Geopolitics

Highlights Europe’s dirty little secret: Euro area debt is already mutualised. Investment implication: Overweight Italian BTPs, underweight German bunds, and overweight the euro on a structural (2-year plus) horizon. ESM plus ECB plus OMT equals a compromise solution to fund stimulus at a mutualised euro area interest rate. Investment implication: Overweight Italian BTPs, underweight German bunds on a cyclical (6-12 month) horizon. Spain’s high early peak in morbidity means that it has taken its pain upfront, at least compared to other countries. Investment implication: upgrade Spain’s IBEX to a tactical overweight – and remove it from the cyclical underweight basket. Feature Chart of the WeekThe Underperformances Of China, Italy And Spain Were A Mirror-Image Of Their Covid-19 Morbidity Curves

The Underperformances Of China, Italy And Spain Were A Mirror-Image Of Their Covid-19 Morbidity Curves

The Underperformances Of China, Italy And Spain Were A Mirror-Image Of Their Covid-19 Morbidity Curves

More About Morbidity Curves Most analyses of the pandemic tend to focus on the grim daily mortality statistics. Yet the key to the pandemic’s evolution is not its mortality rate, but rather its morbidity (severe illness) rate. This is because, without a vaccine, the total area underneath the morbidity curve is fixed. The cumulative number of people who will fall severely ill is pre-determined at the outset (Figures 1-3). Figure I-1The Area Under The Morbidity Curve Is Fixed, A High First Peak Means A Low Second Peak

Will Europe Unite Or Split?

Will Europe Unite Or Split?

Figure I-2A Low First Peak Means An Extended First Peak…

Will Europe Unite Or Split?

Will Europe Unite Or Split?

Figure I-3…Or A High Second Peak

Will Europe Unite Or Split?

Will Europe Unite Or Split?

Very optimistically assuming a Covid-19 morbidity rate of 1 percent, and that 65 percent of the population must get infected to exhaust the pandemic, we know that Covid-19 will ultimately make 0.65 percent of the population severely ill. Absent a vaccine, this number is set in stone. But the number of deaths is not set in stone. It depends on the availability of emergency medical treatment for those that are severely ill. For Covid-19 this means access to ventilation in an intensive care unit (ICU). Yet even the best equipped countries only have ICUs for 0.03 percent of the population. Therefore, the emergency treatment must be rationed either by supply or by demand. Without a Covid-19 vaccine, we cannot change the cumulative number of people who will become severely ill. Rationing by supply means that we must deny emergency treatment to the severely ill – not just Covid-19 patients but victims of, say, heart attacks or car crashes. Accept more deaths. Rationing by demand means that we must flatten the demand (morbidity) curve so that demand is always satisfied by the limited ICU supply. During the pandemics of 1918-19 and 1957, countries could ration emergency medical treatment by supply. Not in 2020. In an era of universal healthcare, everybody is entitled to, and expects to get, emergency medical care. Which means we must ration emergency medical treatment by demand. As such, we must analyse the 2020 response differently to the responses in 1918-19 and 1957. To repeat, without a vaccine, we cannot change the area under the morbidity curve. There is no way of escaping this truth. A low first peak requires a very elongated peak or a high second peak (Chart I-2). Conversely, countries that have suffered a high first peak will need a shorter peak and small (or no) second peak. Chart I-2Japan's Early Stabilisation Was A False Dawn

Japan's Early Stabilisation Was A False Dawn

Japan's Early Stabilisation Was A False Dawn

Turning to an equity market implication, the underperformances of highly cyclical and domestically exposed Spain and Italy have closely tracked their morbidity curves (Chart I-1). Given that both countries have suffered very high first peaks in morbidity, the strong implication is that they have taken their pain upfront – at least compared to other countries. In the case of Spain, the market is also technically oversold (see Fractal Trading System). Investment implication: upgrade Spain’s IBEX to a tactical overweight – and remove it from the cyclical underweight basket. How Europe Could Unite Europe is dithering on its fiscal response to the pandemic. Specifically, Germany and the Netherlands are pushing back against the concept of mutualised euro area debt in the form of ‘corona-bonds’. But a pandemic is an act of nature, an indiscriminate exogenous shock. What is the point of the economic and monetary union if Italy must fund its response to an act of nature at the Italian 10-year yield of 1.5 percent rather than the euro area 10-year yield of 0 percent? (Chart I-3 and Chart I-4) Chart I-3To Fight An Act Of Nature Why Should Italy Borrow At A Higher Rate...

To Fight An Act Of Nature Why Should Italy Borrow At A Higher Rate...

To Fight An Act Of Nature Why Should Italy Borrow At A Higher Rate...

Chart I-4...When It Could Borrow At A Lower Mutualised Rate?

...When It Could Borrow At A Lower Mutualised Rate?

...When It Could Borrow At A Lower Mutualised Rate?

The good news is there is a compromise solution to fund stimulus at a mutualised interest rate. It uses the euro area’s €500 billion bailout fund, the European Stability Mechanism (ESM). But the compromise solution carries two problems which need mitigation. First, ESM credit lines come with conditionality. Italy would rightly balk if it were shackled like Greece, Portugal, and Ireland were after the euro debt crisis. Luckily, the ESM is likely to regard the current ‘act of nature’ crisis very differently to the debt crisis and impose only minimum and appropriate conditionality – for example, that credit lines should be used for healthcare and social welfare spending. Second, ESM credit lines come with a stigma. Taking fright that Italy is tapping the ESM, the bond market might drive up the yields on Italian BTPs. If this pushed up Italy’s overall funding rate, it would defeat the purpose of using the ESM in the first place. ESM plus ECB plus OMT equals a compromise solution to borrow at a mutualised interest rate. The hope is that the bond market, realising that Italy is using the bailout facility to counter an act of nature, would not drive up BTP yields. But if it did, the ECB could counter this by buying BTPs. One option would be to use its Outright Monetary Transactions (OMT) facility. Set up during the euro debt crisis, the OMT’s specific function is to counter bond market attacks when they are not justified by the economic fundamentals. In other words, to prevent a liquidity crisis escalating into a solvency crisis. Thereby, ESM plus ECB plus OMT equals a compromise solution to fund stimulus at a mutualised euro area interest rate. Investment implication: Overweight Italian BTPs, underweight German bunds on a cyclical (6-12 month) horizon. Europe’s Dirty Little Secret Outwardly, Germany and the Netherlands are reluctant to go down the slippery slope to mutualised euro area debt. But here’s the dirty little secret they don’t want you to know. Euro area debt is already mutualised. The stealth mutualisation has happened via the Target2 banking imbalance which now stands at €1.5 trillion. This imbalance is an accounting identity showing that Italy is owed ‘German euros’ via its large quantity of bank deposits in German banks while Germany is symmetrically owed ‘Italian euros’ via its large effective holding of Italian government bonds. The imbalance is irrelevant if a German euro equals an Italian euro. But if Italy defaulted on its bonds – by repaying them in a reinstated and devalued lira – then Target2 means that Germany must pick up the bill (Chart I-5). Chart I-5Target2 Means That If Italy Defaults, Germany Picks Up The Bill

Will Europe Unite Or Split?

Will Europe Unite Or Split?

The Target2 imbalance is the result of the ECB’s QE program, in which the central bank has bought hundreds of billions of Italian bonds. If Italy repaid those bonds in a devalued lira, then the ECB would become insolvent, and the central bank’s remaining shareholders would have to plug the hole. The biggest shareholder would be Germany. Could Germany force Italy to repay its bonds in euros? No. According to a legal principle called ‘lex monetae’ Italy can repay its debt in its sovereign currency, whatever that is. Meanwhile, because of the fragility of the Italian banking system, the Italians who sold the bonds to the ECB deposited the cash in German banks. Legally, these depositors must be paid back in whatever is the German currency. Euro area debt is already mutualised. If euro area debt is already mutualised, why do policymakers continue to pretend that it isn’t? There are three reasons. First no policymaker would want to publicise that Germany is now on the hook if Italy left the euro. Second, no policymaker would want to publicise that the ECB has put Germany in this position (Chart I-6). Chart I-6ECB QE Has Created The Target2 Imbalance

ECB QE Has Created The Target2 Imbalance

ECB QE Has Created The Target2 Imbalance

Third, and most important, policymakers would point out that the mutualisation of debt only happens if the euro breaks up. They would argue that because the euro is irreversible, the debt is not mutualised. In fact, their argument is completely back to front. The truth is: Because euro area debt is now mutualised, the euro has become irreversible. Investment implication: Overweight Italian BTPs, underweight German bunds, and overweight the euro on a structural (2-year plus) horizon. Fractal Trading System* As already discussed, this week’s recommended trade is long Spain’s IBEX 35 versus the Euro Stoxx 600. The profit target is 3 percent with a symmetrical stop-loss. Meanwhile our other trade, long Australia versus New Zealand has moved into a 2 percent profit. The rolling 12-month win ratio now stands at 66 percent. Chart I-7IBEX 35 Vs. EUROSTOXX 600

IBEX 35 Vs. EUROSTOXX 600

IBEX 35 Vs. EUROSTOXX 600

When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Global shortages of medical equipment – including medicines – are frontloaded until emergency production kicks in. As the crisis abates, political recriminations between the US and China will surge. The US will seek to minimize medical supply exposure to China going forward, a boon for India and Mexico. China has escaped the COVID-19 crisis with minimal impact on food supply. Pork prices are surging due to African Swine Flu, but meat is a luxury. Still, the “Misery Index” is spiking and this will increase social instability. Food insecurity, inflation, and large current account deficits suggest that emerging market currencies will remain under pressure. Turkey and South Africa stand to suffer while we remain overweight Malaysia. Feature Chart 1Collapse In Economic Activity

Collapse In Economic Activity

Collapse In Economic Activity

With a third of the world population under some form of lockdown, general activity in the world’s manufacturing powerhouses has collapsed (Chart 1). The breakdown is a double whammy on market fundamentals. On the supply side, government-mandated containment efforts force workers in non-essential services to stay home while, on the demand side, households confined to their homes are unable to spend. Acute demand for medical supplies is causing shortages, while supply disruptions threaten states that lack food security. While global monetary and fiscal stimulus will soften the blow (Chart 2), the economic shock is estimated to be a 2% contraction in real GDP for every month of strict isolation. If measures are extended beyond April, markets will sell and new stimulus will be applied. Already the US Congress is negotiating the $1-$2 trillion infrastructure package that we discussed in our March 4 report, and cash handouts will be ongoing. When the dust settles the political fallout will be massive. Authoritarian states like China and especially Iran will face greater challenges maintaining domestic stability. Democracies like Italy and the US, which lead the COVID-19 case count, are the most likely to experience a change in leadership (Chart 3). Initially the ruling parties of the democracies are receiving a bump in opinion polling, but this will fade as households will be worse off and will likely vent their grievances at the ballot box.

Chart 2

Chart 3

Until a vaccine or treatment is discovered, medical equipment and social distancing are the only weapons against the pandemic. National production is (rightly) being redirected from clothing and cars to masks and ventilators to meet the spike in demand. Will the supply shock cause shortages in food and medicine – essential goods for humankind? In this report we address the impact of COVID-19 on global supply security and assess the market implications. Medical Equipment Shortages Will Spur Protectionism

Chart

Policymakers are fighting today’s crisis with the tools of the 2008 crisis, but a lasting rebound in financial markets will depend on surmounting the pandemic, which is prerequisite to economic recovery (Table 1). As the US faces the peak of its COVID-19 outbreak, public health officials and doctors are raising the alarm on the shortage of medical supplies. A recent US Conference of Mayors survey reveals that out of the 38% of mayors who say they have received supplies from their state, 84.6% say they are inadequate (Chart 4). Italy serves as a warning: A reported 8% of the COVID-19 cases there are doctors and health professionals, often treating patients without gloves or with compromised protective gear. These workers are irreplaceable and when they succumb the virus cannot be contained. In the US, doctors and nurses are re-using masks and sometimes treating patients behind a mere curtain, highlighting the supply shortage. While the shortages are mainly driven by a surge in demand from both medical institutions and households, they also come from the supply side, particularly China. Factory closures and transportation disruptions in China earlier this year, coupled with Beijing’s government-mandated export curbs, reduced Chinese exports, a major source of US and global supplies (Chart 5).

Chart 4

Chart 5

Other countries have imposed restrictions on exports of products used in combating the spread of COVID-19. Following export restrictions by the French, German, and Czech governments in early March, the European Commission intervened on March 15 to ensure intra-EU trade. It also restricted exports of protective medical gear outside of the EU. At least 54 nations have imposed new export restrictions on medical supplies since the beginning of the year.1 Both European and Chinese measures will reduce supplies in the US, the top destination for most of these halted exports (Chart 6).

Chart 6

Thus it is no wonder that the Trump administration has rushed to cut import duties and boost domestic production. The administration has released strategic stockpiles and cut tariffs on Chinese medical equipment used to treat COVID-19. With the whole nation mobilized, supply kinks should improve greatly in April. After a debacle in rolling out test kits (Chart 7), the US is rapidly increasing its testing capabilities to manage the crisis, with over a million tests completed as of the end of March (Chart 8). Meanwhile a coalition of companies is taking shape to make face masks. The president has invoked the defense production act to force companies to make ventilators.

Chart 7

Chart 8

However, with the pandemic peaking in the US, the hardest-hit regions will continue experiencing shortages in the near term. Shortages are prompting public outcry against the US government for its failure to anticipate and redress supply chain vulnerabilities that were well known and warned against. A report in The New York Times tells how Mike Bowen, owner of Texas-based mask-maker Prestige Ameritech, has advised the past three presidents about the danger in the fact that the US imports 95% of its surgical masks. “Aside from sitting in front of the White House and lighting myself on fire, I feel like I’ve done everything I can,” he said. He is currently inundated with emergency orders from US hospitals. The same report tells of a company called Strong Manufacturers in North Carolina that had to cut production of masks because it depends on raw materials from Wuhan, China, where the virus originated.2 The Trump administration will suffer the initial public uproar, but the US government will also seek to reduce import dependency going forward, and it will likely deflect some of the blame by focusing on the supply risks posed by China. Beijing, for its part, is launching a propaganda campaign against the US to distract from its own failures at home (some officials have even blamed the US for the virus). Meanwhile it is cranking up production and shipping medical supplies to crisis hit areas like Italy to try to repair its global image after having given rise to the virus. In addition, the city of Shenzhen is sending 1.2 million N95 masks to the US on the New England Patriots’ team plane. Even Russia is sending small donations. But these moves work to propagandistic efforts in these countries and will ultimately shame the Americans into taking measures to improve self-sufficiency. Bottom Line: The most important supply shortage amid the global pandemic is that of medical equipment. While these shortages will abate sooner rather than later, the supply chain vulnerabilities they have exposed will trigger new policies of supply redundancy and import substitution. The US in particular will seek to reduce dependency on China. That COVID-19 is aggravating rather than reducing tensions between these states, despite China’s role as a key supplier in a time of need, highlights the secular nature of their rising tensions. The US-China Drug War Shortages of pharmaceuticals are also occurring, despite the fact that the primary pandemic response is necessarily “non-pharmaceutical” (e.g. social distancing). The US Food and Drug Administration (FDA) announced the first COVID-19 related drug shortage in the US on February 27. While the specific drug was not disclosed, the announcement notes that “the shortage is due to an issue with manufacturing of an active pharmaceutical ingredient used in the drug.”3 The FDA is monitoring 20 other (non-critical) drugs potentially at risk of shortages because the sole source is China. The global spread of the pandemic will increase these shortages. On March 3 India announced export restrictions on 26 drugs, including paracetamol and several antibiotics, due to supply disruptions caused by the Chinese shutdown. While Chinese economic activity has since picked up, India is now among the string of countries under a nationwide lockdown. Similar measures enforced across Europe will also hamper the production and transportation of these goods. The implication is that even if Chinese drugs return to market, supplies further down the chain and from alternative suppliers will take a hit. The risk that this will evolve into a drug shortage depends on the intensity of the outbreak. Drug companies generally hold 3-6 months’ worth of inventories. Consequently, while inventories are likely to draw as supplies are disrupted, consumers may not experience an outright shortage immediately. In the US, as with equipment and protective gear, the government’s strategic stockpile will buffer against shortfalls in supplies of critical drugs. COVID-19 is aggravating rather than reducing US-China tensions. Nevertheless the supply chain is getting caught up in the larger US-China strategic conflict. Even before the pandemic, the US-China trade war brought attention to the US’s vulnerabilities to China’s drug exports. This dispute is not limited to illicit drugs, as with China’s production of the opioid fentanyl, but also extends to mainstream medicines, as highlighted in the selection of public statements shown in Table 2.

Chart

Chart 9

How much does the US rely on China for medicine? According to FDA data, just over half of manufacturing facilities producing regulated drugs in finished dosage form for the US market are located abroad, with China’s share at 7% (Chart 9).4 The figures are higher for manufacturing facilities producing active pharmaceutical ingredients, though still not alarming – 72% of the facilities are located abroad, with 13% in China. Of course, high-level data understate China’s influence. The complex nature of global drug supply chains means that the source of finished dosage forms masks dependencies and dominance higher up the supply chain (Figure 1).

Chart

For instance, active pharmaceutical ingredients produced in Chinese facilities are used as intermediate goods by finished dosage facilities in India as well as China. The FDA reports that Indian finished dosage facilities rely on China for three-quarters of the active ingredients in their generic drug formulations, which are then exported to the US and the rest of the world. Any supply disruption in China – or any other major drug producer – will lead to shortages further down the supply chain.

Chart 10

Chinese influence becomes more apparent when the sample is restricted to generic prescription drugs. These are especially relevant because nearly 70% of Americans are on at least one prescription drug, of which more than 90% are dispensed in the generic form. In this case, 87% of ingredient manufacturers and 60% of finished dosage manufacturers are located outside the US, with 17% of ingredient facilities and 8% of dosage facilities in China (Chart 10). Of all the facilities that manufacture active ingredients that are listed on the World Health Organization’s Essential Medicines List – a compilation of drugs that are considered critical to the health system – 71% are located aboard with 15% located in China (Chart 11). Moreover, manufacturers are relatively inflexible when adapting to market conditions and shortages. Drug manufacturing facilities generally operate at above 80% of their capacity and are thus left with little immediate capacity to ramp up production in reaction to shortages elsewhere. In addition, manufacturers face challenges in changing ingredient suppliers – there is no centralized source of information on them, and additional FDA approvals are required. The US will look to reduce its dependency on China for its drug supplies regardless of 2020 election outcome. China also has overwhelming dominance in specific categories. The Council on Foreign Relations reports that China makes up 97% of the US antibiotics market.5 Other common drugs that are highly dependent on China for supplies include ibuprofen, acetaminophen, hydrocortisone, penicillin, and heparin (Chart 12).

Chart 11

Chart 12

Taking it all together, US vulnerability can be overstated. Consider the following: Of the 370 drugs on the Essential Medicines List that are marketed in the US, only three are produced solely in China. None of these three are used to treat top ten causes of death in the United States. Import substitution is uneconomical. Foreign companies, especially Chinese companies, are attractive due to their lower costs and lax regulations. While China’s influence extends higher up the supply chain, this is true for US markets as well as other consumer markets. While China can cut off the US from the finished dosages it supplies, it cannot do the same for the ingredients that are used by facilities in other countries and eventually make their way to the US in finished dosage form. Americans are demanding that drug prices be reduced and an obvious solution is looser controls on imports. The recent activation of the Defense Production Act shows that the US can take action to boost domestic production in emergencies. Nevertheless, China is growing conspicuous to the American public due to general trade tensions and COVID-19. As it moves up the value chain, it also threatens increasing competition for the US and its allies. Hence the US government will have a strategic reason to cap China’s influence that is also supported by corporate interests and popular opinion. This will lead to tense trade negotiations with China and meanwhile the US will seek alternative suppliers. China will not want to lose market share or leverage over the United States, so it may offer trade concessions at some point to keep the US engaged. Ultimately, however, strategic tensions will catalyze US policy moves to reduce the cost differential with China and promote its rivals. Pressure on China over its currency, regulatory standards, and scientific-technological acquisition will continue regardless of which party wins the White House in 2020. The Democrats would increase focus on China’s transparency and adherence to international standards, including labor and environmental standards. Both Republicans and Democrats will try to boost trade with allies. The key beneficiaries will be India, Southeast Asia, and the Americas. Taiwan’s importance will grow as a middle-man, but so will its vulnerability to strategic tensions. Bottom Line: The US and the rest of the world are suffering shortfalls of equipment necessary to combat COVID-19. There is also a risk of drug shortages stemming from supply disruptions and emergency protectionist policies. These shortages look to be manageable, but they have exposed national vulnerabilities that will be reduced in future via interventionist trade policies. While the US and Europe will ultimately manage the outbreak, the political fallout will be immense. The US will look to reduce its dependency on China. This will increase investment in non-China producers of active pharmaceutical ingredients, such as India and Mexico. The US tactics against China will vary according to the election result, but the strategic direction of diversifying away from China is clear and will have popular impetus in the wake of COVID-19. Food Security In addition to the challenges posed by COVID-19 on medical supplies, food – another essential good – also faces risk of shortages. China is a case in point. Food prices there were on the rise well before the COVID-19 outbreak, averaging 17.3% in the final quarter of 2019. However inflation was limited to pork and its substitutes – beef, lamb and poultry – and reflected a reduction in pork supplies on the back of the African Swine Flu outbreak. While year-on-year increases in the prices of pork and beef averaged 102.8% and 21.0%, respectively, grain, fresh vegetable, and fresh fruit prices averaged 0.6%, 1.5%, and -5.0% in Q42019 (Chart 13). Chart 13Chinese Inflation Has (Thus far) Been Contained To Pork

Chinese Inflation Has (Thus far) Been Contained To Pork

Chinese Inflation Has (Thus far) Been Contained To Pork

Chart 14China's Misery Index Is Spiking - A Political Liability

China's Misery Index Is Spiking - A Political Liability

China's Misery Index Is Spiking - A Political Liability

However China’s COVID-19 containment measures had a more broad-based impact on food supplies, threatening to push up China’s Misery Index (Chart 14). Travel restrictions, roadblocks, quarantined farm laborers, and risk-averse truck drivers introduced challenges not only in ensuring supplies were delivered to consumers, but also to daily farm activity and planting. The absence of farm inputs needed for planting such as seeds and fertilizer, and animal feed for livestock, was especially damaging in regions hardest hit by the pandemic. Livestock farmers already struggling with swine flu-related reductions in herd sizes were forced to prematurely cull starving animals, cutting the stock of chicken and hogs. Now as the country transitions out of its COVID-19 containment phase and moves toward normalizing activity (Chart 15), food security is top of the mind. Authorities are emphasizing the need to ensure sufficient food supplies and adopt policies to encourage production.6 This is especially important for crops due to be planted in the spring. Delayed or reduced plantings would weight on the quality and quantity of the crops, pushing prices up.

Chart 15

With food estimated to account for 19.9% of China’s CPI basket – 12.8% of which goes towards pork (Chart 16) – a prolonged food shortage, or a full-blown food crisis, would be extremely damaging to Chinese families and their pocketbooks.

Chart 16

However, apart from soybeans and to a lesser extent livestock, China’s inventories are well stocked (Chart 17) and are significantly higher than levels amid the 2006-2008 and 2010-2012 food crises. Inventories have been built up specifically to provide ammunition precisely in times of crisis. Corn and rice stocks are capable of covering consumption for nearly three quarters of a year, and wheat stocks exceeding a year’s worth of consumption. Thus, while not completely immune, China today is better able to weather a supply shock. Moreover, with the exception of soybeans, China is not overly dependent on imports for agricultural supplies (Chart 18).

Chart 17

Chart 18

As the COVID-19 epicenter shifts to the US and Europe, farmers there are beginning to face the same challenges. Reports of delays in the arrival of shipments of inputs such as fertilizer and seeds have prompted American farmers to prepare for the worst and order these goods ahead of time.

Chart 19

While these proactive measures will help reduce risks to supply, farmers in Europe and parts of the US who typically rely on migrant laborers will need to search for alternative laborers as the planting season nears. Just last week France’s agriculture minister asked hairdressers, waiters, florists, and others that find themselves unemployed to take up work in farms to ensure food security. As countries become increasingly aware of the risks to food supplies, some have already introduced protectionist measures, especially in the former Soviet Union: The Russian agriculture ministry proposed setting up a quota for Russian grain exports and has already announced that it is suspending exports of processed grains from March 20 for 10 days. Kazakhstan suspended exports of several agricultural goods including wheat flour and sugar until at least April 15. On March 27, Ukraine’s economy ministry announced that it was monitoring wheat export and would take measures necessary to ensure domestic supplies are adequate. Vietnam temporarily suspended rice contracts until March 28 as it checked if it had sufficient domestic supplies. The challenge is that, unlike China, inventories in the rest of the world are not any higher than during the previous food crisis and do not provide much of a buffer against supply shortfalls (Chart 19). Higher food prices would be especially painful to lower income countries where food makes up a larger share of household spending (Chart 20). In addition to using their strategic food stockpiles, governments will attempt to mitigate the impact of higher food prices by implementing a slew of policies:

Chart 20

Trade policies: Producing countries will want to protect domestic supplies by restricting exports – either through complete bans or export quotas. Importing countries will attempt to reduce the burden of higher prices on consumers by cutting tariffs on the affected goods. Consumer-oriented policies: Importing countries will provide direct support to consumers in the form of food subsidies, social safety nets, tax reductions, and price controls. Producer-oriented policies: Governments will provide support to farmers to encourage greater production using measures such as input subsidies, producer price support, or tax exemptions on goods used in production. While these policies will help alleviate the pressure on consumers, they also result in greater government expenditures and lower revenues. Thus, subsidizing the import bill of a food price shock can weigh on public finances, debt levels, and FX reserves. Currencies already facing pressure due to the recessionary environment, such as Turkey, South Africa and Chile will come under even greater downward pressure. Food inventories ex-China are insufficient to protect against supply shortages. Bottom Line: COVID-19’s logistical disruptions are challenging farm output. This is especially true when transporting goods and individuals across borders rather than within countries. This will be especially challenging for food importing countries, as some producers have already started erecting protectionist measures and this will result in an added burden on government budgets that are already extended in efforts to contain the economic repercussions of the pandemic. Investment Implications Chart 21Ag Prices Inversely Correlated With USD

Ag Prices Inversely Correlated With USD

Ag Prices Inversely Correlated With USD

China will continue trying to maximize its market share and move up the value chain in drug production. At the same time, the US is likely to diversify away from China and try to cap China’s market share. This will result in tense trade negotiations regardless of the outcome of the US election. The COVID-19 experience with medical shortages and newfound public awareness of potential medical supply chain vulnerabilities means that another round of the trade war is likely. Stay long USD-CNY. Regarding agriculture, demand for agricultural commodities is relatively inelastic. This inelasticity should prevent a complete collapse in prices even amid a weak demand environment. Thus given the risk on supplies, prices face upward pressure. However, not all crops are facing these same market dynamics. While wheat and rice prices have started to move in line with the dynamics described above, soybeans and to a greater extent corn prices have not reacted as such (Chart 21). In the case of soybeans, we expect demand to be relatively muted. China accounts for a third of the world’s soybean consumption. 80% of Chinese soybeans are crushed to produce meal to feed China’s massive pork industry. However, the 21% y/y decline in pork output in 2019 on the back of the African Swine Flu outbreak will weigh on demand and mute upward pressures on supplies. Demand for corn will also likely come in weak. The COVID-19 containment measures and the resulting halt in economic activity reduce demand for gasoline and, as a consequence, reduce demand for corn-based ethanol, which is blended with gasoline. In addition to the above fundamentals, ag prices have been weighed down by a strong USD which makes ex-US exporters relatively better off, incentivizing them to raise exports and increase global supplies. A weaker USD – which we do not see in the near term – would help support ag prices. It is worth noting that if there is broad enforcement of protectionist measures, then producers will not be able to benefit from a stronger dollar. In that case we may witness a breakdown in the relationship between ag prices and the dollar. In light of these supply/demand dynamics, we expect rice and wheat prices to be well supported going forward and to outperform corn and soybeans. Roukaya Ibrahim Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 See "Tackling COVID-19 Together: The Trade Policy Dimension," Global Trade Alert, University of St. Gallen, Switzerland, March 23, 2020. 2 See Rachel Abrams et al, "Governments and Companies Race to Make Masks Vital to Virus Fight," The New York Times, March 21, 2020. 3 The announcement also notes that there are other alternatives that can be used by patients. See "Coronavirus (COVID-19) Supply Chain Update," US FDA, February 27, 2020. 4 All regulated drugs include prescription (brand and generic), over the counter, and compounded drugs. 5 Please see Huang, Yanzhong, "The Coronavirus Outbreak Could Disrupt The US Drug Supply," Council on Foreign Relations, March 5, 2020. 6 The central government ordered local authorities to allow animal feed to pass through checkpoints amid the lockdowns. In addition, Beijing has relaxed import restrictions by lifting a ban on US poultry products and announcing that importers could apply for waivers on goods tariffed during the trade war such as pork and soybeans. The lifting of these restrictions also serves to help China meet its phase one trade deal commitments. Please see "Coronavirus hits China’s farms and food supply chain, with further spike in meat prices ahead," South China Morning Post, dated February 21, 2020.

Highlights The odds of an emergency meeting of OPEC 2.0 to get supply under control are growing, based on the repeated overtures from Russian officials providing the Kingdom of Saudi Arabia (KSA) an opening to resume talks on their production-management regime. We have developed a not-unreasonable scenario in which global oil consumption falls by ~ 20% y/y in April to assess the COVID-19-induced price impact. Even an aggressive 3.5mm b/d cut from OPEC 2.0 – presuming a rapprochement between KSA and Russia – and an additional 200k b/d market-induced cut by North American producers still sees Brent prices bottoming over the next two months at ~ $18/bbl. OECD inventories surge, reaching ~ 3.6 billion by June 2020, before production cuts and demand restoration start to drain them. Comments from Texas Railroad Commission (RRC) leadership indicate they could be back in the business of pro-rating production in the Lone Star state. If a new OPEC 3.0 described here can move quickly enough, Brent prices could revive to ~ $45/bbl by year end, and clear $60/bbl by 2Q21. We are getting long Dec20 Brent and WTI at tonight’s close. Feature Refiners worldwide are reducing runs as the COVID-19 pandemic continues to cut through oil demand like a scythe through wheat.1 Refiners’ inability to sell gasoline, diesel and jet fuel, and a host of other products, is forcing crude oil to back up globally in storage facilities, pipelines and, soon, on ships (Chart 1).2 This is occurring while KSA and Russia wage a global market-share war, targeting each others’ refinery customers with lower and lower prices. Without a concerted effort by OPEC 2.0 – the coalition led by KSA and Russia – and the US shales to rein in production, the global supply of storage will be exhausted and oil prices will push well below $20/bbl to force output to shut in. Indeed, numerous grades of crude oil worldwide already are trading below $20/bbl after factoring in their spreads vs. Brent crude oil as regional takeaway and storage infrastructure are overwhelmed (Chart 2). Chart 1Even With Production Cuts Oil Inventories Will Surge

Even With Production Cuts Oil Inventories Will Surge

Even With Production Cuts Oil Inventories Will Surge

Chart 2Global Crude Prices Trading Below $20/bbl

Global Crude Prices Trading Below $20/bbl

Global Crude Prices Trading Below $20/bbl

Chart 3“The Other Guys” Production Declines Will Accelerate

"The Other Guys" Production Declines Will Accelerate

"The Other Guys" Production Declines Will Accelerate

The consequences for oil producers outside core-OPEC will be disastrous, as they were following the last market-share war led by OPEC in 2014-16. The producer group we’ve dubbed “The Other Guys” – producers outside core-OPEC – will continue to see production falling, most likely at an accelerating rate, if the market-share war persists (Chart 3). Even within core-OPEC – principally the GCC states – governments will be required to cut spending on public works, salaries for workers, and services.3 Sovereign wealth funds and foreign reserves will have to be drawn down to fill holes in budgets, as happened during the last market-share war of 2014-16 launched by OPEC. The IMF last week noted the world economy is in recession, and that EM economies in particular will see growth fall sharply as a result of the COVID-19 pandemic.4 “We are in an unprecedented situation where a global health pandemic has turned into an economic and financial crisis. With a sudden stop in economic activity, global output will contract in 2020. … emerging market and developing countries, especially low-income countries, will be particularly hard hit by a combination of a health crisis, a sudden reversal of capital flows and, for some, a sharp drop in commodity prices. Many of these countries need help to strengthen their crisis response and restore jobs and growth, given foreign exchange liquidity shortages in emerging market economies and high debt burdens in many low-income countries.” For commodity markets, this means the principal source of demand growth is being severely hobbled. The Oil Demand Hit … Estimating the demand destruction caused by COVID-19 is fraught with uncertainty. Instead of attempting such an estimate, we simulate a sharp drop in oil demand of close to 20% y/y in April 2020, which is consistent with the lockdowns that are bringing the global economy to a standstill. Specifically, we have 2Q20 demand falling ~ 12mm b/d (y/y vs. 2Q19). Thereafter, demand picks up rapidly in 2H20, reaching a growth rate of 800k b/d by 4Q20. For all of 2020, we model average demand losses equal to 3.8mm b/d. For next year, we expect the combination of massive fiscal and monetary stimulus hitting markets globally will lift demand 5.3mm b/d. Net, we view the COVID-19 demand shock as transitory. But it leaves a huge amount of unrefined crude oil in storage and massive amounts of unsold products in inventory. Left unaddressed, crude oil will continue to fill storage globally, as will unsold refined products. This will leave oil producers and refiners in an untenable situation, even after demand returns to normal following the pandemic. Strategists in Riyadh, Moscow and Austin, Texas, know this. … Requires A Supply Offset KSA is forcing its competitors to endure what John Rockefeller, one of the founders of Standard Oil Co., once called a “good sweating.”5 A good sweating was a price-cutting strategy designed to drive competitors out of business and force them to sell to Rockefeller’s company. This occurred in 2014-16 and in 1986, when KSA had to rein in fellow OPEC members that were free-riding on its production discipline. We believe KSA is well aware it cannot endure a years-long market-share war, nor does it want to. Its primary goal in the current circumstances is to remind oil producers globally that it can, when it choses, take as much market share as it deems necessary. After flooding global markets in April 2020 we expect the core-OPEC producers in the Gulf (Kuwait, the UAE, Iraq and, of course, KSA) to reduce production by ~ 2.5mm b/d starting in May 2020, and hold these cuts until 2021 (around the time inventories are drawn down to their 5-year average). In 2021, we have the group increasing production by 2.5mm b/d in 1Q21. As for Russia, we have them increasing production in April 2020 – contributing to the surge in inventories globally. However, beginning in May, we believe Russia and its non-OPEC allies will agree to remove ~ 1mm b/d , in line with the cuts we expect from core-OPEC. Russia faces political and geopolitical constraints that work against maintaining the market-share war. First, President Vladimir Putin has already been forced to shift his national strategy over the past three years to address growing concerns with domestic discontent due to the recession caused by the 2014 oil shock and the economic austerity policies his government pursued afterwards. These policies give Putin policy room to fight today’s market-share war, but they also portend another massive blow to the livelihood and wellbeing of the nation. Second, Putin is in the midst of arranging an extension of his term in office through 2036, which requires the constitutional court to approve of constitutional changes as well as a popular referendum. The referendum has been delayed due to the pandemic and need for an emergency response. While Putin is generally popular and has underhanded means of orchestrating the referendum, it would be extremely dangerous for him to compound the pandemic and global recession with an oil market-share war that makes matters even worse for the Russian people while simultaneously preparing for a plebiscite. Third, internationally, Putin cannot ultimately defeat the Saudis or US shale in terms of market share. Therefore the domestic risks posed above are not compensated by an improvement in Russia’s international standing – neither in oil markets nor in broader strategic influence, given that an economic recession hurts Russia’s ability to maintain and modernize its military and security forces. In the US shales, we are modeling a sharp fall-off in production starting as early as May 2020. For the rest of 2020, production will gradually decline naturally from low rig counts. In 2H20 – probably in 4Q20 – we expect the Texas Railroad Commission to once again regulate oil production in the state, provided other state regulators (e.g., in North Dakota) and producing countries, (e.g., Russia and KSA) also sign on to take on a similar role.6 In addition to the market-driven shut-ins between now and 4Q20, we expect the RRC to secure production cuts of up to 1.5mm b/d by Dec 2020. As prices pick up next year, shale production will stabilize and slowly move up. The supply-demand assumptions we make in this scenario produce a physical surplus for the better part of 2020 (Chart 4). Chart 4Supply-Demand Imbalance Leads to Physical Surplus

Supply-Demand Imbalance Leads to Physical Surplus

Supply-Demand Imbalance Leads to Physical Surplus

Prices Could Fall Further, Then Take Off Even if we see OPEC 2.0 cut, and sharp drops in US shale output followed by renewed pro-rationing by state regulators in the US led by Texas, the fact that they’ve all increased production for April means storage will inevitably rise drastically in the coming months (Chart 5). As inventory skyrockets in the wake of both the massive demand and supply shocks in 1Q20 and April 2020, prices will fall to $20/bbl (Chart 6). Chart 5Inventories Swell on Demand Shock, Then Drain on Supply Cuts

Inventories Swell on Demand Shock, Then Drain on Supply Cuts

Inventories Swell on Demand Shock, Then Drain on Supply Cuts

Chart 6Brent Prices Forced Lower, Then Move Above $60/bbl

Brent Prices Forced Lower, Then Move Above $60/bbl

Brent Prices Forced Lower, Then Move Above $60/bbl

Once the large-scale OPEC 2.0 cuts start, prices rebound rapidly. Demand also starts picking up this summer, which also will lift prices. For 2020, we expect Brent prices to average $35/bbl, while in 2021 we expect Brent to average $66/bbl. Over this period, WTI will trade $2-$4/bbl below Brent. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Matt Gertken Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 Please see Global oil refiners shut down as coronavirus destroys demand published by reuters.com March 26, 2020, and S&P Global Platts report Refinery margin tracker: Global refining margins take a severe hit on falling gasoline demand published March 23. 2 This appears to be happening now, as pipeline operators ask shippers to reduce the rate at which they fill the lines. Please see Pipelines ask U.S. drillers to slow output as storage capacity dwindles published by worldoil.com March 30, 2020. 3 Prominently among the GCC states, KSA cuts public spending 5% and introduced fiscal measures meant to cushion the blow of the COVID-19 shock and to offset the low prices resulting from its market-share war with Russia. Please see Saudi Arabia announces $32 billion in emergency funds to mitigate oil, coronavirus impact published by cnbc.com March 20, 2020. 4 Please see the Joint Statement by the Chair of International Monetary and Financial Committee and the Managing Director of the International Monetary Fund issued by International Monetary and Financial Committee Chair Lesetja Kganyago and International Monetary Fund Managing Director Kristalina Georgieva March 27, 2020. 5 Please see Daniel Yergin’s The Prize: The Epic Quest for Oil, Money & Power, published by Simon & Schuster in 1990, particularly Chapter 2 for a discussion of Rockefeller’s “good sweating,” in which competitors were driven out of business by low prices engineered by Rockefeller if they refused to sell out to Standard Oil. 6 The tone of remarks from TRR Chairman Wayne Christian has become more agreeable to having the TRR Commission return to pro-rating oil production in the Lone Star state. His recent editorial for worldoil.com notes, “Any action taken by Texas must be done in lockstep with other oil producing states and nations, ensuring that they cut production at similar times and in similar amounts.” Please see Christian’s editorial, Texas RRC Chairman Wayne Christian: We must stabilize worldwide oil markets, published by worldoil.com March 25, 2020.

Highlights The pandemic has a negative impact on households and has not peaked in the US. But a depression is likely to be averted. Our market-based geopolitical risk indicators point toward a period of rising political turbulence across the world. We are selectively adding risk to our strategic portfolio, but remain tactically defensive. Stay long gold on a strategic time horizon. Feature I'm going where there's no depression, To the lovely land that's free from care. I'll leave this world of toil and trouble My home's in Heaven, I'm going there. - “No Depression In Heaven,” The Carter Family (1936) Chart 1The Pandemic Stimulus Versus The Great Recession Stimulus

GeoRisk Update: No Depression

GeoRisk Update: No Depression

Markets bounced this week on the back of a gargantuan rollout of government spending that is the long-awaited counterpart to the already ultra-dovish monetary policy of global central banks (Chart 1). Just when the investment community began to worry about a full-fledged economic depression and the prospect for bank runs, food shortages, and martial law in the United States, the market rallied. Yet extreme uncertainty persists over how long one third of the world’s population will remain hidden away in their homes for fear of a dangerous virus (Chart 2). Chart 2Crisis Has Not Verifiably Peaked, Uncertainty Over Timing Of Lockdowns

GeoRisk Update: No Depression

GeoRisk Update: No Depression

Chart 3The Pandemic Shock To The Labor Market

The Pandemic Shock To The Labor Market

The Pandemic Shock To The Labor Market

While an important and growing trickle of expert opinion suggests that COVID-19 is not as deadly as once thought, especially for those under the age of 50, consumer activity will not return to normal anytime soon.1 Moreover political and geopolitical risks are skyrocketing and have yet to register in investors’ psyche. Consider: American initial unemployment claims came in at a record-breaking 3.3 million (Chart 3), while China International Capital Corporation estimates that China’s GDP will grow by 2.6% for the year. These are powerful blows against global political as well as economic stability. This should convince investors to exercise caution even as they re-enter the equity market. We are selectively putting some cash to work on a strategic time frame (12 months and beyond) to take advantage of some extraordinary opportunities in equities and commodities. But we maintain the cautious and defensive tactical posture that we initiated on January 24. No Depression In Heaven The US Congress agreed with the White House on an eye-popping $2.2 trillion or 10% of GDP fiscal stimulus. At least 46% of the package consists of direct funds for households and small businesses (Chart 4). This includes $290 billion in direct cash handouts to every middle-class household – essentially “helicopter money,” as it is financed by bonds purchased by the central bank (Table 1). The purpose is to plug the gap left by the near complete halt to daily life and business as isolation measures are taken. A depression is averted, but we still have a recession. Go long consumer staples. Chart 4The US Stimulus Package Breakdown

GeoRisk Update: No Depression

GeoRisk Update: No Depression

Table 1Distribution Of Cash Handouts Under US Coronavirus Response Act

GeoRisk Update: No Depression

GeoRisk Update: No Depression

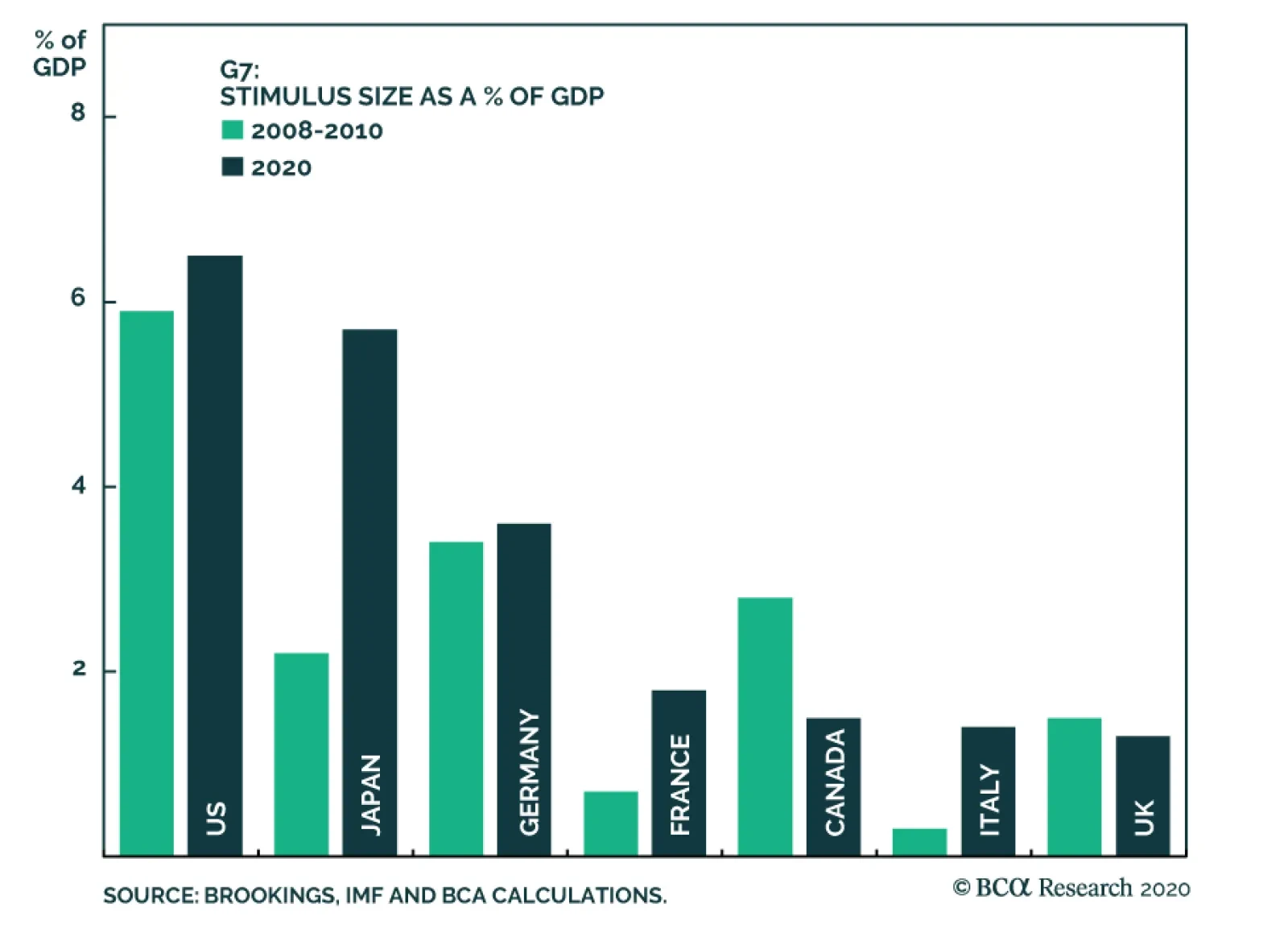

China, the origin of the virus that triggered the global pandemic and recession, is resorting to its time-tried playbook of infrastructure spending, with 3% of GDP in new spending projected. This number is probably heavily understated. It does not include the increase in new credit that will accompany official fiscal measures, which could easily amount to 3% of GDP or more, putting the total new spending at 6%. Germany and the EU have also launched a total fiscal response. The traditionally tight-fisted Berlin has launched an 11% of GDP stimulus, opening the way for other member states to surge their own spending. The EU Commission has announced it will suspend deficit restrictions for all member states. The ECB’s Pandemic Emergency Purchase Program (PEPP) enables direct lending without having to tap the European Stability Mechanism (ESM) or negotiate the loosening of its requirements. It also enables the ECB to bypass the debate over issuing Eurobonds (though incidentally Germany is softening its stance on the latter idea). The cumulative impact of all this fiscal stimulus is 5% of global GDP – and rising (Table 2). Governments will be forced to provide more cash on a rolling basis to households and businesses as long as the pandemic is raging and isolation measures are in place. Table 2The Global Fiscal Stimulus In Response To COVID-19

GeoRisk Update: No Depression

GeoRisk Update: No Depression

President Trump has signaled that he wants economic life to begin resuming after Easter Sunday, April 12. But he also said that he will listen to the advice of the White House’s public health advisors. State governors are the ones who implement tough “shelter in place” orders and other restrictions, so the hardest hit states will not resume activity until their governors believe that the impact on their medical systems can be managed. Authorities will likely extend the social distancing measures in April until they have a better handle on the best ways to enable economic activity while preserving the health system. Needless to say, economic activity will have to resume gradually as the government cannot replace activity forever and the working age population can operate even with the threat of contracting the disease (social distancing policies would become more fine-tuned for types of activity, age groups, and health risk profiles). The tipping point from recession to depression would be the point at which the government’s promises of total fiscal and monetary support for households and businesses become incapable of reassuring either the financial markets or citizens. The largest deficit the US government has ever run was 30% of GDP during World War II (Chart 5). Today’s deficit is likely to go well beyond 15% (5% existing plus 10% stimulus package plus falling revenue). If authorities were forced to triple the lockdown period and hence the fiscal response the country would be in uncharted territory. But this is unlikely as the incubation period of the virus is two weeks and China has already shown that a total lockdown can sharply reduce transmission. Chart 5The US's Largest Peacetime Budget Deficit

The US's Largest Peacetime Budget Deficit

The US's Largest Peacetime Budget Deficit

Any tipping point into depression would become evident in behavior: e.g. a return to panic selling, followed by the closure of financial market trading by authorities, bank runs, shortages of staples across regions, and possibly the use of martial law and curfews. While near-term selloffs can occur, the rest seems very unlikely – if only because, again, the much simpler solution is to reduce the restrictions on economic activity gradually for the low-risk, healthy, working age population. Bottom Line: Granting that the healthy working age population can and will eventually return to work due to its lower risk profile, unlimited policy support suggests that a depression or “L-shaped” recovery is unlikely. The Dark Hour Of Midnight Nearing While the US looks to avoid a depression, there will still be a recession with an unprecedented Q2 contraction. The recovery could be a lot slower than bullish investors expect. Global manufacturing was contracting well before households got hit with a sickness that will suppress consumption for the rest of the year. There is another disease to worry about: the dollar disease. The world is heavily indebted and holds $12 trillion in US dollar-denominated debt. Yet the dollar is hitting the highest levels in years and global dollar liquidity is drying up. The greenback has rallied even against major safe haven currencies like the Japanese yen and Swiss franc (Chart 6). Of course, the Fed is intervening to ensure highly indebted US corporates have access to loans and extending emergency dollar swap lines to a total of 14 central banks. But in the near term global growth is collapsing and the dollar is overshooting. This can create a self-reinforcing dynamic. The same goes for any relapse in Chinese growth. Unlike in 2008 – but like 2015 – China is the epicenter of the global slowdown. China has much larger economic and financial imbalances today than it did in 2003 when the SARS outbreak occurred, and it will increase these imbalances going forward as it abandons its attempt to deleverage the corporate sector (Chart 7). Chart 6The Greenback Surge Deprives The World Of Liquidity

The Greenback Surge Deprives The World Of Liquidity

The Greenback Surge Deprives The World Of Liquidity

Chart 7China's Financial Imbalances Are A Worry

China's Financial Imbalances Are A Worry

China's Financial Imbalances Are A Worry

The rest of emerging markets face their own problems, including poor governance and productivity, as well as the dollar disease and the China fallout. They are unlikely to lift themselves out of this crisis, but they could become the source for credit events and market riots that prolong the global risk-off phase. Bottom Line: It is too soon to sound the all-clear. If the dollar continues on its rampage, then the gigantic stimulus will not be enough, markets will relapse, and fears of deflation will grow. World Of Toil And Trouble Political risk is the next shoe to drop. The pandemic and recession are setting in motion a political earthquake that will unfold over the next decade. Almost all of our 12 market-based geopolitical risk indicators have exploded upward since the beginning of the year. Chart 8China's Political Risk Is Rising

China's Political Risk Is Rising

China's Political Risk Is Rising

These indicators show that developed market equities and emerging market currencies are collapsing far more than is justified by underlying fundamentals. This risk premium reflects the uncertainty of the pandemic, but the recession will destabilize regimes and fuel fears about national security. So the risk premium will not immediately decline in several important cases. China’s political risk is shooting up, as one would expect given that the pandemic began in Hubei (Chart 8). The stress within the Communist Party can be measured by the shrill tone of the Chinese propaganda machine, which is firing on all cylinders to convince the world that Chinese President Xi Jinping did a great job handling the virus while the western nations are failing states that cannot handle it. The western nations are indeed mishandling it, but that does not solve China’s domestic economic and social troubles, which will grow from here. Of course, our political risk indicator will fall if Chinese equities rally more enthusiastically than Chinese state banks expand credit as the economy normalizes. But this would suggest that markets have gotten ahead of themselves. By contrast, if China surges credit, yet equity investors are unenthusiastic, then the market will be correctly responding to the fact that a credit surge will increase economic imbalances and intensify the tug-of-war between authorities and the financial system, particularly over the effort to prevent the property sector bubble from ballooning. China needs to stimulate to recover from the downturn. Obviously it does not want instability for the 100th birthday of the Communist Party in 2021. An even more important reason for stimulus is the 2022 leadership reshuffle – the twentieth National Party Congress. This is the date when Xi Jinping would originally have stepped down and the leading member of the rival faction (Hu Chunhua?) would have taken over the party, the presidency, and the military commission. Today Xi is not at risk of losing power, but with a trade war and recession to his name, he will have to work hard to tighten control over the party and secure his ability to stay in power. An ongoing domestic political crackdown will frighten local governments and private businesses, who are already scarred by the past decade and whose animal spirits are important to the overall economic rebound. It is still possible that Beijing will have to depreciate the renminbi against the dollar. This is the linchpin of the trade deal with President Trump – especially since other aspects of the deal will be set back by the recession. As long as Trump’s approval rating continues to benefit from his crisis response and stimulus deals, he is more likely to cut tariffs on China than to reignite the trade war. This approach will be reinforced by the bump in his approval rating upon signing the $2 trillion Families First Coronavirus Response Act into law (Chart 9). He will try to salvage the economy and his displays of strength will be reserved for market-irrelevant players like Venezuela. But if the virus outbreak and the surge in unemployment turn him into a “lame duck” later this year, then he may adopt aggressive trade policy and seek the domestic political upside of confronting China. He may need to look tough on trade on the campaign trail. Diplomacy with North Korea could also break down. This is not our base case, but we note that investors are pricing crisis levels into the South Korean won despite its successful handling of the coronavirus (Chart 10). Pyongyang has an incentive to play nice to assist the government in the South while avoiding antagonizing President Trump. But Kim Jong Un may also feel that he has an opportunity to demonstrate strength. This would be relevant not because of North Korea’s bad behavior but because a lame duck President Trump could respond belligerently. Chart 9Trump’s Approval Gets Bump From Crisis Response And Stimulus

GeoRisk Update: No Depression

GeoRisk Update: No Depression

Chart 10South Korean Political Risk Rising

South Korean Political Risk Rising

South Korean Political Risk Rising

We highlighted Russia as a “black swan” candidate for 2020. This view stemmed from President Vladimir Putin’s domestic machinations to stay in power and tamp down on domestic instability in the wake of domestic economic austerity policies. For the same reason we did not expect Moscow to engage in a market share war with Saudi Arabia that devastated oil prices, the Russian ruble, and economy. At any rate, Russia will remain a source of political surprises going forward (Chart 11). Go long oil. Putin cannot add an oil collapse to a plague and recession and expect a popular referendum to keep him in power till 2036. The coronavirus is hitting Russia, forcing Putin to delay the April 22 nationwide referendum that would allow him to rule until 2036. It is also likely forcing a rethink on a budget-busting oil market share war, since more than the $4 billion anti-crisis fund (0.2% of GDP) will be needed to stimulate the economy and boost the health system. Russia faces a budget shortfall of 3 trillion rubles ($39 billion) this year from the oil price collapse. It is no good compounding the economic shock if one intends to hold a popular referendum – even if one is Putin. For all these reasons we agree with BCA Research Commodity & Energy Strategy that a return to negotiations is likely sooner rather than later. Chart 11Russia: A Lake Of Black Swans

Russia: A Lake Of Black Swans

Russia: A Lake Of Black Swans

However, we would not recommend buying the ruble, as tensions with the US are set to escalate. Instead we recommend going long Brent crude oil. Political risk in the European states is hitting highs unseen since the peak of the European sovereign debt crisis (Chart 12). Some of this risk will subside as the European authorities did not delay this time around in instituting dramatic emergency measures. Chart 12Europe: No Delay In Offering 'Whatever It Takes'

Europe: No Delay In Offering 'Whatever It Takes'

Europe: No Delay In Offering 'Whatever It Takes'

Chart 13Political Risk Understated In Taiwan And Turkey

Political Risk Understated In Taiwan And Turkey

Political Risk Understated In Taiwan And Turkey

However, we do not expect political risk to fall back to the low levels seen at the end of last year because the recession will affect important elections between now and 2022 in Italy, the Netherlands, Germany, and France. Only the UK has the advantage of a single-party parliamentary majority with a five-year term in office – this implies policy coherence, notwithstanding the fact that Prime Minister Boris Johnson has contracted the coronavirus. The revolution in German and EU fiscal policy is an essential step in cementing the peripheral countries’ adherence to the monetary union over the long run. But it may not prevent a clash in the coming years between Italy and Germany and Brussels. Italy is one of the countries most likely to see a change in government as a result of the pandemic. It is hard to see voters rewarding this government, ultimately, for its handling of the crisis, even though at the moment popular opinion is tentatively having that effect. The Italian opposition consists of the most popular party, the right-wing League, and the party with the fastest rising popular support, which is the right-wing Brothers of Italy. So the likely anti-incumbent effect stemming from large unemployment would favor the rise of an anti-establishment government over the next year or two. The result would be a clash with Brussels even in the context of Brussels taking on a more permissive attitude toward budget deficits. This will be all the worse if Brussels tries to climb down from stimulus too abruptly. Our political risk indicators have fallen for two countries over the past month: Taiwan and Turkey (Chart 13). This is not because political risk is falling in reality, but because these two markets have not seen their currencies depreciate as much as one would expect relative to underlying drivers of their economy: In Taiwan’s case the reason is the US dollar’s unusual strength relative to the Japanese yen amidst the crisis. Ultimately the yen is a safe-haven currency and it will eventually strengthen if global growth continues to weaken. Moreover we continue to believe that real world politics will lead to a higher risk premium in the Taiwanese dollar and equities. Taiwan faces conflicts with mainland China that will increase with China’s recession and domestic instability. In Turkey’s case, the Turkish lira has depreciated but not as much as one would expect relative to European equities, which have utterly collapsed. Therefore Turkey’s risk indicator shows its domestic political risk falling rather than rising. Turkey’s populist mismanagement will ensure that the lira continues depreciating after European equities recover, and then our risk indicator will shoot up. Chart 14Brazilian Political Risk Is No Longer Contained

Brazilian Political Risk Is No Longer Contained

Brazilian Political Risk Is No Longer Contained

Prior to the pandemic, Brazilian political risk had remained contained, despite Brazilian President Jair Bolsonaro’s extreme and unorthodox leadership. Since the outbreak, however, this indicator has skyrocketed as the currency has collapsed (Chart 14). To make matters worse, Bolsonaro is taking a page from President Trump and diminishing the danger of the coronavirus in his public comments to try to prevent a sharp economic slowdown. This lackadaisical attitude will backfire since, unlike the US, Brazil does not have anywhere near the capacity to manage a major outbreak, as government ministers have warned. This autumn’s local elections present an opportunity for the opposition to stage a comeback. Brazilian stocks won’t be driven by politics in the near term – the effectiveness of China’s stimulus is critical for Brazil and other emerging markets – but political risk will remain elevated for the foreseeable future. Bottom Line: Geopolitical risk is exploding everywhere. This marks the beginning of a period of political turbulence for most of the major nation-states. Domestic economic stresses can be dealt with in various ways but in the event that China’s instability conflicts with President Trump’s election, the result could be a historic geopolitical incident and more downside in equity markets. In Russia’s case this has already occurred, via the oil shock’s effect on US shale producers, so there is potential for relations to heat up – and that is even more true if Joe Biden wins the presidency and initiates Democratic Party revenge for Russian election meddling. The confluence of volatile political elements informs our cautious tactical positioning. Investment Conclusions If the historic, worldwide monetary and fiscal stimulus taking place today is successful in rebooting global growth, then there will be “no depression.” The world will learn to cope with COVID-19 while the “dollar disease” will subside on the back of massive injections of liquidity from central banks and governments. Gold: The above is ultimately inflationary and therefore our strategic long gold trade will be reinforced. The geopolitical instability we expect to emerge from the pandemic and recession will add to the demand for gold in such a reflationary environment. No depression means stay long gold! US Equities: Equities will ultimately outperform government bonds in this environment as well. Our chief US equity strategist Anastasios Avgeriou has tallied up the reasons to go long US stocks in an excellent recent report, “20 Reasons To Buy Equities.” We agree with this view assuming investors are thinking in terms of 12 months and beyond. Chart 15Oil/Gold Ratio Extreme But Wait To Go Long

Oil/Gold Ratio Extreme But Wait To Go Long

Oil/Gold Ratio Extreme But Wait To Go Long

Tactically, however, we maintain the cautious positioning that we adopted on January 24. We have misgivings about the past week’s equity rally. Investors need a clear sense of when the US and European households will start resuming activity. The COVID-19 outbreak is still capable of bringing negative surprises, extending lockdowns, and frightening consumers. Hence we recommend defensive plays that have suffered from indiscriminate selling, rather than cyclical sectors. Go tactically long S&P consumer staples. US Bonds: Over the long run, the Fed’s decision to backstop investment grade corporate bonds also presents a major opportunity to go long on a strategic basis relative to long-dated Treasuries, following our US bond strategists. Global Equities: We prefer global ex-US equities on the basis of relative valuations and US election uncertainty. Shifting policy winds in the United States favor higher taxes and regulation in the coming years. This is true unless President Trump is reelected, which we assess as a 35% chance. Emerging Markets: We are booking gains on our short TRY-USD trade for a gain of 6%. This is a tactical trade that remains fundamentally supported. Book 6% gain on short TRY-USD. Oil: For a more contrarian trade, we recommend going long oil. Our tactical long oil / short gold trade was stopped out at 5% last week. While we expect mean reversion in this relationship, the basis for gold to rally is strong. Therefore we are going long Brent crude spot prices on Russia’s and Saudi Arabia’s political constraints and global stimulus (Chart 15). We will reconsider the oil/gold ratio at a later date. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 See Joseph T. Wu et al, "Estimating clinical severity of COVID-19 from the transmission dynamics in Wuhan, China," Nature Medicine, March 19, 2020, and Wei-jie Guan et al, "Clinical Characteristics of Coronavirus Disease 2019 in China," The New England Journal Of Medicine, February 28, 2020. Section II: Appendix : GeoRisk Indicator China

China: GeoRisk Indicator

China: GeoRisk Indicator

Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

UK

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Canada

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Taiwan

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Section III: Geopolitical Calendar

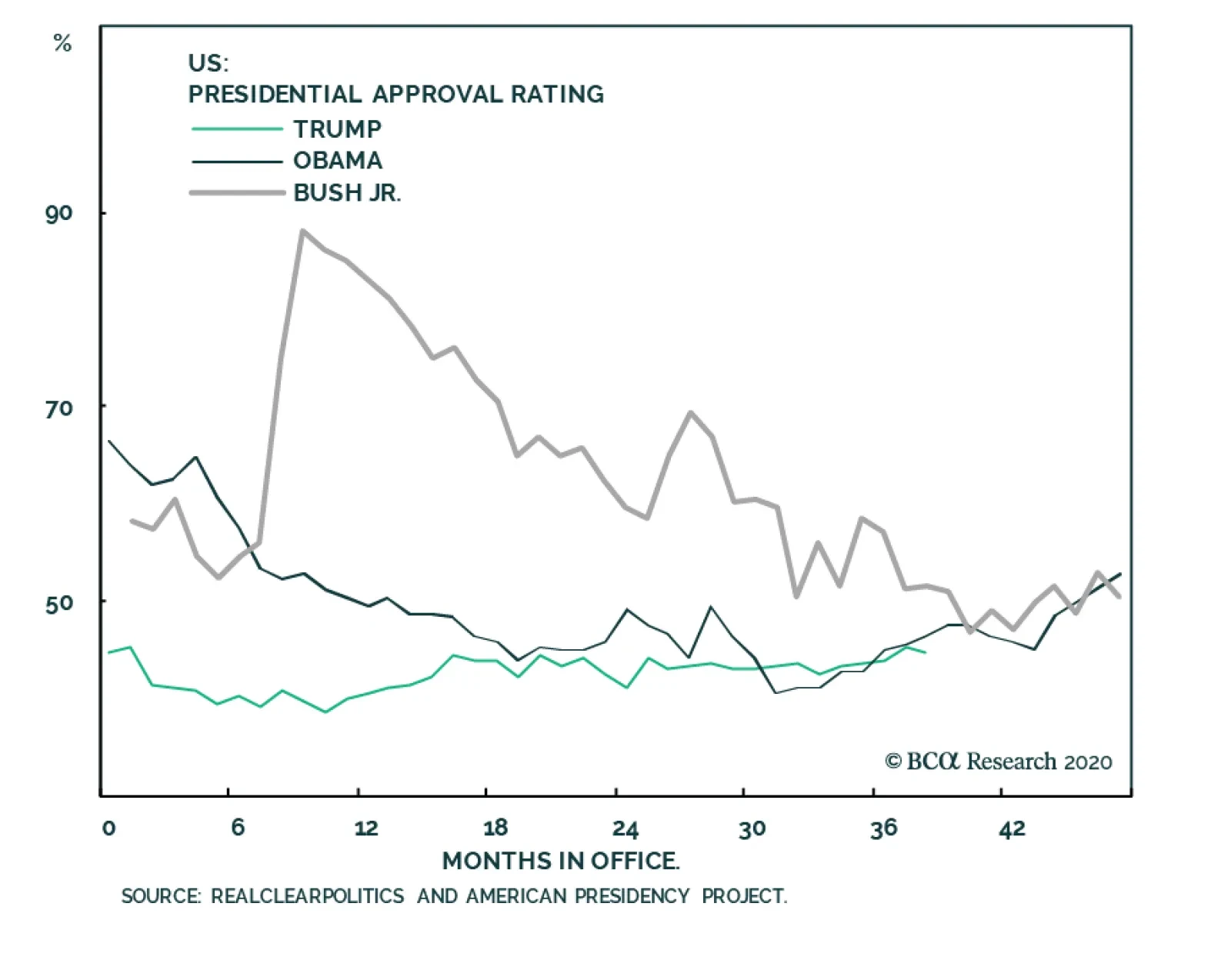

US President Trump’s approval rating has fallen amid the pandemic. It is now deviating from that of President Obama in 2012. Our Geopolitical Strategy argues that Trump is no longer favored to win reelection. Trump apparently believes he can still salvage…

Feature We are downgrading US President Donald Trump’s odds of winning election. We now consider him an underdog. Since November 2018 we had given Trump a 55% chance of victory – and when former Vice President Joe Biden clinched the nomination in the midst of the virus crisis we argued that the election was “too close to call.” Now, subjectively, we would say Trump has a 35% chance of winning. This is generous relative to history, but seems appropriate to us due to the unpredictable nature of the coronavirus pandemic (which could claim either presidential candidate), the massive US and global stimulus, and the weakness of his opponent. Trump’s approval rating has fallen, albeit slightly, amid the coronavirus pandemic (Chart 1). It is now deviating from the rising approval rating of President Barack Obama at this stage in the 2012 election cycle. Since Trump has been generally less popular than the average president (Chart 2), including Obama, this is a very worrying sign for Trump. Chart 1Virus Knocked Trump Off Track

Downgrading Trump's Odds Of Reelection

Downgrading Trump's Odds Of Reelection

Chart 2Trump Has Zero Buffer For Loss Of Popularity

Downgrading Trump's Odds Of Reelection

Downgrading Trump's Odds Of Reelection

It is also a worrying sign for global risk assets despite their recent collapse. Chart 3To Boost Economy, Trump Must Allow Outbreaks

To Boost Economy, Trump Must Allow Outbreaks

To Boost Economy, Trump Must Allow Outbreaks