentiment. Update On The Democratic Primary: The Lead-Up To Super Tuesday Chart 5Bloomberg May Supplant Biden As Pro-Establishment Front Runner

An Electoral College Tie?!?

An Electoral College Tie?!?

With the ninth Democratic Party primary debate concluding, the race for the nomination has blown open. Our view has been that a centrist or moderate candidate is most likely to emerge as the nominee and that former Vice President Joe Biden’s true testing ground would be in the South: South Carolina and Super Tuesday. Biden’s performance in Iowa and New Hampshire — where he angrily called a voter a “lying, dog-faced, pony soldier” — has been disastrous. Opinion polls suggest that New York City Mayor Michael Bloomberg may supplant him as the pro-establishment front runner (Chart 5). Bloomberg, however, has only just entered the race and has just suffered a hit from the combined onslaught of all the candidates at the ninth debate in Las Vegas. We need to see the votes — not just the money — to assess whether he can replace Biden (not to mention South Bend Mayor Pete Buttigieg and Minnesota Senator Amy Klobuchar) as the leading moderate candidate. Super Tuesday is critical for Bloomberg as well as for the other candidates who qualify for delegates and stay in the race after the Nevada Caucus on February 22 and South Carolina primary on February 29. With the roughly 55% share of votes going to moderates, Vermont Senator Bernie Sanders is benefiting from the ability to monopolize the remaining 45% of the vote for himself. That is, if Elizabeth Warren keeps failing to qualify. The problem for him is that his support could end up getting capped at around 25-30%, based on his performance thus far in Iowa, New Hampshire, and polling in Nevada, which is very different from 2016 when he divided the vote with Hillary Clinton alone (Chart 6). Chart 6Sanders’s Share Could Get Capped At 25-30%

An Electoral College Tie?!?

An Electoral College Tie?!?

The question is whether Sanders can beat Warren definitively and sustain the momentum — which is very strong at the moment (Chart 7). He has tapped into the anti-establishment vein of the populace that propelled Trump to the Republican nomination in 2016. Chart 7Can Sanders Sustain The Strong Momentum?

An Electoral College Tie?!?

An Electoral College Tie?!?

Party elites will not be able to reject Sanders if he wins a commanding plurality of the vote. Sanders is, thus far in the polling, more competitive for the nomination than Bloomberg (Chart 8), and more competitive than any candidate other than Biden when head-to-head against Trump (Chart 9). This is a tailwind in an election in which voters prioritize beating Trump: the more capable of doing so, the more momentum, the more capable of doing so. Chart 8Sanders Is Thus Far More Competitive Than Bloomberg

An Electoral College Tie?!?

An Electoral College Tie?!?

Chart 9Sanders Is More Competitive Than Other Dem Candidates Vs. Trump, Except Biden

An Electoral College Tie?!?

An Electoral College Tie?!?

There won’t be much clarity on the nomination process till after Super Tuesday at earliest. What is clear is that while Sanders may win a plurality of delegates (Chart 10), the moderates will take the nomination if they can coalesce around a candidate in time (Chart 11). Chart 10Sanders Likely To Win A Plurality Of Delegates …

An Electoral College Tie?!?

An Electoral College Tie?!?

Chart 11… Unless Moderates Coalesce Around One Candidate

An Electoral College Tie?!?

An Electoral College Tie?!?

Chart 12Super Delegates Could Tip The Scales Against Sanders, But Risk Sowing Discord

An Electoral College Tie?!?

An Electoral College Tie?!?

It matters whether Sanders wins a commanding plurality of the vote and the proportionately allocated “unpledged delegates” to the Democratic convention. We benchmark his performance at 40%+, keeping in mind the 43% of the popular vote for the nomination that Sanders won in 2016. If he can win this large of a share of the Democratic Party voters, and stay well ahead of his second-ranked competitor due to vote splitting, then it will be hard for the party elites and elders to reject him. The so-called automatic delegates or “super delegates” can join in the second round of voting at the Democratic National Convention, and they would hesitate about a Sanders nomination and would be numerous enough to tip the scales against him (Chart 12). But to do so they would have to send 40%+ of their voters home aggrieved, which would be undemocratic and un-strategic for the party as it would cause a split in July just when it needed to band together to try to beat Trump. Game theory can help to illuminate the constraints of the primary if Sanders fails to win a strong plurality.2 What follows is a simple demonstration to provide a framework for understanding the voting procedure of the Democratic primary elections as a whole, and specifically multiple rounds of voting at a contested convention. Let us assume that the Democratic Party can be divided into three roughly equally popular voting groups for the primary contest: E = The Establishment = Biden, Klobuchar R = Reformers = Buttigieg, Bloomberg A = Anti-Establishment = Sanders, Warren The preferences of the groups are as follows: Establishment: E, R, A. The establishment cannot tolerate losing power to left-wing populism. Reformers: R, E, A. The reformers believe the establishment is out of date but favor gradual change rather than revolution and would prefer the establishment over a radical candidate. Anti-Establishment: A, R, E. The anti-establishment would prefer a populist, but would accept a reformer, as long as he is not the establishment. If the front runner is Sanders, he will lose the first round of voting, as E + R > A. In the second round, if the choice is Biden, Biden will be rejected: R + A > E. Therefore a reformer wins. This is still the outcome if Biden is the front runner in the first round, since Biden would lose (R + A > E) but then his voters would have to help a reformer win (R + E > A). Or, if Bloomberg were put up in the second round instead of Biden, the reformer still would win since R + A > E. Only if Bloomberg began the first round as a front runner would the outcome change. The first round he would lose because E + A > R. And then in the second round Biden would win because E + R > A. In the above voting sequence, neither the establishment nor the reformist voters would have an incentive to vote strategically — both would vote straightforwardly — since both rank the anti-establishment as their least preferred option. Super Tuesday will be critical in seeing if Sanders’s trajectory points toward a strong plurality. Therefore if Sanders cannot get a large enough plurality to win outright — large enough to compel unpledged candidates to join his coalition to win a majority of delegates — then he becomes the victim of a rational decision making process that works against him. The foregoing is a simple demonstration of the way the voting procedure will hurt a weak front runner — and elect someone other than an anti-establishment candidate — if the primary is conceived of as a simple sequential voting procedure, or if it comes to a contested election. But it is still possible that we could have the nomination decided by Sanders outperforming and clinching a majority in the primary elections, or in a brokered deal in June. Or another candidate, a moderate, could become the front runner and clinch the nomination while other moderate candidates are winnowed. Bottom Line: The Sanders risk to the equity market is immediate because he could win a strong plurality of delegates that could then create a dynamic that enables him to clinch the nomination. But if he falls short of a strong plurality then a reformer or establishment Democrat is favored. Super Tuesday will be critical in seeing if his trajectory points toward such a strong plurality. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 See Robert Griffin, Ruy Teixeira, and William H. Frey, "America's Electoral Future: Demographic Shifts and the Future of the Trump Coalition," Center for American Progress, April 2018. 2 See Steven J. Brams, Game Theory And Politics (Dover, 2004).

Highlights Analyses on Asian semis, Argentina and Russia are available on pages 7, 12 and 14, respectively. The most likely trajectory for Chinese growth will be as follows: the initial plunge in business activity will be succeeded by a rather sharp snap-back due to pent-up demand. However, that quick rebound will probably be followed by weaker growth. Financial markets will soon focus on growth beyond the temporary rebound. In our opinion, it will be weaker than markets are currently pricing. Thus, risks for EM risk assets and currencies are skewed to the downside. A major and lasting selloff in EM stocks will only occur if EM corporate bond yields rise. In this week’s report we discuss what it will take for EM corporate credit spreads to widen. Feature The downside risks to EM risk assets and currencies are growing. We continue to recommend underweighting EM equities, credit and currencies versus their DM counterparts. Today we are initiating a short position in EM stocks in absolute terms. Chart I-1 illustrates that the total return index (including carry) of EM ex-China currencies versus the US dollar has failed to break above its 2019 highs, and has rolled over decisively. In contrast, the trade-weighted US dollar has exhibited a bullish technical configuration by rebounding from its 200-day moving average (Chart I-2). Odds are the dollar will make new highs. An upleg in the greenback will foreshadow a relapse in EM financial markets. Chart I-1EM Ex-China Currencies Have Been Struggling Despite Low US Rates

EM Ex-China Currencies Have Been Struggling Despite Low US Rates

EM Ex-China Currencies Have Been Struggling Despite Low US Rates

Chart I-2The US Dollar Remains In A Bull Market

The US Dollar Remains In A Bull Market

The US Dollar Remains In A Bull Market

Growth Trajectory After The Dust Settles The evolution of the coronavirus remains highly uncertain and unpredictable. As with any pandemic or virus outbreak, its evolution will be complex with non-trivial odds of a second wave. Even under the assumption that the epidemic will be fully contained by the end of March, its economic impact on the Chinese and Asian economies will likely be greater than global financial markets are currently pricing. As investors come to the realization that this initial pick-up in economic activity after the virus outbreak will be followed by weaker growth, the odds of a selloff in equities and credit markets will rise. In our January 30 report titled Coronavirus Versus SARS: Mind The Economic Differences, we argued that using the framework from the SARS outbreak to analyze the current epidemic is inappropriate. First, only a small portion of the Chinese economy was shut down in 2003, and for a brief period of time. The current closures and limited operations are much more widespread and likely more prolonged. Table I-1China’s Importance Now And In 2003

EM: Growing Risk Of A Breakdown

EM: Growing Risk Of A Breakdown